Stephanie Keith

Apple (NASDAQ:AAPL) released its fiscal fourth quarter earnings Yesterday. The results beat expectations on both revenue and EPS. Revenue came in at $90 billion, up 8% and ahead of the $88 billion estimate, while earnings per share were $1.29, ahead of the $1.27 estimate. Investors took the earnings very well. The stock rose in-pre market trading on Friday, and even more through the trading day. The guidance was less impressive than the release itself: the company refused to provide revenue guidance and said that it expected deceleration due to a 10% Forex hit. It did not forecast an actual decline in revenue, which looked strong compared to what other tech companies did in Q3.

Apple’s release showed strength across many of its business segments. Hardware revenue grew 9%, iPhone revenue grew 9.8%, wearables grew 9.8%, and even services grew 4.98%. I use the word “even” here because services is the part of Apple’s business that’s most similar to those of the ad-tech companies that missed badly on earnings this week. The segment includes app store advertising and a variety of other software offerings; the fact that its revenue increased was extremely impressive after other software companies dropped the ball in Q3.

Apple’s stock stumbled in the weeks heading into the release. Expectations were low, peer companies missed earnings estimates, and a rumor circulated saying that Apple cut iPhone 14 Plus production. I was personally optimistic heading into earnings, as I knew that the iPhone 14 rumor was overblown (the 14 Plus is just one of four iPhone 14 models). Still, the magnitude of the earnings beat impressed me. I was not expecting Apple to grow the top line faster than Alphabet (GOOGL) did, nor was I expecting positive earnings growth. It was not only a good showing by the low standards of big tech in 2022, it was a great showing in any market. In the fourth quarter of 2019, Apple’s revenue only grew 2%, so Apple is, in the middle of a bear market, growing faster than it did in the 2019 bull market.

On the day this article was written, Apple rallied 7.6%, its best showing since July 2020. Most likely, the stock got a lift from its favorable comparison to other tech stocks. Meta (META), Alphabet and Amazon (AMZN) all missed, Microsoft (MSFT) beat but fell due to poor guidance. Apple’s large beat and relatively upbeat guidance lifted the stock, which was the only ‘FAANG’ name to post truly good news in the quarter just recorded. Therefore, the 7.6% one day rally was quite justified, and there are reasons to think Apple could head much higher than the level it trades at today.

Competitive Landscape

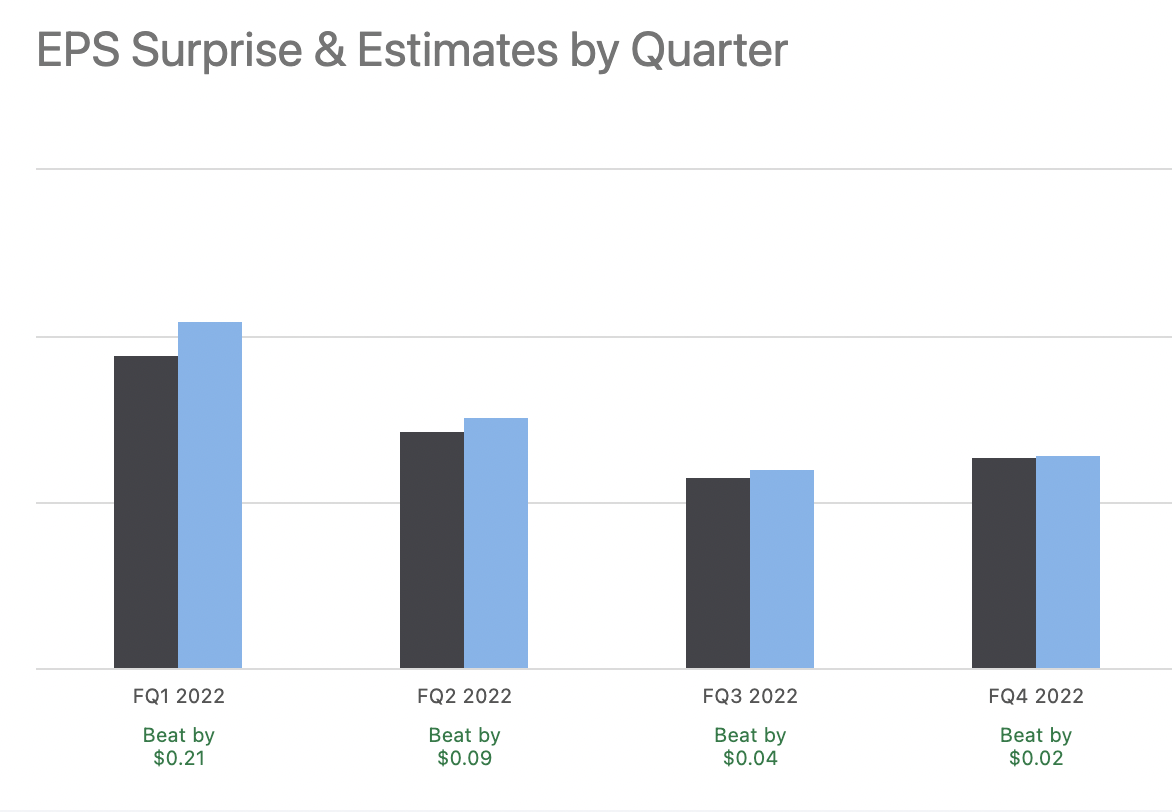

Apple has a pretty good track record with earnings. It scores a ‘C’ on revisions in Seeking Alpha’s Quant system, which might sound low, but remember that revisions refers to estimates, not reported results. Apple beat estimates in all of the past four reported quarters, but its 2023 guidance was a little below expectations.

Apple’s earnings beats (Seeking Alpha Quant)

One of the big reasons why Apple does so well on earnings is because of its competitive position. In general, a company with a solid position in its industry will produce good earnings over time. There are exceptions, of course: a solid position in a dying industry won’t save you. But Apple has a solid position in a good industry, so its earnings should be at least adequate most of the time.

How do we know that Apple has a solid competitive position?

It comes down to three things:

-

Customer loyalty.

-

Brand strength.

-

The ecosystem strategy.

Apple’s customer loyalty is legendary. Apple itself touted this factor as one of the reasons for its Q4 beat. Additionally, the firm ‘Access’ calculated Apple’s brand loyalty (defined as customers who repeatedly buy similar products) at 87%. That figure is higher than average, so Apple’s claims of having high customer loyalty are backed by third party studies.

Next up we have brand strength. Apple was rated the world’s most valuable brand in 2022 by the Visual Capitalist. This is both a factor in itself, and also an explanation of factor #1 (customer loyalty). Apple’s brand strength gets people interested in the first place, and it also keeps existing customers coming back for more. So Apple’s brand strength contributes to both gaining and retaining customers.

Finally, we have the ecosystem strategy. Apple puts a lot of emphasis on building an interconnected ecosystem of devices that integrate well with each other. When you buy a new MacBook with an existing Apple ID, your iPhone, iCloud and other apps are immediately connected. You can achieve this integration by combining other tech companies’ products, but that usually involves downloading apps after you’ve finished setting up your computer: Apple lets you integrate all your devices before setup is complete. This incentivizes buying one Apple product after another, which leads to repeat sales.

Google is the only other company that offers anything close to this. It’s attempting to build an ecosystem of its own, but the problem is, it drops products from its lineup so frequently that the ecosystem isn’t consistent. For example, it just recently axed the next generation PixelBook due to poor sales. Because of moves like this, Google rarely has a truly up-to-date ecosystem; in order to integrate all your Google products together, you sometimes have to buy outdated models. Technically, a Google ecosystem exists, but it is very rarely “complete.”

It’s also worth noting that, even if Google’s ecosystem does become a thing, then Apple will only have one real competitor. The rest of big tech has totally given up on building ecosystems. Microsoft left the smartphone game entirely, while Amazon only builds a few of the devices used in a typical ecosystem. So the worst case scenario for Apple is it has to compete with Google, it’s not going to face an avalanche of competition that appears out of nowhere.

Financials and Valuation

Having looked at Apple’s competitive position, we can now move on to its financials and valuation.

In the most recent quarter, Apple delivered:

-

$90 billion in revenue, up 8%.

-

$38 billion in gross profit, up 8.2%.

-

$24.8 billion in operating income, up 4.7%.

-

$20.72 billion in net income, up 0.82%.

-

$1.29 in EPS, up 3.2%.

-

$122 billion in full year cash from operations, up 17%.

It was a pretty solid showing in terms of growth. In addition, the profitability was healthy. Based on the metrics above, we get a 42% gross margin, a 27.5% EBIT margin, and a 23% net margin. A big win on all of these metrics.

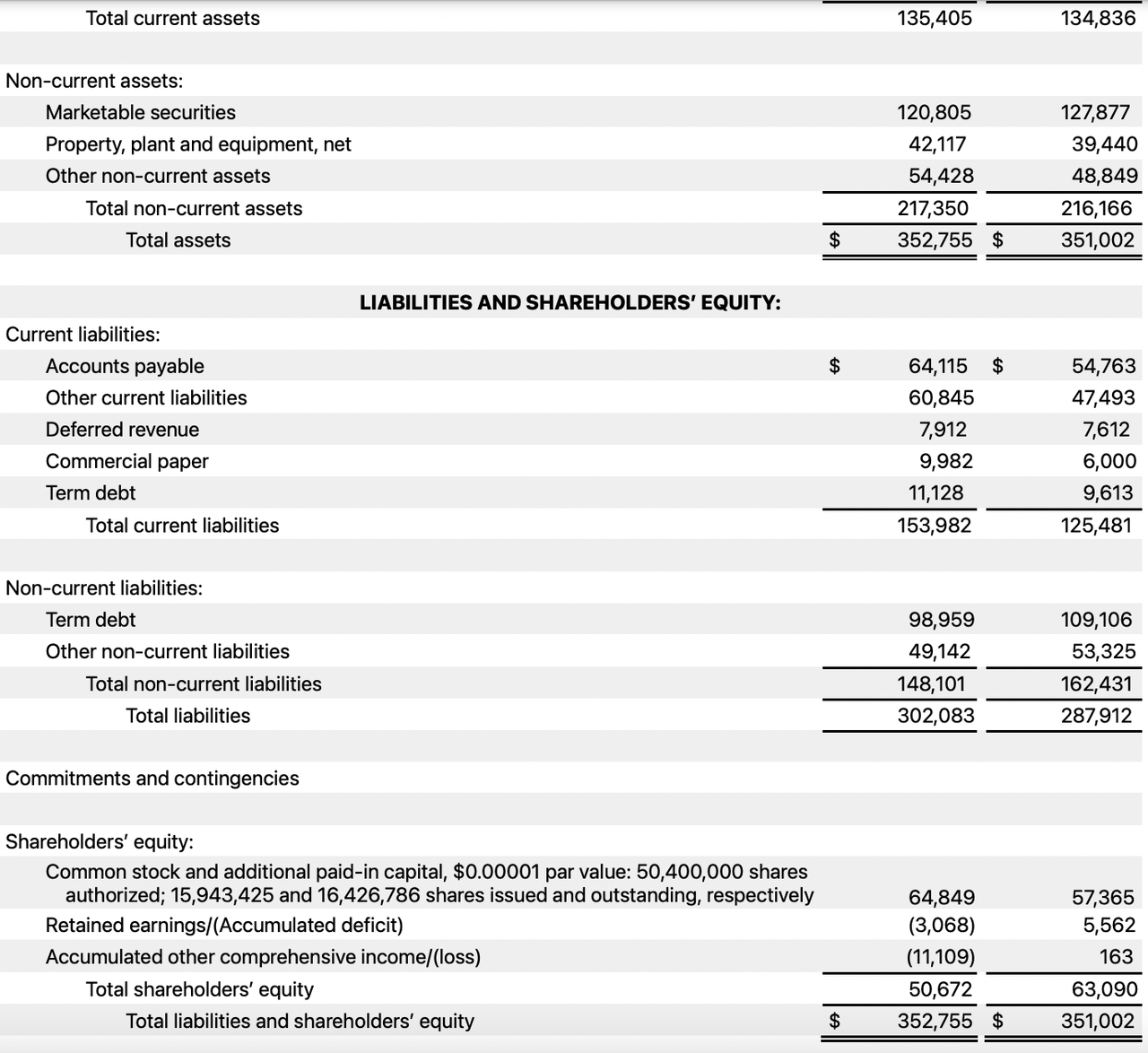

Apple’s balance sheet is less good than its quarterly performance. Based on the fourth quarter balance sheet, you get a 0.88 current ratio and a 1.95 debt/equity ratio. Typically you want the current ratio to be above 1 and the debt to equity ratio to be below 1, so Apple’s most important balance sheet metrics are a little less than ideal. With that said, All of Apple’s debt together is worth less than a year’s operating cash flows, so you can argue that asset-based solvency metrics aren’t that relevant here.

Apple Balance Sheet (Apple)

Now, let’s move on to the valuation. According to Seeking Alpha Quant, Apple trades at:

-

23.7 times earnings.

-

6.1 times sales.

-

40 times book value.

-

19.7 times operating cash flows.

This is a pretty mixed picture. The sales and book value ratios are very high, but the earnings and cash flow multiples aren’t. We would conclude that Apple is richly but not “insanely” valued based on multiples alone. Discounted cash flows present a different picture. Apple had $6.87 in free cash flow per share in the trailing 12 month period. If you assume that Apple stops growing this year, and discount its FCF at the treasury yield (about 4%), you get a $171 terminal value estimate, which is higher than today’s price. If you assume that cash flows grow at 5% per year and then stop growing after that, you get a total fair value estimate of $215. If you add a 1% risk premium on to the treasury yield you get $171 in fair value, the same as in the “no growth from here on” scenario at a 4% discount rate. So, assuming that interest rates don’t go TOO high, Apple is worth buying today.

The Big Risk to Watch Out For

As I showed above, Apple stock is basically undervalued in today’s economic conditions. However, it is somewhat vulnerable to rising interest rates. If the treasury yield were to rise to 6%, Apple would need to grow much faster than 5% per year in order to be worth buying. It isn’t conservative to just assume that a huge company will grow faster than 5% per year forever, recessions make 10% growth hard to achieve. Currently, Fed officials are aiming for a 5.25% terminal fed funds rate. If the treasury yield stays pretty close to the Fed funds rate then Apple will remain a buy, but if it goes higher than that, it won’t be so attractive. So, if you’re going to buy Apple, pay attention to the macro picture. The stock is expensive enough to be vulnerable to monetary tightening.

Bottom Line

Putting everything together, Apple stock looks like a great value in 2022. Certainly, it’s a comparatively good value by the standards of big tech. One of the few FAANG names still delivering positive growth in earnings and cash flows, it really stands out. Just be careful not to chase the stock price ever higher, because the ongoing monetary tightening does weaken the thesis a little. I would not personally be buying at prices higher than $171.

Be the first to comment