FeelPic

Investment Thesis

Badger Meter (NYSE:BMI) is experiencing healthy demand for its products, leading to strong order rates and healthy backlog levels. Additionally, the supply chain constraints have started to moderate sequentially. All this should act as a tailwind for the company’s revenue in the near term. The macro drivers in the Advanced Metering Infrastructure (AMI) and water quality monitoring systems, along with the U.S. infrastructure bill, should benefit in the long term. The margins should benefit from the stabilization in higher input costs, pricing actions, and improvements in Selling, Engineering, and Administration (SEA) expenses as a percentage of sales. The stock is currently trading at 43.19x FY23 consensus EPS estimate of $2.56, which is slightly above its five-year average forward P/E of 41.15x. Hence, I have a neutral rating on the stock.

Revenue Outlook

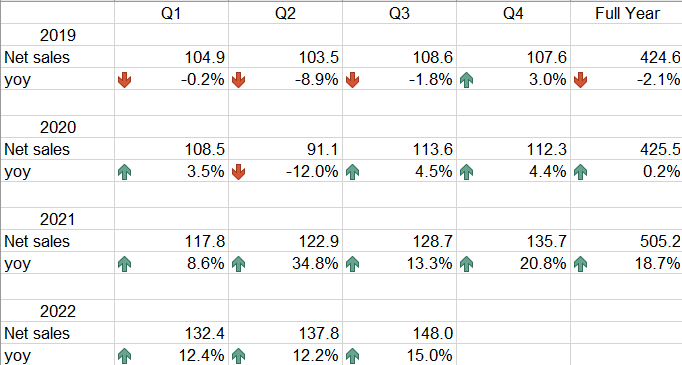

The company’s sales are continuing to benefit from the healthy demand trends in its end markets, along with the acquisitions of Analytical Technology (January 2021) and s::can (November 2020). In Q3 FY22, sales growth was broad-based across both water quality and quantity, ultrasonic meters, ORION cellular radio endpoints, and BEACON Software-as-a-Service (SAAS). The continued strong order demand, improvement in production output, and ongoing price realization, helped offset the supply chain challenges. Despite the slowing macroeconomic environment, the order rates and backlog levels in the utility water business remained strong.

BMI’s revenue growth (Company data, GS Analytics Research)

Looking forward, the strong order rate and a robust backlog should benefit revenue growth in the near term. Additionally, the company should also benefit from the moderation in supply chain constraints. BMI saw sequential improvement in supply chain challenges in the last quarter. The company has a resilient business model, which should help it during times of potential economic softening. The replacement-driven demand, secular AMI (Advanced Metering Infrastructure) drivers, and growing proportion of stable SaaS revenue are supportive of multi-year growth against the backdrop of uncertain macros. The meter portion of the business is replacement-driven which is usually less cyclical. The company is seeing good volume growth in cellular radios and is experiencing a ~100% attachment rate in its software.

There are macro drivers around AMI and real-time water quality monitoring systems that should benefit in the near term as well as in the long term. AMI systems are meter reading devices in which data is gathered by utilizing a network (fixed or cellular) of data collectors or receivers that are able to receive radio data transmission from utility meters. It eliminates the need for utility personnel to drive through service territories. Utility companies are concerned about Nonrevenue Water (NRW), which could have an impact on their business operations, in areas where the availability of water is stressed. Nonrevenue water is the water that is pumped out/produced, but is lost due to leaking and broken pipes, or poor maintenance. BMI’s products, such as the E-series ultrasonic meters, ORION cellular solution, and BEACON SaaS are well-positioned to take advantage of this opportunity. The BEACON software help improve the visibility of utilities and other end water users (such as homeowners) to their water usage.

The company is gaining a sustainable market share in its AMI business, especially cellular solutions and software. The different government mandates and laws related to the discharge of water should benefit BMI’s water quality monitoring products. ATi and s::can are the leading providers of this solution.

Additionally, in the long run, the company should also benefit from the U.S. infrastructure bill. The Bipartisan Infrastructure law will deliver more than $50 bn to the Environmental Protection Agency (EPA) to improve the nation’s drinking water, wastewater, and stormwater infrastructure.

I believe in the near term, the company’s revenue should benefit from the strong order rate, healthy backlog levels, pricing actions, and improvements in the supply chain. In the long run, it should benefit from the U.S. infrastructure bill and macro drivers in the AMI and water quality improvement systems.

Margin Outlook

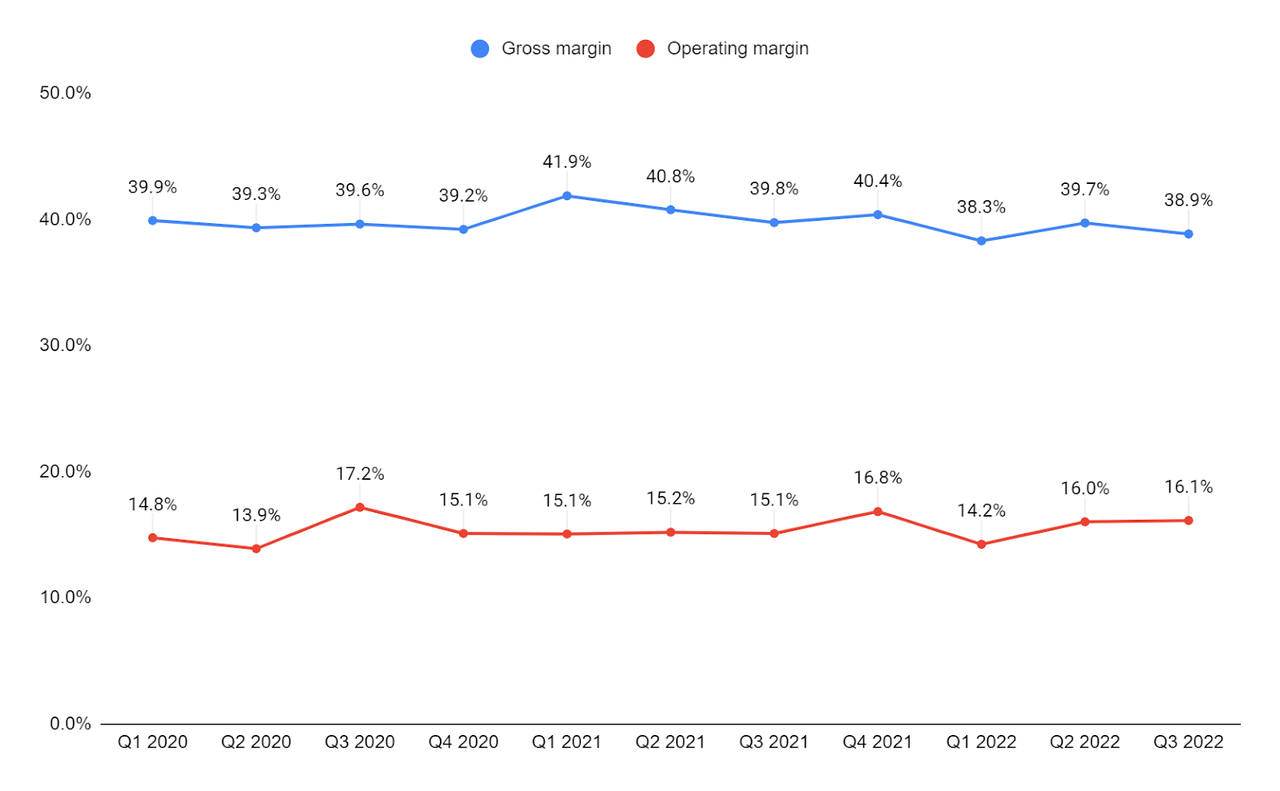

The company’s gross margin was impacted in 2021 as well as 2022 due to the increased costs of resins and electronic and brass components, as well as increasing freight and logistics costs. This was partially offset by the pricing actions taken over the last few quarters. Copper prices have started to decline. However, due to the one-quarter lag in realization, it did not benefit the gross margins in the third quarter of 2022. The operating margin is continuing to benefit from the improvement in Selling, Engineering, and Administration as a percentage of sales.

BMI’s gross margins and operating margin (Company data, GS Analytics Research)

Looking forward, I believe the company’s gross margins should benefit from the improvement in the supply chain, moderation in inflationary costs, and the pricing actions taken over the last few quarters. The operating margins should benefit from the slight improvement in gross margins and by continuing to leverage selling, engineering, and administration expense as a percentage of sales. The company is also focusing on growing its revenue from SaaS, which is a higher-margin business.

Valuation & Conclusion

The stock is currently trading at 43.19x FY23 consensus EPS estimate of $2.56, which is above its five-year average forward P/E of 41.15x. Even on the FY24 consensus EPS estimate of $2.75, the stock is trading at a P/E of 40.32x. This isn’t particularly cheap.

BMI EPS estimates and Forward P/E (Seeking Alpha)

While I like the company’s growth prospects, I believe they are already getting priced in at the current levels. Hence, I have a neutral rating on the stock.

Be the first to comment