Fahroni

Although current market conditions have proven to be painful for most investors, there is an upside to the extreme volatility being experienced. This upside is the fact that there are many companies that are currently trading at levels that they normally wouldn’t. There likely are some companies that are overvalued. But at the same time, there are many companies that are trading at attractive discounts to what they should be trading at. A great example of a discounted firm at this time can be seen by looking at Asbury Automotive Group (NYSE:ABG), a major franchised automotive retailer in the US. Over the past couple of months, the firm has followed the market lower. This has come even as fundamental performance has been robust. Given where shares are priced today, I do believe that attractive upside is eventually on the table, leading me to retain my ‘buy’ rating on the firm for now.

A great prospect at this time

Back in July of this year, I wrote an article that looked upon Asbury Automotive Group in a favorable light. I found myself impressed by how the company had performed on both the top and bottom lines over the prior few years. Recent performance, in particular, had been amazing, with the company benefiting from both organic robustness and the acquisitions it had engaged in. Add on top of this the fact that shares were at fundamentally attractive levels, and I could not help but to rate it a ‘buy’, reflecting my belief that it would likely generate returns that surpassed the broader market. Since then, things have not gone exactly as I anticipated. The S&P 500 has dropped by 8%, with shares of Asbury Automotive Group falling an even greater 9.5%.

Author – SEC EDGAR Data

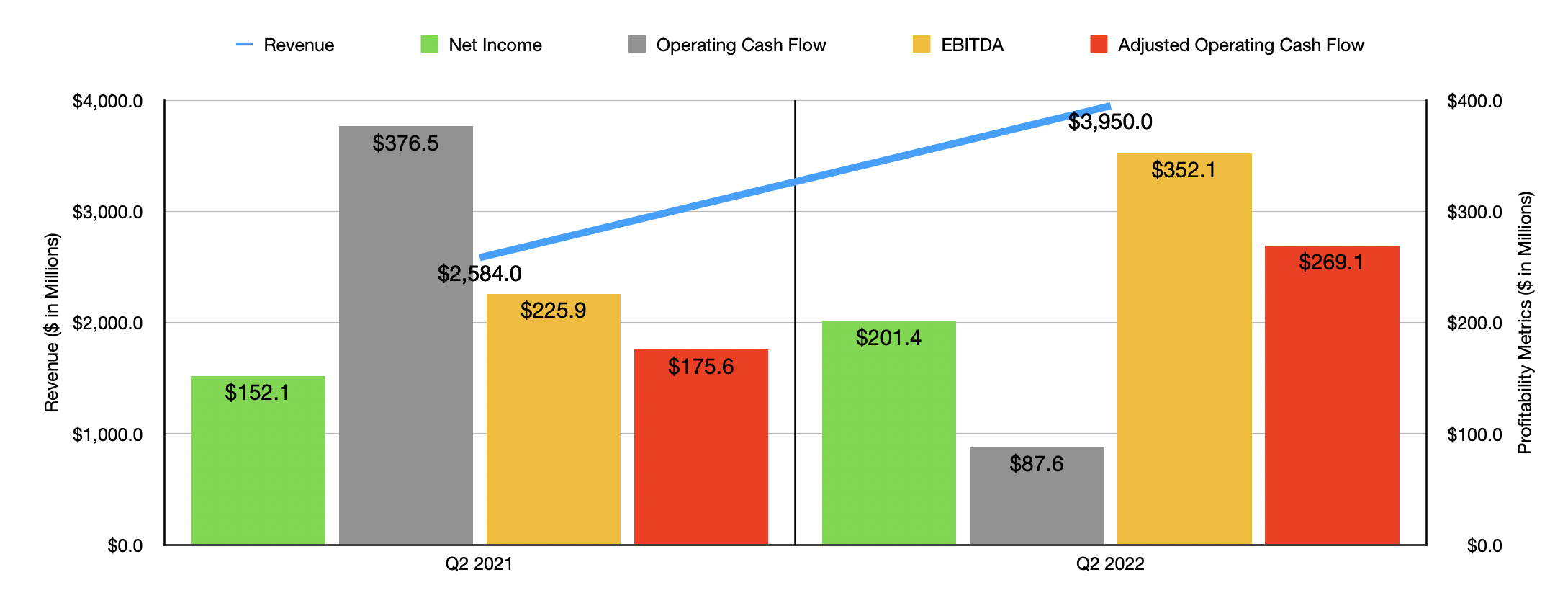

If you were to look solely at these share price movements, you might think that Asbury Automotive Group was experiencing some fundamental deterioration. But that couldn’t be further from the truth. All we need to do is to look at how the company performed during the second quarter of its 2022 fiscal year. This is the only quarter for which we did not have data available as of the last article I published, but for which we do have data available today. Sales during that time came in at $3.95 billion. That represents a 52.9% increase over the $2.58 billion generated the same quarter just one year earlier.

This increase in revenue was driven by strength across the board. In absolute dollar terms, the single largest contributor to the company’s increase was a rise in used vehicle revenue, with the metric climbing from $816.2 million to $1.36 billion. That’s a rise of roughly 67%. Revenue per used vehicle retailed managed to rise by 13% from $28,277 to $31,941. But the big increase for the company came from a 48% jump in the number of units sold, climbing from 26,856 to 39,848. While this growth should be considered explosive, it is appropriate to put the data in proper context. All of the increase in unit count came from acquired properties. In fact, retail used vehicle unit sales at an organic level actually declined by 2% year over year. Clearly, price increases and other economic concerns are showing signs of weighing on business.

There were, of course, other contributors to this increase in sales. For instance, new vehicle revenue achieved by the company jumped by 36%, climbing from $1.37 billion to $1.86 billion. This, in turn, which driven by a 22% increase in units sold, with that metric climbing from 31,725 to 38,697. Pricing also increased, climbing by 12% from $43,133 to $48,182. Parts and service revenue grew an even more impressive 78%, climbing from $292.4 million to $520.2 million. Meanwhile, finance and insurance revenue shot up 90%, jumping from $107 million to $203 million.

Author – SEC EDGAR Data

This increase in revenue brought with it improved profitability for the company. Net income, for instance, came in at $201.4 million during the second quarter of the 2022 fiscal year. This compares favorably to the $152.1 million generated one year earlier. Operating cash flow did fall, dropping from $376.5 million to $87.6 million. But if we adjust for changes in working capital, it would have risen from $175.6 million to $269.1 million. Even EBITDA increased, climbing from $225.9 million to $352.1 million. As can be expected, this performance was also instrumental in pushing up total results for the first half of the 2022 fiscal year as a whole. This, compared to the data from the same time last year, can be seen in the chart above.

Asbury Automotive Group

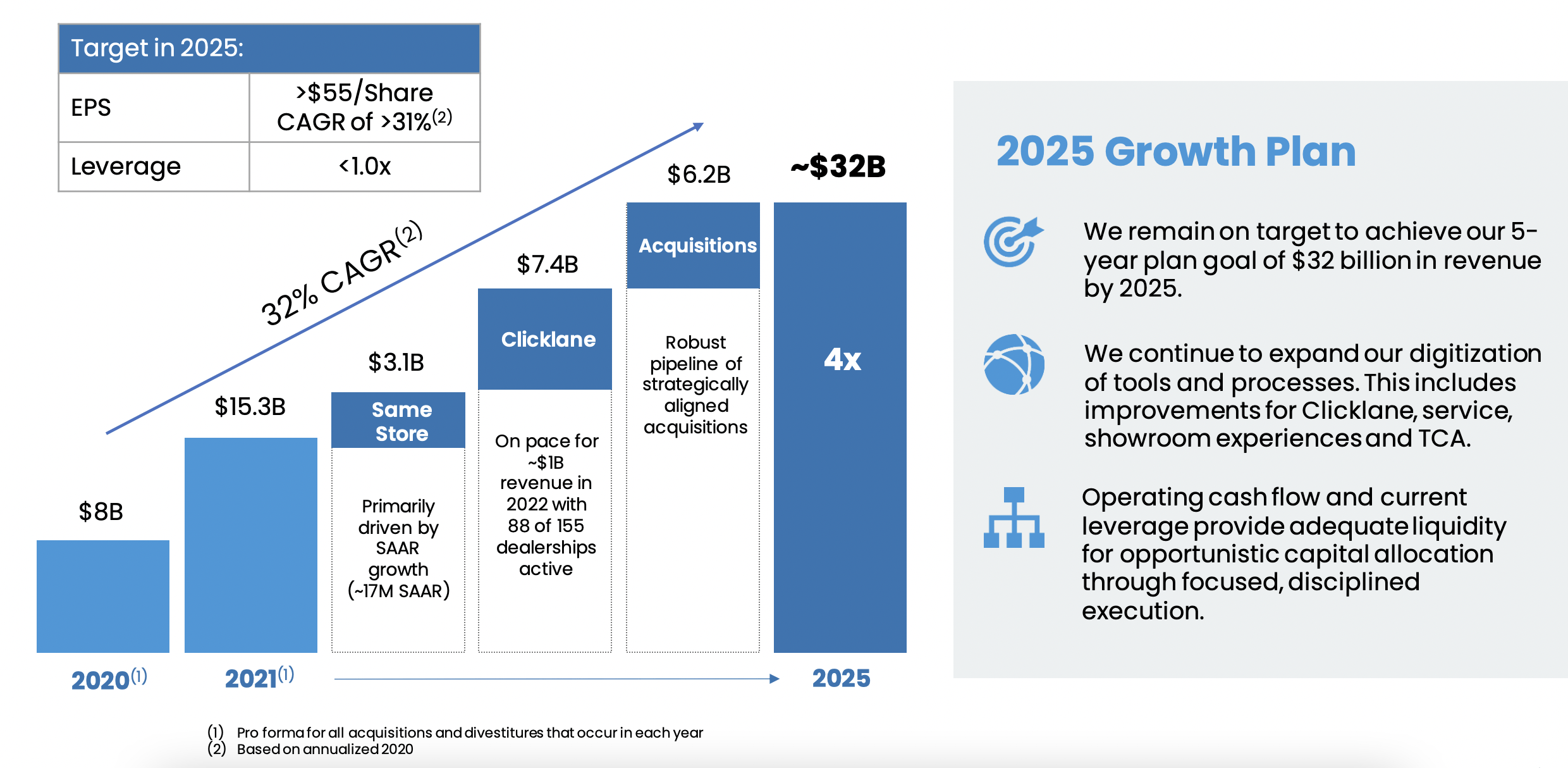

When it comes to the 2022 fiscal year as a whole, management has not provided that much in the way of guidance. All they said is that revenue should be at least $16 billion, translating to a year-over-year growth rate of 63%. While this may seem unlikely, it’s part of a broader effort by management to supercharge growth over the next few years. Ultimately, management wants to take the company to $32 billion in revenue by 2025. $6.2 billion of this increase will come from acquisitions. Another $7.4 billion would be attributable to the company’s new-ish Clicklane offering. In short, this is referred to by management as the industry’s first end-to-end digital platform aimed at facilitating the purchase and sale of vehicles, both used and new. Another $3.1 billion worth of the sales increase from the 2021 fiscal year through 2025 will involve same-store growth. This is basically organic growth by the company.

Author – SEC EDGAR Data

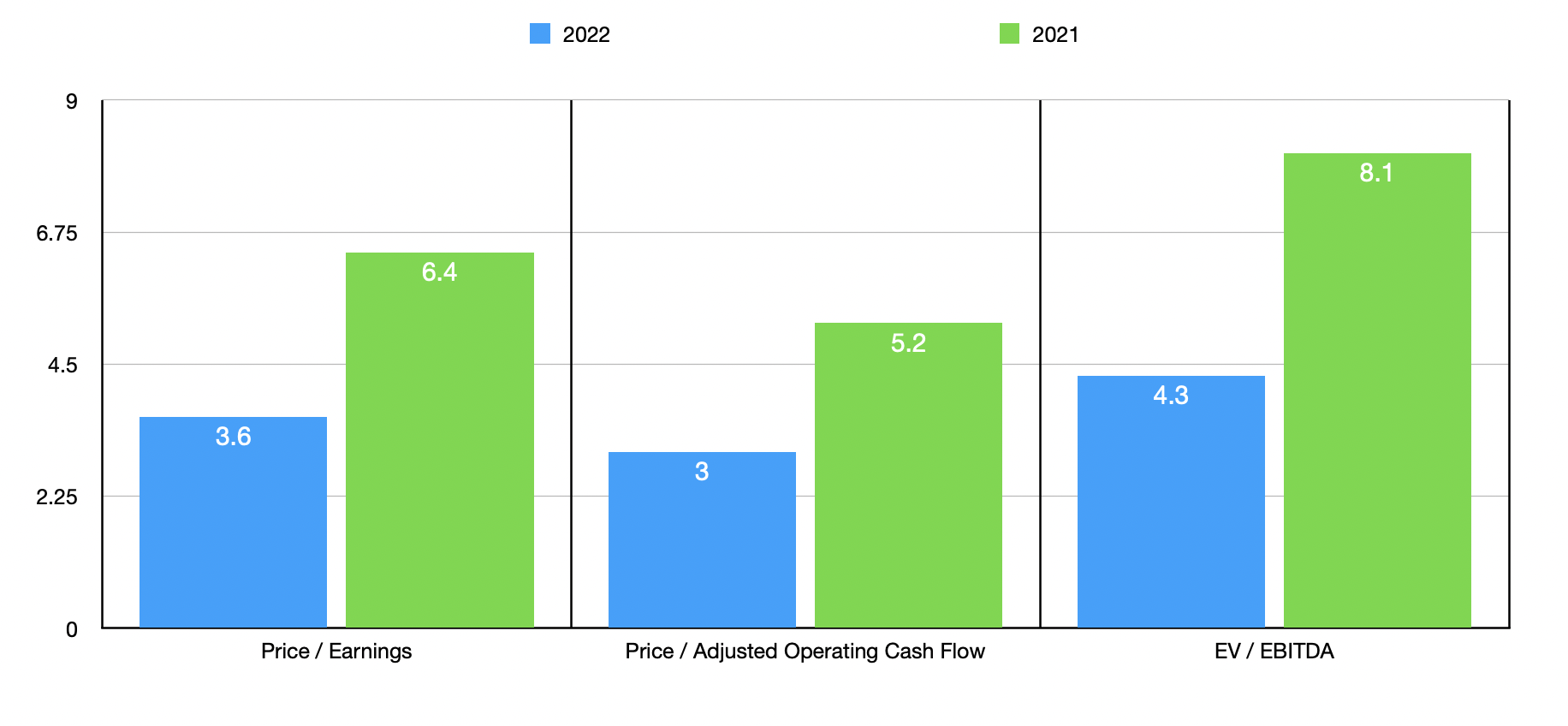

Unfortunately, we don’t know what to expect from a profitability perspective. But if we were to annualize the results seen in the first half of the year, we should anticipate net income of $954.6 million, adjusted operating cash flow of $1.13 billion, and EBITDA of $1.55 billion. This would imply a forward price to earnings multiple of 3.6, a forward price to adjusted operating cash flow multiple of 3, and a forward EV to EBITDA multiple of 4.3. But even if we assume that financial performance will revert back to what we saw during the 2021 fiscal year, shares would still be cheap, with the multiples at 6.4, 5.2, and 8.1, respectively. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 6.1 to a high of 30.5. Only one of the five firms was cheaper than it. Using the price to operating cash flow approach, the range was between 2.7 and 13, with two of the five being cheaper than our prospect. And finally, using the EV to EBITDA approach, the range was between 6.2 and 11.2, with four of the five companies being cheaper than Asbury Automotive Group.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Asbury Automotive Group | 6.4 | 5.2 | 8.1 |

| Group 1 Automotive (GPI) | 6.5 | 2.7 | 6.2 |

| Sonic Automotive (SAH) | 6.1 | 7.0 | 7.3 |

| Monro, Inc. (MNRO) | 30.5 | 13.0 | 11.2 |

| Lithia Motors (LAD) | 8.2 | 4.8 | 7.4 |

| Penske Automotive Group (PAG) | 7.2 | 6.6 | 6.7 |

Takeaway

Based on all the data provided, I must say that I continue to find myself impressed with Asbury Automotive Group. The company is continuing to expand at a great pace and shares look incredibly cheap on an absolute basis. Relative to similar firms, pricing is a bit mixed, leaving open the opportunity to perhaps buy up stock in a more appealing competitor. But all things considered, I do think that the long-term outlook for the company is favorable, leading me to rate it a solid ‘buy’ at this time.

Be the first to comment