DenisTangneyJr/iStock via Getty Images

This article continues my recent series on water utility and services stocks. The first two entries on American Water Works Company, Inc. (AWK) and Essential Utilities, Inc. (WTRG) can be found here:

American Water Works: The Short Term Pain May Be Over.

Essential Utilities: Despite Some Risks, The Name Says It All.

Today I’ll be taking a look at Artesian Resources Corporation (NASDAQ:ARTNA), a relatively small $550M market cap water utility serving just over 300,000 customers in the Delmarva Peninsula.

ARTNA: Slow And Steady Wins The Race

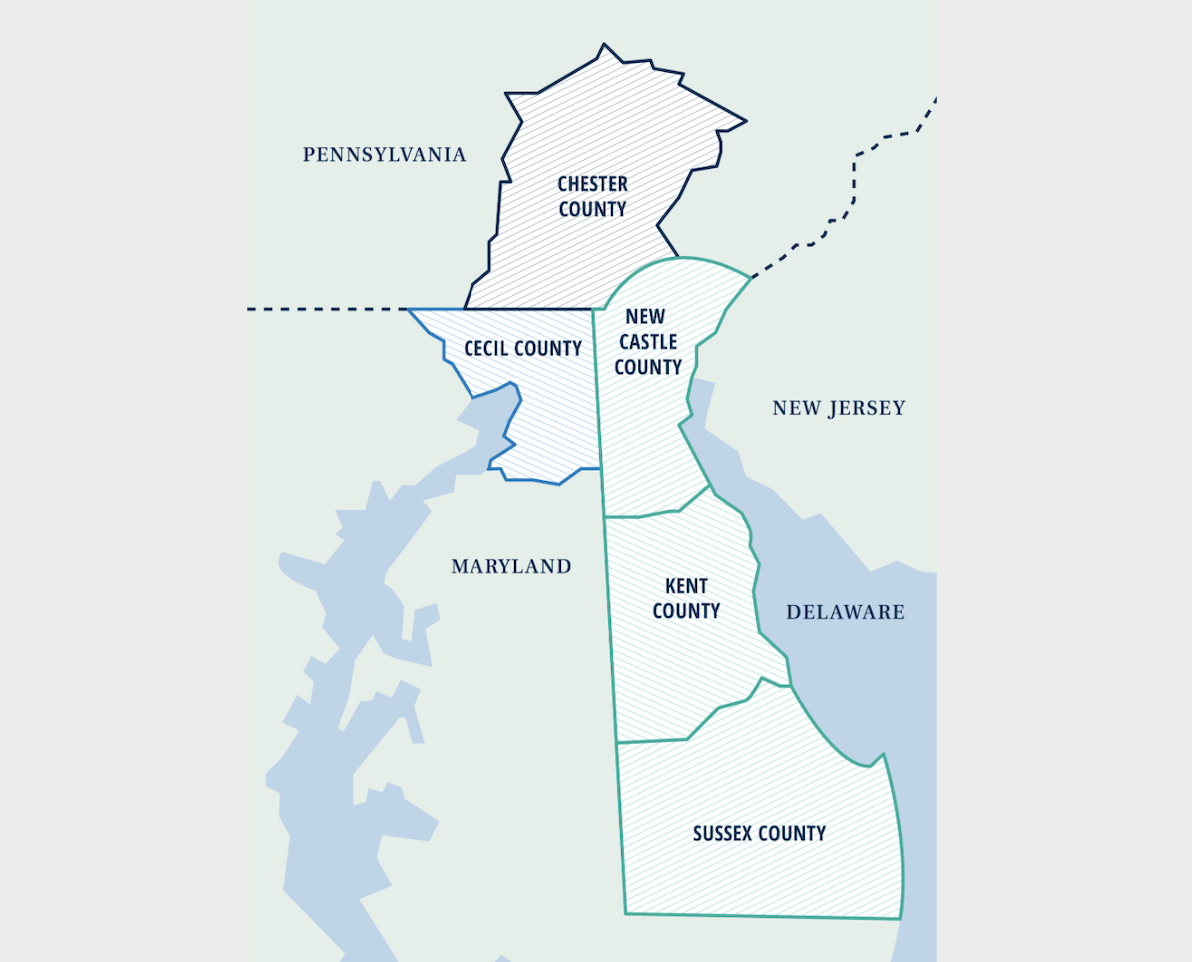

For those not familiar with the area, Delmarva includes most of the state of Delaware along with portions of the Maryland and Virginia shores. Artesian Resources Corporation also serves communities in adjacent Chester County in southeastern Pennsylvania.

The Delmarva Peninsula (Artesian Resources)

While the company also offers wastewater treatment and water engineering services, over 90% of ARTNA’s revenues are derived from their water utility business. Like most water utilities, they grow both organically through rate increases, area expansion, and customer additions, and by gradually acquiring smaller local utilities and water infrastructure assets. Their recent acquisitions include TESI, a small Delaware-based wastewater business, from Middlesex Water Company (MSEX), another top-notch water utility, as well as the municipal water assets of the Town of Frankford, Delaware.

Although it is only the 8th-largest public water utility with fewer than 300 employees, Artesian Resources Corporation has stood the test of time. Founded in 1905 in Delaware, ARTNA has paid dividends since 1933 and boasts a 26-year dividend growth streak dating back to its IPO in 1996. Historically, it has grown its revenue and earnings at around 5% per year with lower dividend growth between 2-4%, but don’t let this slow-growth utility fool you into thinking it has also been a slow-growth stock.

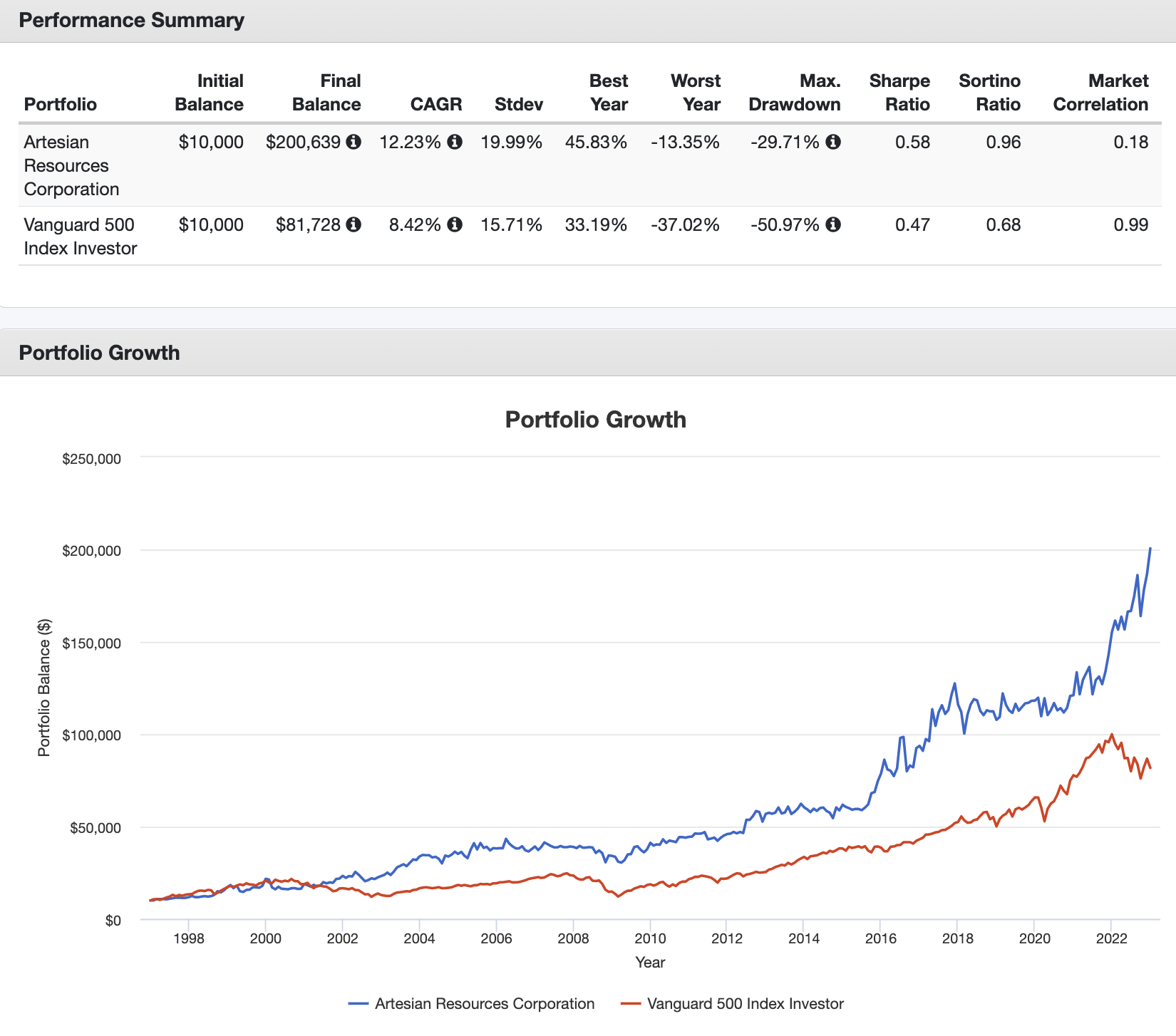

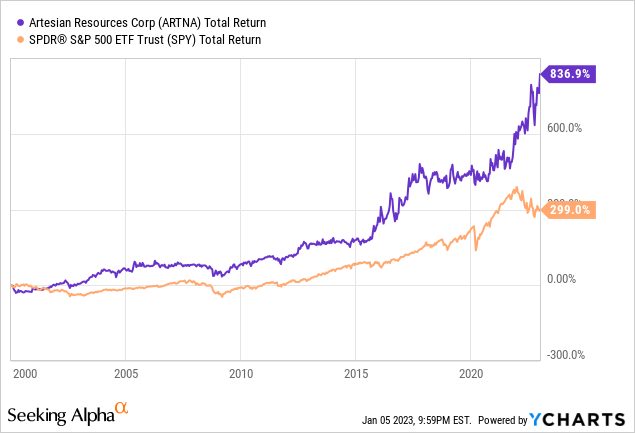

ARTNA has trounced the S&P in total returns since its IPO, delivering a 12.23% CAGR with dividend reinvested versus 8.42% for the S&P index, with a far better risk-adjusted return profile (Sortino ratio), an ultra-low beta, and a worst-year return of just -13.4% compared to -37% for the S&P.

Below, we can see how a $10K investment in ARTNA made at the beginning of 1997 would have fared against the S&P 500 Index (SP500):

ARTNA vs S&P 500 (portfoliovisualizer.com)

Dividend Strength

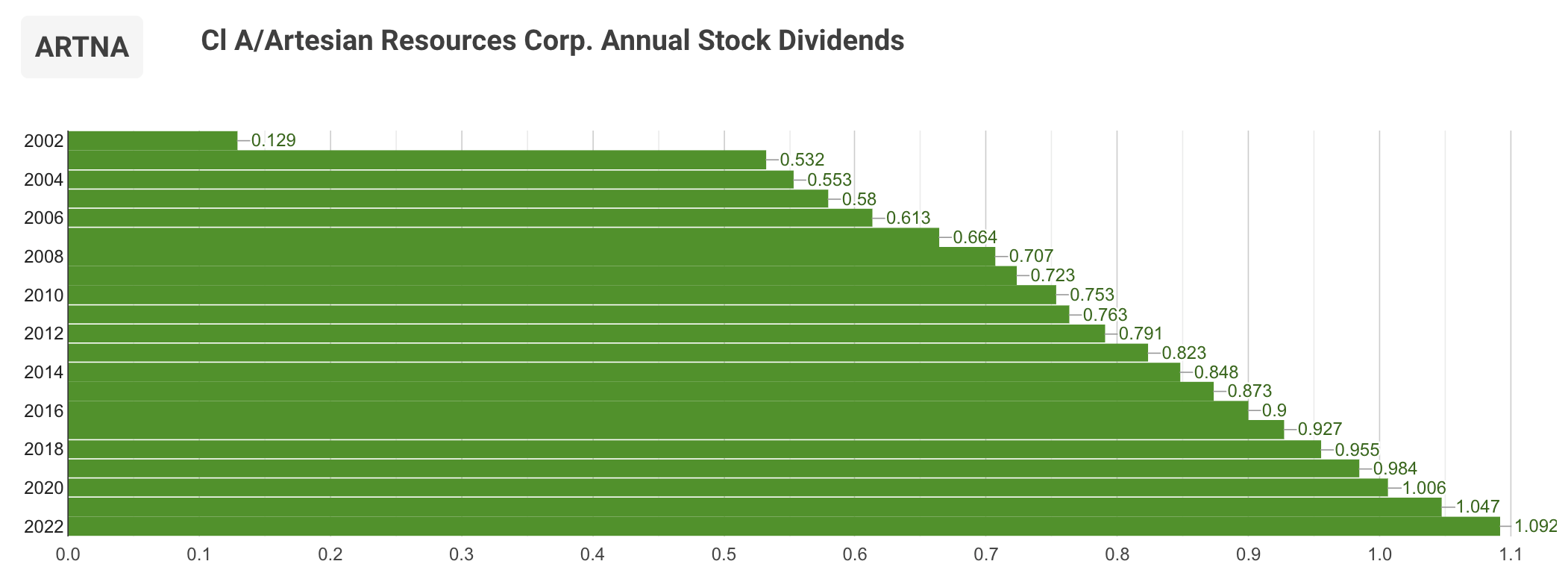

Along with this stellar performance, ARTNA has been committed to returning a growing income stream to investors since its IPO. Its dividend growth record, while at a low CAGR, is as consistent as they come. (Note below that the company only provides payout data from 2003, so the 2002 figure should be disregarded.)

dividendinvestor.com

Currently yielding a respectable-for-its-subsector 1.90%, ARTNA’s most recent dividends hikes totaled 2% in 2022 and a more-typical 4% in 2021. Its current payout ratio is a healthy 55% compared to its historical average in the 60-65% range, and its 5-year dividend CAGR is 3.54%. For comparison, the largest U.S. water utility AWK sports the same payout ratio with a lower 1.69% dividend yield and a much higher 5-year dividend CAGR of 9.65%.

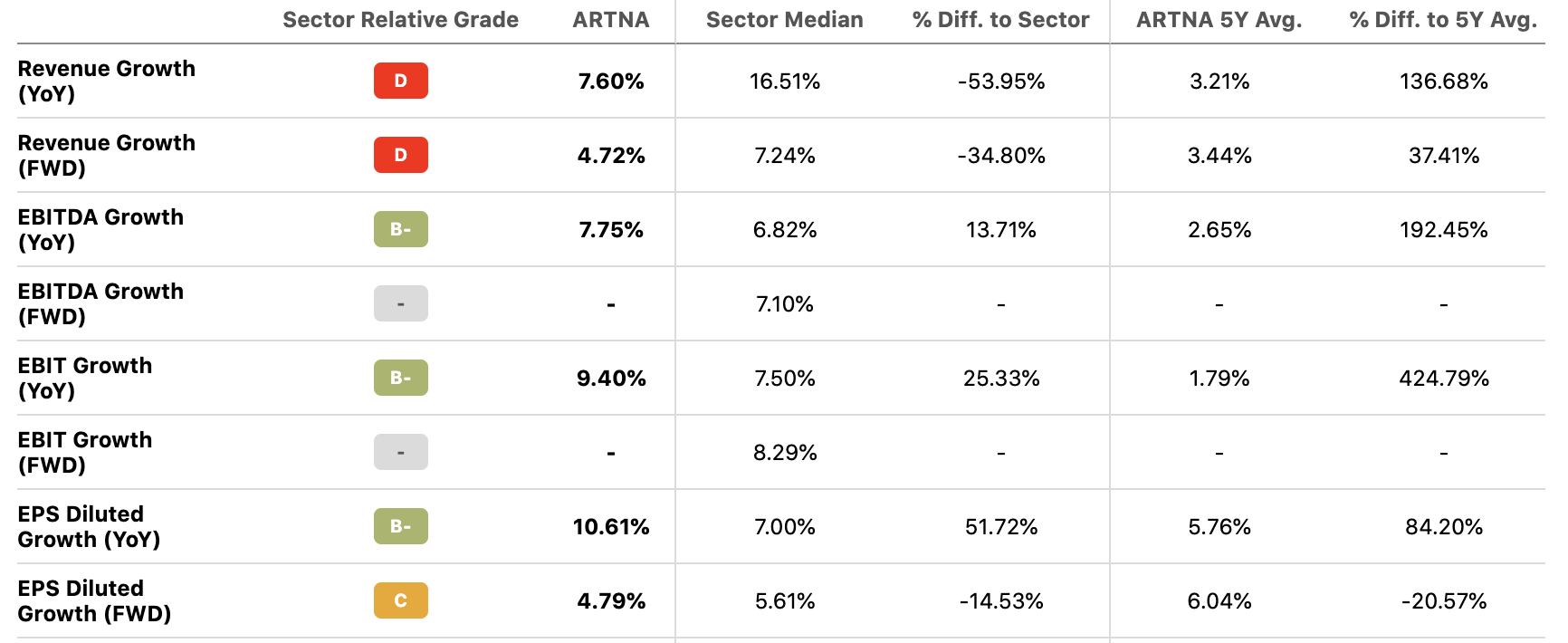

Like most utility companies, Artesian performed extremely well in 2022, growing revenue at 7.6% and earnings at 10.6% YoY, roughly double the company’s 5-year (and going much further back) historical averages. This recent growth combined with its historically low payout ratio makes me interested to see if a bigger-than-usual dividend raise is in the cards for 2023.

Seeking Alpha

Regardless, even if growth moderates and the company’s lower forward EPS growth estimates play out at 5-6% in 2023 and beyond, ARTNA should be able to comfortably continue raising its dividend at the 2-4% CAGR investors are accustomed to. Clearly, Artesian’s management has been extremely disciplined and conservative with their dividend approach, delivering a slow-growing income stream that shareholders can depend on since the company’s IPO.

Valuation

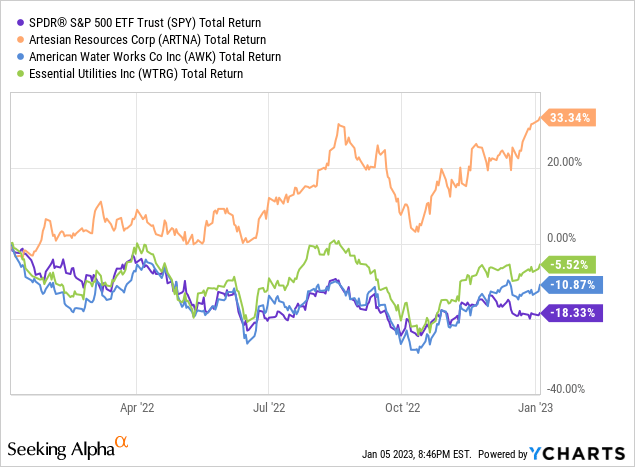

Artesian Resources shares have had an incredible run this past year, delivering a total return of over 33% against SPY’s -18%, AWK’s -11%, and WTRG’s -5.5%. It might be more accurate to say that ARTNA has actually had two incredible runs, as it gave up most of its gains midway through the year and then staged another ~30% run-up beginning in mid-October.

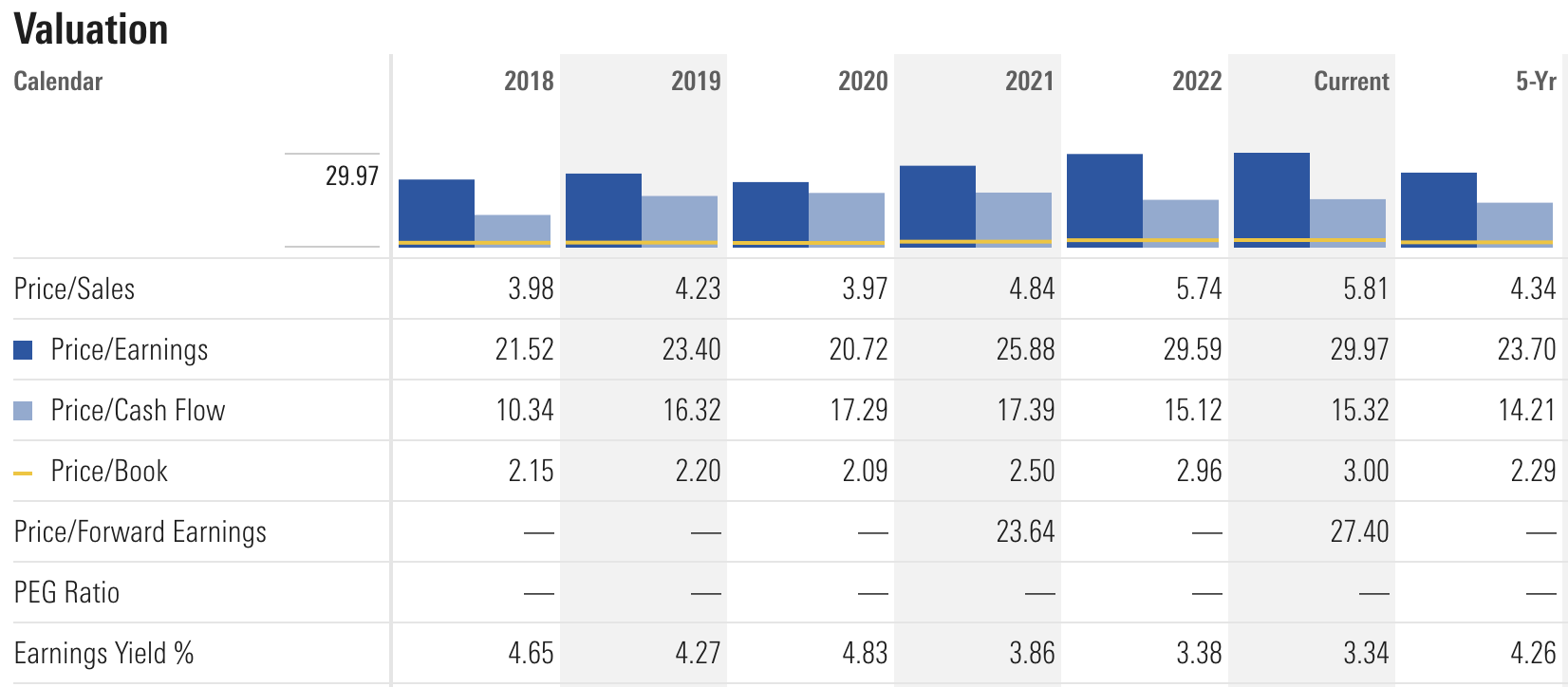

Even with the company’s strong 2022 revenue and earnings growth, this rapid share price appreciation has left ARTNA’s valuation at nosebleed levels for a utility that is predicted to grow revenue and EPS at less than 5% annually going forward.

ARTNA 5-Year Valuation (Morningstar)

As we can see, its current P/S ratio of 5.8 dwarfs its 5-year average of 4.3, as does its current P/E ratio of 29.9 against its 23.7 historical average. Even as a huge fan of ARTNA’s disciplined management and its consistent growth record, I think it’s impossible to justify the current valuation and view ARTNA shares as at least 20% overvalued.

Conclusion

Staring down a recession with the Fed remaining hawkish on interest rates, this strikes me as the perfect time to lock in some gains of “inflation-proof” stocks that have somewhat irrationally run up over the past year. Artesian Resources Corporation is a fantastic and resilient business that deserves to trade at a premium based on its historical performance, but it is not growing its revenue, EPS, or dividend anywhere near fast enough to justify its current stock price or its massive 60% share price appreciation over the past 18 months.

Water infrastructure requires frequent and expensive maintenance, and a high-interest-rate environment may eventually pressure ARTNA’s earnings. During the Great Recession the stock pulled back quite a bit, although far less than the market overall, and historically the share price has moved in fits and starts, with large bull runs like the one it has experienced between mid-2020 and now offset by long periods of stagnation.

With risk-free Treasury rates and even bank savings account rates well above the level of ARTNA’s current 1.9% yield, I think it would be prudent for investors to lock in this past year’s fantastic gains and wait until the stock’s valuation deflates to be more inline with historical levels before buying again. Based on Artesian Resources Corporation’s long-term chart, I don’t expect a large pullback in the share price, but rather a years-long period of consolidation around the current price level while its slow and steady growth allows its revenue and earnings multiples to gradually come down to more reasonable levels.

Be the first to comment