Abu Hanifah/iStock via Getty Images

A Quick Take On AvidXchange

AvidXchange Holdings, Inc. (NASDAQ:AVDX) went public in October 2021, raising approximately $660 million in gross proceeds from an IPO that priced at $25.00 per share.

The firm provides B2B accounts payable system software to organizations worldwide.

Until AVDX makes a clear and credible move toward GAAP operating breakeven, I’m on Hold for the stock in the near term.

AvidXchange Overview

Charlotte, North Carolina-based AvidXchange was founded to develop a cloud-based AP accounting and payments system aimed at middle market companies and their suppliers.

Management is headed by co-founder, Chairman and CEO Michael Praeger, who has been with the firm since inception and was previously co-founder of PlanetResume and InfoLink Partners.

The company’s primary offerings include:

-

AP Automation Software

-

AvidPay Network

-

Cash Flow Manager

The firm seeks customers in the middle market space via a direct sales and marketing approach as well as indirectly through independent resellers and strategic partnerships such as through MasterCard’s B2B Hub.

The company also sells through third-party software providers like RealPage, MRI Software and SAP Concur.

AvidXchange’s Market & Competition

According to a 2021 market research report by Verified Market Research, the global market for accounts payable software was an estimated $8.77 billion in 2020 and is forecast to reach $17.6 billion by 2028.

This represents a forecast CAGR (Compound Annual Growth Rate) of 9.1% from 2021 to 2028.

The main drivers for this expected growth are a growth in middle-market and small organizations in adopting accounts payable software and a continuing trend toward cloud-based systems.

Also, users have continuing concerns about security related to data authentication, which may act as a brake on the growth of demand in the market.

Major competitive or other industry participants include:

-

Bill.com

-

Coupa Software

-

Others

AvidXchange’s Recent Financial Performance

-

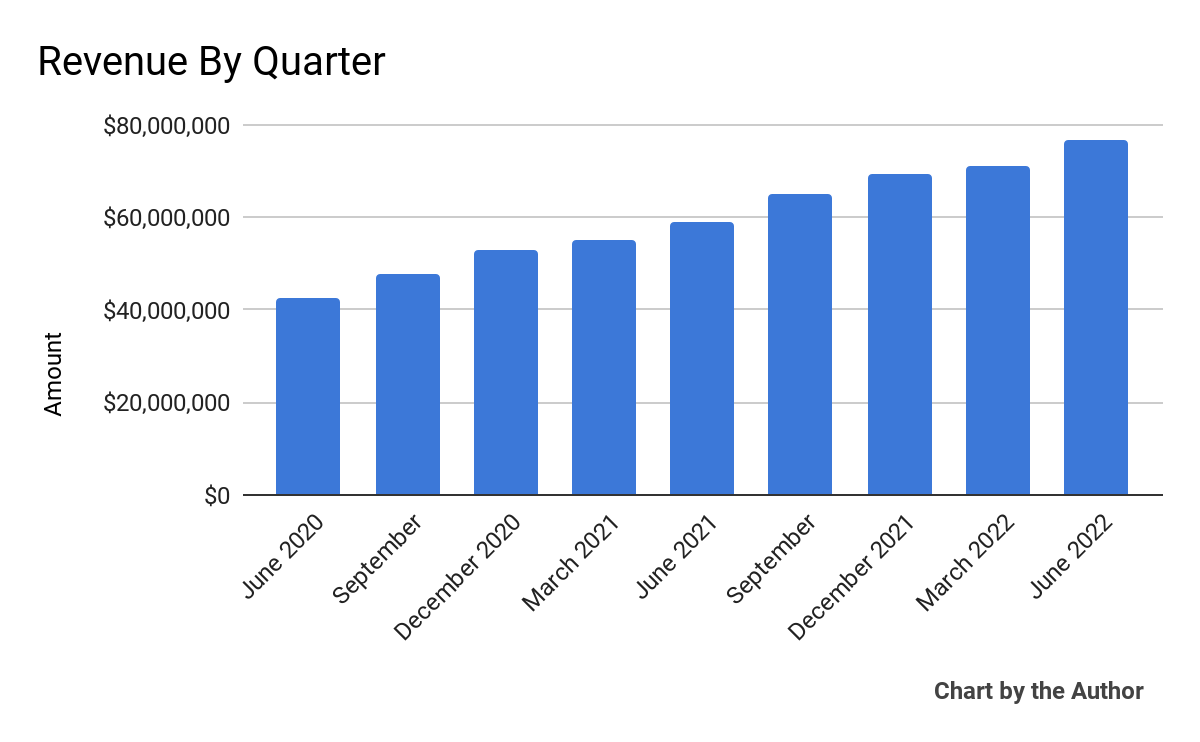

Total revenue by quarter has risen steadily as the chart shows below:

9 Quarter Total Revenue (Seeking Alpha)

-

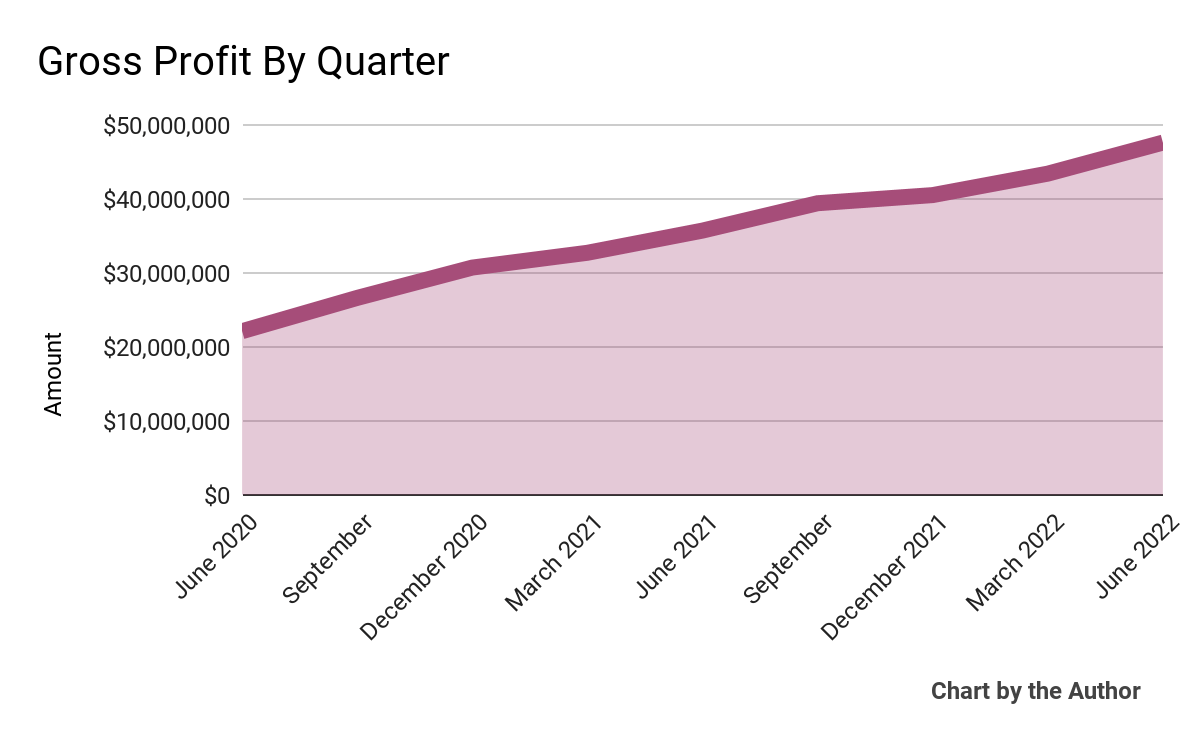

Gross profit by quarter has also grown accordingly:

9 Quarter Gross Profit (Seeking Alpha)

-

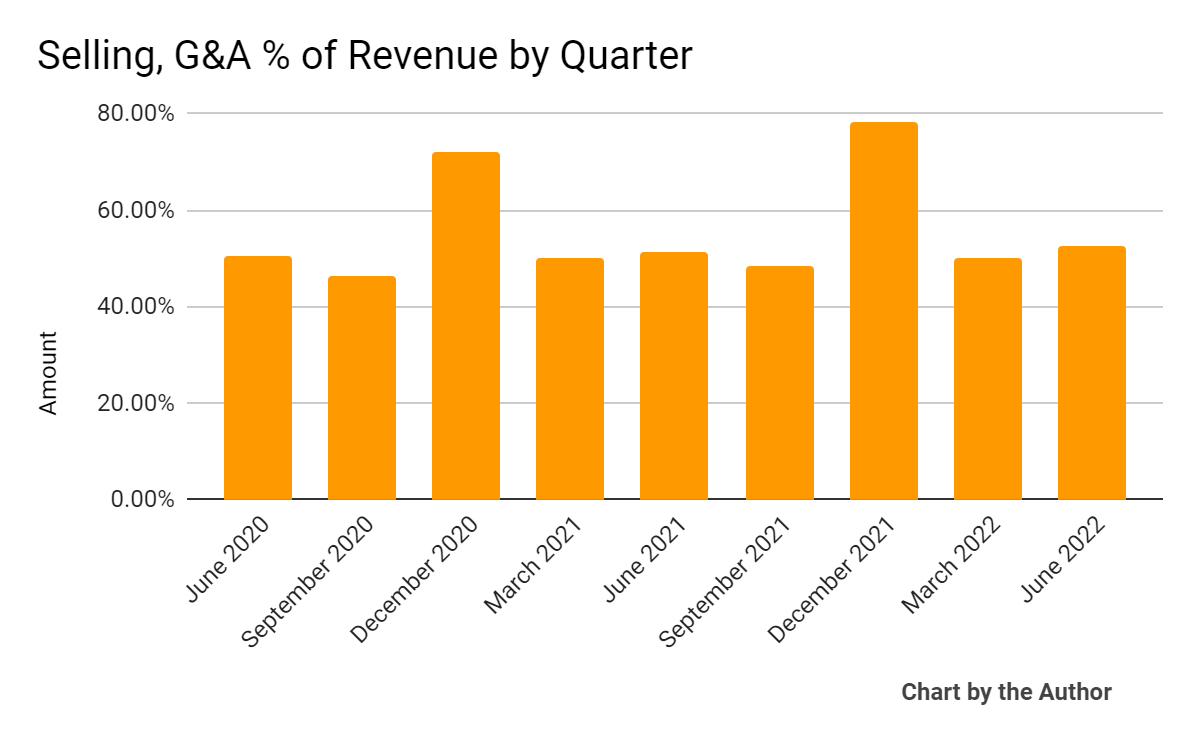

Selling, G&A expenses as a percentage of total revenue by quarter have followed the trajectory shown below:

9 Quarter Selling, G&A % Of Revenue (Seeking Alpha)

-

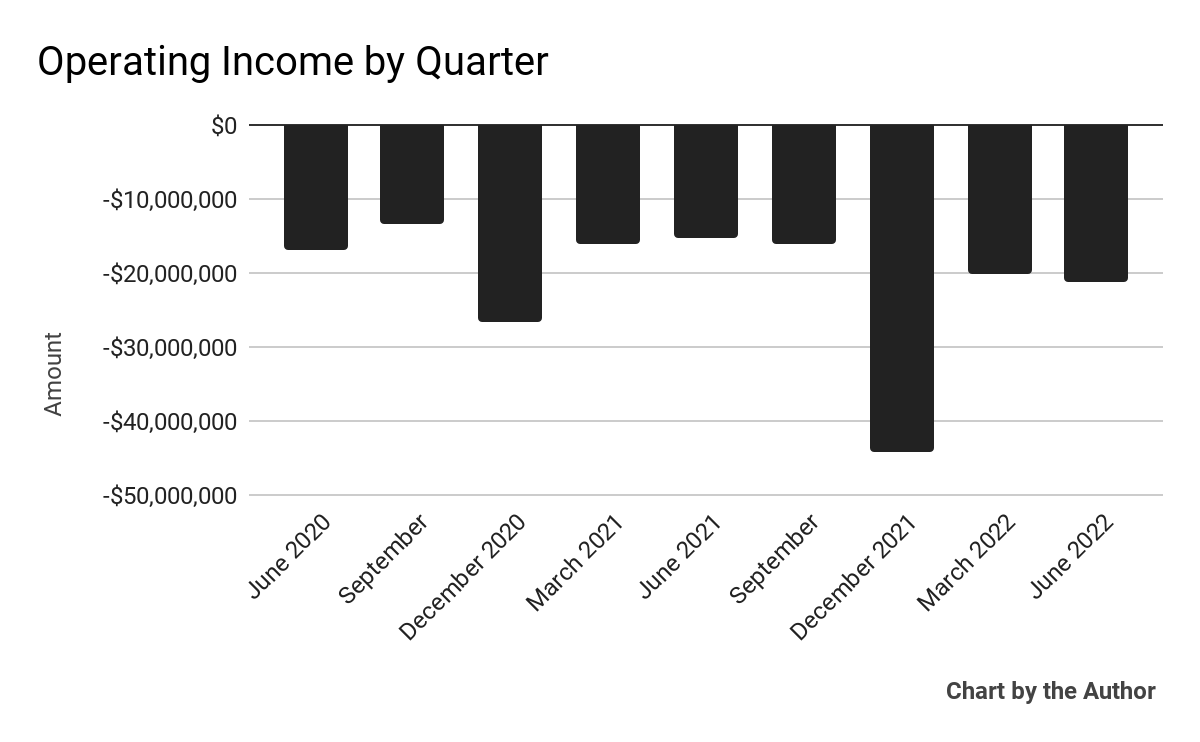

Operating losses by quarter have worsened in recent quarters:

9 Quarter Operating Income (Seeking Alpha)

-

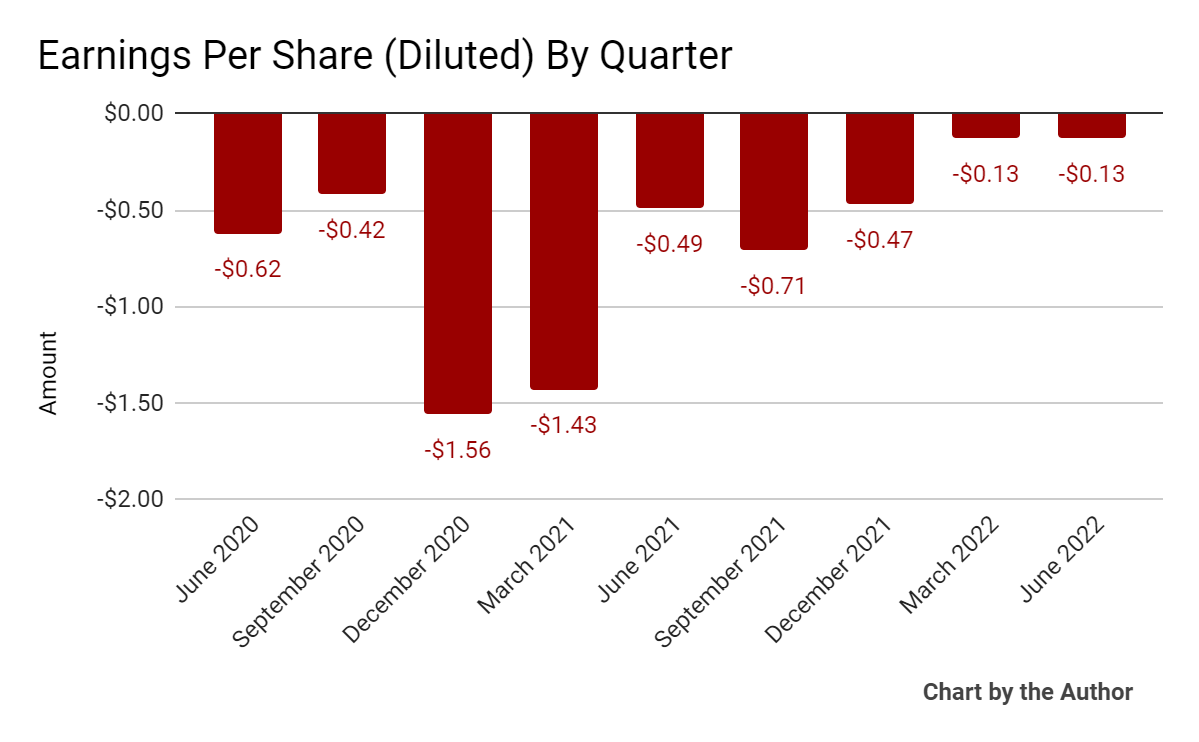

Earnings per share (Diluted) have remained substantially negative, as the chart shows below:

9 Quarter Earnings Per Share (Seeking Alpha)

(All data in above charts is GAAP.)

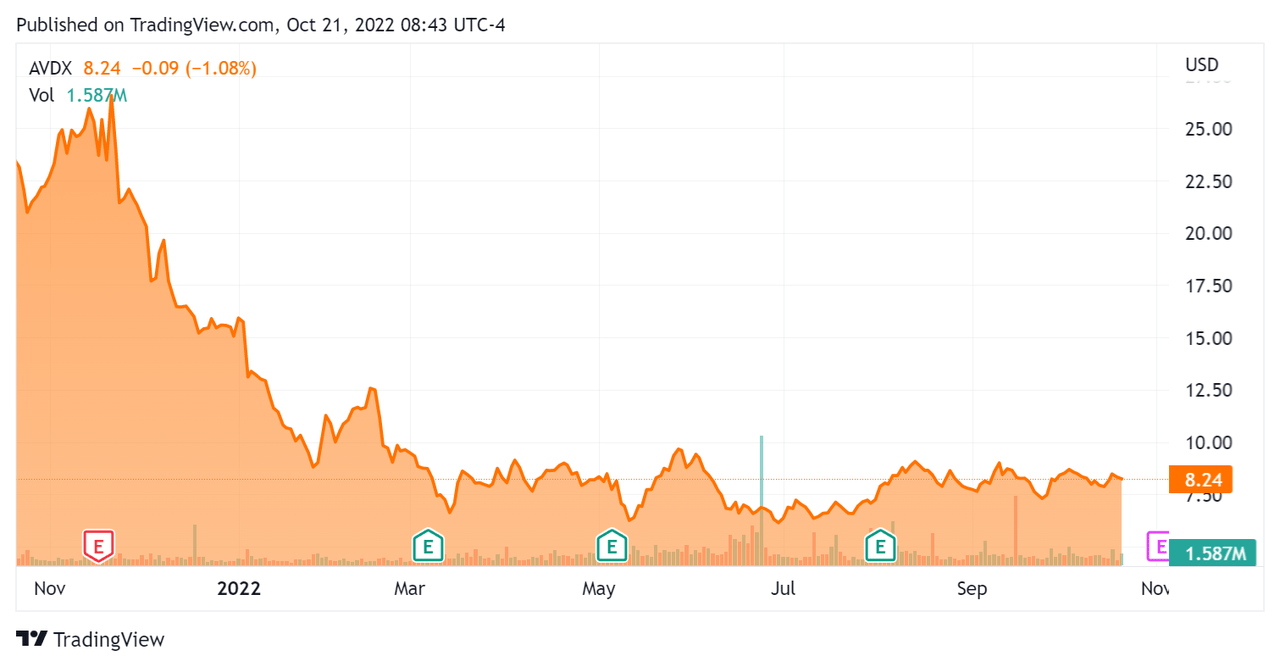

Since its IPO, AVDX’s stock price has fallen 65% vs. the U.S. S&P 500 index’ drop of around 19.2%, as the chart below indicates:

52 Week Stock Price (Seeking Alpha)

Valuation And Other Metrics For AvidXchange

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

4.73 |

|

Revenue Growth Rate |

31.6% |

|

Net Income Margin |

-56.2% |

|

GAAP EBITDA % |

-24.6% |

|

Market Capitalization |

$1,650,000,000 |

|

Enterprise Value |

$1,340,000,000 |

|

Operating Cash Flow |

-$58,310,000 |

|

Earnings Per Share (Fully Diluted) |

-$1.44 |

(Source – Seeking Alpha)

As a reference, a relevant partial public comparable would be Coupa Software (COUP); shown below is a comparison of their primary valuation metrics:

|

Metric |

Coupa Software |

AvidXchange |

Variance |

|

Enterprise Value / Sales |

12.49 |

4.73 |

-62.1% |

|

Revenue Growth Rate |

22.4% |

31.6% |

41.2% |

|

Net Income Margin |

-43.7% |

-56.2% |

28.4% |

|

Operating Cash Flow |

$174,030,000 |

-$58,310,000 |

-133.5% |

(Source – Seeking Alpha)

A full comparison of the two companies’ performance metrics may be viewed here.

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

AVDX’s most recent GAAP Rule of 40 calculation was 7.1% as of Q2 2022, so the firm needs significant improvement in this regard, per the table below:

|

Rule of 40 – GAAP |

Calculation |

|

Recent Rev. Growth % |

31.6% |

|

GAAP EBITDA % |

-24.6% |

|

Total |

7.1% |

(Source – Seeking Alpha)

Commentary On AvidXchange

In its last earnings call (Source – Seeking Alpha), covering Q2 2022’s results, management highlighted its continued growth and lack of deal slippage due to slowing macroeconomic conditions.

The firm believes it can produce adjusted EBITDA breakeven for full calendar year 2024. Adjusted figures usually exclude stock-based compensation (which dilutes equity holders) and one-time items.

Notably, the company has seen encouraging initial results from its straight-through process or STP offering, with supplier counts doubling as well as the number of monthly payments and spend doubling.

As to its financial results, revenue rose by 30.3% year-over-year while non-GAAP gross margin increased to nearly 64%.

Management did not disclose the company’s transaction retention rate, while its Rule of 40 results have been disappointing.

Operating expenses grew by 33.4% year-over-year, due to continued headcount growth, among other expense increases.

As a result, operating losses remain elevated, with no obvious path to operating breakeven.

The company handed out $34.5 million in stock-based compensation over the trailing twelve-month period, the highest rolling 12-month figure as a public company, so management is diluting equity holders to pay employees.

For the balance sheet, the firm finished the quarter with cash, equivalents and short-term investments of $511.1 million and $122.9 million in long-term debt.

Over the trailing twelve months, free cash used was $61.8 million.

Looking ahead, management raised its full year 2022 forward guidance for revenue to $309 million at the midpoint of the range.

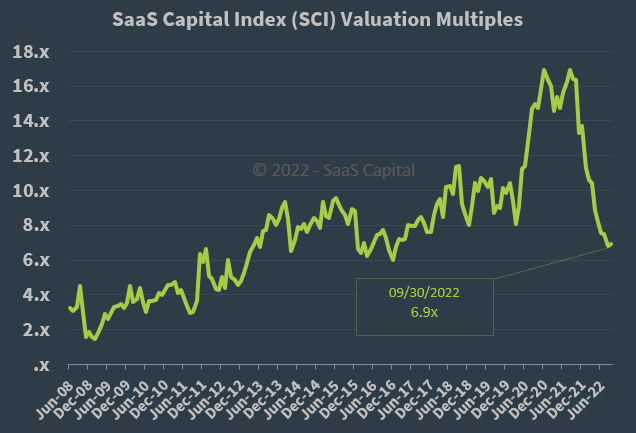

Regarding valuation, the market is valuing AVDX at an EV/Sales multiple of around 4.7x.

The SaaS Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 6.9x at September 30, 2022, as the chart shows here:

SaaS Capital Index (SaaS Capital)

So, by comparison, although AVDX is not a pure SaaS play, it is currently valued by the market at a discount to the broader SaaS Capital Index, at least as of September 30, 2022.

The primary risk to the company’s outlook is an increasingly likely macroeconomic slowdown or recession, which may accelerate new customer discounting, produce slower sales cycles and reduce its revenue growth trajectory.

While AVDX is growing revenue, there is no path to operating breakeven and other performance metrics are underwhelming.

Like so many technology software-enabled companies, management takes pains to point to their growth initiatives but the firm loses ever-increasing amounts of money either through increased expenses or handing out stock to employees, increasing existing shareholder dilution in the process.

Until AVDX makes a clear and credible move toward GAAP operating breakeven, I’m on Hold for the stock in the near term.

Be the first to comment