tofumax

Arcos Dorados Holdings Inc. (NYSE:ARCO) remains a Caribbean gem with its sound fundamentals. It holds the largest customer base in the region, making it the largest McDonald’s (MCD) franchisee. It has already bounced back after the pandemic hit its operations. Today, it sustains its rebound and keeps an eye on its expansion goals. It also adapts to the changing market landscape to leverage its growth in the market.

Investors must watch out for Arcos Dorados stock as growth prospects become more enticing. Also, the stock price stays reasonable with dividend payments. Its current uptrend is consistent with its impressive fundamentals in the recent quarter.

Company Performance

In the last two years, Arcos Dorados Holdings, Inc. faced challenges in its operations. The restrictions became a problem for its inventory levels and market demand. Limited operations and lower purchasing power added more pressure to it. Even so, it proved to be a durable giant in the region. After a year, the tables turned, and revenue growth became more robust.

Today, it continues to dominate in Latin America and the Caribbean. But, the market landscape is changing, and it has to get ahead of the tighter competition. Fortunately, Arcos Dorados appears to be ten steps ahead of it. Its continued restaurant openings and digital transformation help sustain growth. With over 2,000 restaurants, it serves millions of customers daily.

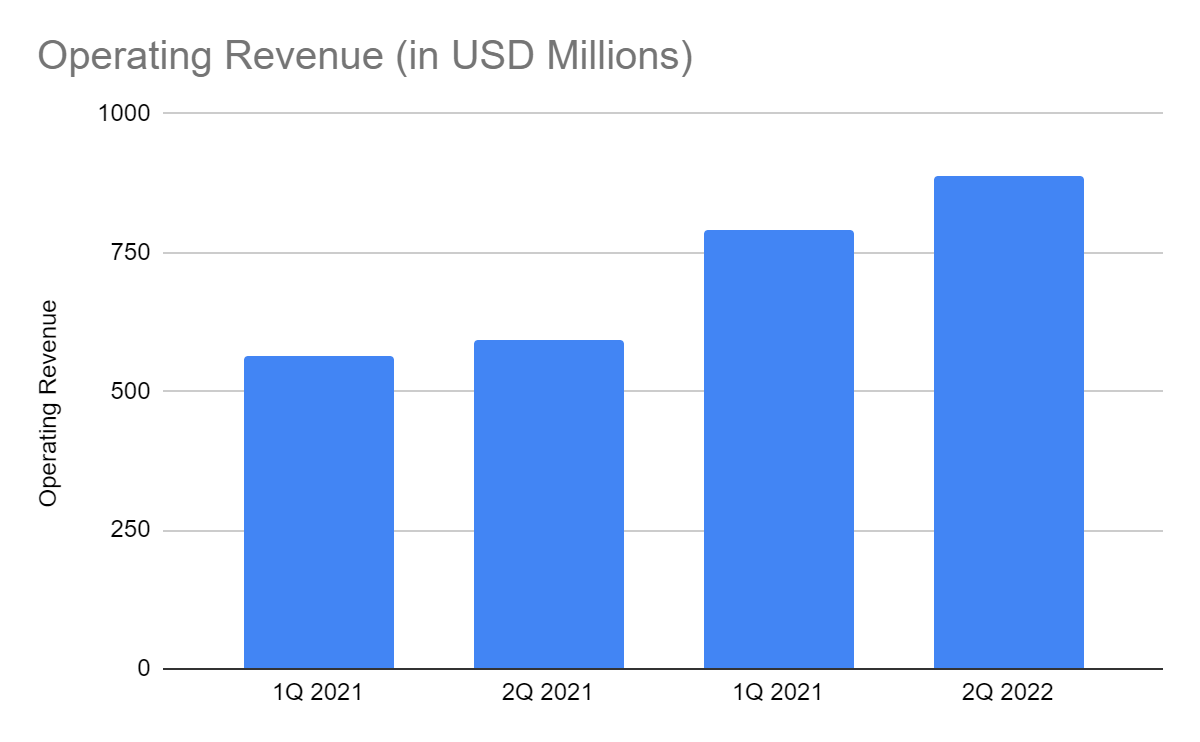

For more than a year, I have watched Arcos Dorados go along with the market trends and expand. It continues to transform in just a half year. Its operating revenue of $888 million is a massive growth from 2Q 2021. It is also a 12% increase from 1Q 2022. Indeed, ARCO sustains its recovery, allowing it to bounce back to pre-pandemic levels. If the trend continues, it may be higher than in 2017, the highest value in the last five years. ARCO does not stay comfortable with its current performance. In fact, it aims to increase its operating capacity to capture more demand.

Operating Revenue (MarketWatch)

Moreover, its capitalization on expansion and technology continues to pay off. Its popularity and solid customer base are some of its cornerstones. It has the largest restaurant visits in the region, with the number increasing from 2020 to 2022. With its numerous openings, it now has 2,286 restaurants from 2,273 in 1Q 2022. But, the primary factor is its digital platform with over ten million active users. It has a wide gap from its closest competitor with only four million users. That is why it comprises 41% of the total sales.

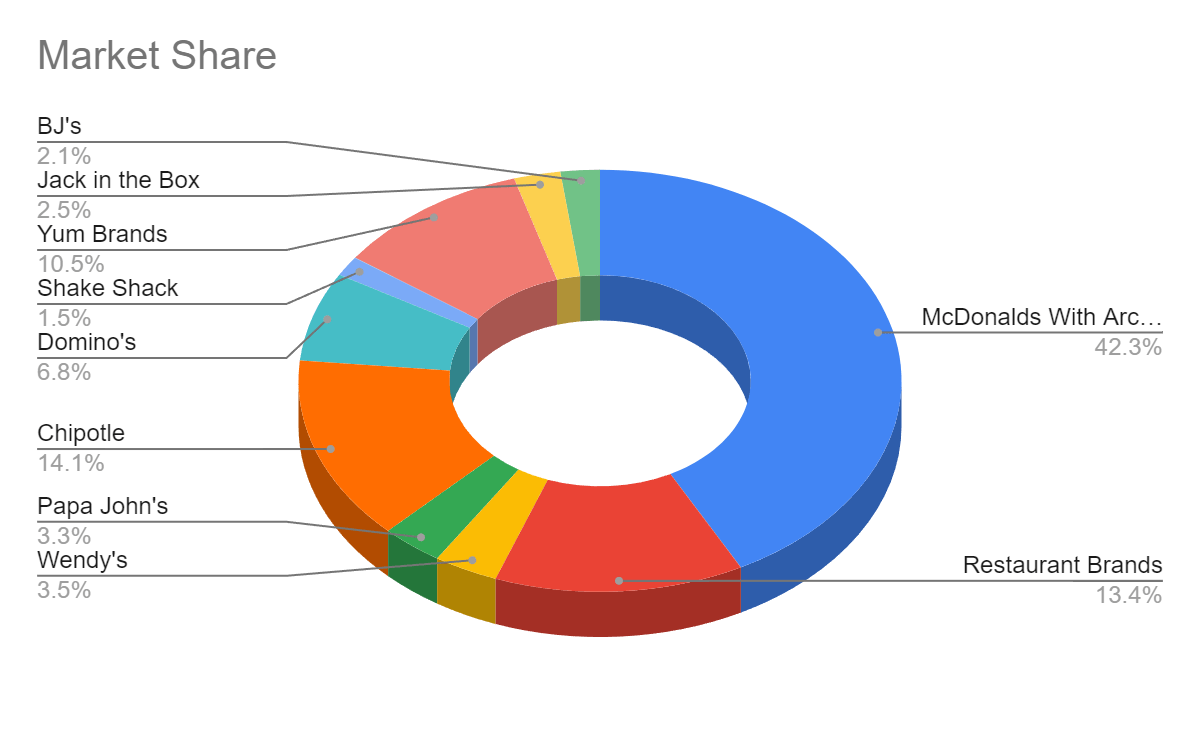

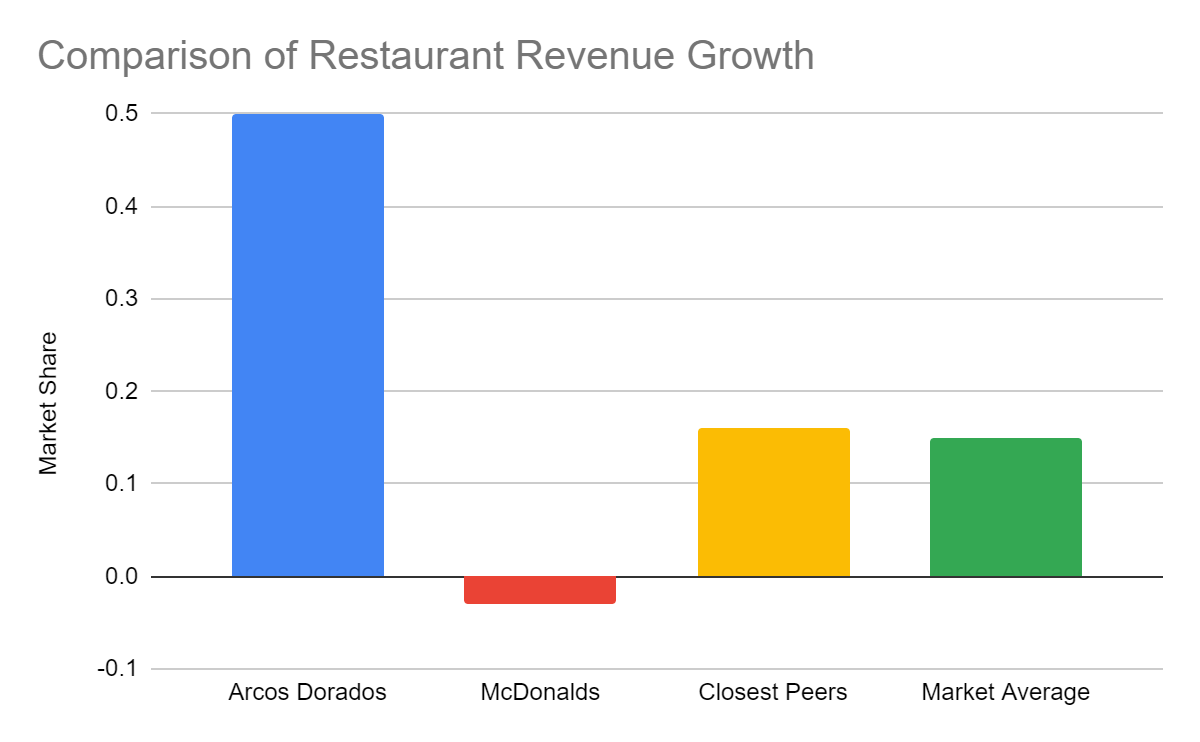

With regards to the competition, we can check the closest peers of McDonald’s. Although ARCO does not compete with them, they have an indirect impact through MCD. The combination of MCD and ARCO remains a force to reckon with. They hold 42% of the global market share. But, it is lower than in 1Q 2021 at 44%. If you check it, the decrease in market share is due to MCD. ARCO has revenue growth of 48% while the market average is 15%. Its market share is 5.7% vs 4.1% in the comparative quarter.

Market Share (MarketWatch)

Comparison of Revenue Growth (MarketWatch)

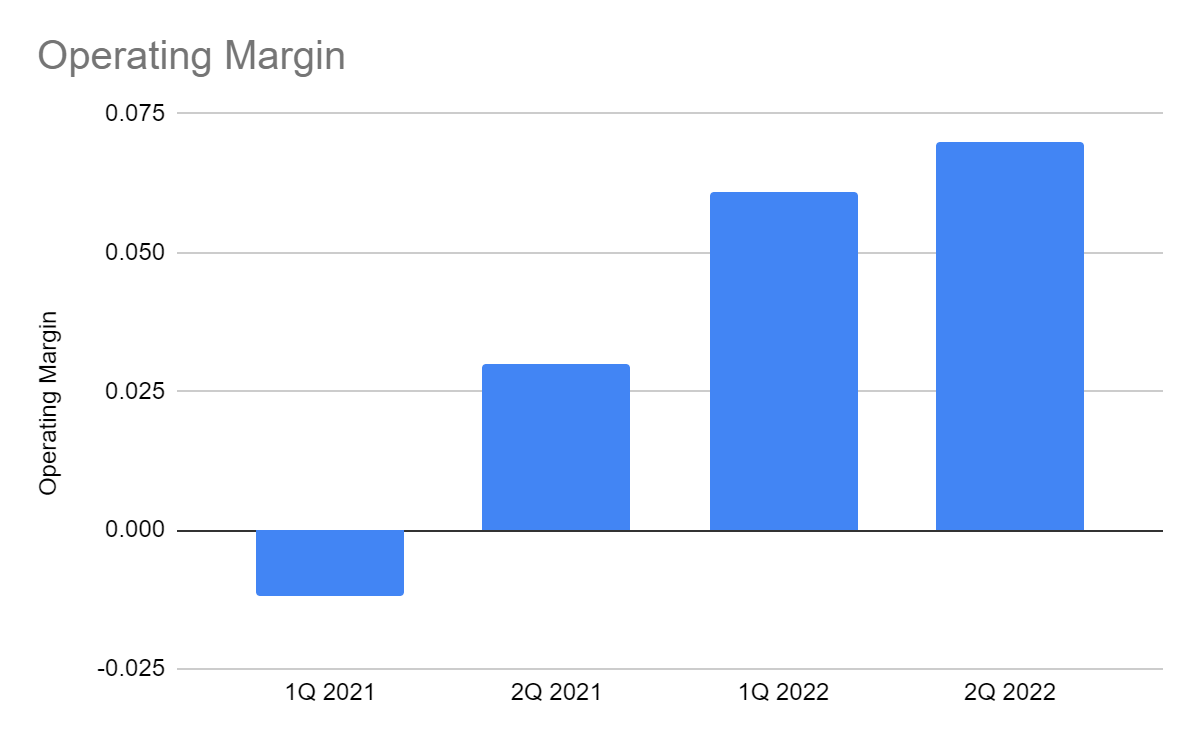

Indeed, ARCO shows absolute and comparative growth. It is also capable of going head-to-head with some of its larger peers. Even better, it has prudent asset management amidst its expansion and transformation. Its costs and expenses are increasing as its operating capacity increases. But, its strategies generate more returns. Revenue growth offsets the increase in costs and expenses. Also, its prime costs are 61% of the operating revenue. It is still lower than the maximum percentage of 63% for restaurants. The operating margin of 7% is more than twice as much as in the comparative quarter.

Operating Margin (MarketWatch)

Potential Risks and Competitive Advantage

Arcos Dorados is a sturdy figure in Latin America and the Caribbean. But, the economy has not recovered yet. Inflation is not helping the operations across industries. Port congestion is getting better, but its improvement remains slow. Both external pressures may affect the supply and demand for the products. Monkeypox is another looming factor that may affect the operations. Another lockdown may affect business operations and employment. Hybrid and remote work setups are popular, but other industries may not afford them.

But thankfully, ARCO is well-positioned to cushion the blow of these uncertainties. Its store openings and digital transformation may become its offense and defense. Its efforts and strategies will not be futile. As discussed, it has 2,286 restaurants, making it the densest in the region. It is an advantage to increase its market visibility. But, its digital platform is vital to keep most of its customers. Again, it has ten million active users. Aside from its popularity and customer base, technology is its primary growth driver. It works best in lockdowns and remote work setups. Despite the restrictions, its digital app allows virtual and cashless transactions. It may stay afloat and remain strong, given its effort to speed up its digital transformation.

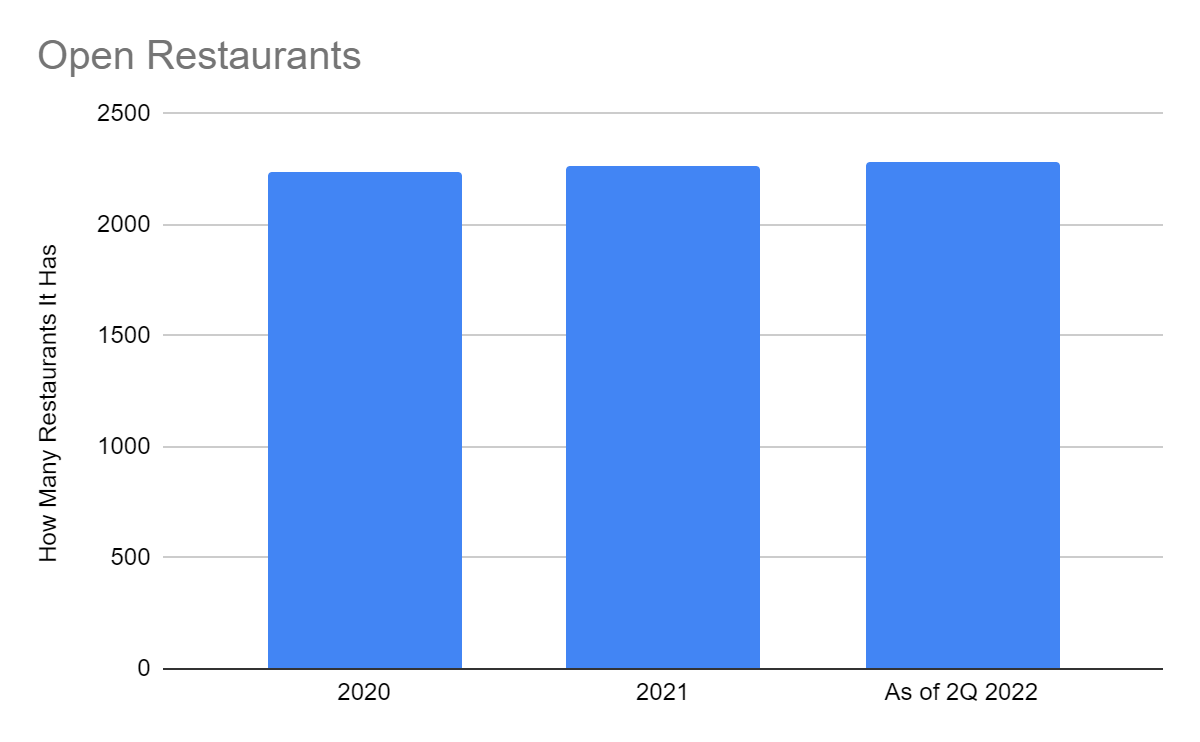

Also, its focus on free-standing restaurants may help it lessen its lease expenses. It expects to open 200 new restaurants, 90% of it or 180 locations free-standing. Out of the total number of restaurants, 62% of them are free-standing. So, it may limit its operating expenses in the long run. As of 2Q 2022, ARCO has made 71 restaurant openings. It is now over 30% of its target. It still has more than two years to achieve it. In Argentina, it is 4.5x more visible than its closest competitor. In Brazil and Chile, its visibility is larger by 4x and 2,5x than its closest competitor. Suppose all restaurants have the same operating revenue. The average will be $153,659. It is an increase from $136,898 in 1Q 2021. On average, the marginal revenue is $38,316 per restaurant.

Open Restaurants (2Q Investor Presentation)

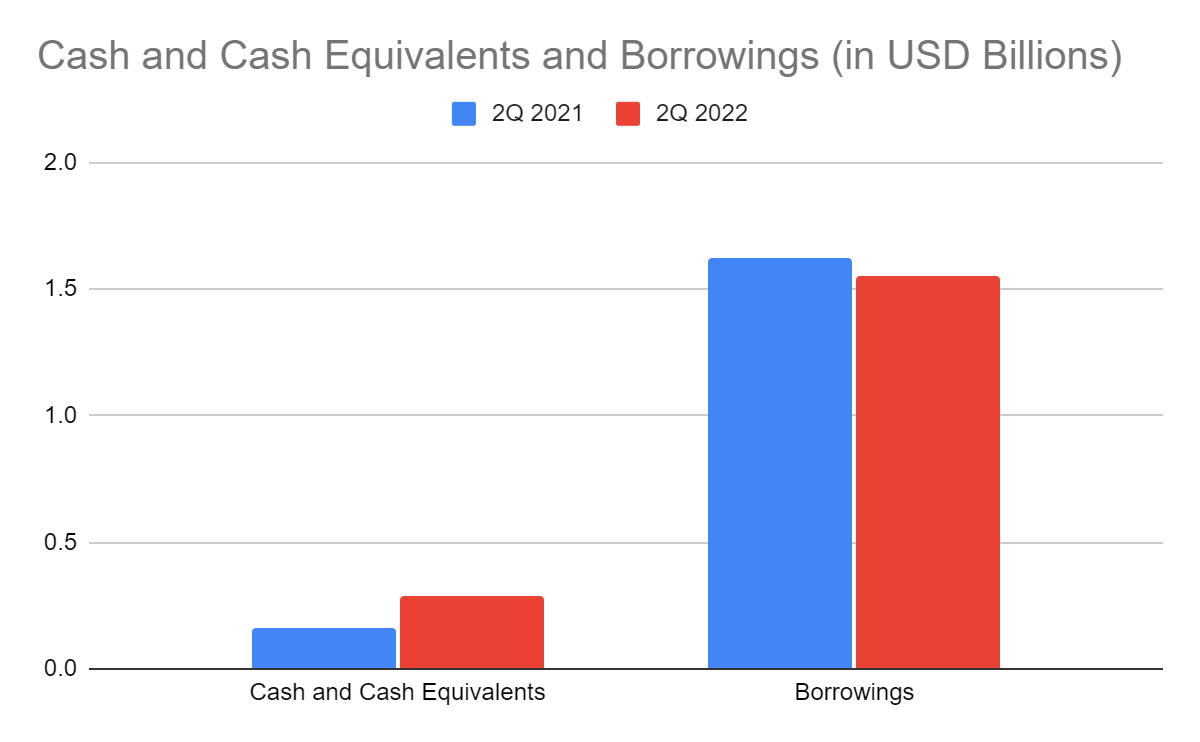

Another edge of Arcos Dorados is its financial stability. It has excellent liquidity, allowing it to expand while keeping its borrowings payable. Its cash levels are increasing, which is not surprising, given the steady cash inflows. Its cash and cash equivalents of $289 million comprise 12% of the total assets. It is a 78% increase from the comparative quarter, which was only 7% of the total assets. As such, the liquidity of the company is improving. Also, borrowings are stable at $1.55 billion vs $1.62 billion. From 10%, the percentage of cash and cash equivalents to borrowings is now 18%. Its Net Debt/EBITDA is 3.52x, which is within the maximum range of 3.5x-4x. So, it is earning enough to cover its borrowings. Cash and cash equivalents alone can cover its current borrowings. It becomes more capital intensive as it opens more free-standing restaurants.

Cash and Cash Equivalents and Borrowings (MarketWatch)

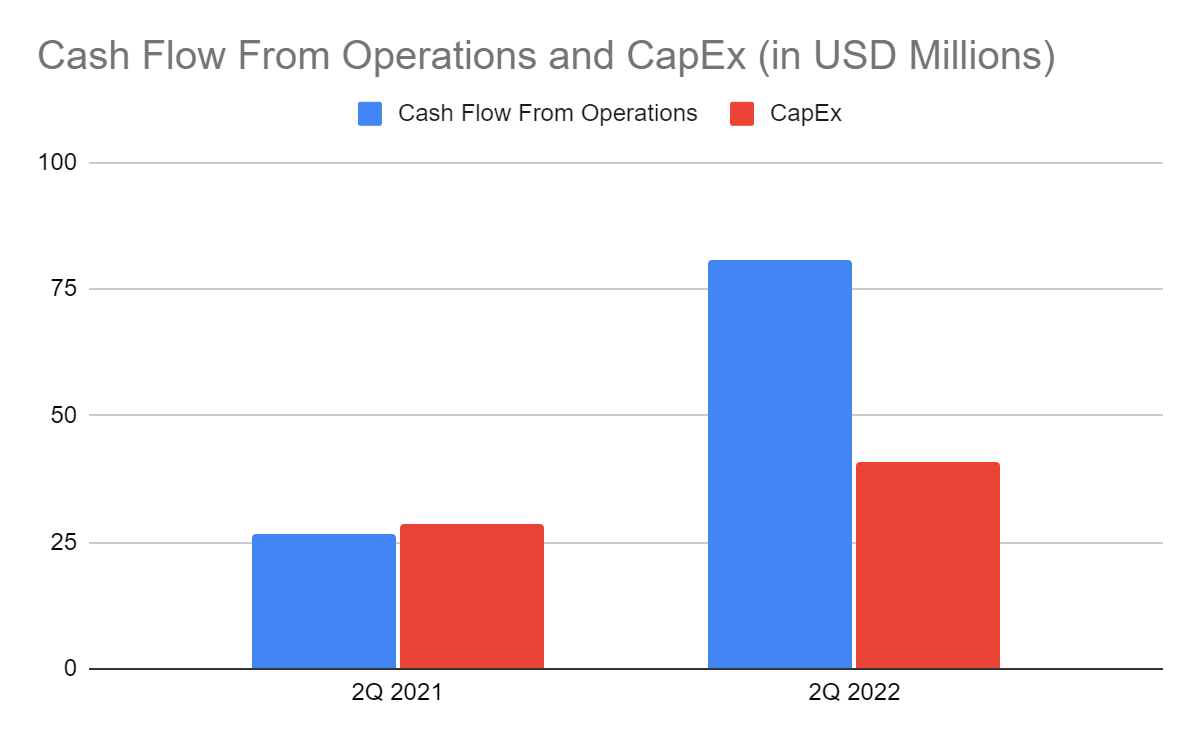

We can confirm using the Cash Flow Statement. Its Operating Cash Flow amounts to $80 million, a massive increase from 2Q 2021 and 1Q 2022. Likewise, CapEx amounts to $41 million vs $28 million in 2Q 2021 and $24 million in 1Q 2022. The FCF/Sales Ratio is 4.5% vs -0.003 in 2Q 2021 and 1.3% in 1Q 2022. It is good to have an increasing ratio since it requires more FCF to sustain its expansion.

Cash Flow From Operations and CapEx (MarketWatch)

Stock Price Assessment

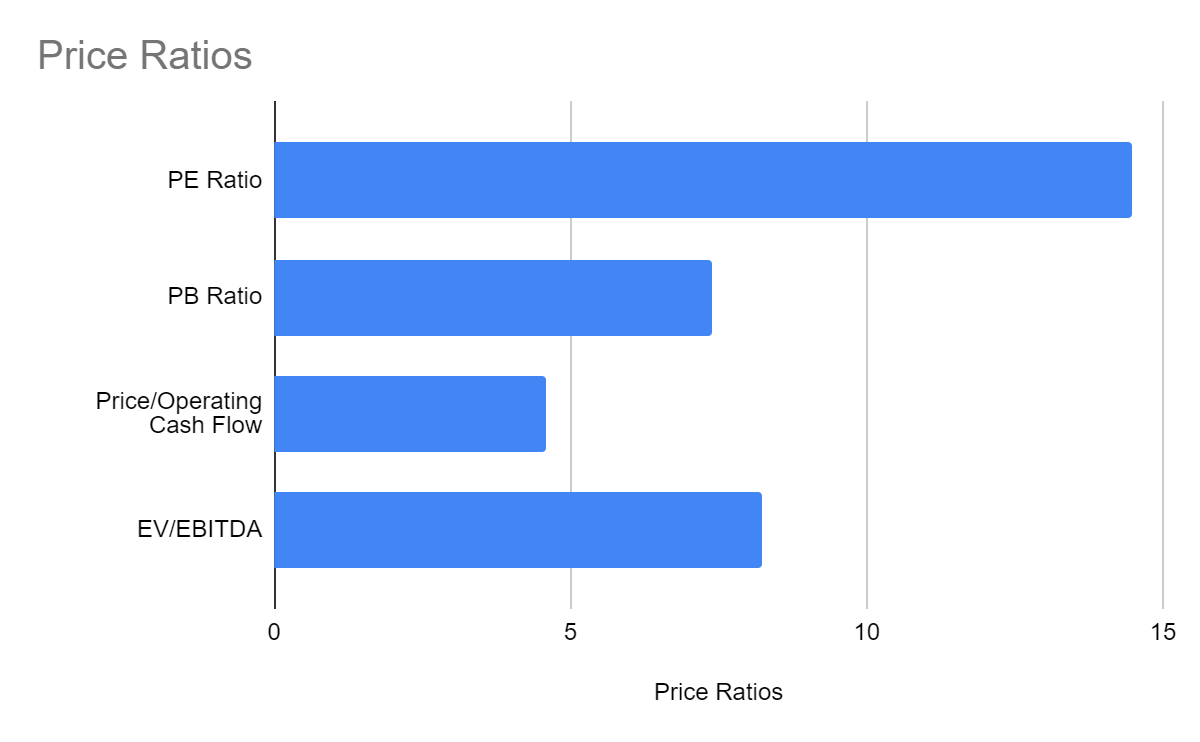

The stock price appears to be moving sideways with a slight uptrend after its dip in July. But, it is still lower than the stock price in my previous article. At $7.51, it is already 26% higher than the start price. It is 5% lower than the stock price in my previous article but 20% more than the most recent dip. The price is still acceptable based on the ratios below. For the PB Ratio, it is high at 7.4. But, it may not be accurate for capital-intensive industries like restaurants. To make it uniform, the acceptable ratio, in general, is 1 or below. But, it appears to vary with different industries. In fact, analysts estimate that the average PB Ratio of the restaurant industry is 9.9650.

Price Ratios (Seeking Alpha)

Also, it covers dividend payments, giving a yield of 1.99%. It may appear low but is still above the average dividend yield of the S&P 600 components. The Dividend Payout Ratio using FCF is 24%. The company has adequate cash inflows to sustain its CapEx, borrowings, and dividends. To assess the stock price better, we will use the discounted cash flow (“DCF”) Model.

DCF Model

FCFF $74,000,000

Cash and Cash Equivalents $288,000,000

Outstanding Borrowings $81,000

Perpetual Growth Rate 4.8

WACC 8.4

Common Shares Outstanding 210,595,000

Stock Price $7.51

Derived Value $10.74

The derived value shows that the stock price is undervalued. There may be a 43% upside in the next 12-18 months. It may also be reasonable, given its continued expansion and transformation.

Bottom Line

Arcos Dorados Holdings, Inc. remains a durable company in a still challenging market landscape. It keeps expanding with adequate cash levels and manageable financial leverage. Also, it has attractive growth prospects with its expansion, digital transformation, and dividends. The stock price is still affordable. The recommendation is that Arcos Dorados Holdings, Inc. is a buy.

Be the first to comment