Whereas many blue-chips are down have lost 30%+ of their market caps already in this market rout, Walmart (WMT) shares have held up very well. Definitely in the near term, retailers are going to do very well, as the fear-led public will most likely continue stocking up at retailing outlets in their droves.

Investing in companies which sell the bare essentials definitely protects against downside risk over the long term. No matter how bad economic conditions get in the near term, people are going to still have to eat. Of course, every industry gets affected if disposable income were to plummet, but strong retailers such as Walmart will undoubtedly see less losses than firms in other sectors. In fact, in the near term, Walmart will continue to gain market share from more expensive retailers, restaurants, hotels, and other fast-casual dining establishments etc.

However, the difference between the present environment and 2008 is that this is also a health crisis. In fact, one of Walmart’s workers tested positive for the COVID-19 virus recently. Being at the cold face, workers at retailers like Walmart are more at risk of contracting the virus. We don’t believe though with the premise that more announcements concerning coronavirus in Walmart will deter customers from buying product. Why?

- Although online purchasing will come under huge pressure in the short term, the coronavirus will definitely increase the number of customers using the service, most likely from the elderly demographic. Again, we see Walmart gaining share here, as it has invested millions into its e-Commerce division over the past few years. Other retailers who have not invested as aggressively will now pay the price for not taking more risk.

- We believe it is only a matter of time before other retailers’ employees contract the virus. In fact, Starbucks (SBUX) reported that one of its employees has already tested positive for COVID-19. We believe soon enough that other retailer will follow suit, which will ensure Walmart will not be signalled out by customers at large.

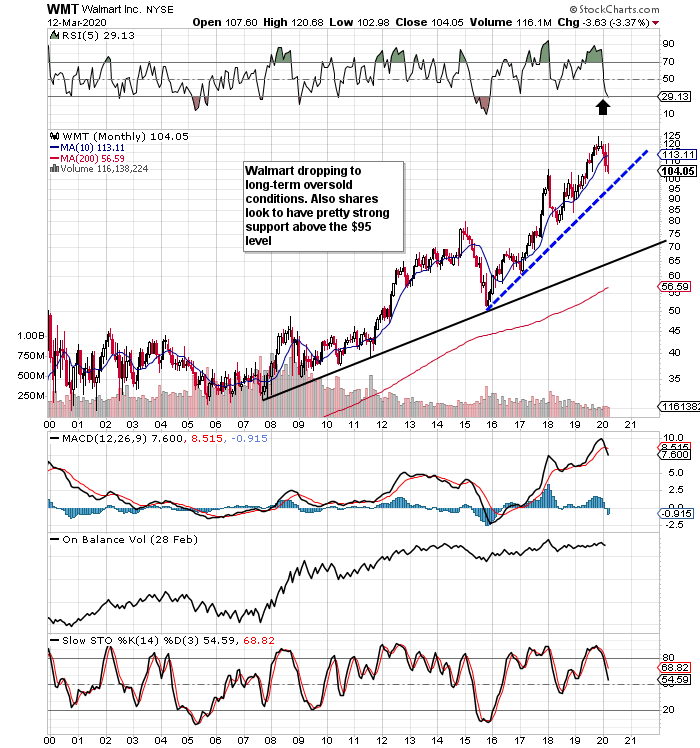

Walmart last month posted its fourth-quarter and full-year numbers last month. We continue to believe that this retailer is an excellent long-term investment. As we can see from the long-term chart below, the RSI indicator is now about to enter oversold territory, which, as shown, does not happen that often with Walmart.

{kind=link}

The biggest calling card when investing in this stock is the stability of its dividend. Recent annual numbers confirmed the sustainability of the dividend. With shares at a post-market price of $102.25 (March 12), the yield at present comes in at 2.11%. Although the dividend is only growing at about 2% a year on average, the low growth rate is not because of a lack of cash flow. In fact, the payout ratio has remained around the 45% mark for the best part of 3 years now.

We state this because when Walmart needed to make a big decision a few years back with respect to going toe to toe with Amazon, it did it. Yes, debt has increased at the firm, but in no way, shape or form has the balance sheet been derailed. Walmart, for example, consistently spends $10+ billion on capital expenditure every year, but has also spent $17+ billion on acquisitions over the past few years. We believe it will be only a matter of time before these investments drop down to show operating income growth, most likely from next year onwards.

Interest expense came in $2.41 billion in the retailer’s latest fiscal year, and operating income came in at $20.56 billion. This gives us an interest coverage ratio of 8.53, which again demonstrates that despite elevated spend in recent times, there is still plenty of scope to keep rewarding shareholders handsomely.

Therefore, to sum up, if Walmart were to drop to the $95 level, it would present an excellent buying opportunity, in our opinion. Yes, the dividend yield may be much lower than the average in this sector (2.78%), but few retailers have similar fundamentals. We sold out of this stock not a long while back very close to its highs. Let’s see if we can retime an entry in due course.

———————-

Elevation Code’s blueprint is simple. To relentlessly be on the hunt for attractive setups through value plays, swing plays or volatility plays. Trading a wide range of strategies gives us massive diversification, which is key. We started with $100k. The portfolio will not not stop until it reaches $1 million.

———————–

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment