Melpomenem

A man is rich in proportion to the number of things which he can afford to let alone.”― Henry David Thoreau, Walden.

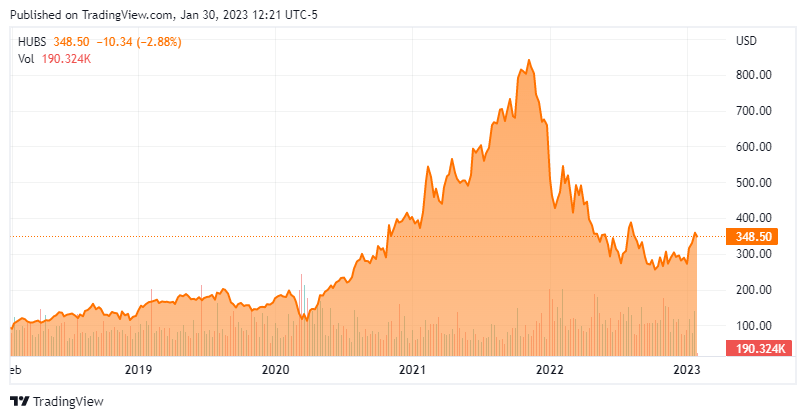

Today, we take our first look at software maker HubSpot, Inc. (NYSE:HUBS). Like most growth names, the stock was hit hard in the markets due to rising rates and growing concerns about economic growth. The company should report fourth quarter results soon (expected 2/16 after the close) and insiders have been selling shares in this equity early in 2023. The shares do appear to be trying to form a floor near current trading levels. Too soon to buy the pull back? An analysis follows below.

Seeking Alpha

Company Overview:

Hubspot, Inc. is an application software company based just outside of Boston, in Cambridge, MA. Hubspot has developed and provides a provides a cloud-based customer relationship management or CRM platform for businesses. Among the capabilities Hubspot’s platform offers to customers are:

November Company Presentation

Marketing, sales, service, and content management systems, as well as integrated applications, such as search engine optimization, blogging, website content management, messaging, chatbots, social media, marketing automation, email, predictive lead scoring, sales productivity, knowledge base, commerce, conversation routing, video hosting, ticketing helpdesk tools and customer NPS surveys.”

In addition, the company professional services to educate and train customers on how to leverage its CRM platform, as well as phone and/or email and chat-based support services. HubSpot, Inc. stock currently trades around $350 a share and sports an approximate market capitalization of $17.5 billion.

November Company Presentation

Third Quarter Results:

On November 3rd, Hubspot posted its third quarter numbers. The company had a non-GAAP profit of 69 cents a share as revenues rose some 31% on a year-over-year basis to nearly $444 million. Non-GAAP operating income for the quarter was $40.7 million, up from $32.9 million from the same period a year ago. Both top and bottom line numbers nicely beat expectations. Leadership revised its Q4 guidance slightly to $444 million to $446 million which was a tad below the consensus at the time. Full year 2022 was right at $1.7 billion, in line with analyst firm estimates.

November Company Presentation

Q3 subscription revenue came in at $435 million, up 32% from 3Q2021 while professional services sales fell 13% from the same period a year ago to $8.9 million. The company’s customer base grew 24% over the year ago period while the average revenue per subscriber was up seven percent to just north of $11,000. Non-GAAP operating margin fell to 9.2% from 9.7% in the prior period despite sales growth north of 30%. GAAP net income was a negative $31.4 million for the quarter as well compared to negative $13.9 million for 3Q2021.

November Company Presentation

Analyst Commentary & Balance Sheet:

The analyst community still leans bullish on the stock. Since third quarter earnings posted, some 17 analyst firms including Needham and Bank of America have reiterated Buy/Outperform ratings on the stock. However, roughly half of these contained downward price target revisions. Price targets proffered now range from $350 to $475 a share, with most in the high $300s. This is not much over the current trading levels of the stock it should be noted. Credit Suisse did initiate the share as a new Outperform with a $400 price target. Both Evercore ($340 price target) and Oppenheimer ($375 price target) maintained Hold ratings on the stock.

Just over three percent of the outstanding float in the shares are currently held short. Numerous insiders were frequent and consistent sellers throughout 2022, disposing of tens of millions of dollars worth of shares in aggregate during the year. That hasn’t change so far in 2023. So far in January, they have sold more than $15 million worth of equity here in January to date. I can’t find a single insider buy in this stock since the company went public.

The company ended the third quarter with $1.4 billion of cash and marketable securities on its balance sheet. HubSpot has just north of $450 million in long term debt. The company did produce $35.5 million in free cash flow in the third quarter, which was down slightly from the $38.2 million in free cash flow delivered in 3Q2021.

Verdict:

The current analyst firm consensus has the company earning nearly $2.50 a share in FY2022 as revenues rise some 30% to $1.71 billion. They see sales growth slowing to approximately 20% in FY2023 and earnings ticking up to $2.83 a share. This would be significantly under growth levels of the past half decade.

November Company Presentation

The stock of HubSpot, Inc. has been more than cut in half since its all-time highs in late 2021. Even with the huge pullback, the equity goes for more than 100 times earnings and and ten times sales. Valuations are a bit cheaper equating for the net cash on the company’s balance sheet.

Based on the third quarter run rate, HubSpot, Inc. has a free cash flow yield around one percent. And that is still “too rich” for me in this current market environment with sales growth projected to slow in FY2023 for this old poker player. Insiders also continue to take “chips” off the table in front of upcoming fourth quarter results. Therefore, I have no investment recommendation around this SaaS concern at current trading levels.

No man is rich enough to buy back his past.”― Oscar Wilde.

Be the first to comment