StockByM/iStock Editorial via Getty Images

Continuing my foray into the value ETF universe, I would like to provide an in-depth assessment of the Avantis U.S. Large Cap Value ETF (NYSEARCA:AVLV), an actively managed investment vehicle with a portfolio of upper-echelon high-quality U.S. value stocks.

I believe AVLV ETF deserves a thorough review for a few reasons. First, although being a comparatively nouveau vehicle, with an inception date of 21 September 2021, AVLV has already demonstrated a fairly competitive performance, trouncing both the iShares Russell 1000 Value ETF (IWD) and iShares Core S&P 500 ETF (IVV). Second, its valuation characteristics are fairly decent (though the situation is nuanced, as usual) while quality is simply superlative, undergirded by the large-size factor, a nice combination. Third, the expense ratio of 15 bps is almost wafer-thin, and liquidity is more than comfortable.

Regardless, AVLV is certainly not entirely spotless, and its principal disadvantages, including valuation nuances, are addressed below in the article.

Now, let us delve deeper to discuss all of the above and arrive at a conclusion about whether the ETF deserves a Buy rating today.

AVLV strategy essentials

AVLV is actively managed, with the benchmark being the Russell 1000 Value index. The fund’s strategy revolves around the large-size, value and, quality factors. Let me quote the prospectus,

The portfolio managers define “value characteristics” mainly as adjusted book/price ratio (though other price to fundamental ratios may be considered). The portfolio managers define “profitability” mainly as adjusted cash from operations to book value ratio (though other ratios may be considered).

There are other considerations described in greater depth in the document that can be found on the AVLV website.

Superb returns over short history

What returns was the strategy capable of yielding in the past?

First, AVLV not only easily trounced IWD over the October 2021 – January 2023 period, but also managed to outpace IVV, hence, beat the market, and by a meaningful margin as illustrated below. However, the highest standard deviation in the group is a disadvantage to mention.

| Portfolio | AVLV | IVV | IWD |

| Initial Balance | $10,000 | $10,000 | $10,000 |

| Final Balance | $11,009 | $9,661 | $10,454 |

| CAGR | 7.47% | -2.56% | 3.38% |

| Stdev | 23.59% | 22.37% | 20.31% |

| Best Year | 8.87% | 11.07% | 7.77% |

| Worst Year | -5.52% | -18.16% | -7.74% |

| Max. Drawdown | -16.98% | -23.93% | -17.78% |

| Sharpe Ratio | 0.35 | -0.08 | 0.18 |

| Sortino Ratio | 0.54 | -0.12 | 0.27 |

| Market Correlation | 0.95 | 1 | 0.95 |

Created by the author using data from Portfolio Visualizer

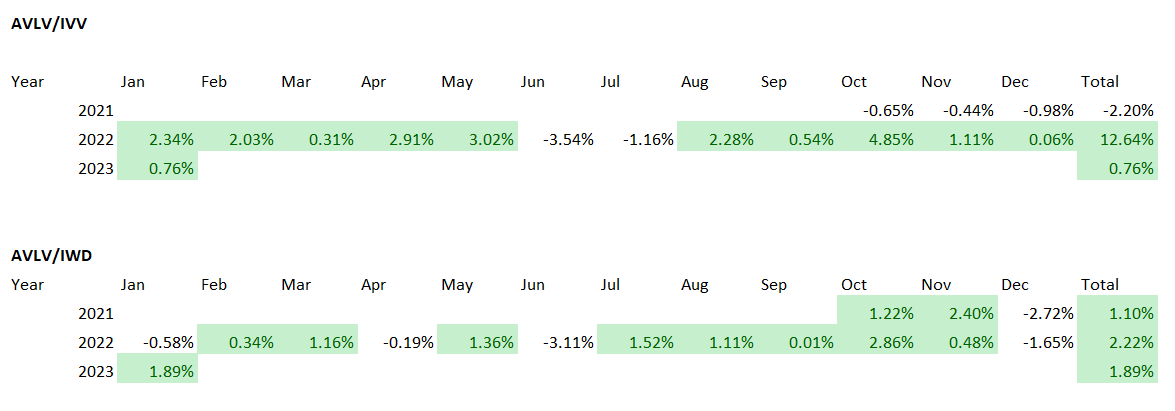

Now, let us look at the monthly and annual returns. There is also a lot to admire here.

Created by the author using data from Portfolio Visualizer

My dear readers might justly note that AVLV was launched during the heyday of the value style revival which grossly contributed to its outperformance, and they will be completely right. Obviously, the results shown above were supported by the capital rotation to the beaten-down value names as the major out-of-the-pandemic stock market narrative, as well as by the inflation and higher interest rates issue in 2022 that triggered the bear market, which cheaper stocks navigated much easier than their counterparts with bloated valuations they had because of the great expectations premia. It is unknown how the fund would have performed during the value drought of the previous decade and what returns it would deliver during the darkest days of the pandemic. That is to say, there is certainly no guarantee AVLV will continue clocking 7.5% in the annualized return going forward when the hawkish period is over or in a scenario when too much tightening triggers a full-scale recession.

Nevertheless, it should be noted that even in January 2023, when investors cranked up bets on the growth cohort that bore the brunt of the 2022 bear market, grossly contributing to the Invesco QQQ (QQQ) and the S&P 500 ETFs rally, AVLV still managed to finish ahead of IVV and IWD.

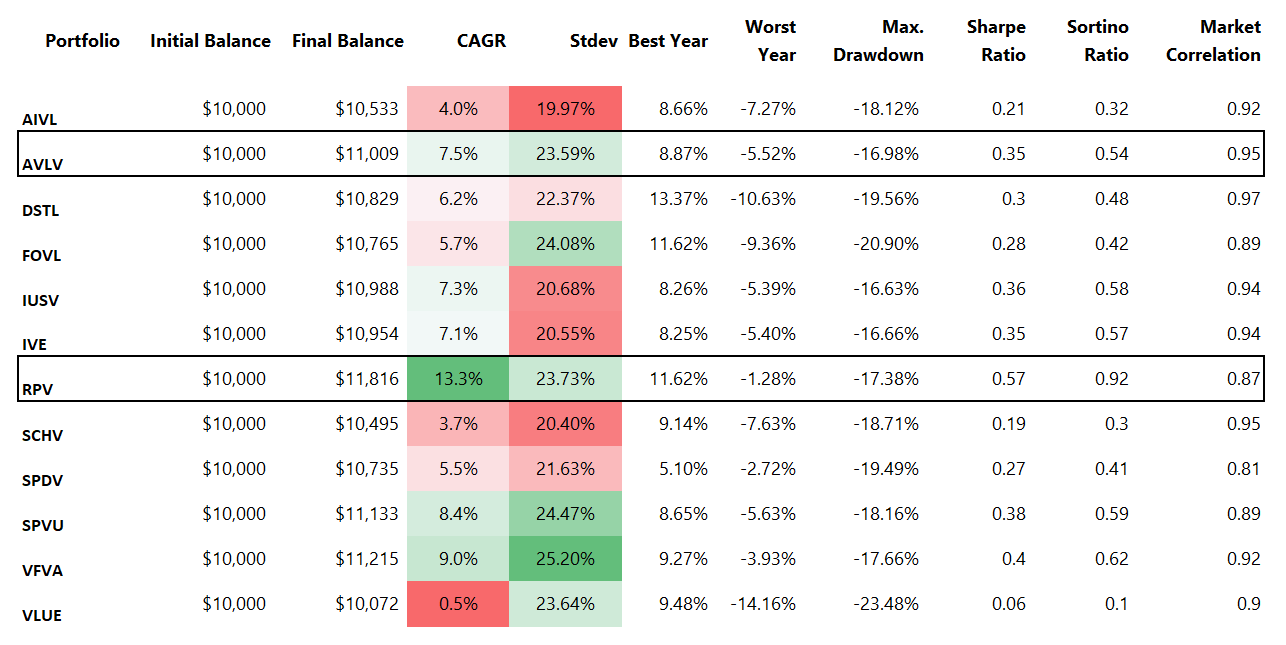

Now, let us compare its returns to a broader group of peers, with the period assessed being the same. For that purpose, I selected the following large-cap-focused funds I covered in the past:

- WisdomTree U.S. AI Enhanced Value Fund (AIVL)

- Distillate Fundamental Stability & Value ETF (DSTL)

- iShares Focused Value Factor ETF (FOVL)

- iShares Core S&P U.S. Value ETF (IUSV)

- iShares S&P 500 Value ETF (IVE)

- Invesco S&P 500 Pure Value ETF (RPV)

- Schwab U.S. Large-Cap Value ETF (SCHV)

- AAM S&P 500 High Dividend Value ETF (SPDV)

- Invesco S&P 500 Enhanced Value ETF (SPVU)

- Vanguard U.S. Value Factor ETF (VFVA)

- iShares Edge MSCI USA Value Factor ETF (VLUE)

Please do not overlook the fact that in the peer group above, only AIVL and VFVA are actively managed vehicles.

Created by the author using data from Portfolio Visualizer

Here, the results do not speak in favor of the Avantis ETF as it delivered a CAGR of about 1.8x lower than the top name in this club, RPV, one of my favorite mega/large-size value plays. AVLV also underperformed VFVA and SPVU.

Quality characteristics: little to criticize

I ardently believe that the quality factor always deserves attention, and I will certainly not ignore it today.

AVLV is clearly capable of selecting top-quality value names as the share of its holdings with no less than a B- Seeking Alpha Quant Profitability grade is almost 97%, a superb result. This is of course hardly coincidental for an equity mix with the weighted-average market capitalization of over $187 billion (partly thanks to two $1 trillion league members Apple (AAPL) and Alphabet (GOOG) (GOOGL), together accounting for 4.4%), as per my calculations.

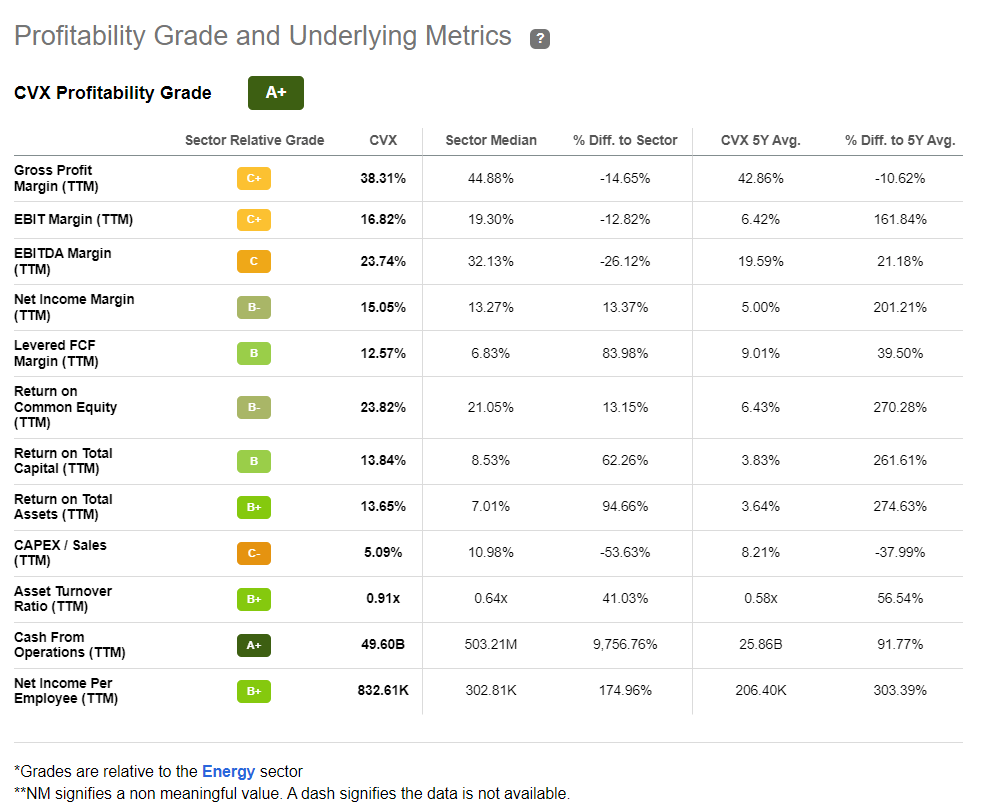

An example of a top-quality stock that deserves attention is Chevron (CVX), an energy supermajor with 2.7% weight in AVLV (its largest holding).

Seeking Alpha

Meanwhile, stocks with profitability issues manifested in a D grade and worse, mostly financials like Equitable Holdings (EQH), account for only 1.4%. An important fact to mention is that as my computations illustrated, the median Return on Total Capital for stocks outside the financial and real estate sectors is in excess of 14%, a solid result highlighting that most firms have outstanding capital efficiency.

At the same time, only a measly number of companies, about 2.4%, were incapable of turning even a small net profit, likely unable to navigate the cost pressures stemming from omnipresent inflation last year.

But most importantly, I found just two cash-burning firms in this basket, Under Armour (UA) (UAA) (both classes of common stock are present), a well-known apparel name with an inventory issue, and Norwegian Cruise Line Holdings (NCLH).

Valuation: the earnings yield reflects a meaningful discount, but there is something to dislike anyway

As per my analysis, AVLV has a weighted-average earnings yield of 9.1% (a Price/Earnings of less than 11x), a justly solid result. The reason for that is likely only a modest growth premia factored in; to corroborate, the WA Forward EPS growth rate is at 12.7% while Forward revenue growth rate is below 9%, a level some investors might call subdued. Another reason is that financials, a low P/E haven, is its key sector with a close to 20% weight. Energy, another low P/E sector, accounts for 15.9%.

Yet this is just the tip of the iceberg. The issue here is that if assessed from a different angle, AVLV does not look as underappreciated as upon the very first inspection. The fact is, only ~27% of the holdings boast a Quant Valuation grade of B- or better, while about 40% are clearly priced at a premium to their respective sectors as they are D-rated or worse. In my view, this is an unattractive proportion.

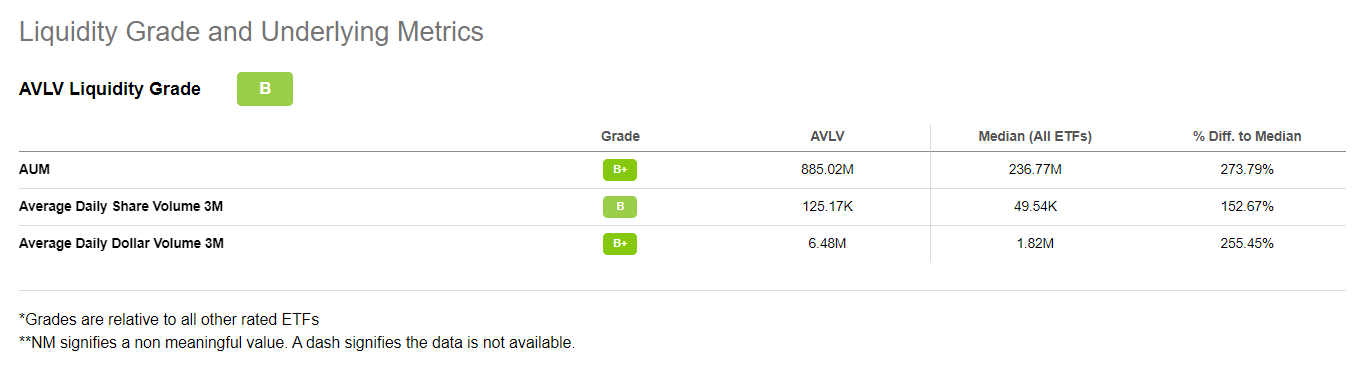

Liquidity: large AUM, substantial volume

AVLV’s clear advantage is that with only sixteen full months in the books, the fund has already amassed a solid AUM of about $885 million. Importantly, average daily share volumes are well above all other rated ETFs’ medians, with a diminutive 30-day median bid/ask spread of 0.06%, as per its website.

Seeking Alpha

Investor Takeaway

AVLV is an excellent low-cost value ETF with high-quality holdings.

I reckon this vehicle might appeal to quality-oriented investors who would like to own a portfolio of cheaper names with a minimal risk of the presence of value traps.

AVLV’s returns were robust in the past, yet a few peers like RPV and VFVA still did better.

In conclusion, I highlight a large share of stocks with a D+ Valuation grade and worse despite an appealing earnings yield as a major risk worth paying attention to. And while acknowledging that AVLV did a great job selecting highly profitable names, I would opt for a Hold rating this time.

Be the first to comment