Remains

What happened?

Apple (NASDAQ:AAPL) just issued a press release yesterday (11/6) saying that Covid disruptions at an iPhone assembly plant in Zhengzhou, China have temporarily impacted the production of iPhone 14 Pro and 14 Pro Max.

“The facility is currently operating at significantly reduced capacity.” – Apple

As a result, the company now expects lower 14 Pro and 14 Pro Max shipments and longer customer wait times. For 4Q22, the Street currently expects 82 million iPhone shipments and revenue of $127 billion (+2.5% YoY). Given Apple’s announcement, these figures are likely too high, and analysts have already begun cutting their Q4 estimates.

What’s the damage?

The most direct impact is longer wait times for customers looking to purchase the 14 Pro and 14 Pro Max models. Per my last article that discussed how lead times for the 14 Pro/14 Pro Max increased from 24 days in week 7 to 31 days in week 8 since launch (ended 10/28), iPhone wait times are likely to stretch out even further now that operations at the Zhengzhou assembly plant face lower utilizations. The facility owned by Foxconn is responsible for about 60% of iPhone assembly capacity.

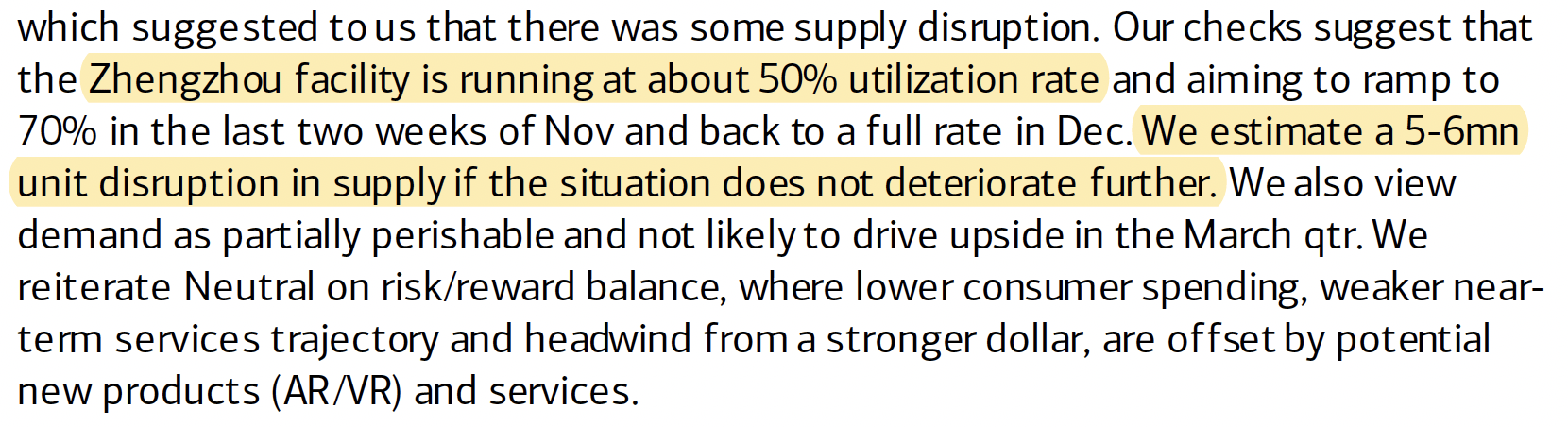

Per BofA checks, the Zhengzhou facility is currently at a 50% utilization rate and expects utilization to increase to 70% in the last 2 weeks of November and ultimately 100% in December. In terms of how many iPhones will not be shipped due to Covid restrictions, BofA believes it’ll be 5-6 million units, while Barclays thinks the number could be as high as 10 million units. Of course, there’s no telling whether local conditions will improve as expected.

BofA Barclays

Assuming 5 million in lost shipments in Q4, split evenly amongst 14 Pro ($999) and 14 Pro Max ($1,099), this comes down to a revenue impact of roughly $5.2 billion vs. consensus Q4 iPhone revenue of $73.4 billion. This also represents a 4% impact on the estimated Q4 total revenue of $127 billion. Overall, it doesn’t look that bad, but there’s the possibility that some of the unfulfilled demand in the current quarter will likely be lost due to weakening consumer spending.

In the September quarter, Apple grew revenue by 8% YoY and expected YoY revenue growth in the December quarter to be less than 8% with FX impacting the top-line by 10 percentage points. Additionally, management expected a gross margin of 43% at the midpoint in the current quarter. Given the higher ASPs of the 14 Pro and 14 Pro Max, actual revenue and gross margin may come in below guidance.

What to do with the stock?

Apple has been dealing with supply chain challenges over the last few years, and there’s really nothing new with the current disruptions in Zhengzhou that will permanently damage Apple’s business. It’s largely a short-term challenge that will unlikely impact the longer-term demand for Apple’s highly desirable products, so those who will be selling the stock on the news are likely to be short-term traders looking for a quick buck.

That said, I see shares as fairly valued at 20x forward earnings, given Apple’s growth is expected to moderate quite a bit going forward. In FY22 (ended September), Apple grew revenue by 8% vs. 33% in FY21. Going forward, the Street expects revenue to grow just 3.2% and 5.4% in FY23 and FY24. Based on a challenging macro and deteriorating consumer affordability, I see a higher chance of downward revisions vs. upward. While I remain a shareholder, I will not look to add to my position until further price corrections.

Be the first to comment