hapabapa/iStock Editorial via Getty Images

Dear readers/followers,

You know that I’m a big fan of investing in conservative consumer staples – everything that’s “necessary” for living our modern lives, but that also comes with safety, dividends, quality, and history. You certainly could make the argument that some companies people recommend in the tech growth sector are necessary for many people’s lives and work, but they lack the safety, dividend, and history that I would consider being desirable in an investment.

So, for that reason, I’m fairly one-sided when it comes to what sort of requirements I have for my investments.

Ahold Delhaize (OTCQX:ADRNY) fulfills every last one of them.

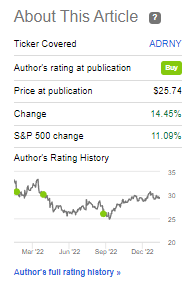

Since my last article, the company has performed like this.

Seeking Alpha Ahold Delhaize (Seeking Alpha)

Ahold Delhaize – Updating for 2023

So, since my latest article, we’ve seen a good performance. We’ve also seen the arrival of the 3Q22 results, which I’ll present here, and we have Full-year results incoming next week, which means I’ll likely edit this article with an update if these results turn out to materially change my thesis or approach to the business.

However, I have doubts that this will be the case. Grocery companies and other consumer staples remain double-digit exposure in my portfolio, and while these do see reactions to ups and downs in the market, these companies have much lower overall beta than the general market. My investments here include Nestlé (OTCPK:NSRGY), Axfood (OTCPK:AXFOF), Unilever (UL), Diageo (DEO), Kesko (OTCPK:KKOYF), Europris (OTCPK:ERPSY), Kroger (KR) and Carrefour (OTCPK:CRRFY). As of right now, I’ve made money on every single one of these investments.

So, I’m pretty traditional with my investing. I don’t go far to left field, I don’t go into the nano, micro, or small-cap space typically, and I spice my investing with very conservative put options – no more than 45 days out in terms of expiration, and requiring 12-19% movements in share price from dividend-yielding, investment-graded businesses with annualized options yields of 9-22% that, in case of the in-the-money assignment are no more than 7% of my total buying power, and are companies I actually want to own at that strike price.

That’s conservative, as I see it.

Ahold Delhaize is part of this strategy – and has been for years. These companies have a very specific purpose in my portfolio. Their purpose is never to make you rich or to provide those 100-200% RoRs in 3-4 years, but instead give safety – and they are very good “at that”.

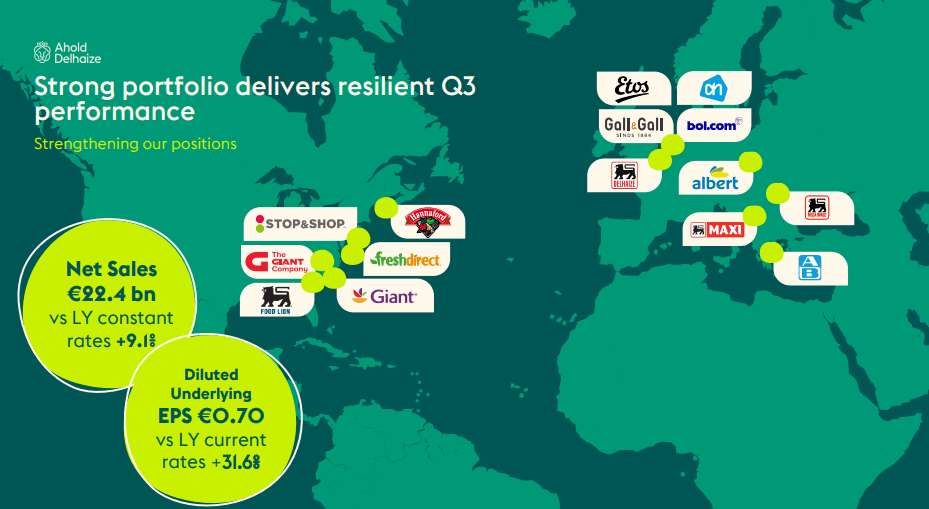

So, remember. Ahold Delhaize, despite its name, isn’t just some Netherlands grocer – it’s one of the largest grocers on the planet.

Ahold Delhaize IR (Ahold Delhaize IR)

The recent quarter was the latest success in a long line of successes. The appeal of a grocer is a combination of attractive pricing and offerings due to scale and SCM, good brands, and growth potential. The company has all of this. Its brands and chains including Food Lion, Albert Heijn, Stop & Shop, and Delhaize Belgium all saw growth rates that are only the latest in consecutive quarters of growth. What’s more, the company has actually continued to manage savings and keep pricing relatively low. Look at both the sales growth and the EPS growth the company is reporting.

Furthermore, we have the company’s online arm. Ahold owns Bol.com, a sort of European Amazon (AMZN) proxy. The company originally intended to separately list Bol.com but pulled back after the market crash last year – a good decision. Still, Bol.com has performed above Amazon’s own European model, with partner sales growth rates of double digits, to where partner sales are now nearly 60% of the 3Q22 total. The company is also building out its fulfillment centers to 240,000 sqm.

Here are the company’s near-term priorities.

Ahold Delhaize IR (Ahold Delhaize IR)

The patterns and flows towards the end of the -22 fiscal were clear. Both online and normal sales increased by double digits, and Ahold is still managing to keep savings a thing with over 100 items under €1, and its own store brands expanding their appeal as customers need to watch their wallets more closely than before. The US pushes, including the Giant Food member program is also growing, and the total ADUSA loyalty programs have generated over $1.5 in incremental sales in 3Q22 YTD alone from 8 billion personalized offers to 28 million households.

In short, Ahold’s strategy is working – and the company is pulling several levers in order to control the flows of its SG&A and costs overall. It acquired a stake in an ad-tech company in order to drive its digital advertising opportunities. The digital media business in Bol.com grew by 60% in 3Q22 due to driving opportunities.

Overall, I want to give you the picture, because I believe it fair, that Ahold Delhaize is doing extremely well. The company’s operating margin is at 4.4% at a constant rate. This may sound abysmal – but it’s a grocery company. US companies have far lower margins, and only Scandinavian ones can, as far as i know, consistently break the 5% margin barrier due to relatively unfair competitive situations in our market (the major players can essentially “force” companies to give up recipes in order for them to leverage store-branded products, or pull them).

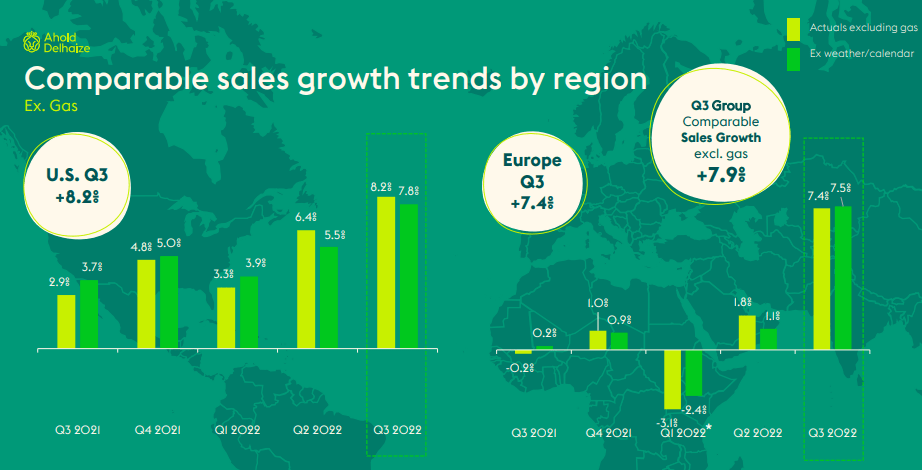

Net sales grew at 9.1% company-wide, with even larger growth in underlying OI of 9.7%, or close to a billion euros. Net income was up 14.4% – again, during this environment. This needs to be highlighted. Here are the growth trends.

Ahold Delhaize IR (Ahold Delhaize IR)

These operating margins we’re seeing we’re despite the heavy impacts of energy pricing. Of course, that’s going to be impacting Ahold – the company has responded by pushing power-saving initiatives, upgrading cooling systems, using LED lighting, and expanding solar and renewables where possible, and profitable.

All of these positives were enough to cause the company to increase its 2022E outlook, which is now at low-double-digit growth in underlying EPS – during one of the most difficult periods we’ve seen in a long time. That also comes with the company’s share buyback targets of €1B in 2023, and a dividend payout ratio of 40-50% with a YoY growth in the dividend.

This quarter was a continued confirmation of the company’s excellent and efficient growth vectors and the stability of its operations. It’s remarkable that not only are the legacy grocery operations growing as they are – but so are the company’s digital pushes, inside and outside of Bol.com.

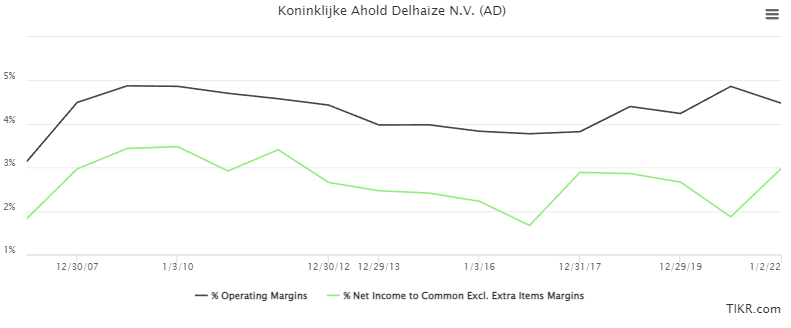

Of course, in the end, I’m a numbers guy more than anything else – and in the end what surprises me the most, is what the company has been able to do with its margins, both net and operating, during this crisis. They haven’t been touched from their long-term averages. Sure, there was some instability – but that’s been recovered.

Ahold Delhaize Margins (TIKR.com)

When it comes to a company like this, once established that its operations are working, what I really want to know is how much the company is making for each €1 of sales revenue. And Ahold Delhaize shows me that the company is still making that €0.04-€0.05 OM, and upwards of €0.03 in net – for a company like this, that’s fairly amazing. Beyond that, what I look at is how the company uses its cash available, and the trends here are excellent as well.

That’s enough for me to move into valuation with conviction.

Ahold Delhaize Valuation – the company is still a “BUY” due to low valuation

So, the peer analyst average for Ahold is virtually unchanged since my last article. Oh, there’ve been some minor adjustments in the averages, where the S&P global 18-analyst average PT is now at €31.7 for the active compared to around €31 last time I wrote about the business. But given that we’re still below €30, most of these analysts believe the company is a “BUY” – 14 of them, to be exact. That’s a 14.9% upside to the average.

You also know where I stand in general due to my latest set of PTs from September -22. Ahold Delhaize remains a global grocer with an investment-grade credit rating trading at a P/E range between 12-14x. That’s insane, given that domestic peers trade closer to 20x, even with the market in its current state. If one of its European peers traded even close to that valuation, I would treat it the same way I do Ahold Delhaize here – it’s a must “BUY” for me.

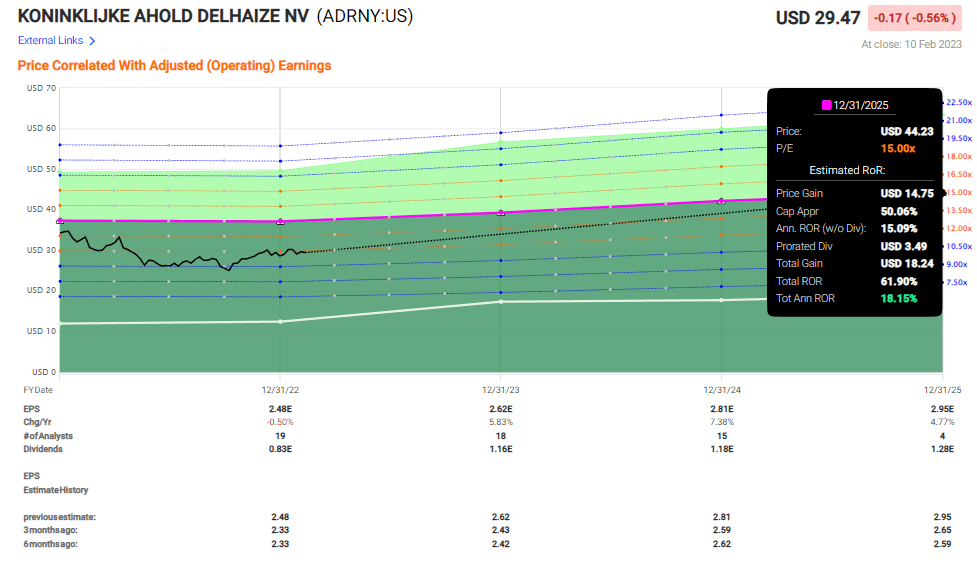

Even calculating Ahold at only a 5-year P/E average of around 15x, the upside for 2025E is close to 62%, assuming a 15x P/E and a share price just above $43. The company is being undervalued due to perceived risks in its IT business, which I see as not being valid here.

F.A.S.T graphs Ahold Delhaize (F.A.S.T graphs)

The best way to explain my current view on the valuation that the market has on Ahold here is to say “No, it’s way too low”. The company yields close to 3.55% native (the ADR yield is incorrect), and that’s before clarity on this year’s dividend bump. That’s high in the sector, and coupled with the capital appreciation potential merely from company growth, I believe this turns Ahold Delhaize into a “Must-own” at this price. That’s why I’m beating the table for the company, and why I believe you should seriously consider investing here.

Analysts rarely miss here – less than 20% on a 2-year basis with a 20% of error, and analysts following the company are equally positive on this business’s upside – so that works as well.

Remember my latest PT on AD? It was €35/share. I’m not moving this a cent. Any upside, or challenge, was already calculated into this price target. That’s how I calculate my targets. I combine peer averages, historicals, sector trends, forecasts, and fundamentals, and use valuation models like DCF to arrive not only at a PT that I consider to be in the ballpark but long-term indicative. The only way I even slightly shift my price targets for stocks i invest in is if the company’s thesis changes materially.

So, don’t expect me to change it on AD in the near term – not to the negative, nor the positive side. I see very few, if any, company-specific risks or downsides that are worth truly discounting the company for. If anything, the company is already addressing most of these risks.

No company is risk-free – but buying the companies that stock our daily bread, milk, vegetables, fruits, and other foodstuffs – that’s as close as i believe you can get to “risk-free”, either by investing in the company’s common share, by going for the options, or maybe even looking at AD bonds.

At this time, I’m going for the common, and here is my 2023 thesis for AD.

Thesis

My thesis for Ahold Delhaize is the following:

- The company is one of the more appealing EU/US grocery retailers that is trading at what I consider to be a significant discount to conservative multiples. This discount has increased since my last article.

- I’m keeping my PT and sticking to my “BUY”. Despite inflation and SCM issues, I believe the company is one of the best in the entire market to stick to during these troubles, and I believe 3Q22 to be even further proof of just how well the company is managing, even with 2Q22 out of the way and FY results just around the corner.

- My PT is €35, and I’m at a “BUY” here.

Remember, I’m all about:

-

Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company still fulfills every single one of my criteria – I remain a strong “BUY”er in the business.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment