Justin Sullivan

AT&T Buy Thesis

AT&T Inc. (NYSE:T) has been put through the proverbial meat grinder, and raked over the coals for that matter. This has been primarily due to the fact that management has made some mistakes in the past. In fact, many market participants have become highly fanatical bears on the stock, stating that current management needs to be summarily dismissed before they will ever consider buying into the stock. Others state that AT&T’s extremely poor performance in the past is the reason why they wouldn’t touch it with the 10-foot pole.

Well, I can completely understand why they feel that way. In fact, I want to thank them very much for their hard work beating down AT&T’s stock price to a point where it actually offers a very enticing buying opportunity! You see, investing in stocks is completely counterintuitive to human nature. My personal catchphrase for the situation AT&T’s stock finds itself in is, “Bad news and buying opportunities go hand in hand.” On top of this, those who are so focused on the past and repeating the negative mantras of the past have missed the fact that AT&T is actually performing quite well at present. In the following sections, I will list off the reasons why AT&T makes for an excellent “safe haven” play, as we are more likely than not on the precipice of a recession of some magnitude.

AT&T Pays A Hefty, Well-covered Dividend

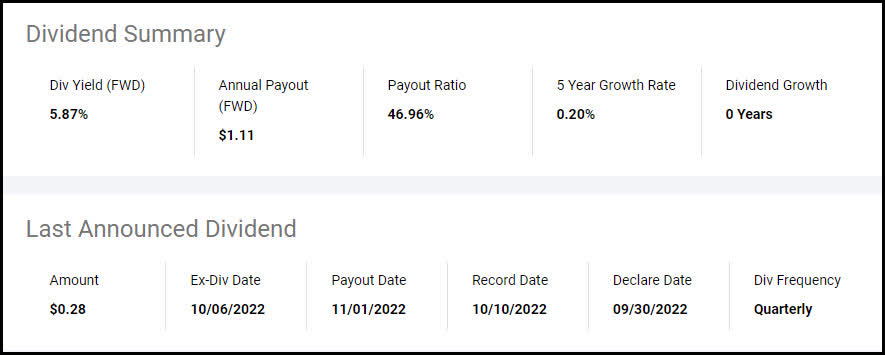

The first thing I look for in one of my “high conviction” safe haven plays is a substantial dividend that is well covered. AT&T has that.

Seeking Alpha

According to Seeking Alpha, AT&T pay a quarterly dividend with a healthy yield of 5.87%. The dividend is well-covered, with a payout ratio of merely 46.96%. I have no worries that the dividend will be cut. Some point to the fact that the company actually just cut the dividend when they sold off the Time Warner media assets. The fact of the matter is, the revenues and earnings from those assets went away along with the sale. So, the company “right-sized” the dividend in order to keep the ratios inline. Those who were expecting the company to continue paying the dividend after selling off a huge chunk of EPS had wildly extravagant expectation to say the least.

Now, the next thing I look for in a safe haven play is a solid valuation. The company needs to be selling for a decent valuation or preferably undervalued if possible. Let’s take a look at AT&T’s valuation statistics.

AT&T’s Valuation Analysis

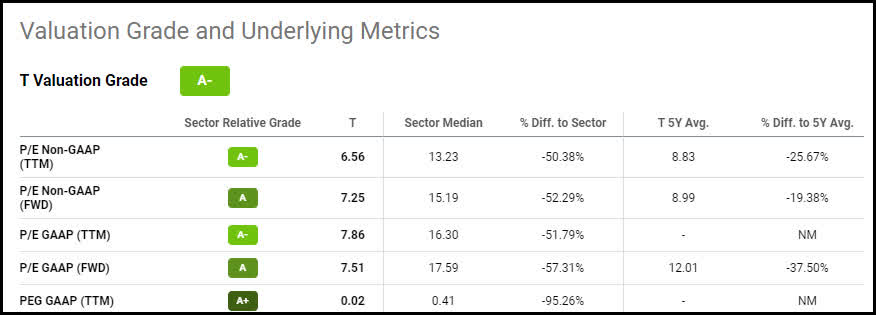

According to Seeking Alpha’s underlying valuation metrics, AT&T scores an A- grade as far as its current value.

Seeking Alpha

In fact, AT&T is trading at a significant discount both to its peer group and on a historical basis. It’s basically a steal right now, even though it has spiked up about 15% since reporting last quarter’s earnings.

AT&T Is Growing And Cash Flow Positive

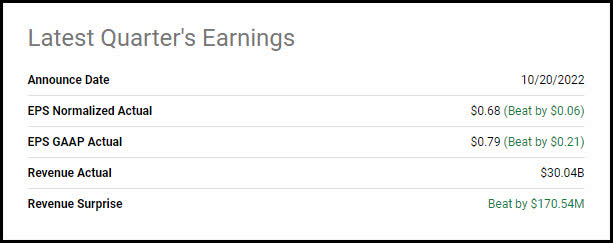

Which brings me to my next point: the company is free cash flow positive, beating earnings estimates, and growing like a weed according to the latest earnings report. Another key factor I look for in a safe haven play is proof the company is executing on plan by beating or exceeding earnings expectations. AT&T has done this.

Seeking Alpha

AT&T beat on the top and bottom lines last quarter. According to Seeking Alpha News, the highlights were:

“The company added 964,000 total subscribers, including postpaid phone subscribers during the period, bringing its total to 2.2M through the end of the third-quarter.

The company added 708,000 total postpaid phone subscribers during the period, bringing its total to 2.2M through Q3. Wireless service revenue grew 5.6% year-over-year, the highest in over a decade.

AT&T (T) said its addition of 338,000 Fiber subscribers was its second-best quarter for subscriber growth in its history.

Breaking it down further, AT&T (T) said mobility revenue for the period was up 6% year-over-year to $20.3B, including equipment revenue of $4.9B, thanks to “increased sales and mix of higher-priced smartphones.”

So, the company not only provides a hefty dividend payment of nearly 6%, but also the opportunity for capital appreciation due to the substantial growth prospects detailed in the latest earnings report. In fact, AT&T scores an A+ in regard to Seeking Alpha’s revisions metric.

Seeking Alpha

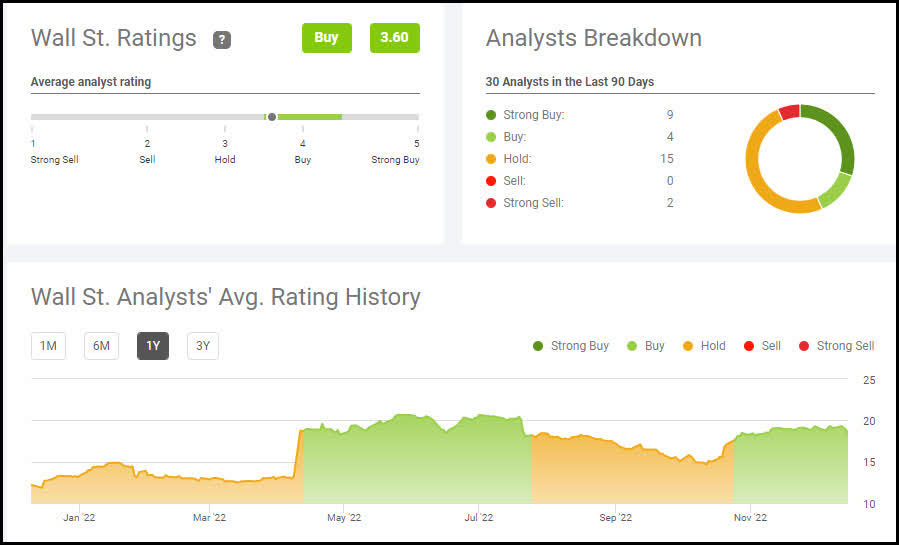

AT&T received 24 EPS and 17 revenue upward revisions to its earnings potential over the last three months. This is a very bullish sign that the company is making all the right moves. What’s more, the company rates a BUY by a majority of Wall Street Analysts, according to Seeking Alpha.

Seeking Alpha

Furthermore, by reviewing the chart, you can see that the upgrades from HOLD to BUY just recently occurred in November. This means you haven’t missed the boat just yet – but it is about to shove off. Now, let’s take a look at the current technical status and my 12-month price target.

AT&T Technical Outlook And Upside Potential

AT&T’s stock is well positioned at present technically.

Seeking Alpha

The stock is trading down about 3% today along with the rest of the market. This is exactly the time to strike. The stock has the 50-day SMA just below it, serving as strong support from further downside. Moreover, it has been consolidating at this level for over a month, increasing the odds it will take another leg higher in the near future and pierce through the top of the current trend channel. I see the stock requiring the $21 level within the next 12 months. This implies 17% upside from current levels coupled with the 6% yield, and if this happens, you have a nice 23% gain on your hands. Not too shabby for the current times.

Now, of course, I can already hear the boobirds in the background bringing up the “massive” debt issue AT&T supposedly has. Let’s take a moment to address that.

AT&T’s Debt

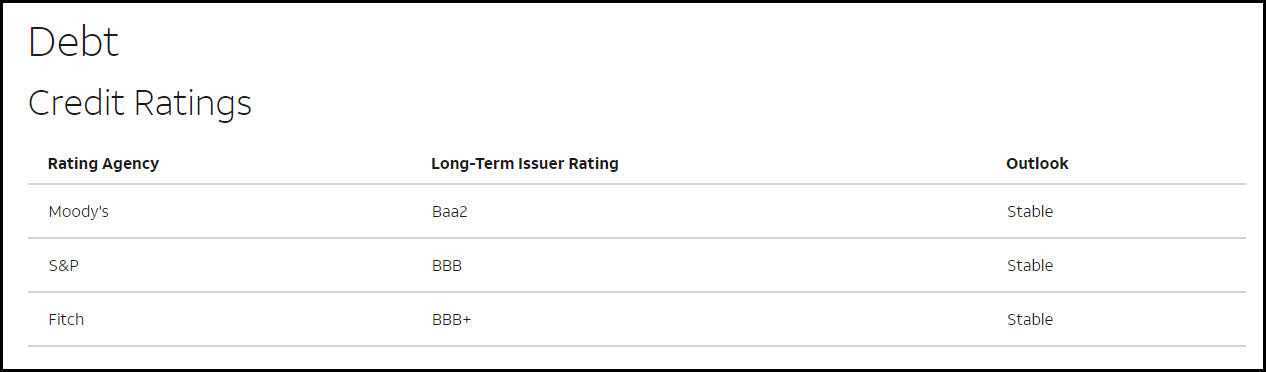

Yes, AT&T has a large debt load. Yet, the thing many don’t take into consideration is a majority of the debt is extremely long term and fixed.

AT&T

In fact, all three rating agencies have AT&T’s debt rated as stable. The fact is that only a very little slice of the debt load is short term, and even a smaller portion of the debt is floating. You can review the actual debt maturity table for yourself here. A majority of the debt comes due over 10 years out, from spanning 75 years all the way to 2097. So, the constant debt “disaster” and “mismanagement” prognostications I submit are somewhat misinformed to say the least.

In my eyes, they have done an extraordinary job of managing the debt. Now, let’s tie a bow on this piece.

Investor Takeaway

We are heading into a time when the markets may experience some significant downside based on the fact the Fed is actually doing their best to purposely bring the markets down. I see a recession on the horizon of some magnitude. It is times such as these when it pays to find shelter from the coming storm in solid safe-haven stocks.

AT&T check all the boxes. It has a very low beta score of 0.57, which means it tends to move up or down at about half the pace of the market. Its primary business of wireless phones is basically a utility at present. No one goes anywhere without their phone these days. It will definitely be the last thing people decide not to pay in a crunch. You have to have a phone these days to operate in this world, no doubt.

AT&T Inc. is profitable, has solid free cash flow, and pays a nice dividend. Tack on the 17% upside potential, and you have the recipe for a winning investment. Always layer in to any new position over time to reduce risk. Those are my thoughts on the matter, I look forward to reading yours!

Be the first to comment