Michael Vi

The massive order book is shielding ASML

ASML (NASDAQ:ASML) (OTCPK:ASMLF) posted another strong quarter of order growth with an €8.5 billion order intake, a net increase of over 5 billion. The €33 billion order book shields ASML against a potential downturn in the semiconductor industry.

Over the last weeks, we’ve seen worry about the semiconductor industry, because of profit warnings from Micron (MU) “because of cooling demand”. While chipmakers might see some cooling, ASML as the monopolistic EUV Lithography equipment manufacturer does not see any cooling at all, rather further heating up of its order intake.

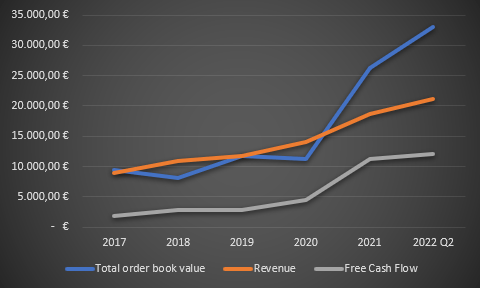

In the graphic below you can see that the order book value outpaced revenue and free cash flow growth in the last year. Before 2021 revenue and total order book value grew roughly in line. Starting in 2020 and accelerating in 2021 the world experienced a massive chip shortage

ASML order book growth (Authors model, data from ASML IR)

Macro and ASML competitive advantage

According to Industry Global News, the market for DUV lithography will grow from $11.6 billion in 2022 to $18 billion in 2028, a 9% CAGR. The other market ASML operates in is EUV, here Future Market Insights expects the market to grow from $4.6 billion by the end of 2021 to $23 billion by 2029, a 21.5% CAGR.

A true monopoly

Because ASML has a monopoly on EUV, it will be able to capture the entire market. Newly emerging competitors are unlikely due to the incredible complexity of the Extreme Ultraviolet lithography machines:

A EUV machine has over 100000 different parts, which are sourced from over 4700 different suppliers. ASML spent €9 billion in sourcing spend in 2021. ASML then assembles these parts over a several-month-long progress, does testing on the systems, disassembles the system again and ships the several hundred tons with multiple planes to the customer where it is reassembled again. Each current generation EUV machine costs around €160 million. Besides the incredibly complex construction of the system, ASML also develops proprietary software to enhance its systems and enable software updates (install base management accounts for almost 1/3 of revenues). Here is a great podcast episode that delves into why writing software for ASML’s machines is so complicated with Arnaud Hubaux, development lead for ASML.

Furthermore, ASML continues to develop new systems. At the beginning of the year, Intel (INTC) preordered the first ASML High-NA EUV system, which is estimated to be shipped in 2025. This system is just for testing purposes and will cost Intel upwards of $200 million. That way ASML can subsidize some of its R&D costs (they spent €2.9 billion in 2021).

Q2 Earnings

In this article, I’ll dive into the Q2 results and digest its implications for the company going forward in this uncertain time.

The raw numbers

First off, we’ll go over the reported numbers:

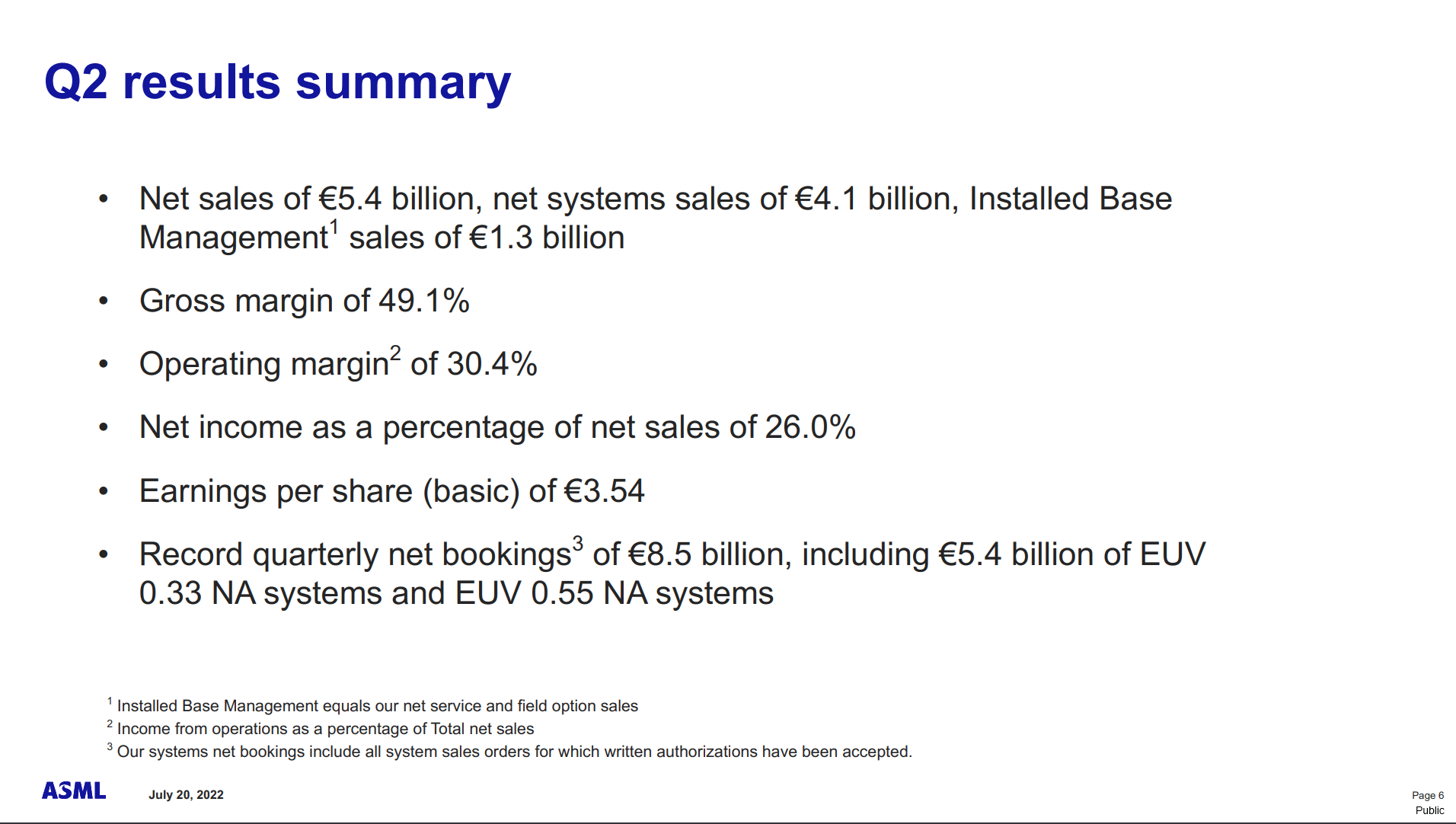

ASML saw 35% YoY growth to €5.4 billion in sales, beating the 5.1-5.3 billion guidance provided last quarter. This number is elevated from the revenue that was deferred last quarter.

Margins are down slightly YoY, due to higher fixed costs per shipped unit resulting from the deferred revenue.

As mentioned in the intro, bookings saw a record quarter with €8.5 billion. Especially the €5.4 billion in EUV NA systems is noteworthy, as these systems will be shipped far out in the future, around 2025. This is where a lot of future growth will come from once the technology is ready.

ASML Q2 summary (ASML Q2 presentation)

DUV export ban into China headlines

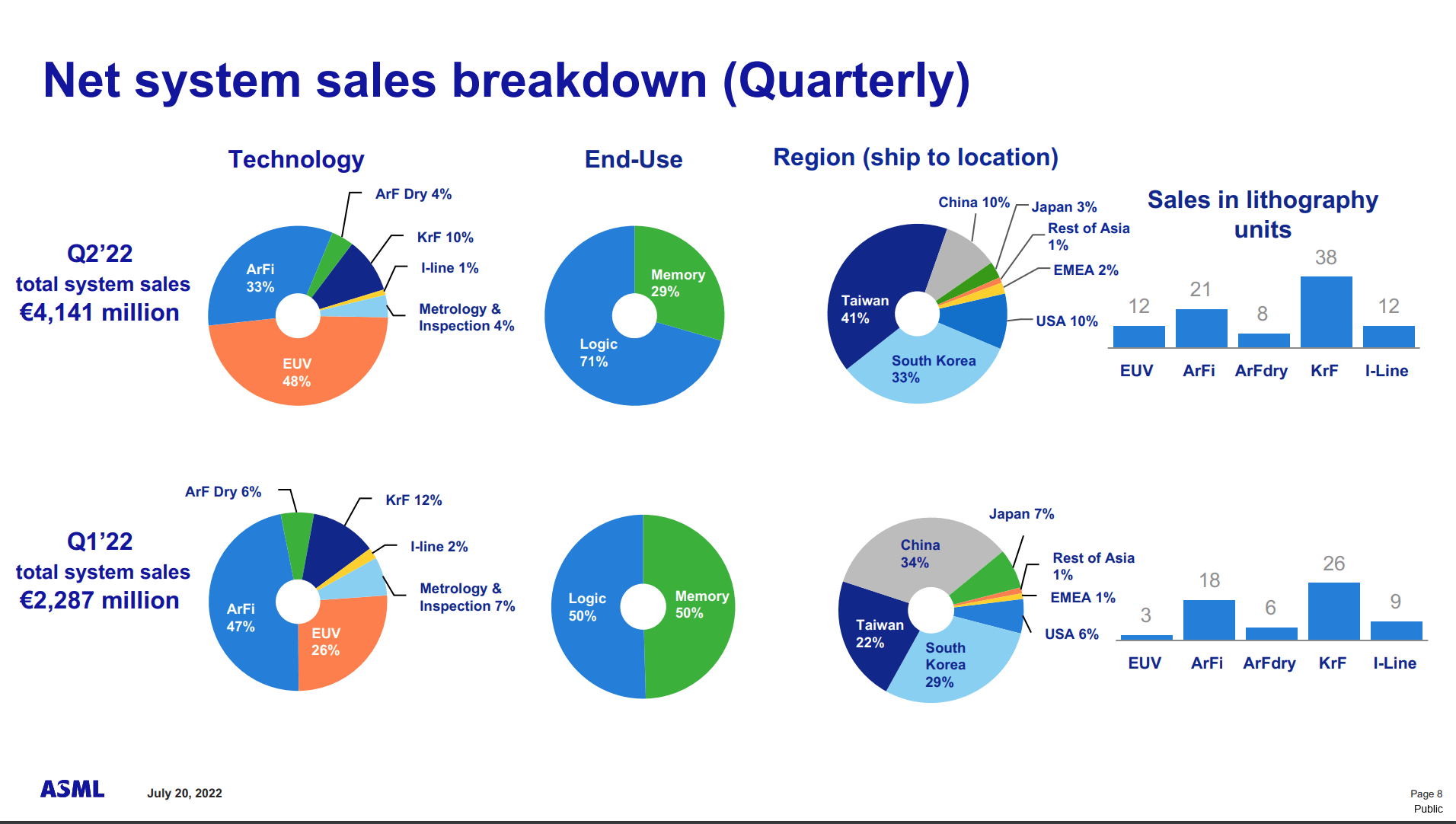

Recently, ASML made headlines when the US administration considered new sanctions on ASML, this time for the DUV business as well. Shares tumbled around 8% intraday on the news. I assume a big contributor was the large 34% revenue share China had last quarter. As we can see in the slide below, this quarter China accounted only for 10%, with EUV revenue picking up again. China is less of an issue than people might have thought, especially with the size of the order book.

ASML revenue breakdown (ASML Q2)

Dividend policy and guidance

ASML changed its dividend policy from a semi-annual to a quarterly payout model. The first payment is €1.37 on the 12th of August, so the total revenue run rate is unchanged compared to 2021 (€5.5 a share). I welcome this change, even though it changes nothing fundamentally it is more convenient to get a quarterly paycheck rather than twice a year.

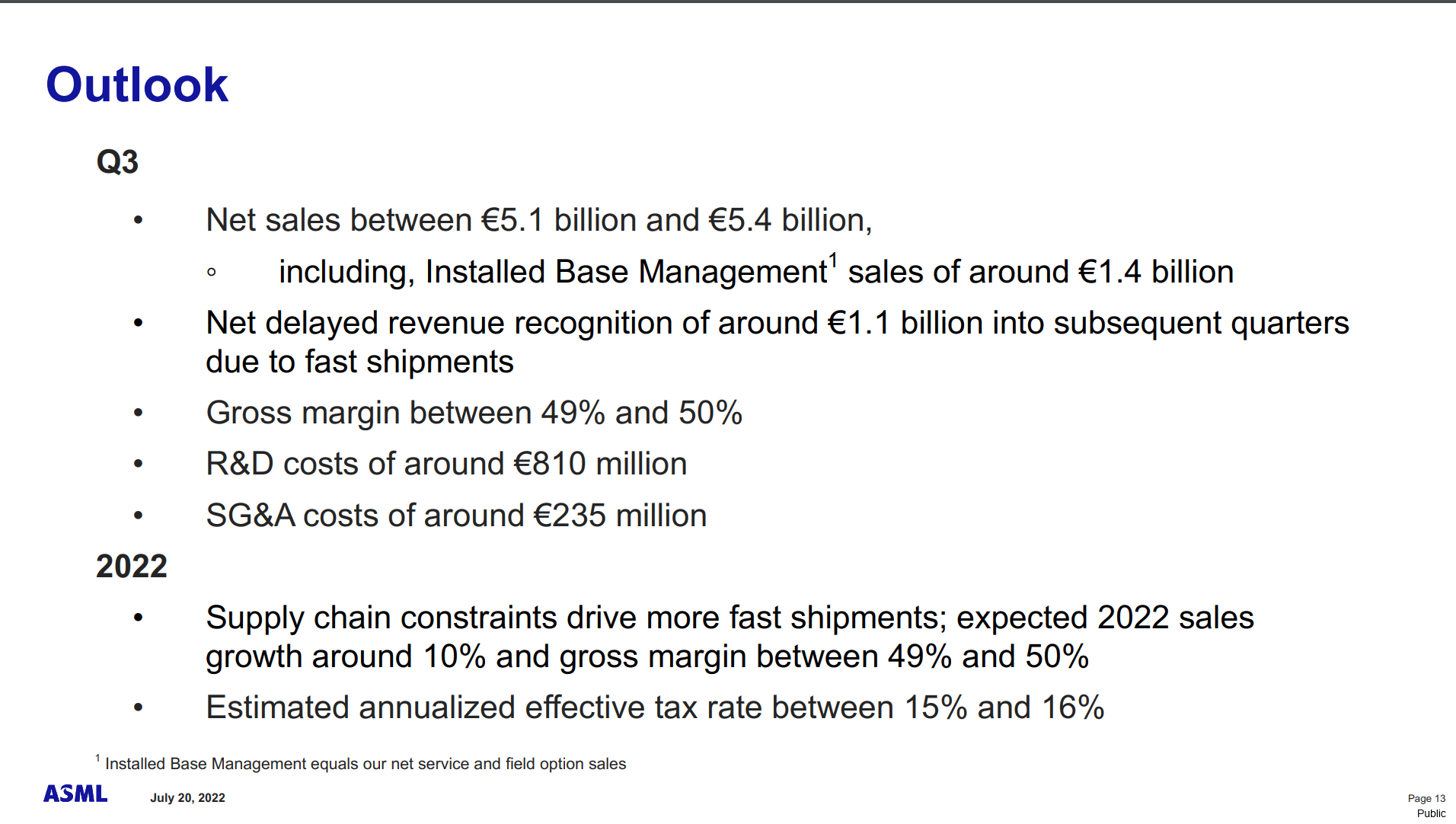

For Q3, ASML expects flat revenues, because of net delayed revenue recognition of €1.1 billion. These delayed recognitions will last for another quarter after this until ASML has a full year of comps with the fast shipment policy. Including deferred revenue, growth for the quarter is expected between 21 and 25%.

The same story goes for the full year. Guidance was cut from 20 % to 10%, but 10% of growth is deferred into 2023. ASML continues its strong growth trajectory in this challenging environment for the chip industry.

ASML guidance and dividend policy change (ASML Q2)

Noteworthy remarks from the earnings call

The full earnings call transcript can be found here.

A weak consumer, but strong secular trends

To start, we have a rough overview from the CEO. We are probably already in a recession and that also shows in the chip sector: The consumer is slowing down, while secular growth trends like high-performance computing and automotive are still seeing high demand.

Looking at the more near-term market dynamics, we see a couple of mixed messages. Some customers are indicating they are seeing signs of slowing demand in certain consumer-driven market segments, primarily PCs and smartphones. Other market segments like high performance computing and automotive are still seeing strong demand.

Peter Wennink, CEO

Are chipmakers canceling orders?

Common speculation over the last months has been that ASML might see canceled orders through double-orders and a general reduction in capital expenditures from manufacturers. Here are three statements that tell a very clear picture about the priority ASMLs systems have for their customers, and that lithography systems aren’t the place where they are saving money right now:

” they pick up the phone and if they tell us, “Listen, we talk about weakness, but don’t you guys dare to just change your shipment pattern to us?” So, this is what I’m holding on to. That is why we have this big order backlog, and we know where to ship to. “

” the only cancellations I can remember were — was a customer actually canceled orders because they wanted to replace that tool type with a new tool type is the kind of cancellation that we are getting, so. And yes, this is actually not what we’ve seen in the past. “

“customers are pushing for faster shipments. Customers aren’t asking to have these tools later. That just isn’t happening”

DUV is still growing strong

For ASML all eyes are on EUV, but we shouldn’t underestimate DUV. Although ASML has some competition from Canon and Nikon in this segment, they are still the undisputed leader. DUV is needed in a lot of segments, I also wrote about this in my Texas Instruments article a while back in more detail, and has a lot of growth tailwinds as you can read in the quote below. “The internet of everything”, as Peter Wennink likes to say is fueled by chips in all sizes and forms.

DUV usage globally is a lot higher than 2-3 years ago, driven by automotive, sensors, IOT, energy transition[…].

Fast shipping might be here to stay

Driven by supply chain, shipping constraints and demand too high to handle ASML started to do fast shipping for a part of its machines. With fast shipping some of the testing phases are not done in the ASML facilities, but rather the machine is shipped to the customer and the final testing is done there. This saves time and did not impact the quality of the machines in the few quarters ASML did this practice.

Now that we’ve done it we might like it and make it our standard.

Roger Dassen, CFO

A recurring situation in the last two earnings was the deferred revenue from fast shipments. Asked about the impact of fast shipments on cash flows, Dassen stated that there is no cash flow impact on fast shipments.

Capacity expansion plans are on track

ASML reiterated its short-term goal of expanding capacity to 60 EUV and 375 DUV systems for 2023. The medium-term goal of 90 EUV, 600 DUV and 25 High-NA systems in 2025 also stands and is being discussed with the supply chain. The investor day in November should have some details regarding the situation for us.

Backlog is mostly cutting-edge

Another reason why ASML is well off even if a semiconductor bust is going to happen is the quality of the order book:

85% of backlog is EUV and immersion for advanced nodes

These are the type of products that aren’t getting canceled, or as Wennink said:

“innovation won’t stop”.

Reasonable valuation based on inverse DCF

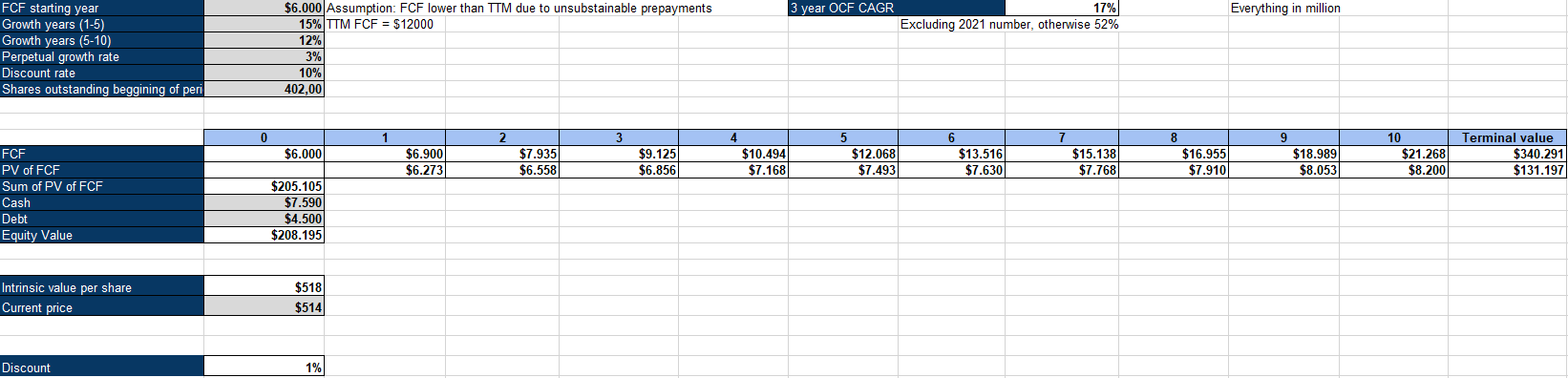

I valued ASML based on an inverse DCF model. I took a conservative $6 billion of Free Cash Flow, half of the current TTM figure, to account for a drop in FCF against tough comps from the large prepayments ASML received with the increased order books. Based on a $6 billion starting FCF, a 3% perpetual growth rate and a 10% discount rate ASML, the market expects ASML to roughly grow 15% in the next 5 years, then decelerating to 12%. This model does not factor in share repurchases, which ASML historically did by around 1% of shares outstanding a year. Given the current 20% YoY growth guidance (including deferred revenue) and long-term tailwinds, I believe ASML to be at a fair value.

ASML inverse DCF (authors model)

Conclusion

ASML remains one of my highest conviction bets. The company continues to show great operational resilience now and in the future, shielded by a full order book. The company may not be a steal, but it’s at a fair value. I’ll end this article with a quote from Warren Buffett:

It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

Be the first to comment