AnnaStills/iStock via Getty Images

Business

Avid provides tools to help musicians and filmmakers create and edit content as well as collaborate in the process. They sell to enterprises and individuals, but have a more dominant position with the former.

In music, their “Pro Tools” product is the industry standard digital audio workstation (DAW). Basically, a DAW packs everything needed to make music into one place, including instruments. Essentially, anything that used to be bought as hardware is now in software form because of a DAW.

Their other major music product is Sibelius, which is the industry-leading program for writing music.

For video, Avid offers Media Composer—the industry standard video editing software used in television, streaming, film, broadcast news and sports.

Competitive Advantages

Avid’s moat comes from their workflow solutions, which create high switching costs. The company positions itself as a platform where multiple users with different tasks can seamlessly collaborate on content.

If you go to the theaters, watch a streaming show or listen to music on a streaming service, 9 out of 10 times they were built using Avid’s tools.

In music for instance, a producer will make a beat (or instrumental) on his Avid workstation. He would then present it to a singer, and that singer would usually sing into a mic that is also plugged into Avid’s system. The recorded vocals can then be tweaked using Avid software. Once those changes are done, an audio engineer would use Pro Tools to stack the vocals on top of the instrumentals to mix and master it. For films and shows, with talent across the globe sharing even larger data files, the workflows are even more convoluted.

Why it is hard to leave Avid’s ecosystem

First, studios are going to find it inconvenient to learn new tools after building up institutional knowledge and processes around Avid for decades. Their relationship with Avid stretches back to the late 80s when they pioneered digital editing. Further, Avid has been doing a good job, having won 18 Emmys, one Grammy, and two Oscar awards for their technical contribution to the arts.

With the whole production process streamlined on Avid, users are forced to learn and use Avid if they want to work for a major studio. This strengthens their network effects and perpetuates them as the industry standard on high-end productions. Avid is even integrated into university film and music programs to prepare students for jobs. This has the added benefit of cementing them as the standard for the next generation.

Having data stored with Avid discourages enterprises from leaving. Most clients store their media files, their most important asset, on Avid’s hardware and/or cloud. Transferring that data not only runs security risks, but risks around compatibility with their new software.

Moreover, by allowing third-party products and services onto their platform, Avid allows users to work with their preferred tools while keeping their competitors at bay. The media-production landscape is fragmented. It’s full of disparate protocols that create incompatibilities between different products and software. Avid removes that friction by allowing users to work with a wider set of tools on a single interface.

Even if a competitor were to offer a better alternative at a lower price, the potential benefits aren’t worth the risk of disrupting a project—especially when the cost of Avid is small relative to the value of a production.

Investment Thesis

Avid is transforming from a hardware model to a subscription-based one with recurring-revenues. The new model not only provides stable and predictable revenues, but comes along with higher profitability and strengthens their competitive position.

History

Avid’s original business model was hardware-centric. It revolved around selling hardware and support for that equipment in the form of maintenance contracts. These contracts typically cover software updates, call support, and the physical upkeep of equipment.

Currently hardware and maintenance make up 40% and 30% of revenue, respectively. Hardware has 40% gross margins and maintenance comes with 80% margins.

Over the years, Avid became complacent. They failed to innovate and adapt to their customers’ changing needs. All the while, their hardware was becoming obsolete as computing power increased, allowing nimbler competitors to enter the market.

Usually, hardware updates were released every 12-24 months. But the industry’s requirements are evolving much faster than that with the proliferation of content across many more mediums (apps, different screen sizes).

Around 2014, Avid began shifting to software. By transitioning to the cloud, Avid became more operationally flexible, allowing them to innovate quicker. This is important because the subscription model isn’t simply about selling the same thing in a different way. It requires giving users new sources of value that didn’t exist in the old model such as remote collaboration.

The transition not only improved product quality, but changed their economics. Avid went from a product-driven hardware company with long-replacement cycles to a subscription model with steady and recurring revenues.

Transformation Successful So Far

While the groundwork for the transition began in 2014, it took some time for the industry to embrace the cloud. Their strategy just started hitting critical mass in 2018, then accelerated during the pandemic as users were forced to collaborate remotely. Since 2018:

- Subscribers grew from 150K to 480K

- Subscription revenue went from 9% of revenues to 35%

- Gross margins expanded from 58% to 65%

- EBITDA margins jumped from 12% to 20%

Valuation

I first lay out the math underlying the valuation, then I’ll dig into the assumptions.

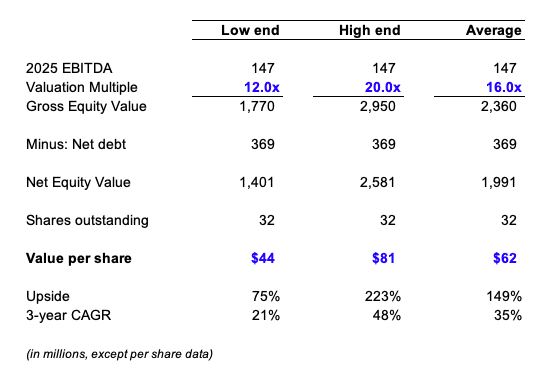

personal estimates

I arrived at a 3-year price target of $62 compared to the current stock price of $25. I used a valuation range of 12-20x, which I think captures a series of reasonable scenarios. At the low end of 12x, I calculated a $44 stock price. At the high end of 20x, the stock is $81. Averaging both gets us a $62 valuation.

Avid currently trades at 14.8x this year’s EBITDA. Although not cheap based on this year’s numbers, I think there’s a case to be made for multiple expansion. Optics matter here. Once the company derives a majority of its revenue from subscriptions, Wall Street will likely label it a “cloud” company. And cloud companies command higher valuations, partially due to the predictability of their revenue.

Adobe (ADBE) currently trades at 18.5x EBITDA, and traded as high as 22.0x before the market penalized them for the Figma acquisition. Adobe paid $20 billion for Figma, an astonishing 50x sales. More broadly, this acquisition highlights the value of software collaboration companies in a post-covid world. I doubt that Adobe will acquire Avid after Figma, but if a strategic buyer were to, it would come at a steep premium. Looking back, Adobe underwent a similar transition to the cloud that proved to be highly successful. It feels like a while ago, but Adobe used to sell their software in shrink-wrapped boxes before distributing it through subscriptions.

Assumptions

Starting with the top line, I project revenue increasing from $420 million this year to $530 million in 2025, an increase of $110 million or a CAGR of 8%. To put things into context, this year’s revenue is understated due to currency headwinds and the semiconductor shortage which pushed hardware sales out into next year. The true starting point is really around $450 million in revenue, which is a 5.6% CAGR to $530 million.

Digging deeper, revenue will be primarily driven by 3 factors—enterprise customers, individual users, and SaaS products.

First, the company will convert existing enterprise customers from hardware and maintenance contracts to subscription deals. This trend is just getting started.

- Avid has about 530 large enterprise customers, each having hundreds of users paying on a per seat basis.

- The last time they disclosed this metric at the end of the first quarter, only 65 of them or 12% were converted to subscription agreements.

Second, subscribers will come from individual users. Avid dominates the high-end business segment with customers like Disney (DIS), Netflix (NFLX) and Universal Music Group, but the market has expanded now that anyone can have a professional studio in their own home. Avid is targeting aspiring professionals as well as trained artists who self-publish. As a selling point, individuals could be incentivized to learn and use Avid’s tools if they hope to work for the larger studios one day.

Management estimates that individual creatives can increase revenues by roughly $120 million by 2025. My estimates aren’t as optimistic. Capturing market share with individuals is challenging because these users are more price sensitive and are siloed off in terms of their workflows, limiting network effects from gaining traction. I view this as an asymmetric option with low downside and high upside. The stock can still work without significant growth from individuals, but if they do execute—that’s just gravy on top.

Third, revenues will be bolstered by introducing new subscription products—specifically SaaS and cloud-based offerings. By shifting workflows to the cloud, creative work isn’t chained to the studio, but can be done from anywhere.

Data storage is another opportunity for the cloud, especially in video which takes up terabytes of data. Moving data from an on-premise server to the cloud makes it easier to store, retrieve, and distribute files, while also providing more security.

Media companies were forced to turn to the cloud during the pandemic, and Avid is building on their first-mover advantage here. They already signed some of the largest media companies to cloud contracts, including Amazon Studios (AMZN) and Paramount (PARA).

Cloud offerings made up only $7 million in revenues last year, but management expects it to grow to $25-45 million by 2025. At the midpoint of $35 million, this will account for about a third of my growth estimates. I think these are conservative assumptions given the multi-million dollar deals that they have already signed as well as the inevitable transition for the industry.

Margin expansion is the main driver of the model

I am forecasting EBITDA margins to expand from 20% this year to 28% in 2025. This estimate is reasonable for a company with 80%+ gross margins on subscription revenues and high operating leverage. Further down the road, I can see EBITDA margins exceeding 30% as they scale.

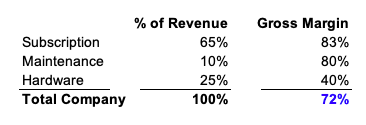

Mix shift accounts for most of the margin expansion. Currently, subscription and SaaS revenues make up 1/3 of revenues, but are growing at a 50% clip and are on pace to reach 2/3 of revenues by 2025. This revenue comes with 80%+ gross margins.

I think the market is underestimating the magnitude of margin expansion here as subscription becomes more meaningful. Assuming revenue is composed of 2/3 subscription with the remainder divided among maintenance and hardware, we arrive at a weighted average gross margin of 72% as shown in the math below:

company filings, personal estimates

Cost structure: As the company scales, opex as a percentage of revenues should drop from the high 40s to mid 40s. The company should achieve cost leverage in both G&A as well as sales and marketing. Further, G&A is a bit elevated now as the company is making a multiyear investment totaling $35 million to modernize their back office in support of their subscriptions and SaaS offerings.

Just to recap, bridging the 72% gross margins to the 46% in opex gets us to a 26% operating margin, plus 2% in depreciation gets us to structural EBITDA margins of 28%.

Buybacks to enhance value

Avid should generate close to $300 million in cumulative free cash flow over the next 3 years. Cash flow will not only be aided by margin expansion, but benefit from a tax shield (NOLs of $700 million), and from favorable working capital dynamics as the company’s new model requires less inventory and has upfront payments on software.

Additionally, Avid is able to borrow another $200 million (leverage of 2.5x), providing the company with a total of $500 million to buy back stock over the next 3 years. At the current valuation of $1.1 billion, the company could theoretically buy back 45% of outstanding shares over the next 3 years. In practice, I’m modeling in them repurchasing about a third of their shares. The amount bought back will be partially offset by price appreciation and stock options. I have the number of shares outstanding being reduced from 45 million to 32 million.

Avid telegraphed that stock buybacks are a priority, and they have been aggressively buying back their stock, having spent $65 million on repurchases since the middle of last year.

Risks

Cannibalization. Hardware and its associated maintenance revenues will decrease as subscriptions grow. Conversely, Avid will come out ahead as the conversion to subscription comes with an uplift of 1.2-1.4x in sales as well as higher margins.

Competition. Moving downmarket, Avid faces stiffer competition from established players including Ableton, FL Studio (formerly FruityLoops), and Cubase by Steinberg.

Conclusion

Film and music workflows will inevitably move to the cloud. Avid is leveraging their legacy to control the workflow of the future. They have already demonstrated success with their strategy. The heavy lifting has been done, and I think the company is positioned for their next phase of growth.

Be the first to comment