bunhill

AT&T Inc. (NYSE:T) delivered a mixed bag in its recent FQ4 earnings release last week. However, it was still enough for an initial post-earnings rally that re-tested its November highs and held firmly.

But, before investors consider adding exposure at the current levels, it’s important to note the company’s weaker-than-expected guidance. Still, some T bulls could point to Verizon’s (VZ) recent report, as the company also delivered a soft outlook.

Moreover, T’s valuation remains undemanding compared to its peers’ median. As such, it’s possible for T to continue consolidating constructively, even as the macro headwinds could worsen.

Accordingly, management accentuated its confidence that it would tide through the macro headwinds confidently, as CEO John Stankey articulated:

We know that the services that we provide to customers are pretty resilient even during more [challenging] economic times. And so we have a reasonably high confidence level that our customers are going to continue to want to use the product and pay us for it. (AT&T FQ4’22 earnings call)

But, is management’s confidence contemplated in its forward guidance? Actually, we think it is.

The company is confident that wireless service revenue (up 4% or more) and broadband (up 5% or more) revenue could continue to drive revenue growth in 2023. Hence, management expects “to grow total revenues” in 2023. Accordingly, its cost rationalization is also expected to improve further, coupled with $2B in working capital benefit driving a 3.3% uptick in its adjusted EBITDA guidance.

Now, we know the metrics may not sound exciting for growth-oriented investors, but AT&T is still a highly profitable company. It’s expecting to report $16B in free cash flow (FCF) for FY23, up more than 14% YoY.

Moreover, it’s also above the Street’s previous October estimates, which projected negative revenue growth for FY23, and an adjusted EBITDA uptick of less than 2%.

Hence, it’s clear that Stankey & team are confident of exiting FY23 in better shape than expected.

So, what’s driving the company’s confidence in a potentially slower growth environment, even as CapEx outlay is projected to be $24B, in line with FY22?

Management is confident that promotional spending should be less intense in FY23. As such, it should help AT&T improve its value proposition without competing over-aggressively with its arch-rivals.

Moreover, the company expects a further buildout of its fiber advantages could lend further momentum to improving its network capability. It’s also leveraging on its “capital-light” partnership with BlackRock (BLK) to lead in the expansion of its fiber network to more than 30M locations.

Hence, should investors consider T at these levels, anticipating a 3.3% adjusted EBITDA growth in their modeling?

Investors need to consider which side they are on: Fed pivot or no Fed pivot. We may get to know soon as the FOMC gathers for its conclave on January 31 to February 1, with a presser scheduled.

If the Fed stays hawkish, it could affect investors’ confidence in the company’s ability to achieve its $6B+ run rate in cost savings, which is critical to driving its profitability recovery. Furthermore, consumer spending could weaken further, affecting AT&T’s ability to meet its more optimistic revenue growth profile.

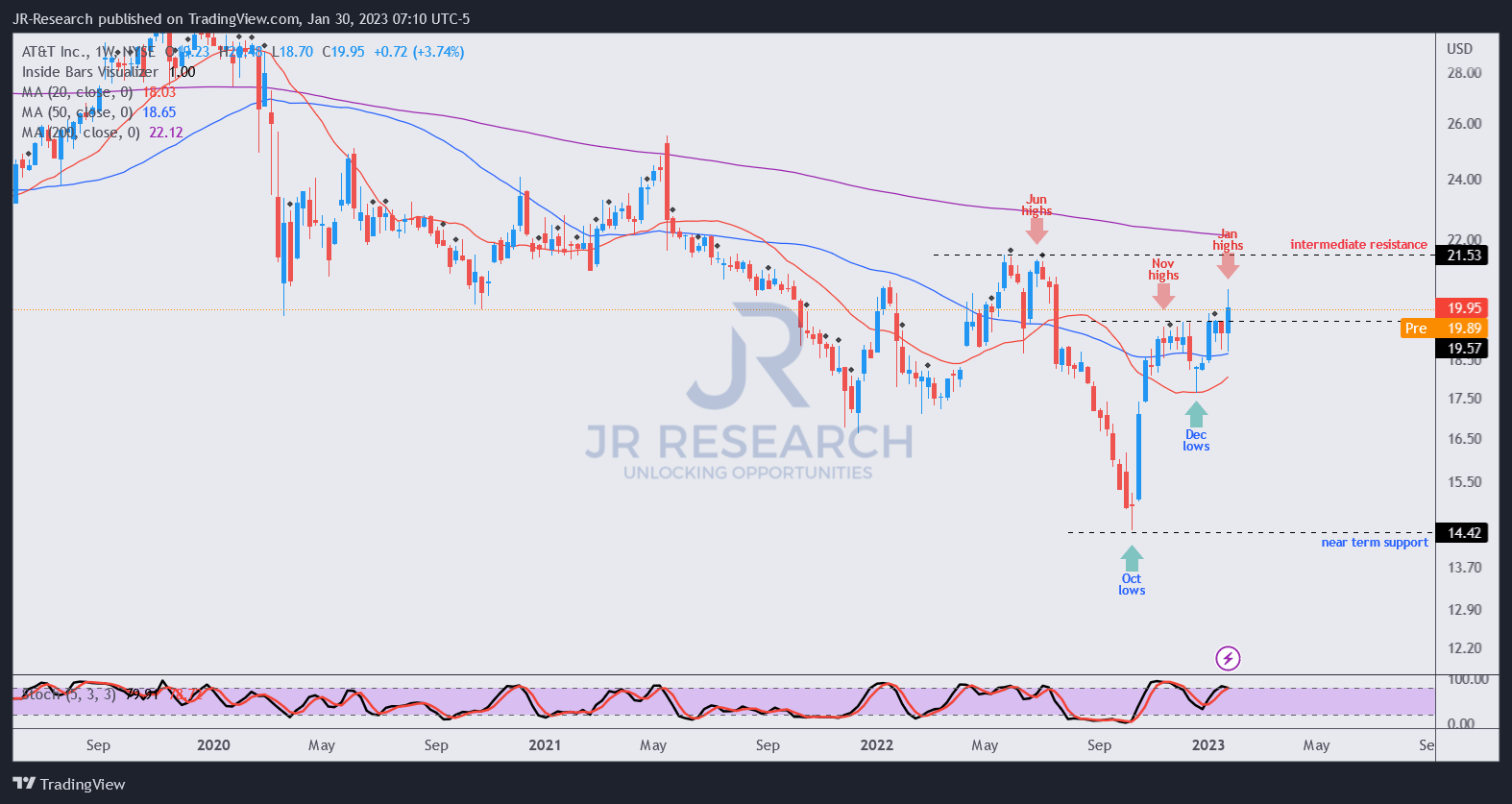

T price chart (weekly) (TradingView)

Furthermore, T is no longer trading at dislocated levels seen in October, when pessimism reached a crescendo.

While T has consolidated constructively along its November highs, retaking its June 2022 highs (its next resistance zone) could prove challenging if the Fed remains hawkish.

Hence, we assessed that a buying opportunity in T seems relatively well-balanced and don’t regard it as attractive.

Rating: Hold (Reiterated).

Be the first to comment