Khosrork

Specialty performance ingredients and food manufacturer Balchem Corporation (NASDAQ:BCPC) offers a considerable number of products in very different markets and regions. The company is well-diversified, and expects to grow through innovation and acquisitions. In my view, if its recent acquisitions are successful, there will be stock demand, which may bring the stock price up. Even considering potential risks from inflation in raw materials and detrimental publicity, Balchem Corporation appears significantly undervalued at its current market price.

Balchem’s Business Model

For more than 50 years, Balchem Corporation has offered solutions for human and animal health through its technologies and services. With a current estimated employee base of 1,400 people spread between its main location in New Jersey and its other facilities and offices throughout the United States and Europe, Balchem Corporation’s business model is divided into three broad categories: Nutrition and Human Health, Animal Nutrition and Health, and special products segment, among which gas packaging and food nutrition stand out.

As far as the human health and nutrition segment is concerned, the company mainly produces and develops amino acids and choline. The latter plays a critical role in the brain cell reproduction, child development and fertility, memory, and muscle health. This segment is accompanied by large investments in the area of research, including synthesized foods, production of energy cereal bars, and different daily supplements for everyday health. The company declares that it is conducting long-term research in order to generate a notable difference in the value of its products in relation to its competitors.

Just as the consumption of daily supplements has grown remarkably in recent years, the same is the case for the market for animal feed. This business segment is mainly dedicated to the production of microcapsules for animal consumption, either to increase fat metabolism or to strengthen the milk generation process in cows. The products in this segment are mainly destined for the pet, swine, and poultry markets, thus demonstrating the variety of applications and the diversification in the consumption of these supplements.

In relation to its specialized products, we find the production of ethylene oxide. This is a sterilizing chemical primarily traded in the body health arena. The manufacture of this type of chemical also includes packaging in compliance with certain quality standards for global transportation. In this segment, the company also works with gases, aimed at different industries and the synthesis of minerals for plant nutrition, with active operations in the field of agriculture.

The company’s products are being permanently updated, looking for improvements and lowering costs through their research area, since their competitors, even if they are small or large corporations, have in many cases financial development on a larger scale. Much of the competition in this sense goes through the acceptance and consumption of its products by the contracting industries, being the nutrition and human health market the most compromised, since its competitors are large companies positioned globally.

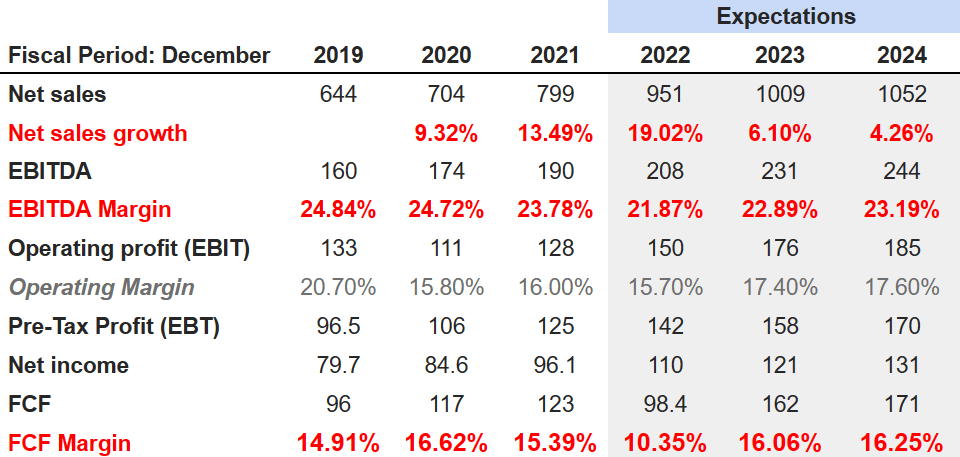

Market Expectations Include Net Sales Growth Around 19%-4%, EBITDA Margin Of 21%-23%, And FCF Margin Close To 10%-16%

I believe that analysts are expecting beneficial numbers for the years 2023 and 2024, which include growing EBITDA margins and sales growth. 2024 net revenue would stand at $1 billion, with sales growth of 4% and an EBITDA margin of 23%. Finally, with 2024 net income around $131 million and free cash flow (“FCF”) of $171 million, the FCF margin would stand at 16.25%.

Source: marketscreener.com

Balance Sheet

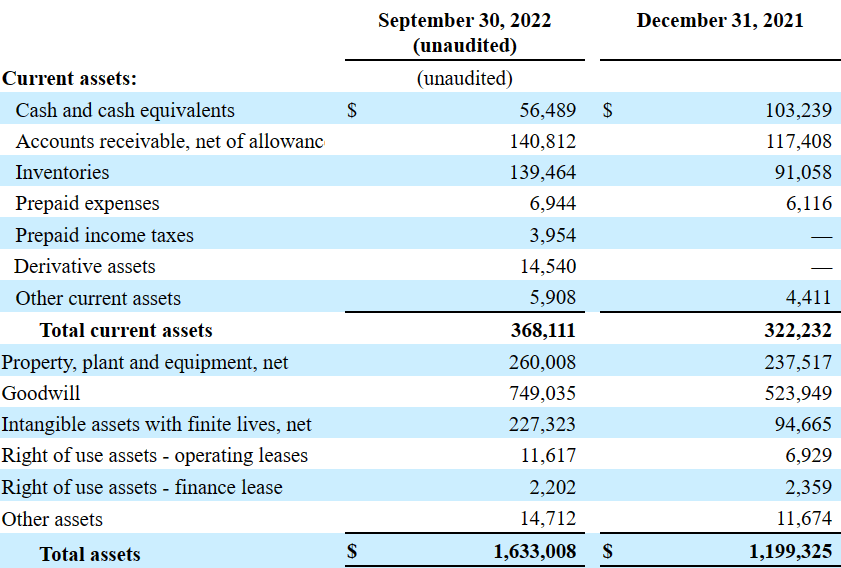

As of September 30, 2022, Balchem reported $56 million in cash, accounts receivable of $140 million, and total current assets of $368 million. The current assets/current liabilities ratio stands at 2x, which indicates that liquidity doesn’t seem an issue here.

The list of assets include property worth $260 million, goodwill of $749 million, and intangible assets worth $227 million. The total amount of assets is equal to $1.6 billion.

Source: 10-Q

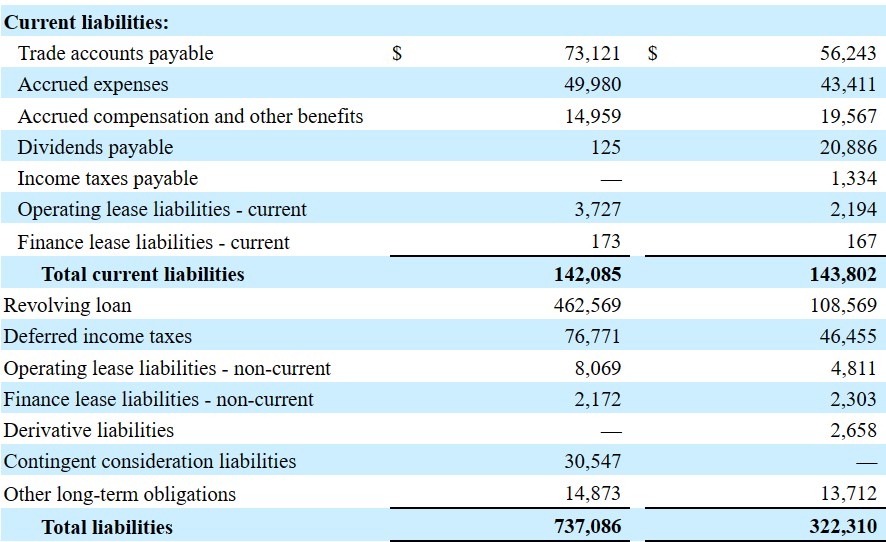

Among the liabilities, the most remarkable are the revolving loan worth $462 million and deferred income taxes of $76 million. The total liabilities are worth $737 million. I am expecting 2027 EBITDA of close to $302 million, so I am really not concerned about the company’s total amount of debt.

Source: 10-Q

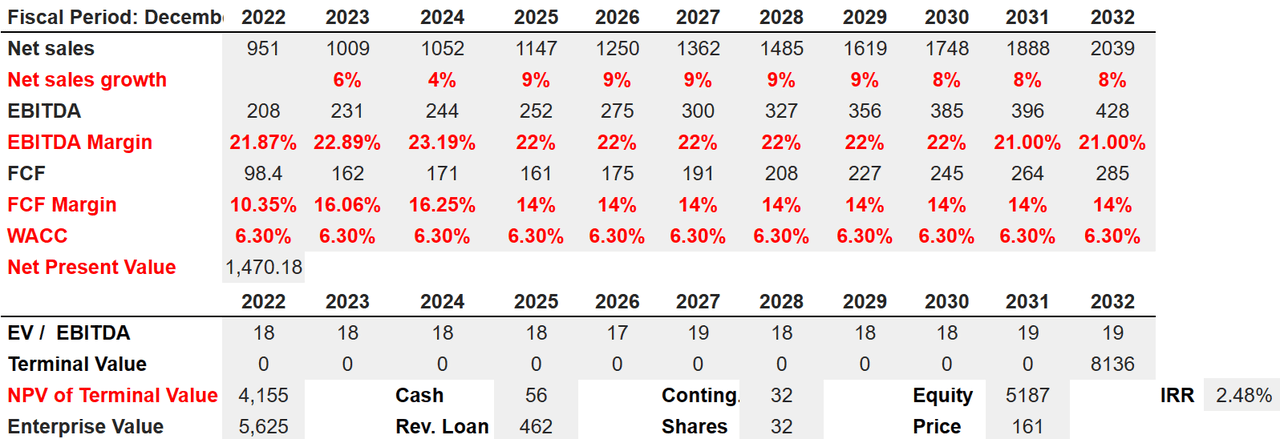

Under My Base Case Scenario, Balchem Is Worth $161 Per Share

Under my base case scenario, I assumed that new innovation will likely create new demand from clients. Besides, healthy margins may bring the attention of more investors, which may create certain stock demand. I would also be expecting that the company’s cash flow from operations will likely be used to reinvest and reduce the total debt outstanding. Management offered some of these promises in the last quarterly report.

Source: Investor Presentation

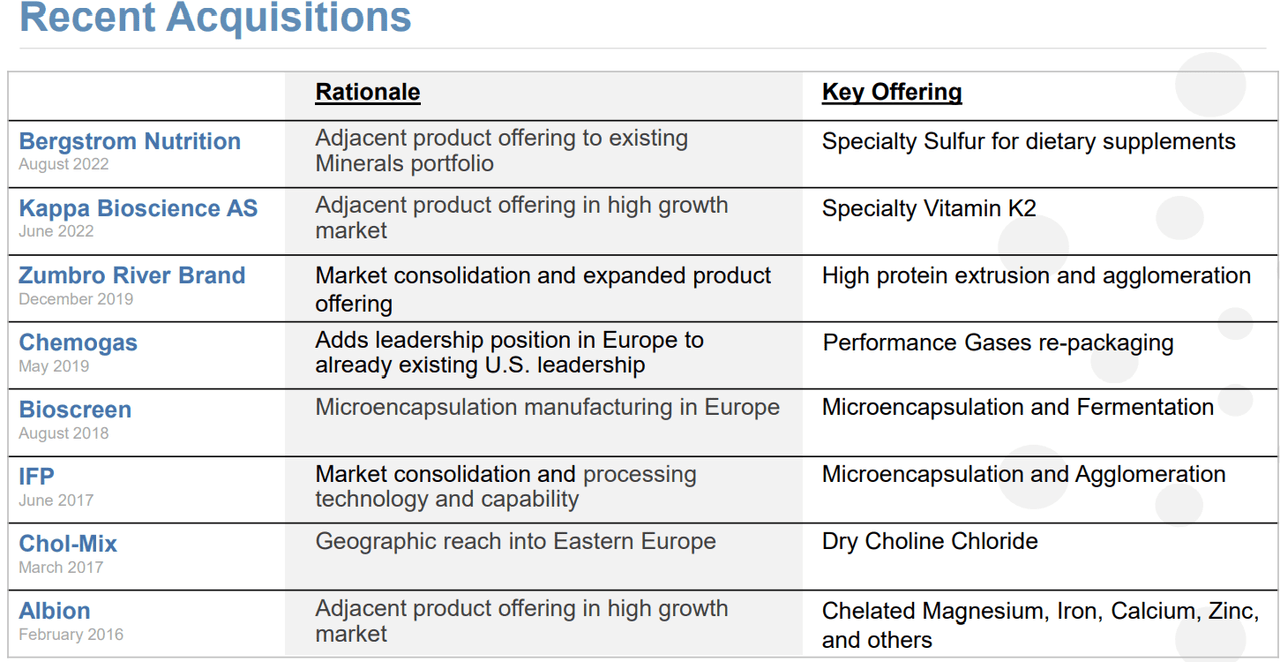

Just as Balchem has its sights set on long-term product development in an increasingly competitive market due to the large number of technical specifications and specific developments for each product, in the same way, it includes the acquisition of other companies as well as the raw materials and intellectual content industry. An example of this is the recent acquisition of Zumbro River Brand as well as Chemogas Holding, which not only allowed the company to expand its client portfolio but also to come into contact with other technological developments in the same field, which is undoubtedly a great benefit to properly allocate funds for future research.

Under this case, I assumed that recent acquisitions will successfully increase revenue growth and the EBITDA margin. Have a look at the number of targets acquired recently. In my view, the company’s M&A operations would most likely bring the attention of certain investors.

Source: Investor Presentation

It is also worth considering the number of patents held by Balchem, which will likely serve as great protection against new competitors or new entrants in the industry.

We currently hold 109 patents in the United States and overseas and use certain trade-names and trademarks. We believe that certain of our patents, in the aggregate, are advantageous to our business. Source: 10-k

Under this scenario, I assumed net sales growth of 6%-8%, 2032 net sales of $2 billion, 2032 EBITDA of $428 million, and an EBITDA margin close to 21%. 2032 free cash flow would stand at $284-$285 million with a FCF margin around 14%. If we assume a WACC of 6.3%, the NPV of future FCF would stand at $1.47 billion. If we include an EV/EBITDA multiple of 19x, the terminal value would stand at $8.1 billion, and the NPV would be $4.15 billion. Finally, I obtained an implied enterprise value of $5.6 billion, equity of $5.18 billion, fair price of $161 per share, and an IRR of 2.48%.

Source: Bersit’s DCF Model

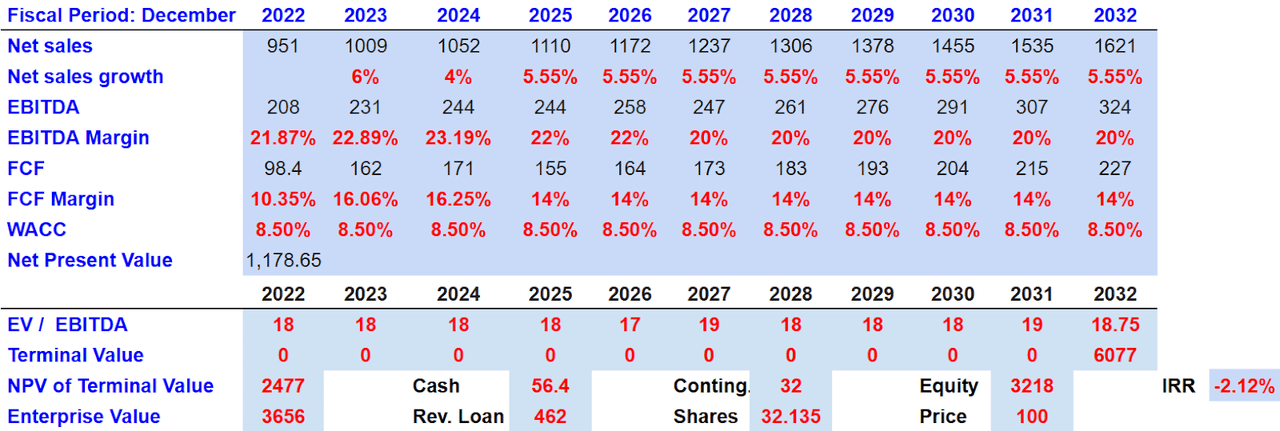

Under Certain Risks, I Obtained A Fair Value Of $100 Per Share

In relation to the risks of Balchem and its business model, in addition to the high competitiveness that it maintains with other companies and corporations, forcing it to improve standards and financial decisions in the short- and long-term, we can add some other factors that directly affect the core of the company’s businesses.

First, the variation in prices of raw materials, as has happened in the last year due to the war situation in Eastern Europe, affects not only the income and expenses of the company but also the ability to foresee budget with certainty. In the same way, variations and changes in its relationships with clients and regulations in both national and regional markets are a constant risk factor in Balchem’s day-to-day activities. In my view, if these risks continue to affect the company’s performance, FCF margins may lower.

On top of this, we can add possible bad publicity from dissatisfied customers as well as legal complications in relation to the quality and consumption of its products, which precisely include delicate health areas that would directly affect the productive capacity and commercial facilities of the company.

Under this scenario, I assumed that Balchem would deliver 2032 net sales of $1.6215 billion, net sales growth of 5.55%, and an EBITDA margin of 20%. 2032 FCF would stand at $227.7 million, and the FCF margin would be 8.5%. Finally, the net present value of the FCF from 2022 to 2032 would be $1.17865 billion.

With an EV/EBITDA of 18.75x, the net present value of the terminal value would be close to $2.5 billion. The enterprise value would be $3.65 billion, and the equity valuation would be $3.2 billion. Finally, I obtained a fair valuation of $100 per share and an IRR of -2.12%.

Source: Bersit’s DCF Model

My Takeaway

Balchem Corporation offers a diversified business model with presence in different continents and extensive experience in the M&A markets. In my opinion, if Balchem Corporation’s recent acquisitions are successful, and new products are added, I would expect revenue and free cash flow generation, which may be used to lower the debt outstanding. Even considering the risks from inflation and potential detrimental publicity about the company’s brand, Balchem Corporation appears quite undervalued.

Be the first to comment