tommaso79

China Remains a Headwind But What’s the Story?

I’ve written numerous Seeking Alpha articles about the impact of U.S. sanctions on lithography equipment from ASML (NASDAQ:ASML), specifically DUV (EUV is already sanctioned and will remain so). ASML has been able to ship DUV and i-line to China, and I reported for the first time that China foundry SMIC was able to make chips at the 7nm node without EUV in my May 18, 2022 Seeking Alpha article entitled “Applied Materials: SMIC Move To 7nm Node Capability Another Headwind.”

Skip Miller – Vice President Investor Relations Worldwide noted at the UBS 2022 Global TMT Conference on Dec. 6, 2022:

“We had an indirect, potential indirect impact. By that, we mean that if these Chinese customers that are — have a targeted technology are unable to secure non-litho equipment for these particular technologies, will they take litho? And that’s a question mark. And so because of a question mark, we define quantified in our backlog, what would be in this category in the, particularly, in DUV.

And we quantify that as 5% of our backlog. Our backlog being $38 billion so that quantify the number, but again, that depends on their decision and whether they’ll take those litho tools in spite of the current new changes to some of the other non-litho areas as it relates to export controls.”

In other words, ASML is assuming it can continue to ship DUV lithography systems to China. But because of current sanctions on processing equipment like etch and deposition from Applied Materials (AMAT) and Lam Research (LRCX), Chinese companies may not want the DUV lithography systems because this equipment is needed for multiple patterning processes to enable the DUV systems to reach the <10nm nodes. Otherwise the lithography systems can only reach 37nm pattern delineation.

I discussed these sanctions in a January 3, 2023 Seeking Alpha article entitled “U.S. Sanctions Are A Catalyst For China’s New Semiconductor Fab Expansion,” noting:

“Keep in mind that the recent U.S. Department of Commerce restrictions are meant to deter China’s access to and ability to make advanced chips at the following thresholds:

- Logic chips with non-planar transistor architectures (i.e., FinFET or GAAFET) of 16nm or 14nm, or below;

- DRAM memory chips of 18nm half-pitch or less;

- NAND flash memory chips with 128 layers or more.”

Importantly, ASML’s issues are not on two fronts:

- China my not buy DUV because it will do them no good because process equipment is sanctioned to enable them to reach <10nm.

- DUV lithography equipment may still be sanctioned.

Both ASML, a Dutch company, and Tokyo Electron (OTCPK:TOELY), a Japanese company are balking that they are being forced to comply with U.S. sanctions.

On Dec. 14, 2022, a Bloomberg article entitled “ASML’s CEO Pushes Back on Further Export Restrictions to China” implies that the issue remains. According to the article:

“Dutch chip-gear giant ASML Holding NV has “given up enough” with the pre-existing restrictions on its sales to China, Chief Executive Officer Peter Wennink said.

With an effective ban already in place on its cutting-edge extreme ultraviolet lithography, or EUV, machines, ASML “has already surrendered,” Wennink told Dutch newspaper NRC in an interview late Tuesday. Wennink said US chip-gear makers benefited from that restriction as more than 25% of their revenue comes from China, whereas the country accounts for 15% of ASML’s sales.

An ASML spokesperson confirmed the comments to Bloomberg News on Wednesday.”

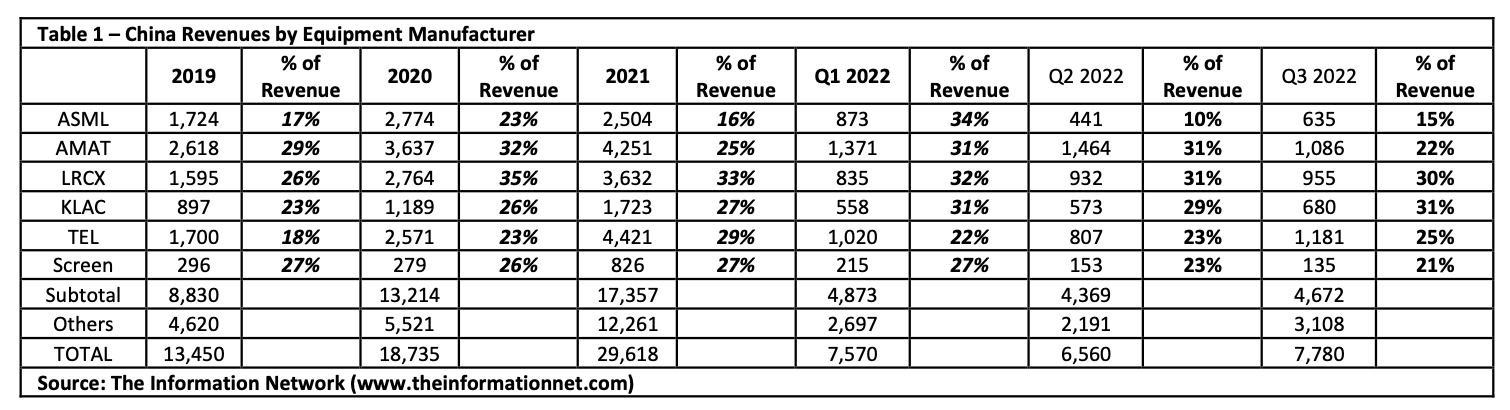

One final word on the Chinese sanctions, as I said above ASML is quantifying the sanctions on processing equipment at 5% of its $38 billion backlog. That value would be $1.95 billion. Yet ASML generated $2.5 billion in revenues from China in 2021 and YTD $2.0 billion for 2022, as shown in Table 1 below.

The Information Network

A Huge and Significant Backlog

ASML has a significant backlog of $38 billion. EUV is roughly $20 billion of that $38 billion, so $17 billion of that is for non-EUV systems.

ASML’s backlog comes from two factors:

- Strong demand as the company has limited competition but is also production limited, and ASML has said several times it was increasing capacity.

- Significant supply-chain problems that have impacted shipments.

I relate this question to one that I raised on several Seeking Alpha articles that I wrote in the past year, which has to do with the fire at ASML’s EUV facility one year ago on January 3, 2022. In the 1-year period, ASML announced an update only a week later, that’s all. More can be learned in my July 21, 2022 Seeking Alpha article entitled “ASML: January Fire Responsible For Big Revenue Pushouts To 2023.”

In that article I noted:

ASML experienced a fire at its facility in Berlin, Germany, that impacted EUV production. That was Jan. 3, 2022, and more than six months have elapsed through two earnings calls and ASML has not used the term “fire” in a press release or earnings call. ASML can only say in its Investor Call prepared remarks:

“We are experiencing increasing supply chain constraints which resulted in delayed system starts and requires us to increase the number of fast shipments in Q3 in order to supply our customers with systems in production as quickly as possible. With more fast shipments planned in the quarter, it will increase the amount of revenue delayed to subsequent quarters.”

I pointed out in my April 26, 2022, Seeking Alpha article entitled “ASML: Dissecting An Incredibly Poor Q1 2022 And Earnings Call,” ASML purposely didn’t provide an update of a fire impacting its EUV production, yet ASML was paid for only three systems compared with 11 the previous year.

In an attempt to educate analysts and investors, what ASML is doing is shipping incomplete EUV systems to customers, as I explain in my article:

“Because of the complexity of the EUV systems, ASML has a unique way of categorizing EUV sales vs. shipped. ASML uses the term “fast shipments,” which is in support of customers’ desire to bring systems into production as quickly as possible. By skipping some of these testings in its factory, ASML can shorten the cycle time. Final testing and formal acceptance then take place at the customer side, at which time ASML will recognize revenue.”

Currently “fast shipments” are significant. As ASML’s Skip Miller notes:

“We currently have $2.2 billion coming out of 2022 into ’23, and depending on how fast shipments evolve, we may have some coming out of Q4 next year unless we’re able to result some of the accounting issues with respect to revenue recognition.”

On the “accounting issues”, ASML is trying to get customers to accept the EUV lithography system on the basis of testing done at ASML, rather than at testing of the incomplete system at the customer’s fab.

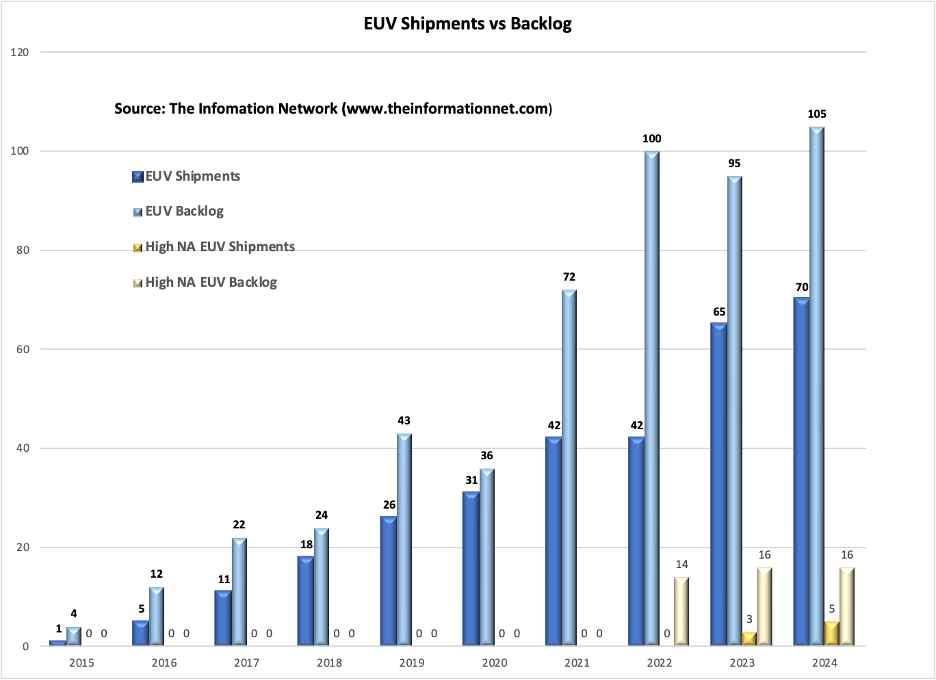

Chart 1 illustrates EUV shipments (units) from 2015 through 2024 (my estimates) for standard, low NA systems and the upcoming “high EUV” systems. It also shows my analysis of the backlog, which in 2024 will be 105 low EUV and 16 high EUV.

The Information Network

Chart 1

In ASML’s Investor Day 2022 presentation, the company announced:

-

We plan to adjust our capacity to meet future demand, preparing for cyclicality while sharing risks and rewards fairly with all stakeholders.

-

We plan to increase our annual capacity to 90 EUV and 600 DUV systems (2025-2026), while also ramping High-NA EUV capacity to 20 systems (2027-2028).

Current capacity is 55 EUV systems.

Investor Takeaway

Guidance for ASML’s Q4 2022 Earnings Call

ASML reported for Q3 2022 revenue of €5.8B and expects Q4 2022 net sales between €6.1B and €6.6B. Midpoint, that represents a growth of 8%. That would be significant given the state of the memory IC sector.

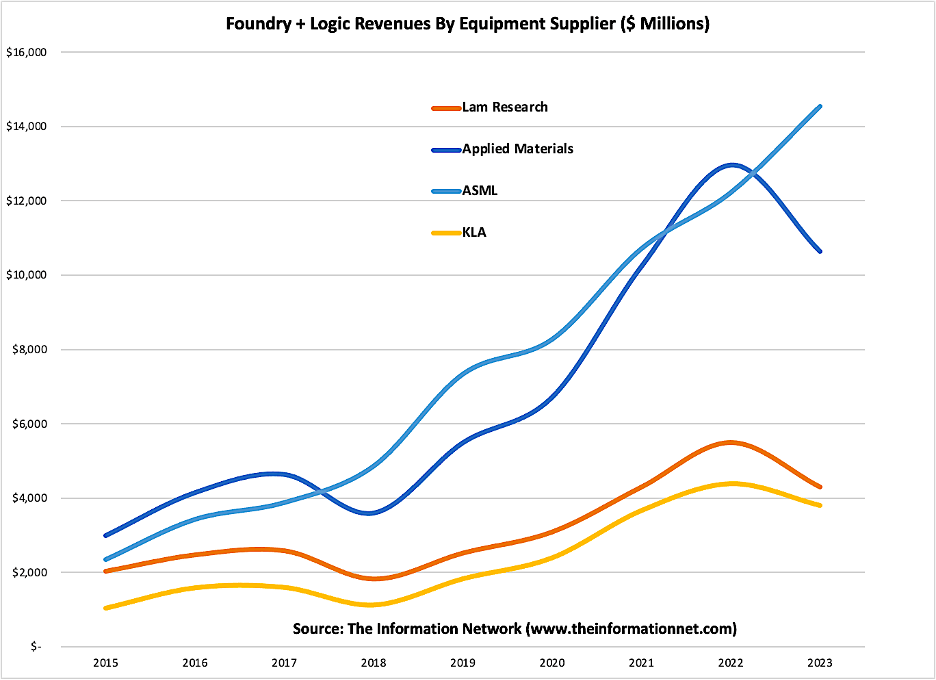

I forecast that ASML, which has been stymied by supply chain problems in 2021 and 2022, will exhibit positive growth in 2023 because of production limitations, as shown in Chart 2. ASML has a backlog of 100 EUV systems with an ASP of $200 million. Unlike memory IC companies, logic/foundry semiconductor companies are not likely to cancel orders despite the downturn and oversupply of chips in 2023 as leading foundry companies migrate to smaller technology nodes. I presented my analysis in my January 5, 2023 Seeking Alpha article entitled “Memory And Logic: Two Different Chips, Two Different Trajectories In 2023.”

The Information Network

Chart 2

Financial Metrics

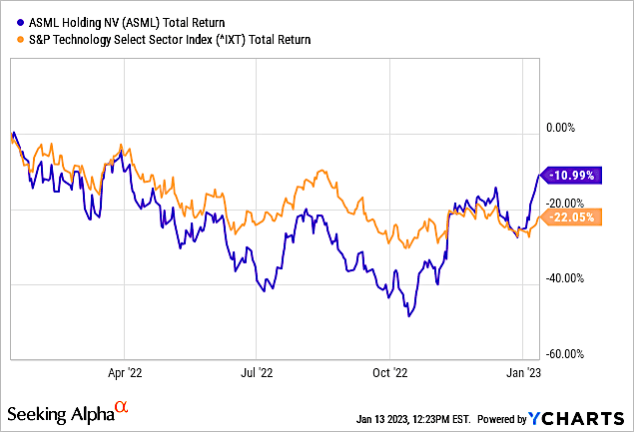

ASML stock performance is shown in Chart 3 for a 1-year period. Two things are evident:

- ASML was significantly underperforming the S&P Technology Select Sector Index (IXT) for the year UNTIL the company announced its Investor Day 2022 forecasts, where we see their impact.

- ASML and IXT have very similar normalized % change, i.e., peaks and valleys simultaneously, which suggests traders are buying the sector where something positive for one company is positive even for competitors.

YCharts

Chart 3

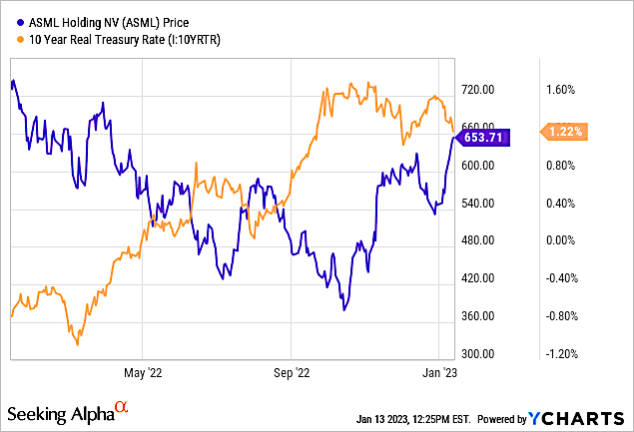

Chart 4 compares ASML’s share performance with the 10-year treasury rate. It shows an inverse relationship that was consistent until ASML’s Investor Day 2022 announcement and promise for strong growth.

YCharts

Chart 4

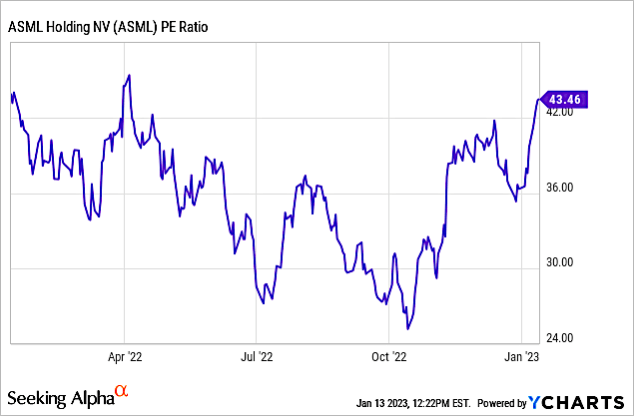

Chart 5 shows ASML’s PE ratio for the 1-year period. ASML is expensive based on its PE Ratio (41.1x) compared to the peer average (23.1x).

YCharts

Chart 5

Seeking Alpha’s Quant Rating History for ASML has been consistently a Hold since March 11, 2021 on a weekly basis. I also rate the company a Hold. I am suspicious of ASML’s inconsistencies in responses and lost revenue on China, on lack of disclosure on its fire and supply chain, deferred revenue “fast shipments”, and high backlog that could take until 2030 to be mediated. All of these could significantly impact earnings in the near and long term.

Be the first to comment