JHVEPhoto

Introduction

Baker Hughes Company (NASDAQ:BKR) released its third quarter 2022 results on October 19, 2022.

Note: This article is an update of my article published on July 27, 2022. I have followed BKR on Seeking Alpha since December 2020.

1 – Third quarter 2022 results snapshot

The company reported third-quarter 2022 adjusted earnings of $0.26 per share, beating analysts’ expectations this quarter. Total quarterly revenues of $5,369 million were below expectations.

Baker Hughes recently rebuilt its organizational structure into two business units from four, one focused on oilfield equipment & services and the other committed to industrial energy & technology.

The solid quarterly earnings were primarily due to higher contributions from the Oilfield Services business segment.

CEO, Lorenzo Simonelli, said in the conference call:

We were generally pleased with our third quarter results with strong performance in OFS, while TPS successfully managed multiple challenges. We also saw strong orders performance with continued momentum in OFE as well as TPS.

Note: I regularly cover three companies in oilfield services. Baker Hughes is my third choice after Schlumberger (SLB) and Halliburton (HAL).

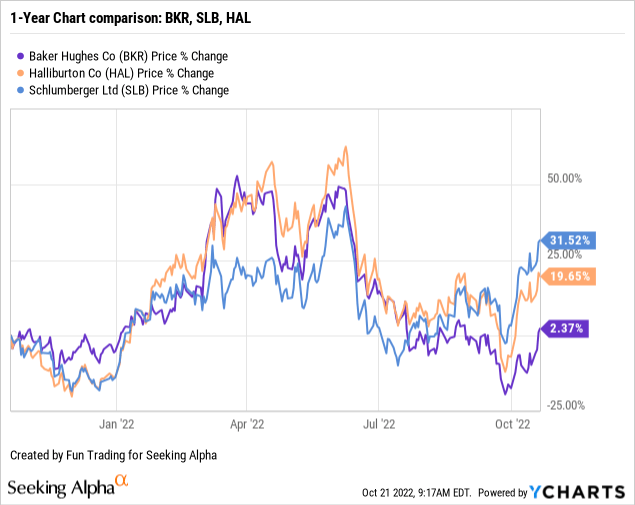

2 – Stock performance

Baker Hughes and its peers have been doing quite well since the start of 2022. However, the sector quickly corrected in June. BKR is up 2% on a one-year basis underperforming its two main competitors significantly.

3 – Investment Thesis

The oilfield-services segment is not the most rewarding in the oil sector. Often late at rebounding and quick to correct on any oil weakness. However, the business outlook turned bullish, and it is perhaps time to look at this segment with an open mind. Three large companies dominate this sector: Schlumberger, Halliburton, and Baker Hughes.

BKR is a decent oilfield-services business that I recommend for a small long-term investment. However, it is not my favorite. It tends to struggle more regarding results and is restructuring and re-segmenting the company into two reporting segments to increase its profitability.

The Restructuring and impairment charges totaled $230 million and produced a net loss of $17 million, or $0.02 per share, in 3Q22.

As I regularly recommend to my subscribers in my marketplace, “The Gold and Oil Corner,” I firmly suggest trading short-term LIFO about 40% of your long-term position to take advantage of the volatility and unforeseen events.

CEO, Lorenzo Simonelli, said in the conference call:

we expect these changes to increase shareholder value and improve the long-term optionality and growth opportunities for Baker Hughes as our markets and customers continue to evolve.

Baker Hughes – The Raw Numbers – Third Quarter of 2022

| Baker Hughes | 3Q21 | 4Q21 | 1Q22 | 2Q22 | 3Q22 |

| Total Orders in $ Billion | 5.38 | 6.66 | 6.84 | 5.86 | 6.06 |

| Total Revenues in $ Billion | 5.09 | 5.52 | 4.84 | 5.05 | 5.37 |

| Net Income available to common shareholders in $ Million | 8 | 293 | 72 | -839 | -17 |

| EBITDA $ Million | 538 | 1,055 | 528 | -321 | 463 |

| EPS diluted in $/share | 0.01 | 0.32 | 0.08 | -0.84 | -0.02 |

| Operating cash flow in $ Million | 416 | 774 | 72 | 321 | 597 |

| CapEx in $ Million | 198 | 266 | 268 | 226 | 180 |

| Free Cash Flow in $ Million | 216 | 508 | -196 | 95 | 417 |

| Total Cash $ Billion | 3.93 | 3.85 | 3.19 | 2.93 | 2.85 |

| Debt Consolidated in $ Billion | 6.76 | 6.73 | 6.69 | 6.66 | 6.66 |

| Dividend per share in $ | 0.18 | 0.18 | 0.18 | 0.18 | 0.18 |

| Shares Outstanding (Diluted) in Million | 857 | 899 | 948 | 1,001 | 1,008 |

Source: Company release

Historical data from 2015 is only available to subscribers.

Analysis: Earnings Details

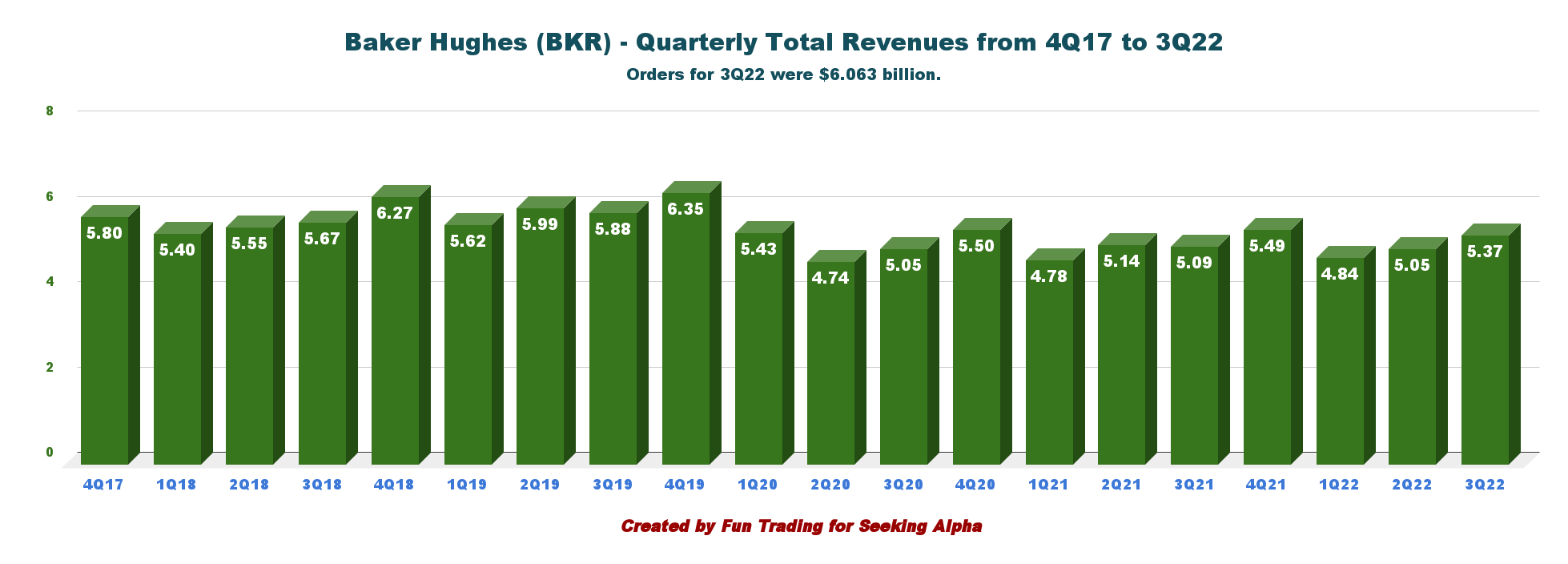

1 – Revenues and other income were $5.37 billion in 3Q22

BKR Quarterly Revenues history (Fun Trading )

BKR’s total orders from all business segments in the third quarter of 2022 were $6,063 million, up 13% yearly. Revenues were $5,047 million this quarter, down 2.1% from the same quarter a year ago and up 6% quarter over quarter.

The increase was due to higher order intakes from Turbomachinery & Process Solutions, Oilfield Equipment, Oilfield Services, and Digital Solutions.

Adjusted operating income was $503 million for the quarter, up 33.8% sequentially and up 25.1% year-over-year.

Adjusted EBITDA was $758 million for the quarter, up 16.4% sequentially and up 14.2% year-over-year.

The company posted total costs and expenses of $5,100 million for the third quarter, up from the same quarter a year ago of $4,715 million.

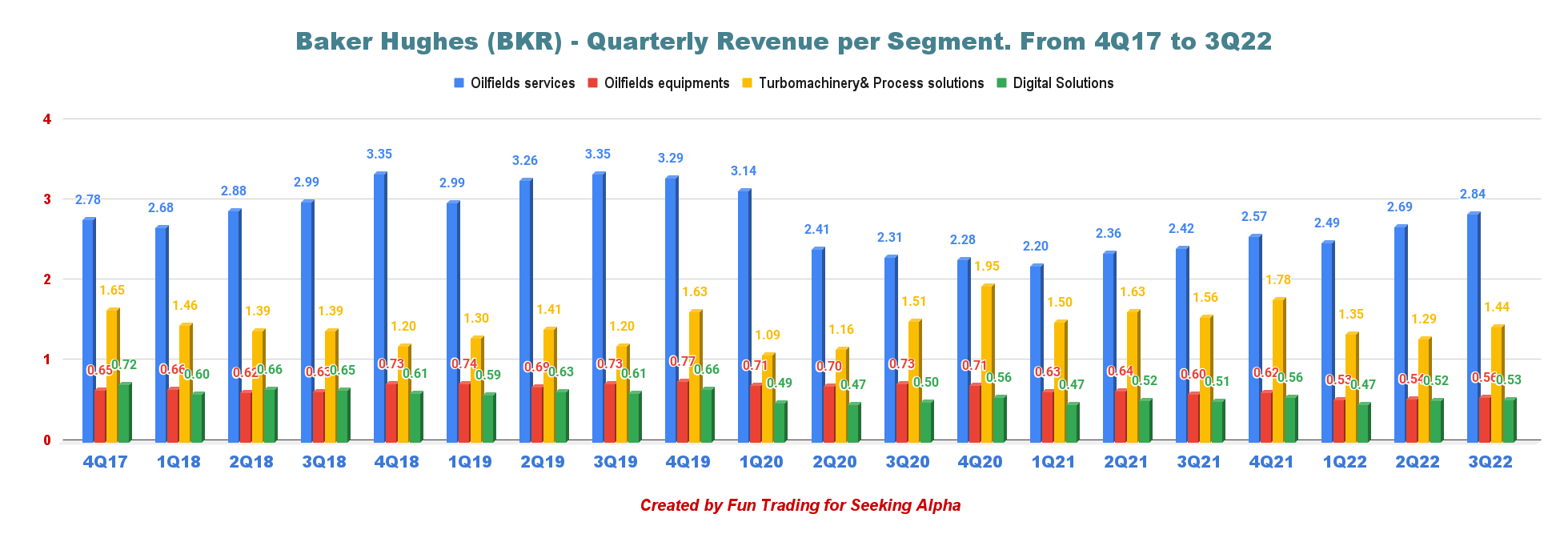

Below are shown revenues per segment history:

BKR Quarterly Revenues per segment history (Fun Trading)

BKR oilfield business segments represented about 63% of its revenue during the quarter through September.

1.1 – Oilfield Services

Revenues were $2,842 million, up 17% from last year of $2,419 million. Operating income from the segment was $330 million, up from $190 million in the third quarter of 2021 due to higher volumes and prices.

1.2 – Oilfield Equipment

Revenues totaled $561 million, down 7% from the last year or $603 million. Lower volumes again hit the company’s Subsea Drilling Systems business and removed the Subsea Drilling services. The segment reported a loss of $6 million from a profit of $14 million in 3Q21. However, better results in Flexibles, Services, and Surface Pressure Control were helping.

1.3 – Turbomachinery & Process Solutions TPS

Higher equipment and service volumes decreased revenues to $1,438 million from $1,562 million a year ago. The segment income fell to $262 million from $278 million in the third quarter of 2021 due to lower service revenues.

1.4 – Digital Solutions

Process & Pipeline Services, Waygate Technologies registered higher volumes. Revenues were $528 million, up from $510 million last year. The segment’s operating profit was $20 million, down 22% from last year’s $26 million. Again, a decline in cost productivity and inflation pressures were to blame for this quarter’s underperformance.

1.5 – 2022 Strategy and outlook

The company expects continued growth through the end of this year and double-digit international expansion in 2023 and will invest in the energy transition and industrial initiatives. The company expects to return 60%-80% of free cash flow to shareholders.

Baker Hughes is restructuring and re-segmenting the company into two reporting segments: Oilfield Services & Equipments OFSE and Industrial & Energy Technology IET.

This change, announced on September 6, 2022, will simplify and streamline the company’s organizational structure with at least $150 million of cost saved and a 25% reduction in the executive management team. This move responds to quickly changing energy markets by improving operational execution.

On October 19, 2022, Baker Hughes announced that it had appointed Nancy Buese as a new CFO. It seeks to reduce costs and boost profit through a reorganization into two business segments indicated above.

Lorenzo Simonelli, Baker Hughes’ Chairman, and CEO said in the conference call:

Looking ahead, we expect continued growth through the end of this year and double-digit international growth in 2023. In North America, pricing across our portfolio remains firm while drilling and completion activity are beginning to level off after significant growth over the last 2 years. Although the U.S. market will be more dynamic and dependent on oil prices, we generally expect solid activity levels through the end of this year with an opportunity for modest growth in 2023 driven by public operators.

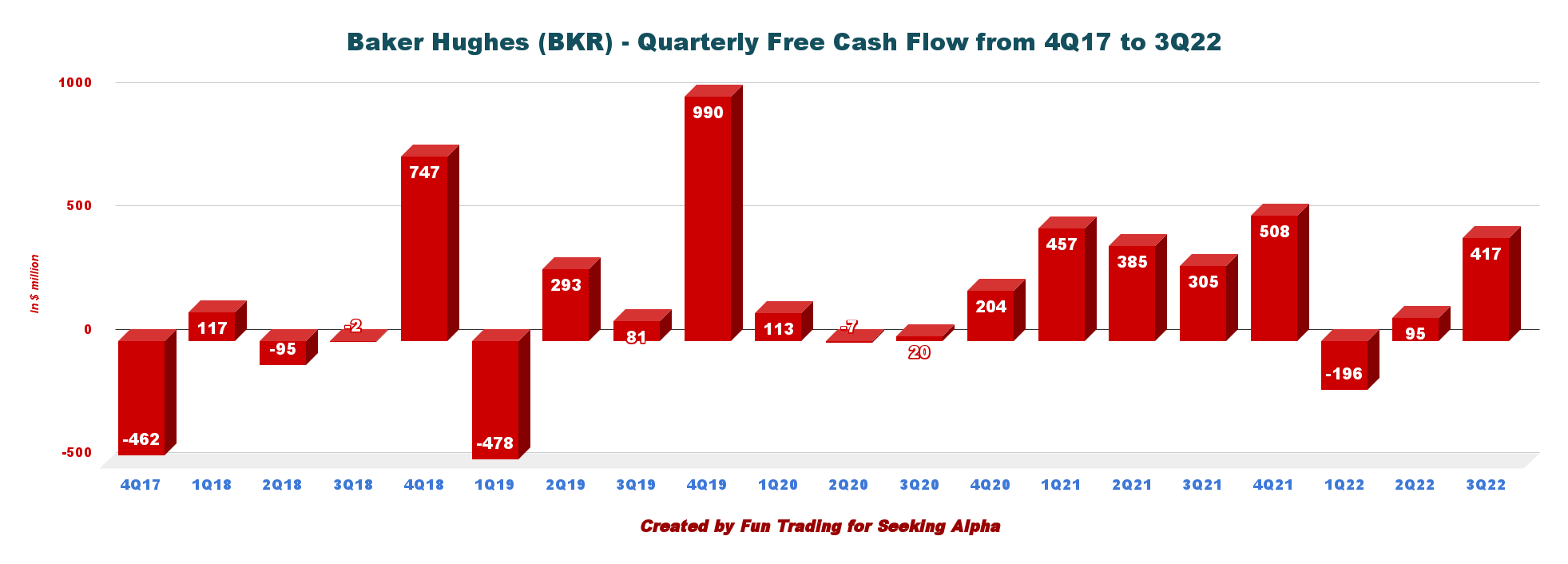

2 – Free cash flow was $417 million in 3Q22

BKR Quarterly Free cash flow history (Fun Trading)

Note: Generic free cash flow is cash flow from operations minus CapEx.

Trailing 12-month free cash flow came in at $824 million, and the company had a free cash flow of Cash million for 3Q22.

This quarter, the quarterly dividend is unchanged at $0.18 per share or an annual cash payment of $726 million. The dividend yield is now 2.7%.

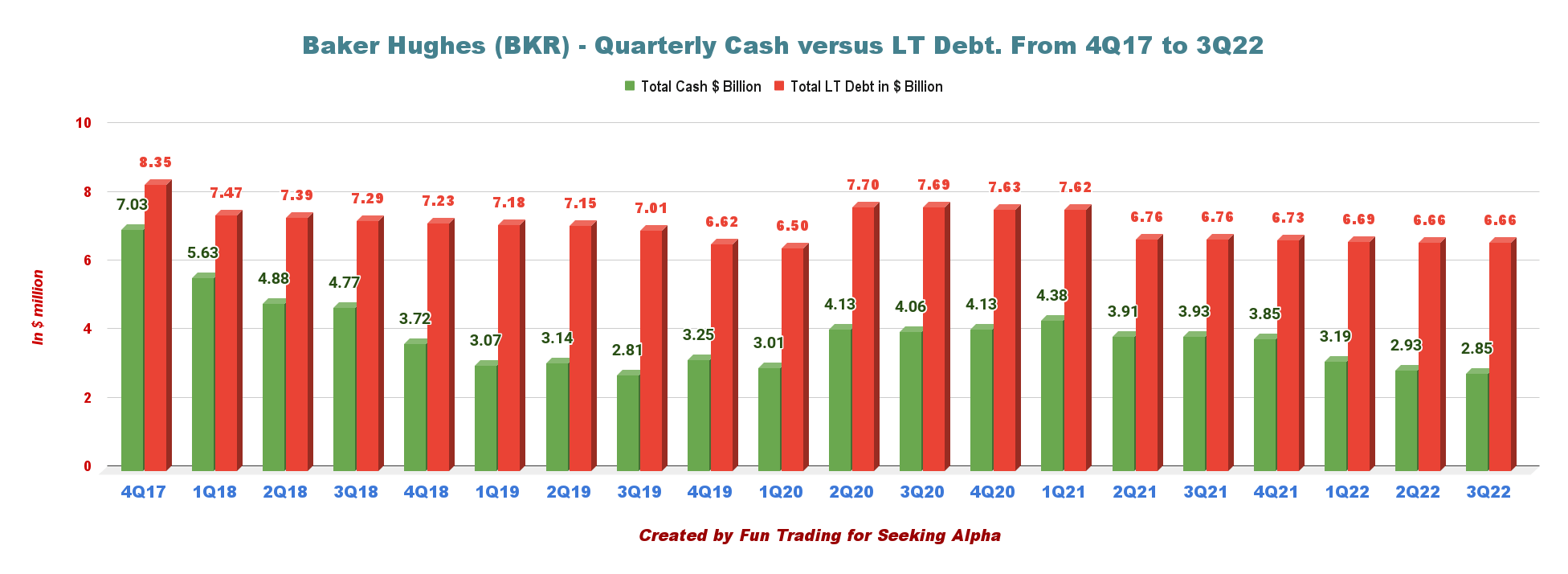

3 – The net debt was $3.80 billion in 3Q22

BKR Quarterly Cash versus debt history (Fun Trading)

As of September 30, 2022, the company had cash and cash equivalents of $2,851 million, down significantly from $3,926 million in the third quarter of 2021.

At the end of the third quarter, Baker Hughes had long-term debt of $6,655 million (including $43 million in current debt), down sequentially from $6,659 million, with a debt to capitalization of 31.7% from 30.6% the preceding quarter (see chart above).

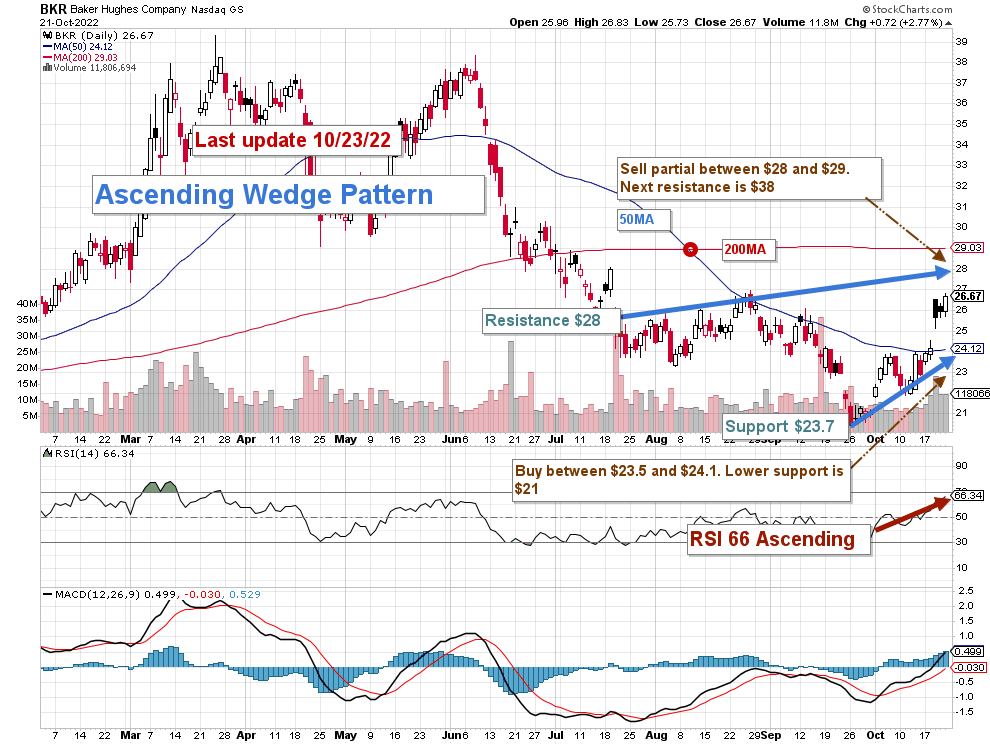

Technical Analysis (short-term) and Commentary

BKR TA Chart Short-term (Fun Trading StockCharts)

Note: The chart includes the effect of the dividend.

BKR forms an ascending wedge pattern with resistance at $28 and support at $23.7. The ascending wedge pattern is a bearish chart pattern that suggests an imminent breakout to the downside.

The general strategy that I usually promote in my marketplace, “The Gold and Oil Corner,” is to keep a core long-term position and use about 30%-40% to trade LIFO while waiting patiently for a higher final price target to sell your core position above $37-$38.

Thus, I recommend selling partially between $28 and $29 (200MA) and waiting for a test at $37 in case of solid momentum to sell again. Conversely, it is reasonable to buy back BKR on any weakness below $24.1 (50MA) with possible lower support at $21.

Note: The LIFO method is prohibited under International Financial Reporting Standards (IFRS), though it is permitted in the United States by Generally Accepted Accounting Principles (GAAP). Therefore, only US traders can apply this method. Those who cannot trade LIFO can use an alternative by setting two different accounts for the same stocks, one for the long term and one for short-term trading.

Warning: The TA chart must be updated frequently to be relevant. It is what I am doing in my stock tracker. The chart above has a possible validity of about a week. Remember, the TA chart is a tool only to help you adopt the right strategy. It is not a way to foresee the future. No one and nothing can.

Author’s note: If you find value in this article and would like to encourage such continued efforts, please click the “Like” button below to vote of support. Thanks.

Be the first to comment