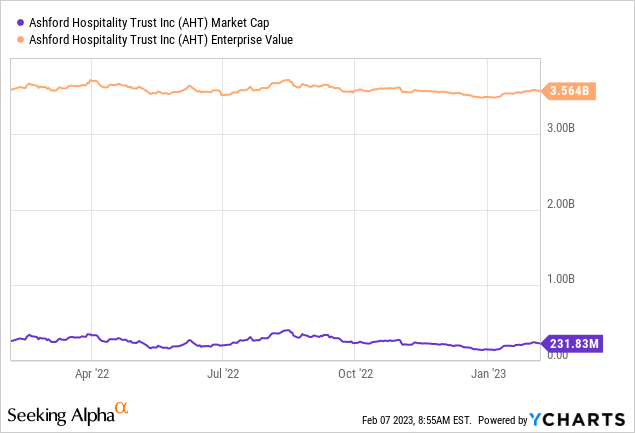

AHT’s Enterprise Value Vs Its 2023 FFO

DNY59

In our last coverage of Ashford Hospitality Trust, Inc. (NYSE:AHT), we suggested that investors should not get seduced by the stock and look elsewhere if they want value. AHT has been ho-hum since then and flatlined around the $6.70 price mark.

Seeking Alpha

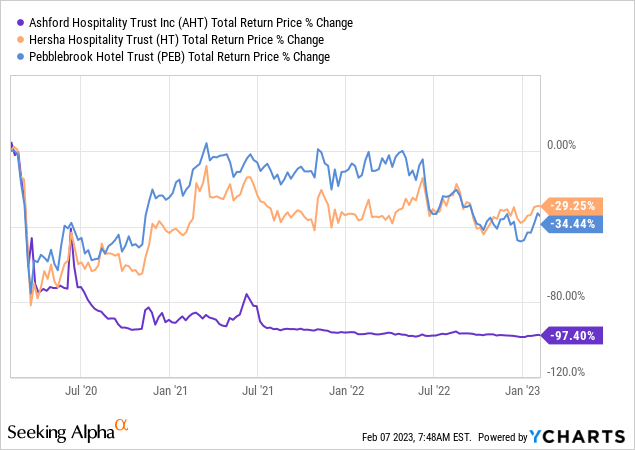

While the shorter term story has been a relaxed one, there are plenty of long suffering shareholders here. While its competitors such as Hersha Hospitality Trust (HT) and Pebblebrook Hotel Trust (PEB), hardly offered investors any solace, they definitely made them feel glad that it was not AHT that they invested in.

We look at what 2023 holds for AHT and why the depressed stock price should not fool you into thinking this is a bargain.

The Performance Explained

AHT’s massive underperformance comes down to a combination of extreme leverage and extreme dilution. Even going into the pandemic, no other hotel REIT carried the amount of leverage that AHT did. AHT’s non-recourse mortgages have often been viewed as an upside lottery ticket where investors benefit if hotels appreciate. If the reverse happens, the thought process was that they could just return the keys to the bank. That simplistic view is the prime reason many are nursing huge losses in this stock.

With large transaction costs for selling and massive annual capital expenditures, properties have to appreciate a lot for AHT to realistically capture any upside. On the other hand, due to extreme operational and financial leverage, a small decline meant that everything would be underwater. This fact can be seen today as a majority of AHT’s hotels remain cash traps.

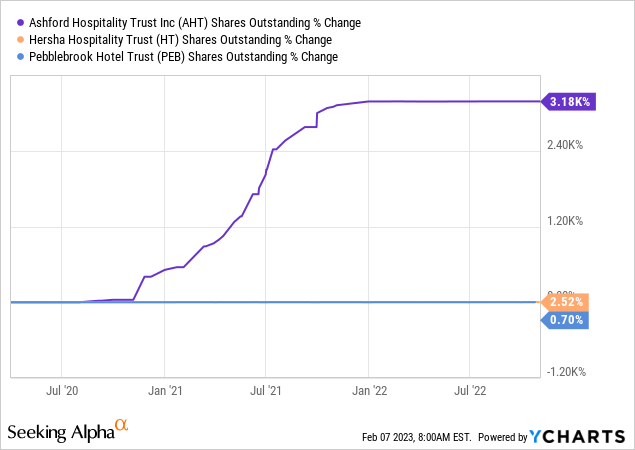

Of course the part two of the story is just as important. There is a reason that we have not once written a scathing review of PEB or HT, but recommended plenty of reasons to sell or short sell AHT over the last 3 years. 3,180% increase in share counts will do that to anyone.

2023

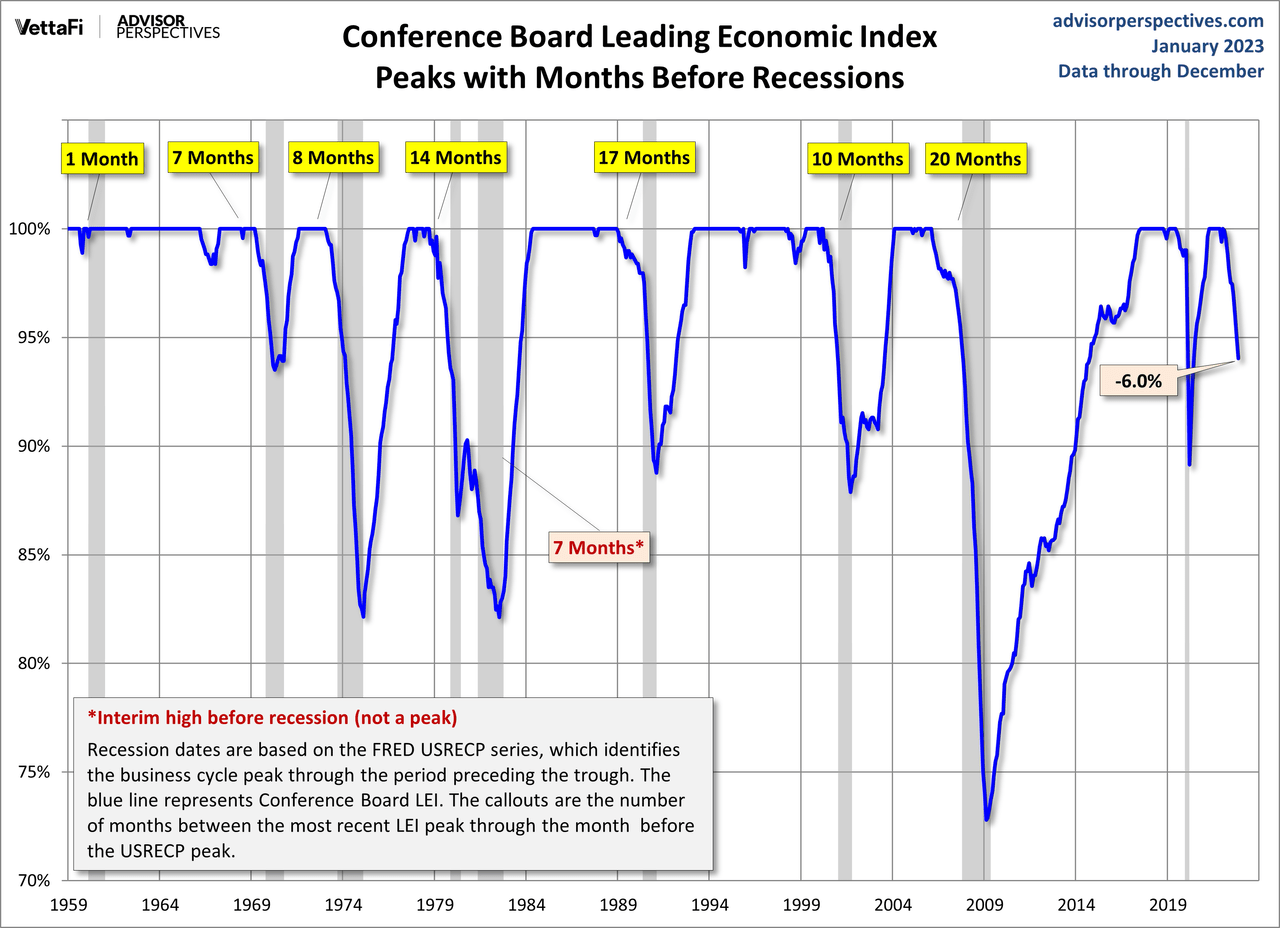

Our outlook here calls for a recession, possibly in the back half of 2023. That is hardly a maverick call based on where the Leading Economic Indicators are and how they evolved over the last six months.

Advisor Perspectives

In such an environment, AHT’s pricing power likely peaks within two quarters. Unlike most other recessions, we expect the unemployment rate to rise very slowly here. The labor market still has a big deficit and this is most true in the hospitality industry. This October report from American Hotel & Lodging Association aka ALHA, shows how bad things are.

Eighty-seven percent (87%) of survey respondents indicated they are experiencing a staffing shortage, 36% severely so. The most critical staffing need is housekeeping, with 43% ranking it as their biggest challenge. Those numbers are slightly better than in May, when 97% of respondents to an AHLA member survey said they were short staffed, 49% severely so, with 58% ranking housekeeping as their biggest challenge. Hotels are offering potential hires a host of incentives to fill vacancies—81% have increased wages, 64% are offering greater flexibility with hours, and 35% have expanded benefits—but 91% say they are still unable to fill open positions. Respondents are trying to fill an average of 10.3 positions per property, down from 12 vacancies in May. According to the U.S. Bureau of Labor Statistics, as of August, hotel employment was down by nearly 400,000 jobs compared to February 2020. Hotels are looking to fill many of the jobs lost during the pandemic, including more than 115,000 hotel jobs currently open across the nation. These staffing challenges are resulting in historic career opportunities for hotel employees. National average hotel wages for 2022 through June are more than $22 per hour—higher than any other year on record. Since the pandemic, average hotel wages have increased faster than average wages throughout the general economy. And hotel benefits and flexibility are better than ever.

Source: AHLA

In this environment we expect AHT’s operational leverage to work against it as costs increase faster than revenues.

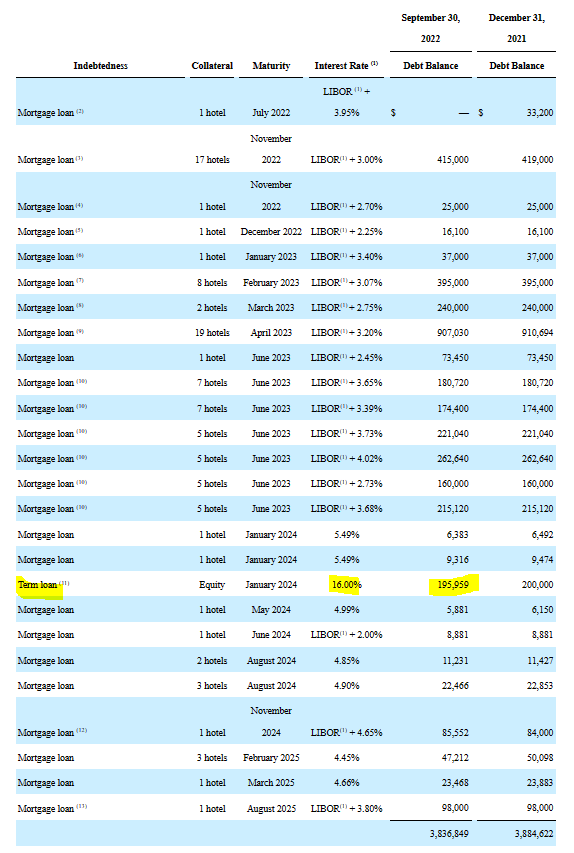

The second issue for AHT will be the interest costs and we cannot emphasize enough of how difficult it will be to service that $3.8 billion of debt with rates rising. The vast majority of its debt is floating with LIBOR (soon to be its successor SOFR). Funnily, the largest portion of the debt is at a fixed rate, but that fixed rate is an eye watering 16%.

Q3-2022 10-Q

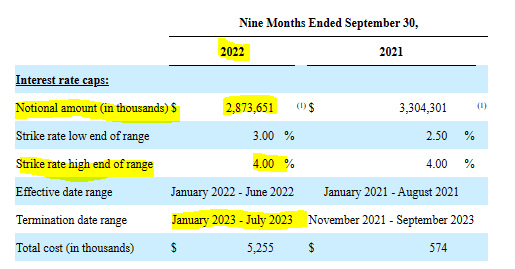

AHT has some interest rate caps in place. Based on Q3-2022 numbers there is protection for a good portion of the floating debt. The bad news is that even at the cap level the interest expense is excruciating.

Q3-2022 10-Q

The worse news is that these caps are running out as we speak. Sure, it is possible that they purchased some extensions, but those would come very expensive and at higher strikes based on where interest rates were after Q3-2022. The weighted average interest rate on AHT’s non-term loan portion was under 6% in Q3-2022. If we move the whole structure about 3% higher by Q4-2023, you will need an additional $108 million in cash flow just to service the debt. As we move into the back half of 2023, these operational and financial challenges should get pretty rough.

About That Cash On The Balance Sheet

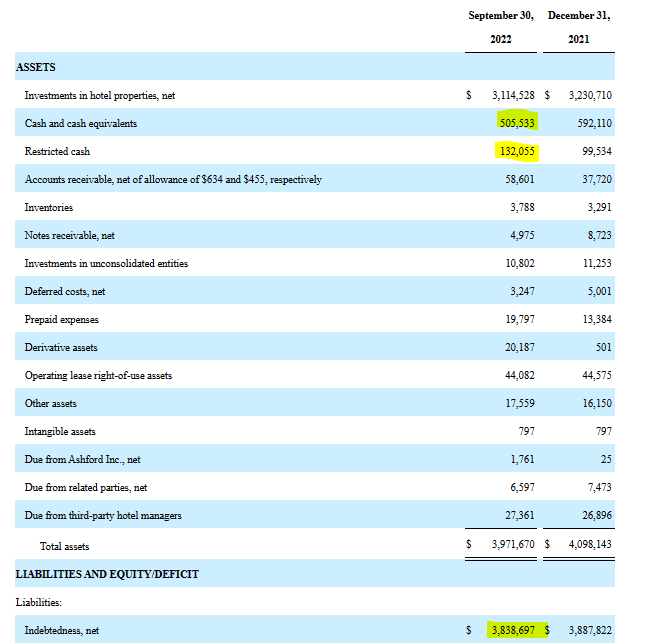

Investors seem to be really seduced by that cash level on the balance sheet.

Q3-2022 10-Q

We have heard that mentioned several times and the relevance here is that it is very large in relation to market capitalization of AHT.

While the cash does remove existential risks, in our books, it has very little relevance for AHT stock going up. The prime reason is that the cash which we assume is now earning 4% interest, is going to be used to pay off the term loan of $195.96 million costing 16%. The term loan does end in January 2024 and at a minimum that amount should be offset in any calculations. After that, we do have some excess over the market capitalization and that works out to maybe $2-$3 of upside. Of course that assumes that business functions in a profitable manner, something that we see as impossible in the back half of 2023.

Verdict

Analysts are slowly coming around to our view and the consensus now believes that funds from operations (FFO) will drop by about 50% in 2023.

Seeking Alpha

We are going out on a limb here to say that they are all still wrong and at least in the back half of the year, FFO will be negative. But assuming they are right and AHT churns out a $1.00 of FFO per share, that is about $32 million. Does that $32 million of FFO on a $3.6 billion enterprise value excite you? Consider yourself alone then.

As we have pointed out before, that FFO is before capital expenditures. Historically, AHT has spent $200 million a year in capital expenditures maintaining its hotels. So you will forgive us if we don’t mortgage our house to buy this lucrative opportunity at just “7X FFO”. We think 2023 should be a challenging year and we are likely to see solid stresses in the back half of 2023. We would not rule out another round of dilution starting in 2024. We rate the stock a Hold for now.

{kind=link}

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment