OlenaMykhaylova/iStock via Getty Images

Archer-Daniel-Midland (NYSE:ADM) is one of the world’s leading agricultural origination and processing companies. It processes corn, oilseeds, and wheat into products for food, animal feed, industrial, and energy uses. It owns milling and processing facilities globally and runs commodities trading operations for a wide range of customers. This is in addition to being a leading provider of other specialized products and services in the global agricultural value chain.

Listed on the NYSE in 1924, ADM currently has a $50 billion market cap, around 40,000 employees and operations in more than 200 countries. As a result of its heritage, scale and global success, it is one of the most widely watched stocks in the agricultural products industry.

Three years ahead of target

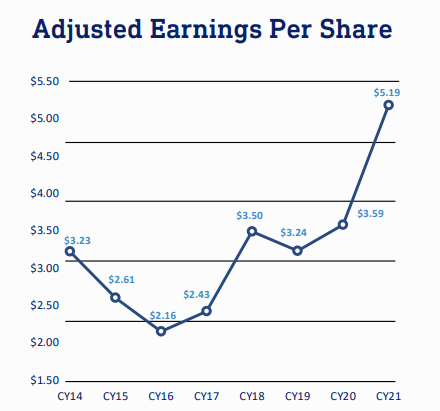

ADM is expected to report its Q4 and FY 2022 earnings in late January and has an impressive track record of beating EPS expectations for 13 consecutive quarters. With a consensus estimate of $7.54 for FY2022 EPS, it’s safe to conclude that ADM will surpass its 2025 Strategic Goal of EPS of $6-$7 three years ahead of target.

ADM’s strategic targets for EPS growth are laid out in the company’s latest comprehensive investor presentation, which also provides great context of how its journey of creating shareholder value has evolved in the past five to seven years

The chart below, drawn from the presentation, shows that after the 2014 – 2016 slump in EPS, investors have been greatly rewarded with steady EPS growth in the years that have followed.

ADM Investor Handout

This strong EPS growth has translated into value for shareholders through increased dividend payouts and strong growth in the stock price. Paid quarterly, the dividend has grown 33% from $0.30 per share in 2016 to the current $0.40 per share. 2022 marks 29 consecutive years of dividend growth and the stock has rallied 37% YTD. It has more than doubled since 2017, indicating that long-term holders have been handsomely rewarded through a combination of capital gains and income growth.

Excellent growth and execution

The main contributor to ADM’s outperformance in recent years has been the global macroeconomic, trade and geopolitical backdrop, which has been constructive for commodities generally and not just food and agricultural products.

The pandemic, supply chain disruptions, Russia’s invasion of Ukraine and runaway inflation have all had an outsized impact on the price of agricultural commodities globally. This is well documented and needs no detailed analysis beyond perhaps looking at how the price increases impacted ADM’s topline growth.

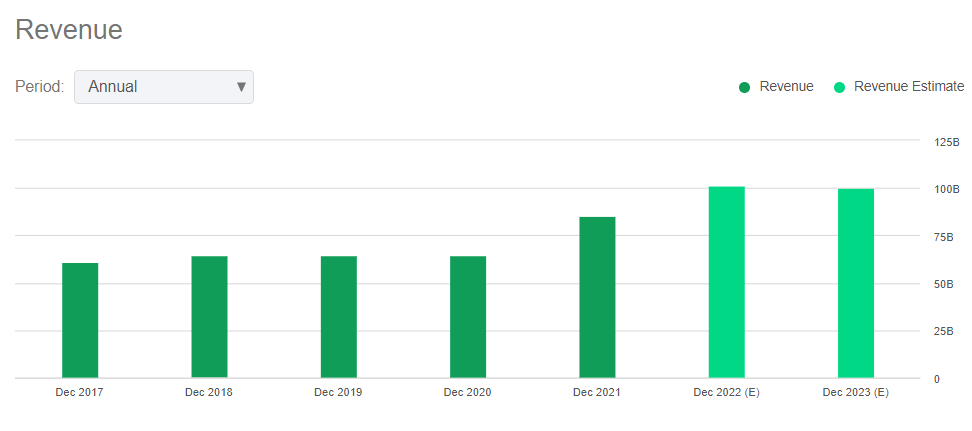

Analysts expect ADM to rake in revenues of $101.90 billion in 2022, up from $85.25 billion in 2021. It was much lower in prior years at around $64 billion as per the chart below, highlighting the impact of commodity price increases on ADM’s revenue.

Seeking Alpha

Price increases for agricultural products have, however, not been the only driver of ADM’s superb growth. The excellent execution by the management team also deserves credit.

The company’s management has been able to notably improve margins in recent years, in line with their mandate as the stewards of the enterprise to prioritize value creation for shareholders.

ADM currently has gross margins of 7.56% vs a 5 year average of 6.76% and EBITDA margin of 5.35% vs a 5 year average of 4.42%. This is impressive considering that, despite the increase in selling price of agricultural products, the management has had to grapple with increased input and manufacturing costs brought on by higher food costs, higher energy costs, higher maintenance expenses, and higher salaries and benefit costs amid a strong labor market.

Another sign that the management is executing well is that it is thinking strategically about the future and making smart and sizable investments in opportunities that can drive growth and unlock value.

If you look at the latest 10-Q under the Management’s Discussion & Analysis section (page 36 and 37) there’s a long list of short and long-term projects that ADM has put money and resources behind in 2022.

These projects offer the opportunity for both organic growth and growth through M&As. I’ve sampled a few of them below but you can look at them in more detail on page 35 and 36 of the latest 10-Q.

-

Acquisition of Comhan, a leading South African flavor distributor, (acquired in Feb 2022)

-

Establishing a $300 million protein innovation center in Illinois (due in Q1 2025)

-

MOU with Bayer (OTCPK:BAYZF) to build a sustainable crop protection model with soybeans farmers in India (announced June 2022)

-

Opening of the company’s first science and technology center in China, bringing state of the art innovation and R&D that serves China and Asia Pacific region (September 2022).

-

Partnership with PepsiCo (PEP) to collaborate on projects that expand regenerative agriculture in their shared value chains in North America (September 2022)

ADM has essentially not rested on its laurels in its moment of glory. Success usually brings complacency, so to see the opposite at play in ADM is a positive sign.

Longer-term, the opportunity for ADM could lie in the ongoing transition to clean energy as the company is one of the three largest publicly traded producers of fuel-grade ethanol in the U.S. The rapidly growing global population is also a positive long-term tailwind at play.

Watch out for changing market trends

I’m a bull when it comes to my long-term outlook of ADM and hold some of its shares in my portfolio. The valuation looks relatively low despite it trading near all-time highs. It has a P/E (‘fwd’) of 12.50x and an EV/EBITDA (‘fwd’) of 9.50x.

However, I wouldn’t add to my position right now. To maximize returns and minimize risks, I believe it’s better to hold your position or trim a bit of it to lock in some gains.

My reasoning is that the 38% run in the stock in 2022 is likely to moderate in 2023 as earnings growth is expected to stabilize in line with cooling growth in food prices. Analysts expect ADM to post revenues of $100.15 billion in 2023 vs $101.90 billion in 2022, signaling the slowing food inflation that will likely have an inverse relation to ADM’s revenue and earnings growth.

Importantly, equity markets in developed countries like the US are also likely to see shifts in 2023 that could lead to profit taking in defensive consumer staple stocks like ADM and subsequent reallocation of capital to other “risk-on” areas like tech and growth stocks.

This expectation is based on the increasing likelihood that interest rate hikes could pause some time in 2023, with rates possibly getting cut in following years. This is based on the view of most economists, who see the Fed and other central banks pausing tightening in 2023 amid signs of slowing inflation.

Overestimating the longevity of a cycle can be a costly mistake that diminishes investors’ total returns, even when the overall performance is positive. ADM has been a good investment in recent years thanks to the favorable commodity cycle. However, adding or initiating a new position now isn’t the best idea given that changes in interest rate regimes could lead to equity sell offs in the broader consumer staples sector.

Conclusion

I’m bullish on ADM’s long-term picture but I’m not eager to add to my position at current levels given where I think the markets are headed in 2023. I’ll wait for the volatility to come and buy the dips to maximize my long-term return. Until then, it’s a hold and wait game where my patience is being rewarded by a reliable quarterly dividend that is likely to continue growing in coming years.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment