gawrav/E+ via Getty Images

The appeal of floating-rate loans usually peaks when interest rates are rising. But they may help diversify portfolios in any environment.

Floating-rate loans are known by many names, including bank loans, senior loans, and leveraged loans. They’re typically extended to companies with higher levels of debt relative to cash flow, and because of this, they carry greater credit risk than investment-grade bonds. But unlike traditional bonds, floating-rate loans don’t make a fixed-interest payment, or coupon, for each period. Instead, their coupons reset every 30 or 90 days, floating up or down with the changes in prevailing interest rates. This floating feature makes loan prices less sensitive to shifts in interest rates, so flows into floating-rate loan funds tend to increase when the Federal Reserve is actively raising rates in response to a growing economy and improved labor market. And, as you can guess, this trend tends to reverse when rates are falling.

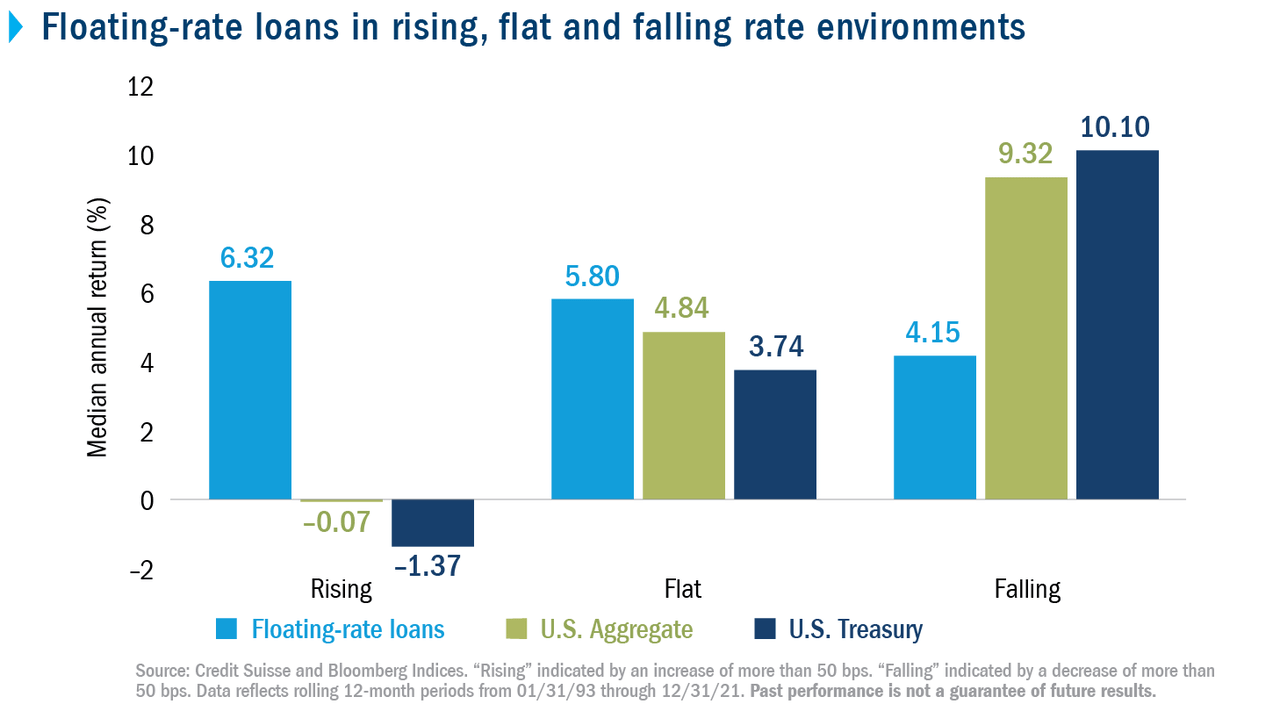

Historically, floating-rate loans have outperformed in rising and flat interest-rate environments. When rates are rising, the median annual return for floating-rate loans, as gauged by the Credit Suisse Leveraged Loan Index, has exceeded the return on U.S. Treasuries and the Bloomberg U.S. Aggregate Bond Index by more than 6 percentage points. But what’s possibly overlooked is that floating-rate loans have also delivered attractive absolute and relative performance regardless of the broader interest-rate environment. Because yield is such a significant component of total return, floating-rate loans also have outperformed U.S. Treasuries and the Bloomberg Aggregate Bond Index when rates are flat. It’s only when rates fall that we have seen floating-rate loans underperform.

Credit Suisse and Bloomberg Indices

Floating-rate loans may add diversification in any interest-rate environment.

Although their interest-rate-related benefits are what drive investors’ flows into and out of the asset class, floating-rate loans can help diversify a portfolio at any time – and this benefit can be overlooked. Most of the return in floating-rate loans comes from their exposure to credit risk (exposure to corporations), while the Bloomberg U.S. Aggregate Bond Index gets most of its return from duration risk (interest-rate sensitivity). So, historically they’ve had a low correlation to each other and behave differently in different market environments.

Bottom line

Floating-rate loans are popular when interest rates are rising, but they may have diversification benefits in any interest rate environment.

Disclosures

Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg owns all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material, or guarantee the accuracy or completeness of any information herein, or make any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, shall not have any liability or responsibility for injury or damages arising in connection therewith.

The Bloomberg U.S. Aggregate Bond Index is a market-value-weighted index that tracks the daily price, coupon, pay-downs and total return performance of fixed-rate, publicly placed, dollar-denominated and non-convertible investment-grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity.

The Credit Suisse Leveraged Loan Index tracks the investable market of the U.S.-dollar-denominated leveraged loan market. It consists of issues rated “5B” or lower, meaning that the highest rated issues included in this index are Moody’s/S&P ratings of Baa1/BB+ or a1/BBB+. All loans are funded term loans with a tenor of at least one year and are made by issuers domiciled in developed countries.

Indices shown are unmanaged and do not reflect the impact of fees. It is not possible to invest directly in an index.

© 2016-2022 Columbia Management Investment Advisers, LLC. All rights reserved.

Use of products, materials and services available through Columbia Threadneedle Investments may be subject to approval by your home office.

With respect to mutual funds, ETFs and Tri-Continental Corporation, investors should consider the investment objectives, risks, charges and expenses of a fund carefully before investing. To learn more about this and other important information about each fund, download a free prospectus. The prospectus should be read carefully before investing. Investors should consider the investment objectives, risks, charges, and expenses of Columbia Seligman Premium Technology Growth Fund carefully before investing. To obtain the Fund’s most recent periodic reports and other regulatory filings, contact your financial advisor or download reports here. These reports and other filings can also be found on the Securities and Exchange Commission’s EDGAR Database. You should read these reports and other filings carefully before investing.

The views expressed are as of the date given, may change as market or other conditions change and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, may not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not take into consideration individual investor circumstances. Investment decisions should always be made based on an investor’s specific financial needs, objectives, goals, time horizon and risk tolerance. Asset classes described may not be appropriate for all investors. Past performance does not guarantee future results, and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that any forecasts are accurate.

Columbia Funds and Columbia Acorn Funds are distributed by Columbia Management Investment Distributors, Inc., member FINRA. Columbia Funds are managed by Columbia Management Investment Advisers, LLC and Columbia Acorn Funds are managed by Columbia Wanger Asset Management, LLC, a subsidiary of Columbia Management Investment Advisers, LLC. ETFs are distributed by ALPS Distributors, Inc., member FINRA, an unaffiliated entity.

Columbia Threadneedle Investments (Columbia Threadneedle) is the global brand name of the Columbia and Threadneedle group of companies.

NOT FDIC INSURED · No Bank Guarantee · May Lose Value

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment