mphillips007/iStock via Getty Images

Ark Restaurants (NASDAQ:ARKR) is a national restaurant operator with 17 locations distributed across the east coast and Las Vegas.

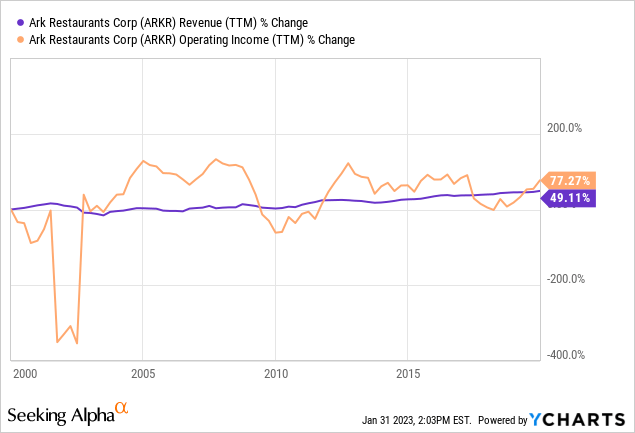

The company did not see growth in the 20 years spanning from 2000 until before the pandemic. Today, it operates at a higher level because of inflation. However, its current earnings are inflated by PPP loan forgiveness.

Because the company has not grown, and trades at a P/E ratio close to 13x after the PPP forgiveness effects are removed, I believe it is not an opportunity.

Note: Unless otherwise stated, all information has been obtained from ARKR’s filings with the SEC.

Business description

Strong moat restaurants: ARKR operates 17 restaurants in New York, Washington D.C., Florida, Alabama and Nevada. The company has acquired, developed and disposed of many others. A quick search shows that these restaurants are well regarded.

Google reviews for some of ARKR’s restaurants (Google Maps)

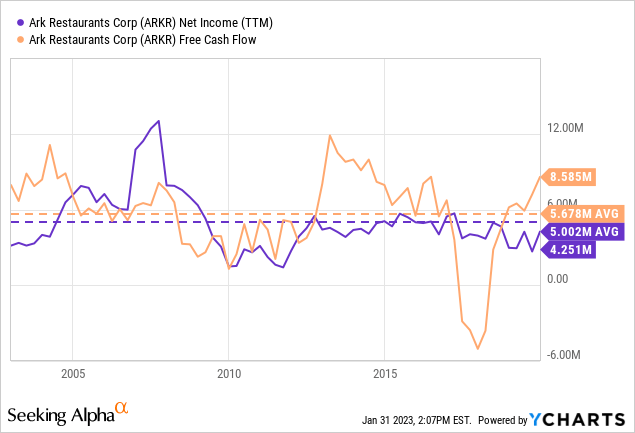

Consistent profitability and returns: The company has been profitable consistently, with the exception of the pandemic period. This period was in turn recovered by the forgiveness of $13 million in PPP loans between FY21 and FY22. The charts below cover the period from January 2002 to January 2020.

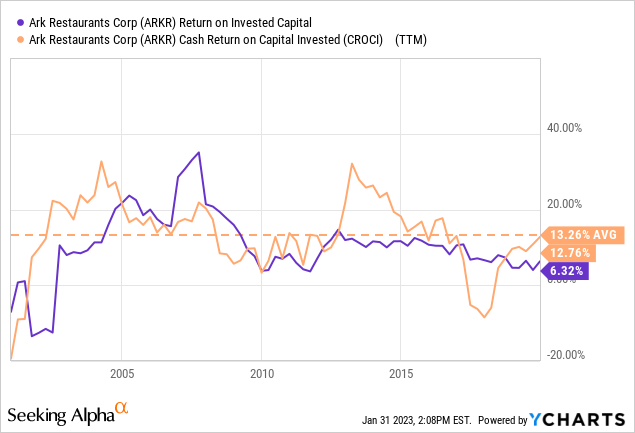

On a related note, the company has not squandered capital, maintaining a healthy return on capital invested and cash return on capital invested. ARKR has shown that it can close restaurants if they do not provide returns, for example with the disposition of four properties between FY21 and FY22.

An OK balance sheet with high interest expenses: ARKR has financed most of its restaurant acquisitions and investments through notes payable with a single bank. As of FY22, the company accumulates $23 million in these notes, maturing between 2023 and 2025. Fortunately the company also has $29 million in cash and deposit certificates to cover those debts.

On the negative side, ARKR is paying LIBOR + 3.5% on these notes. With LIBOR-1 year at 5.3%, this implies a financing cost of 8.8%, or $2 million a year.

High insider ownership: The company’s CEO owns 27% of the outstanding shares. The executive group owns 38% in total.

Valuation

Depressed multiples because of PPP forgiveness: ARKR’s earnings have been inflated by the forgiveness of $13 million of PPP loans ($10.5 million in FY21, $2.5 million in FY22, and $2 million to be forgiven). This is a non-recurring and non-operating item that should not be considered for long term profitability calculations. An additional aspect contributing to inflated earnings is a lower effective tax rate because of the PPP loans.

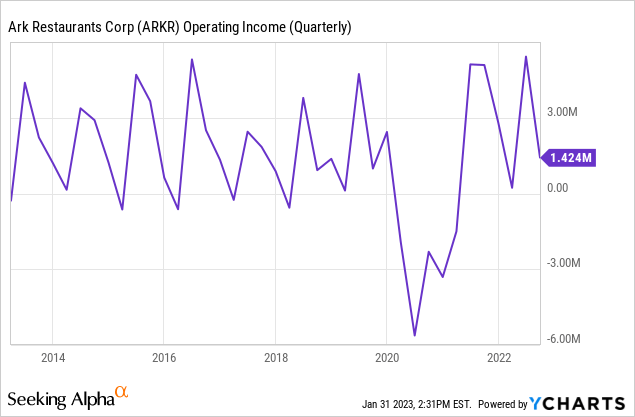

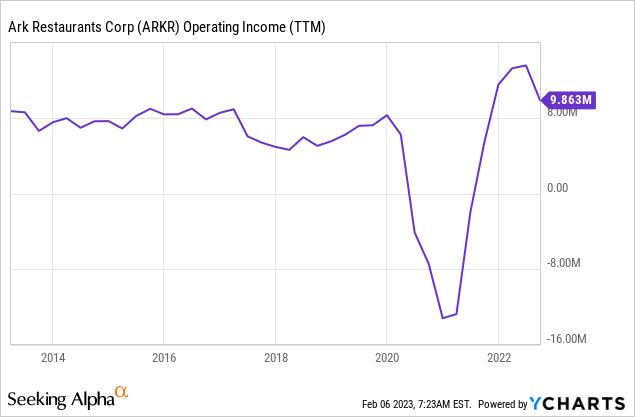

Inflation growth, but nothing much: Even when eliminating the effect of PPP loans, ARKR is posting higher net income than before the pandemic. At the operating level it can be seen in the chart below. This is consistent with significant inflation accumulated after the pandemic, but does not imply a growth trend.

Restaurants do not grow: The company recognizes on its 10-K annual report that restaurants rarely generate more revenues once they are operating in normal conditions. ARKR has to open new restaurants in order to grow.

In the period spanning from the year 2000 to 2020, the company grew earnings only meagerly.

True earnings capacity: Considering the results for FY22, ARKR can generate about $10 million in operating income.

From these, the company has to subtract $2 million in yearly interest expenses. Interest expenses should be reduced in the future if interest rates decrease or as debt is repaid.

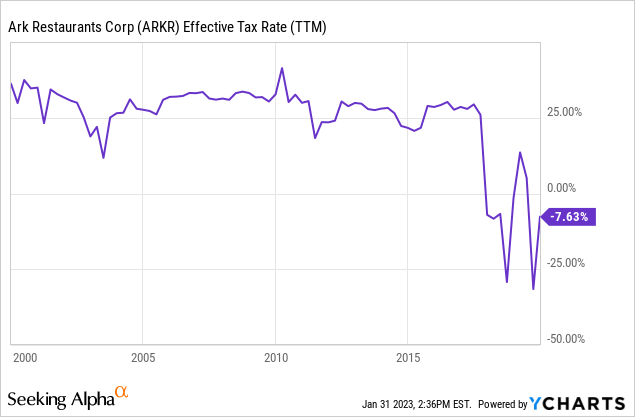

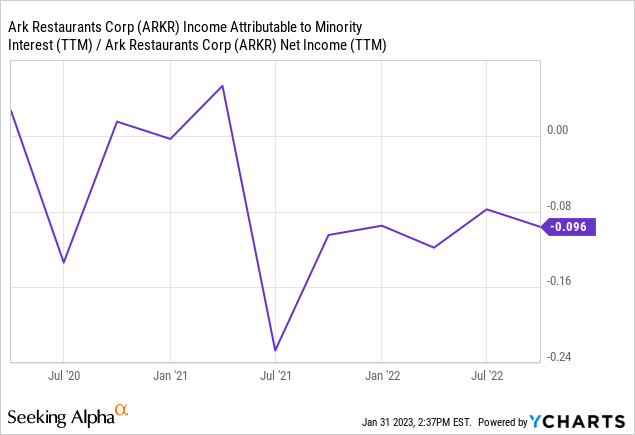

That leaves about $8 million in pre-tax income, which is taxed at 25% on average, as seen below (21% federal and the rest at the state level), leaving $6 million in net income. From net income, about 10% belongs to minority shareholders (second chart below). The result is $5.4 million attributable to common shareholders.

Conclusion

After adjusting for non-recurring expenses and the effective income tax rate, ARKR trades at a P/E ratio to adjusted TTM earnings of 13x.

In my opinion, this seems a lofty price for a company that has not shown the capacity to grow in the past. Further, the fall that we can expect in net income after the PPP effect is removed in FY23, plus heightened interest expenses, could expose the stock to downward volatility.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment