Shahid Jamil

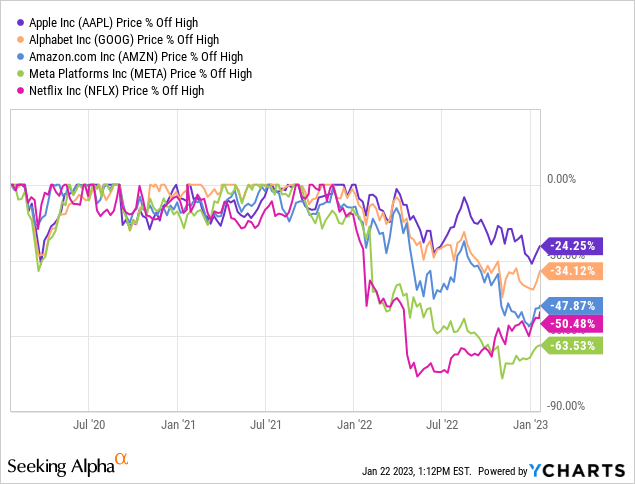

In my most recent article about Microsoft Corporation (MSFT), I pointed out that the U.S. software giant is performing much better than most of the other major technology stocks (or, for example, the former FAANG stocks). However, there is another technology company that also seems to outperform its peers – Apple Inc. (NASDAQ:AAPL).

In the following article, we take a closer look at Apple once again and try to answer the question why the stock is performing better than its peers and if Apple is a good investment now. Since my last article about Apple was published at the end of August 2022, the stock has declined about 11%.

Recurring Revenue And Cult-like Status

In my article about Microsoft, I assumed that the company’s transformation towards subscription might be a reason for the better performance – at least when compared to other mega-cap technology companies like Alphabet Inc. (GOOG), Amazon.com, Inc. (AMZN) or Meta Platforms, Inc. (META).

And we can also make the argument that Apple has been transforming towards a business model that is also generating more and more revenue from subscriptions. In my first article “Apple: Widening its moat,” I explained how Apple is transforming. But in the case of Apple, subscription services account only for a small part of revenue. In fiscal 2022, service sales were $78,129 million and compared to $394,328 million in total sales they account for 19.8%. And in many cases, the revenue from the app store can be seen as rather recurring (due to subscriptions), but people are also making one-time purchases in the app store. Additionally, a small part of “Wearables, Home and Accessories” can also be seen as recurring as revenue from Apple TV is listed in this business segment. And during the earnings call, CFO Luca Maestri underlined the strong growth of subscriptions:

Third, paid subscriptions showed very strong growth. We now have more than 900 million paid subscriptions across the Services on our platform, up more than 155 million during the last 12 months alone and double what we had just three years ago.

Nevertheless, the biggest part of Apple’s revenue are still one-time sales – the purchase of an iPhone, an iPad, or a MacBook is a one-time sale and certainly not recurring (even if some people might buy an iPhone again and again – it is not the same as a subscription). In my article about Microsoft, I explained the difference:

Companies might stop advertisements (or reduce the amount spent) when times are difficult, and shoppers might reduce the amount spent during a recession. However, I (and many others) won’t terminate my subscription of Microsoft 365 and companies probably won’t stop using Microsoft Teams or terminate contracts for Microsoft Azure.

And while not every app is as essential as Microsoft Azure or Microsoft 365 and some app subscriptions might be terminated during a recession, it is much easier to postpone the purchase of a new iPhone for a few months or a year. But we should not ignore the loyal customer base that Apple has. Regarding the loyal customer base, the statements of CFO Maestri are interesting:

“Overall, our installed base of active devices continue to grow nicely. It reached an all-time high for all major product categories and geographic segments at the end of the quarter, thanks to extremely strong customer satisfaction and loyalty and a high number of customers that are new to our products.

(…)

Thanks to our strong iPhone lineup, we set a quarterly record for upgraders and grew switchers double digits. This level of sales performance, along with unmatched customer loyalty, drove the active installed base of iPhones to a new all-time high across all geographic segments. And the latest survey of US consumers from 451 Research indicates iPhone customer satisfaction of 98%.

And while a loyal customer base is not the same as recurring revenue from subscriptions, it could be a close second. A loyal customer base buying a new iPhone or new MacBook regularly can also lead to high levels of stability and consistency for the business.

Quarterly Results and Annual Results

And we should also not ignore that Apple is still reporting solid results – especially compared to other major technology companies, which already seem to struggle a little bit.

In fiscal 2022, Apple generated $394.3 billion in total sales. Compared to $365.8 billion in sales in fiscal 2021, this is an increase of 7.8% year-over-year. Operating income could also be increased by 9.6% year-over-year, from $108.9 billion in fiscal 2021 to $119.4 billion in fiscal 2022. And diluted earnings per share also increased by 8.9% year-over-year, from $5.61 in fiscal 2021 to $6.11 in fiscal 2022.

When looking at the two different revenue segments, services sales as well as product sales contributed to growth. While product sales increased 6.3% year-over-year, from $297.4 billion to $316.2 billion, services sales increased 14.2% YoY, from $68.4 billion to $78.1 billion. And when looking at the sales by category, four out of the five categories contributed to growth. Aside from service sales, iPhone sales increased by 7.0% to $206.5 billion, MacBook sales increased by 12.4% to $40.2 billion, and sales for “Wearables, Home, and Accessories” increased by 7.3% to $41.2 billion. Only iPad sales declined, by 8.2% to $29.3 billion in fiscal 2022.

Is Apple Still Innovative?

One of the decisive questions regarding Apple is: How innovative is the company? Apple is actually an interesting company, and a great case study for several reasons. Without doubt, Apple is a great business, and while the iPhone is still generating most of Apple’s revenue, the company also introduced several new products in the last few years – including the Apple Watch or the AirPods. And both can be seen as very successful.

And while we don’t have accurate sales numbers for the Apple Watch and AirPods, we know that “Wearables, Home and Accessories” generated $41.2 billion in revenue, and these two products are certainly the main contributors for this segment. When talking about innovation, we can also mention that Apple released a number of health-related features – including the Research app, which allows users to participate in medical research studies. And the Apple Watch now has temperature sensing capabilities, retrospective ovulation estimates, and crash detection.

But there are also projects and grand visions that did not play out so far. Regarding the Apple Watch, it was already speculated years ago that Apple might be close to enter the diabetes care market by including a CGM system (continuous glucose monitoring) system in its Apple Watch (in a 2017 article about DexCom (DXCM) I wrote about the speculations if Apple could become a major competitor for Dexcom as well as Abbott Laboratories (ABT)). However, it is still unclear if this project is becoming reality anytime soon – at least the Apple Watch 8 is not able to monitor blood sugar levels.

Another project is Apple’s self-driving car – better known as “Project Titan.” In case of this project, it is also unclear where Apple stands. But it was reported recently that the launch is not before 2026, and the project got delayed again. And Apple seems not to have the ambition anymore to build its own car, but will rather contribute components for other businesses.

Especially for that project, hopes were high it would be able to diversify Apple’ revenue streams, as the dependency on iPhone sales remains high. But in Q4/22, growth was still strong and above Apple’s own expectations:

iPhone grew 10% in the Q4 timeframe to $42.6 billion. Customer demand was strong and better than we anticipated that it would be. And keep in mind that this is on top of a fiscal year of 2021 that had iPhone revenue grow by 39%, and so it’s a tough compare as well. And so we were happy with it.

However, the high dependency on the iPhone remains problematic as it can replaced by a more innovative product of another company. New innovations could make the iPhone obsolete in a few years. Apple seems to be aware of this risk and is investing heavily in research and development as well as augmented reality and artificial intelligence.

And therefore, Apple is a really interesting company. On the one hand, an innovative product from a competitor can put immense pressure on Apple. But we also have a highly profitable and innovative company with a great balance sheet.

Balance Sheet, Share Buybacks and Dividend

When talking about Apple, we should not forget that the company has a solid balance sheet – but to be honest, it is not so great anymore (compared to the balance sheet in previous years). On September 24, 2022, Apple had $11,128 million in short-term debt as well as $98,959 million in long-term debt. When comparing the total debt to the shareholders’ equity of $50,672 million we get a debt-equity-ratio of 2.17, which is rather high. Of course, we should not be worried as Apple generated $119,437 million in operating income in 2022, which is enough to repay all its debt in less than a year.

The question, however, remains: why did Apple raise debt? There are several theories – including theories about financing share buybacks as well as taking on debt to lower its taxes. I am certainly not an expert on taxation and tax laws, and, therefore, can’t evaluate if taking on debt to reduce taxes is a good idea. However, taking on debt for share buybacks is not a horrible idea in my opinion – even if interest rates were law and the stock might be undervalued.

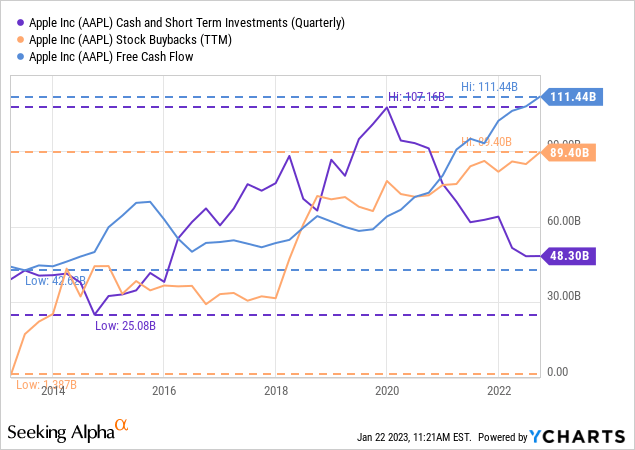

When looking at the financial statements, Apple was clearly focusing on share buybacks in the recent past. Cash and short-term investments clearly decreased since 2020 while the company increased share buybacks. But we also must point out, that Apple is still generating enough free cash flow to finance the share buybacks. In fiscal 2022, Apple generated $111 billion in FCF, which is enough to finance about $15 billion in dividends as well as $89 billion in share buybacks. Therefore, I would not subscribe to the theory that Apple is using debt to finance share buybacks.

Aside from short-term investments, Apple also has long-term investments or non-current marketable securities of $120.8 billion on its balance sheet. And although these investments – mostly different forms of debt securities – are not due in the next 12 months, they are still highly liquid and can in theory be sold at every time. These assets mostly consistent of mortgage and asset backed securities ($19.9 billion), U.S. treasury securities ($18.0 billion) and corporate debt securities ($70.4 billion).

Apple is also paying a quarterly dividend, but that is probably no reason for anybody to be interested in Apple as an investment. Right now, Apple is paying a quarterly dividend of $0.23, which is resulting in an annual dividend of $0.92 and a dividend yield of 0.67%. That dividend likely is not making the stock interesting for dividend investors, but it could be interesting for dividend-growth investors. Apple has now increased the dividend for 9 consecutive years, and in the last 5 years the dividend increased with a CAGR of 8.15%. While the growth rate is not so impressive, Apple is currently paying only about 15% of its annual earnings per share as a dividend, giving the company room to grow the dividend (if it chooses to go down that path).

Summing up, we should not worry about the company’s balance sheet, and if Apple’s doesn’t find better ways to use the generated cash, I support share buybacks (and increasing the dividend).

Intrinsic Value Calculation

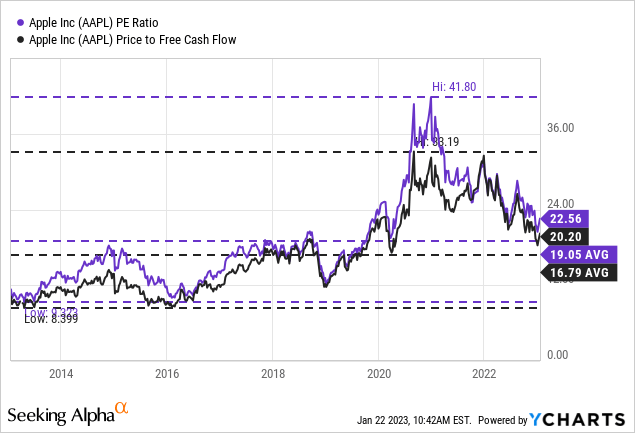

One question remains that should be part of every analysis: Is Apple a good investment or not? And to answer the question, we can start again by looking at simple valuation metrics. Right now, Apple is trading for 22.5 times earnings and 20.2 times free cash flow. Both metrics are slightly above the 10-year average, but neither the P/E ratio nor the P/FCF ratio are extremely high.

And when using a discount cash flow (“DCF”) calculation to determine an intrinsic value, we take the free cash flow of $111,443 million in fiscal 2022 as basis. Calculating with 16,030 million outstanding shares and 10% discount rate, Apple must grow 5% annually from now till perpetuity in order to be fairly valued. Even when being cautious, it seems likely that Apple can grow 5% annually for years to come. In the last 10 years, Apple could grow its revenue with a CAGR of 9.68% and earnings per share with a CAGR of 14.51%. While we should keep in mind that growth rates might slow down further, analysts are still expecting earnings per share to grow with a CAGR of 8.64%. Similar to my last articles, I would still claim that Apple is fairly valued. It is not an extreme bargain, but it is also not extremely overvalued.

Conclusion

Compared to several other technology stocks (and stocks from several other sectors), I would see Apple Inc. not as overvalued – but it is also not a bargain in my opinion. When ignoring the sword of Damocles, which constantly hangs over Apple (can a competitor introduce a product that will make the iPhone obsolete), Apple is a great business.

On Thursday February 2, Apple Inc. is going to report its next quarterly results. It will be interesting to see if Apple is still able to withstand the economy slowing down. According to IDC, smartphone shipments declined about 18% year-over-year. While Apple might gain market shares according to IDC, it will also report declining iPhone sales.

Be the first to comment