Nikada/iStock Unreleased via Getty Images

Introduction

We consider that Apple Inc. (NASDAQ:AAPL) is a “hold” right now. In this article, I will provide evidence that the stock market price ranging between $130 and $170 per share year-to-date is moving around its intrinsic value; in other words, the current stock price is neither expensive nor cheap.

I will show a new perspective about the calculation of Apple’s intrinsic value that will help readers to understand why the stock price has not dropped as some bearish analysts might expect. First, I will use the DCF methodology for making projections of the current Apple’s products and services. Second, I will include the virtual and augmented reality products AR/VR in the calculation taking the assumptions made by one of the most reliable analysts about Apple – Ming-Chi Kuo from TF International Securities, and GlobalData Forecasts; the goal is to estimate a present value of the projected free cash flow (FCF) that would be generated by the AR/VR products that would be launched in 2023. Finally, I will add the effect of share buy-backs in the intrinsic value’s calculation.

I need to remind you that Apple stock should be seen as a long-term investment as Tim Cook clearly emphasized in the last TIME100 summit based on New York in June 2022, Tim Cook said:

If you are a short term trader, do not invest in Apple stock. Because if you are doing that, you are trading at a different time horizon than we’re investing in. We invest for the long term. Doing good is creating shareholder value in the long term; it may not in the very short term. Our interests are not aligned to the short term trader.

Context

Apple is facing some problems in one of the main Foxconn’s facilities which is the world’s largest iPhone factory located in Zhengzhou, China, due to the zero-COVID policy implemented in the country. This could affect the expectations of the analysts for the last quarter in 2022. However, the problem is not in the demand but in the supply as mentioned in the Apple’s web site in November 2022:

COVID restrictions have temporarily impacted the primary iPhone 14 Pro and iPhone 14 Pro max assembly facility located Zhengzhou, China. The facility is currently operating at significantly reduced capacity. As we have done throughout the COVID-19 pandemic, we are prioritizing the health and safety of the workers in our supply chain.

We continue to see strong demand for iPhone 14 Pro and iPhone 14 Pro Max models. However, we now expect lower iPhone 14 Pro and iPhone 14 Pro Max shipments than we previously anticipated and customers will experience longer wait times to receive their new products.

Furthermore, there are recent worrisome news about the protests in the Zhengzhou’s facilities with all the new recruited workers. However, Tim Cook has a strong specialization in supply chain management; in fact, that was one of the main reasons why Steve Jobs believed that there was anyone better than Tim Cook as his successor.

Therefore, we don’t have to be worried about the short-term issues mentioned on the news particularly if we are focused on a long-term horizon. In my opinion, a key factor is that Tim Cook has developed a long-term strategy in the company focused on delivering more value for long-term investors, which is reflected by the Apple stock’s capital appreciation of more than 600% in the last 10 years.

Given our focus on the long-term, I propose to calculate an intrinsic value considering the strong business model and the outstanding management; these two factors are key to make decent projections of the future FCFs to calculate Apple’s intrinsic value. Let’s see why this stock is at a fair price.

First stage: standard intrinsic value

In this part, I will show you that this is the typical way of calculation of the intrinsic value in several analysis using the DCF, considering a conservative growth in revenues and FCF of the company for the next years.

These are my assumptions for this stage:

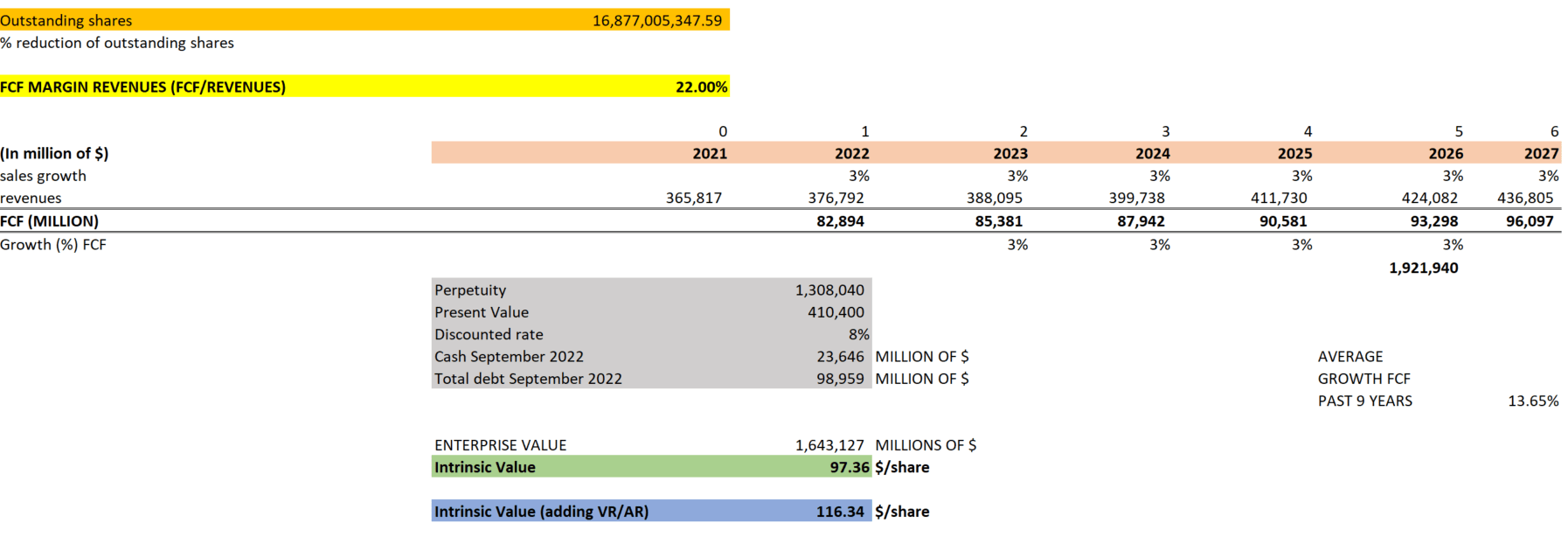

- Outstanding shares from 2021: 16,877,005,347

- FCF margins based on the last 10 years average: 22%

- Revenue growth of 3% for the next 6 years

- Total debt and cash on hand in the balance sheet as of September 2022

- Enterprise value is the subtraction of the total debt from the present value of the all the future FCF projected adding the cash on hand from the balance sheet.

- Growth in FCF perpetuity (FCFP): 3%

- Discounted rate: 8%

Prepared by the author

The estimations are conservative; for example, the growth of FCF has been 13.65% compound annual growth rate (CAGR) in the last 10 years while I am assuming 3% for my projections. The revenue growth expected from the consensus is 3% for 2023, 5.5% for 2024, and 5.1% for 2025; my estimations are 3% of revenue growth for all the years projected.

The intrinsic value according to this stage of calculation is $97.36 per share which is similar to the number that some bearish analysts are getting in their calculations.

Second stage: including VR/AR products

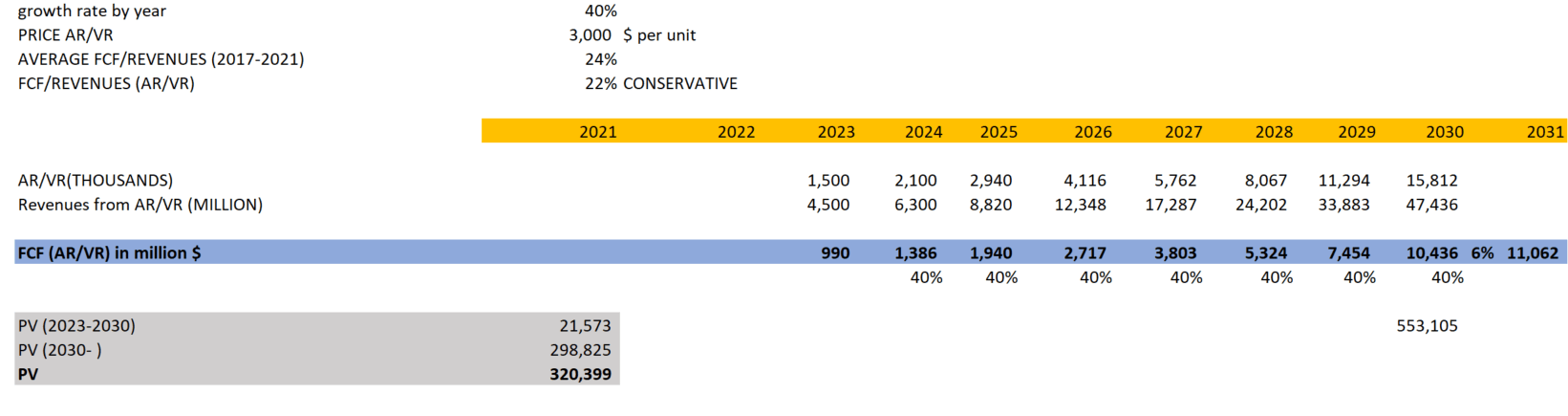

According to Ming-Chi Kuo, one of the most reliable analysts about Apple, the AR/VR products might be launched in 2023. The goal is to estimate FCF projections for the AR/VR products using the next assumptions:

- AR/VR products will be launched in 2023

- The number of units sold estimated in 2023 would be 1,500

- Price estimated per unit is $3,000 per unit

- Growth of sales: 40% annual, according to GlobalData Forecasts, it is expected to reach $30 billion in sales in 2030, which means a 40% CAGR roughly since 2023

- FCF margins (FCF/Revenues) generated by the AR/VR products: 22% which are aligned with FCF margins of the entire company.

- Growth of FCFP: 6% annual.

- Discounted rate: 8%

Prepared by the author

The present value (PV) of the future FCFs obtained under these assumptions is $320,399 million. This number will be summed up to the enterprise value previously calculated in the first stage. In this sense, we are keeping all the assumptions made in the first stage; therefore, our new intrinsic value including the AR/VR products forecast is 116.34$ per share:

Prepared by the author

Third stage: including the share buyback’s effect

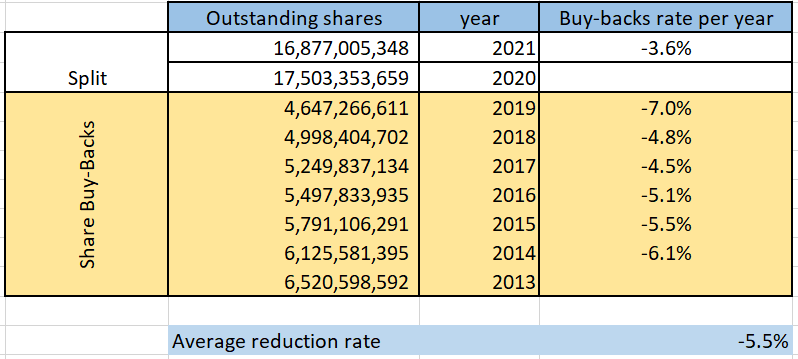

In this stage, we need to know what was the rate at which Apple makes its share buy-backs, so reviewing its past history in the last 9 years, we have the following:

Prepared by the author, Apple’s Annual report

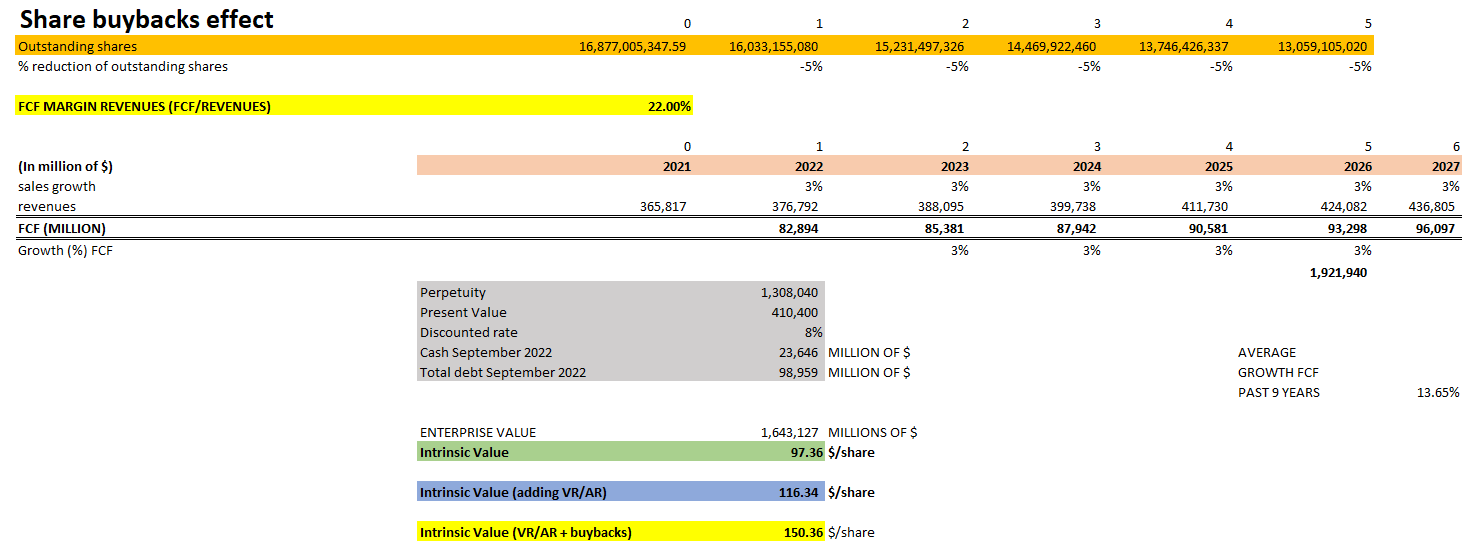

We consider the share buy-backs from 2013 to 2019 since there was a 4-to-1 split in 2020. Taking the average rate, Apple repurchases 5.5% of the outstanding shares of the previous year. Now, we will apply 5% for the next years projected to the year 2026:

Prepared by the author

In this stage, we take the enterprise value and divide it by the outstanding number of shares projected for the year 2026. Of course, Apple might keep reducing its number of outstanding shares beyond 2026, driving up even more the intrinsic value but we want to be conservative in our assumptions; thus, according to this model, the number of outstanding shares for 2027 onwards will be the same as 2026.

The final intrinsic value including the projections of the AR/VR products and the share buy-back’s effect is 150$ per share which is the average price at which Apple stock was trading in the last months.

Challenges to the thesis

Some of the assumptions that we’ve made might be broken, so that the intrinsic value could be lower than that we are expecting. For instance, if the annual rate of buy-backs falls from 5% to 3% keeping the other factors unchanged, the intrinsic value would drop from $150 to $135 per share. We don’t know if Apple will keep the same rate or not, so I would consider a range between $135$ to $150 per share as the intrinsic value.

A second factor would be a scenario in which the AR/VR products are not launched in 2023 delaying the propel to an unknown date. In that case, our intrinsic value would only incorporate the buy-backs and the projection of the current products for the next years. In this scenario, the Apple’s intrinsic value would be around 125.82$ per share. Nevertheless, it is hard to imagine that Tim Cook would delay the launch of the AR/VR products since he said in September 2022:

Not too long from today, people will wonder how they led a life without augmented reality, stressing the “profound” impact it will have on the not so distant future.

This combined by the expectations of analyst Ming-Chi Kuo, strengthen the possibility of that important event for Apple in 2023 with a high probability.

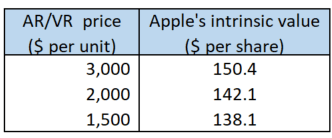

A third factor that could weak our thesis is related to the average price of the AR/VR products. The average price per unit for these products assumed in our calculation was $3,000. If the price was lower than expected keeping the other factors unchanged, the intrinsic value will be impacted:

Prepared by the author

However, I cannot imagine a scenario in which the price per unit reaches $1,500 since we know that the segment targeted for Apple’s products is the wealthier segment of the market; this is another reason why Apple has an strong pricing power since its products are well-demanded and its customers have high buying power.

Another factor that could affect the valuation is the more restrictive monetary policy by the Fed in the next years. More interest rate hikes to control the inflation rates in the economy could affect the demand for Apple’s products and services, so the revenue growth might be impacted. Nonetheless, the Apple’s business model is very resilient since the main target of the company is the wealthier segment of the market. Most likely, the problem continues being the supply instead of the demand for Apple’s products, and the launch of the new AR/VR products could be another interesting catalyzer to deliver more revenue growth, so I feel comfortable with the 3% of revenue growth for the next years.

Finally, we are considering that the risk frequently mentioned on the news about the possibility that China could invade Taiwan is no significant. In Taiwan, Taiwan Semiconductors Manufacturing Company (TSM) is a critical Apple’s provider of the 3nm-chips. However, there would be several negative implications for China, like beginning a war with the US, or the possibility that Taiwan or the US destroy all TSM’s assets, making the invasion a failure. Apparently, Warren Buffett is also assigning a low probability for such event since he has recently invested in TSM.

In a nutshell, taking all these scenarios, we could establish a range for the Apple’s intrinsic value between 135$ and 150$ per share. The stock price has been moving around that range in the last months, so it is likely that the market is considering the launch of the AR/VR products and the share buy-back’s effect. Apparently, the market is not considering the Apple car as part of the valuation of the company either.

Strategy with Apple stock

Apple stock is a hold for those investors who have invested in the company several years ago. A new investor who is thinking of buying Apple stock could consider that the current price ranging between $130 and $150 per share is the fair price. I would start a position when the price is between $130 and $140 per share, increasing my position gradually if the stock falls below that range.

Given the uncertainty related to the monetary policy from the FED, the war between Ukraine and Russia, the zero-COVID policy in China, a recession in 2023, and so on, the stock might drop below the range of the intrinsic value previously mentioned giving an opportunity to new investors. Being aware of which is Apple’s fair value will enable us to know if we should start a position or not right now. If we consider the stock to be expensive, we would have the incentives to wait for a significant fall in the stock price that may never come since we are not making a proper calculation of the intrinsic value of the company.

Final Thoughts

Some analysts state that Apple stock is overvalued using multiples, comparing them with other competitors, and encouraging investors to wait for a significant decline in Apple stock, a fall that may not come. We need to be aware of the limitations of only using multiples like P/E, EV/Sales, EV/EBITDA, EV/EBIT, etc. since these multiples assume almost the same quality among all the comparables without considering factors that are only intrinsic to each company.

In addition, most of these analyses do not include neither the launch of the AR/VR products in 2023 and most importantly, nor the share buy-back’s effect which is a regular practice of the Apple’s management in the last 10 years to deliver more value to long-term investors.

A critical factor behind all the assumptions we’ve made in this article is the management’s capabilities to deliver the highest value to the shareholders; Tim Cook has done an amazing job in all these years, strengthening Apple’s market position, the innovative culture inside the company, the brand’s reputation, the efficiency in the supply chain management and the capital allocation.

Apple is a compounder since it is able to reinvest its cash flows at high returns; this combined with its strong buybacks year by year ends up boosting the intrinsic value. So most likely the current intrinsic value ranging between $130 and $150 per share would be higher in the next years as the company keeps delivering more value to its clients and investors.

Thanks to a solid and consistent long-term strategy, we feel confident making projections for Apple’s future performance, getting an approximation of Apple’s intrinsic value ranging between $135 and $150 per share. Therefore, there could be an interesting opportunity to buy Apple stock when the price drops below that range.

Be the first to comment