Sundry Photography

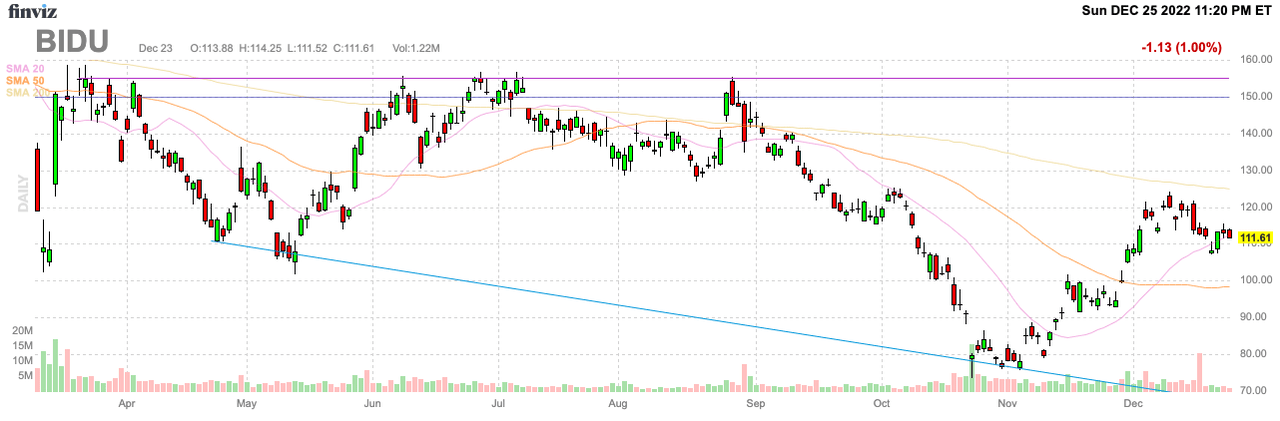

After a few dismal years for Chinese stocks, Baidu (NASDAQ:BIDU) is set up for a much better 2023. The stock has already rallied off the 2022 lows, but the company has far more upside with the reduction of the delisting fears and a rebound in the Chinese economy. My investment thesis remains Bullish on the stock trading some $40 below the 2022 highs, which were already 50% below all-time highs at nearly $340.

Source: FinViz

Return To Growth In 2023

Baidu should be a standard technology company benefitting from secular growth in China. Unfortunately, the internet search company has faced a tough road the last few years with multiple periods where revenues have declined.

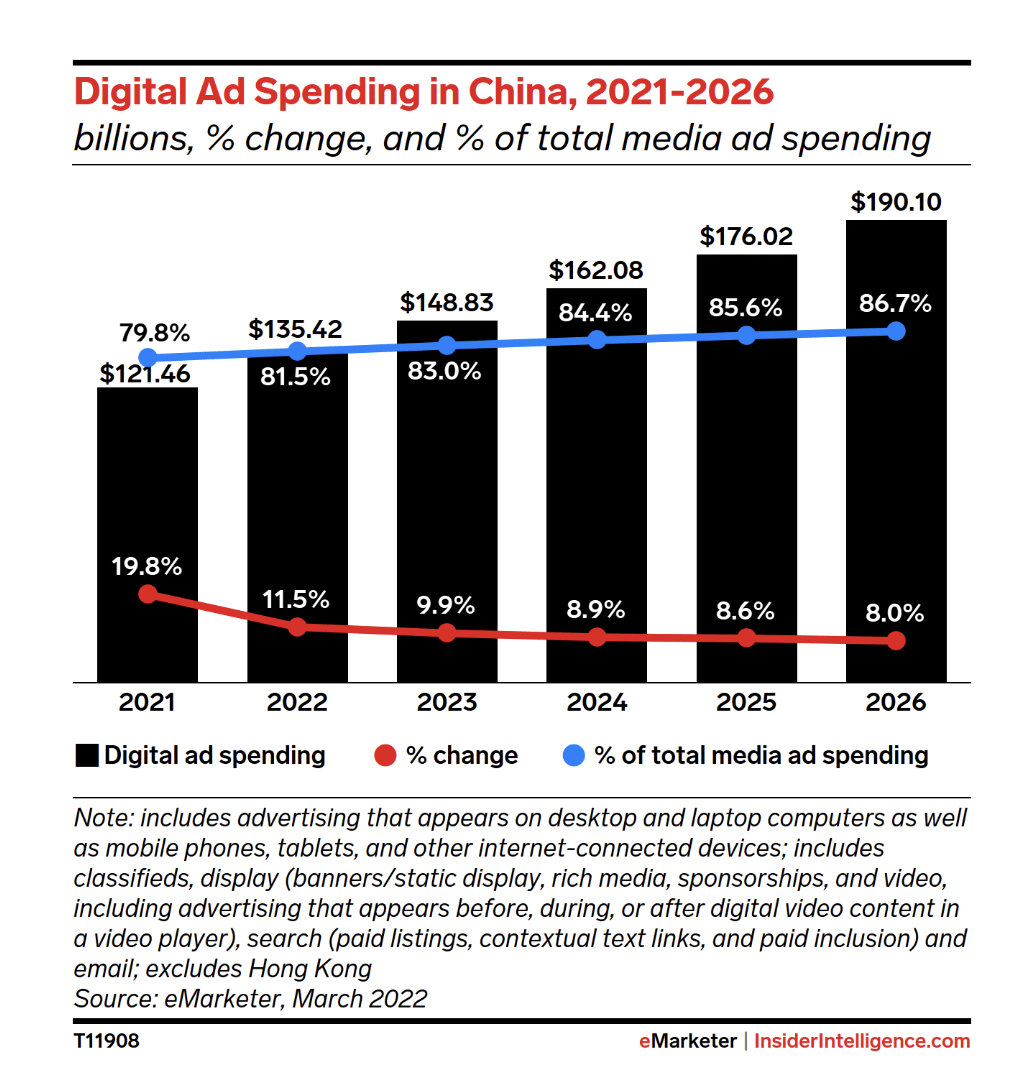

The China digital ad market is forecast to produce strong growth through 2026, but the covid lockdowns haven’t helped growth. Not to mention, the surging growth by ByteDance (BDNCE) has limited the growth by Baidu despite a digital ad market growing nearly 20% in 2021 to reach $121 billion.

Source: eMarketer

Unfortunately, Baidu divested businesses back in 2018 leading to the 2019 revenue declines while covid knocked down growth just as a rebound was expected in 2020. Now, covid lockdowns have again impacted growth in the sector during 2022.

The story should be different in 2023 with China finally reopening the economy. The rebound will be lumpy with millions of Chinese currently being infected by covid, but the country should quickly return to growth mode as covid burns out in a few months.

Apollo Go Becomes Real

With the CCP is finally taking the pain, Baidu should finally see a more normal growth opportunity with the ability to participate in near double digit growth rates in digital advertising. At the same time, the robotaxi business is starting to push the AI division towards material growth.

Baidu has reported the following Apollo Go metrics:

- 287,000 rides were provided in Q2, surpassing 1 million rides total on July 20, 2022.

- The self-driving service also started charging fees after receiving a permit on July 20.

- On August 8, Apollo Go began fully driverless rides, making it the first to do so in China.

- 474,000 rides were provided in Q3, up 311% year over year, and a 65% increase compared to the previous quarter.

Apollo Go already covers 10 cities in China and provided 474,000 rides in Q3’22. According to Baidu, the average robotaxi in Beijing and Shanghai provides 15 rides a day or ~105 a week assuming no down time for maintenance.

At $10 a ride (probably less in China), the average robotaxi would generate $1,000 per week in fares. Baidu has to dramatically ramp up the fleet in order to produce material revenues, though the company has provided any fare details.

Poni.ai announced plans to charge passengers 2.6 yuan, or just$0.38, per kilometer. Data shows that Shenzhen taxis average 384 km a day with 71% of those with passengers, or the equivalent of 273 km of paying trips per taxi on a daily basis.

A Baidu robotaxi operating 24 hours a day with similar traffic patterns would generate daily fares of 710 yuan or $102. The service is now restricted to work hours in major cities reducing the ability to reach the peak daily trips of up to 25 in the major Chinese cities of Shanghai. Apollo Go currently averages 15 daily trips in a restricted operating time of 9am to 5pm.

The whole question with Apollo Go is a matter of scale. Baidu will need to deliver thousands of robotaxis in each city with a goal of reaching operations in 50 cities by 2025 and 100 by 2030.

As an example, Shenzhen has ~21,500 taxis. The long-term goal would be to expand upon the current taxi base and drive more efficient operations. Apollo Go would need over 5,000+ robotaxis to just garner nearly 25% market share.

Some quick math on the opportunity here:

- 2025 – 1,000 robotaxis across 50 cities = 50,000 robotaxis @ $102/d = $5.1M/d

- 2030 – 5,000 robotaxis across 100 cities = 500,000 robotaxis @ $102/d = $51.0M/d

By 2025, Baidu would have below 5% of the taxi market and generate ~$464 million in quarterly revenues. By 2030, the taxi market share could approach 25% with quarterly revenues of nearly $4.7 billion per quarter.

The revenue metrics start escalating, but only once Baidu crosses over the 50-city threshold and operates 1,000 robotaxis per city. The Chinese tech giant already generates ~$18 billion in annual revenues, so the Apollo Go business needs to produce billions in annual revenues to even become material to Baidu.

As an example, Uber (UBER) already produces nearly $32 billion in annual revenues from ridesharing trips and food delivery. The higher US fares clearly make a difference in valuation, but Baidu has the ability to expand their strong AV technology lead into other parts of the world where fare values are vastly higher.

Takeaway

The key investor takeaway is that Baidu is a crazy cheap Chinese tech stock on any return to growth in 2023. Apollo Go could be a complete game changer for the stock valuation.

The stock fell from a repeated test of $150 to below $75 on dual fears of a delisting from the Nasdaq and covid lockdowns crushing the Chinese economy. At just $112 here, the stock trades at only 12x 2023 EPS targets making Baidu a stock to own for a rebound next year.

Be the first to comment