Dragos Condrea/iStock via Getty Images

A Quick Take On AppFolio

AppFolio, Inc. (NASDAQ:APPF) reported its Q4 2022 financial results on January 26, 2022, beating revenue and EPS estimates.

The company provides property and investment management software to the real estate industry.

Given the firm’s high and increasing operating losses in a higher cost-of-capital market environment, until management can make meaningful progress toward operating breakeven, I’m on Hold for APPF.

AppFolio Overview

Santa Barbara, California-based AppFolio, Inc. was founded in 2006 to provide a range of software capabilities to real estate owners, managers and investors.

Its products offer tools for tracking rental income, tenant screening, online rent payment processing, maintenance requests, communication with tenants, and more. AppFolio also provides a suite of marketing and advertising services to assist property managers in marketing their properties.

The firm is headed by Chief Executive Officer Jason Randall, who was previously Sr. Director, Product Management at Citrix Systems and Director, Product Development at SupplySolution.

The company’s primary offerings include:

-

Real Estate Property Management

-

Real Estate Investment Management.

The firm acquires customers via its direct sales and marketing efforts as well as through partner referrals.

AppFolio has over 17,800 customers of all sizes, managing over 6.8 million units worldwide.

AppFolio’s Market & Competition

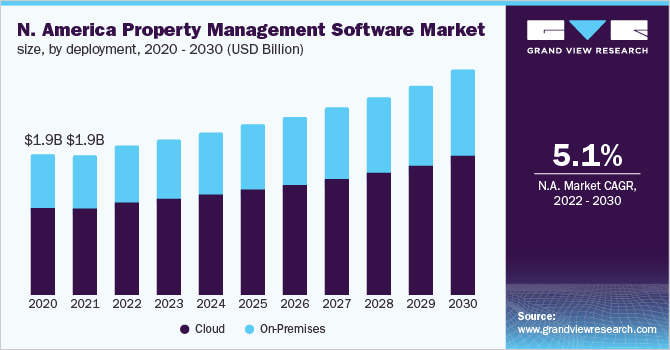

According to a 2022 market research report by Grand View Research, the market for real estate property management software was around $3 billion in 2021 and is forecast to reach $4.9 billion by 2030.

This represents a forecast CAGR of 5.6% from 2022 to 2030.

The main drivers for this expected growth are a changing real estate landscape and increasing demand from buyers for more advanced and integrated offerings that increase business efficiencies across the organization.

Also, below is a chart showing the historical and projected future growth trajectory of the North American property management software market:

N. America Property Management Software Market (Grand View Research)

Major competitive or other industry participants include:

-

CoreLogic

-

Console Australia Pty. Ltd.

-

Entrata

-

InnQuest Software

-

IQware

-

MRI Software

-

RealPage

-

REI Master

-

Yardi Systems.

APPF’s Recent Financial Performance

-

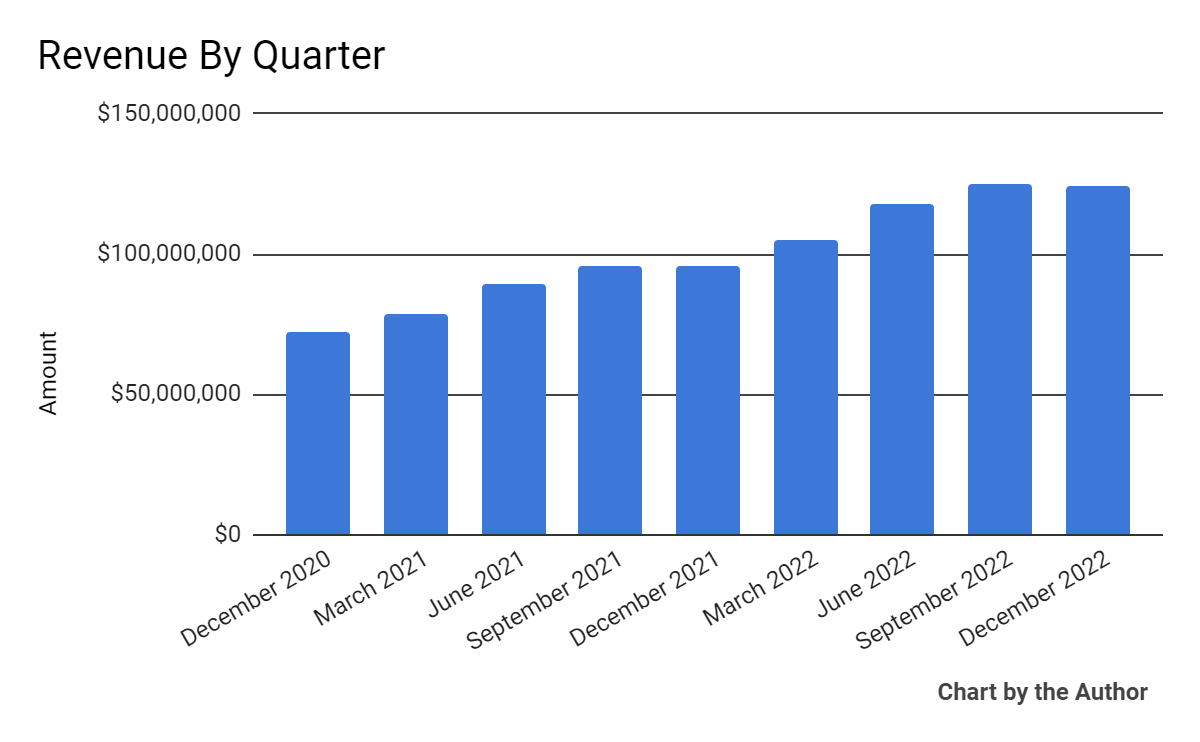

Total revenue by quarter has risen per the following chart:

Total Revenue (Seeking Alpha)

-

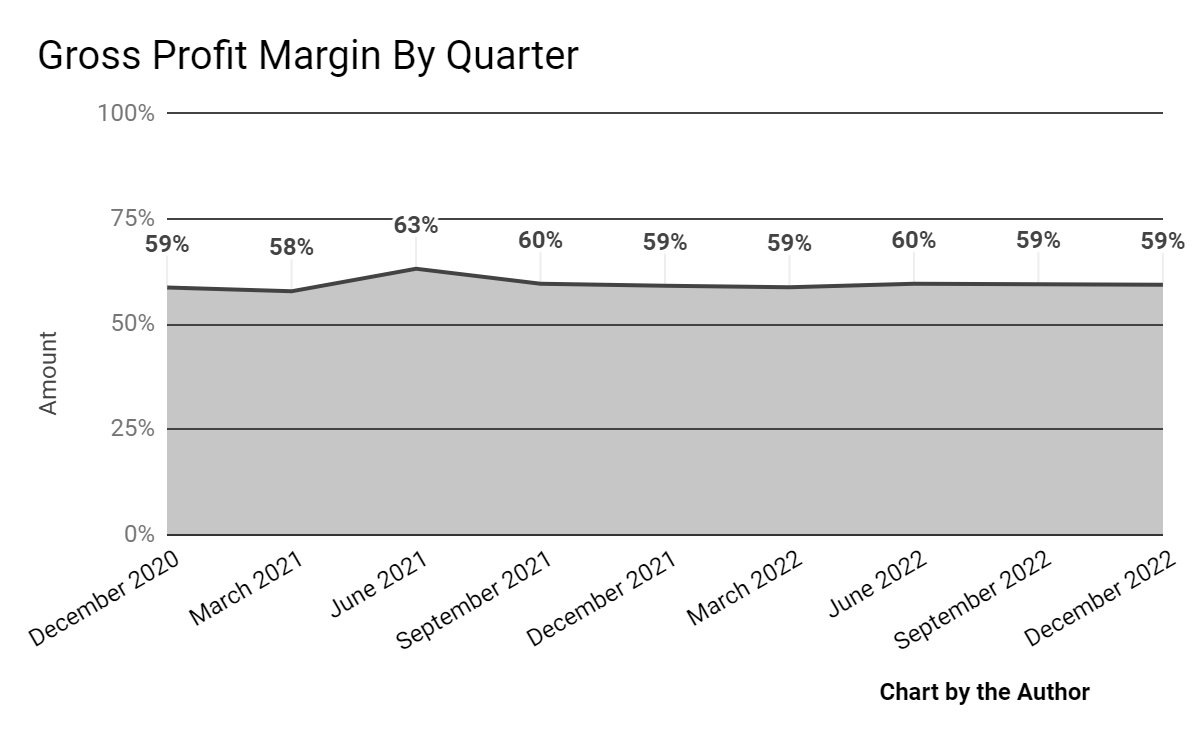

Gross profit margin by quarter has remained largely flat, as shown below:

Gross Profit Margin (Seeking Alpha)

-

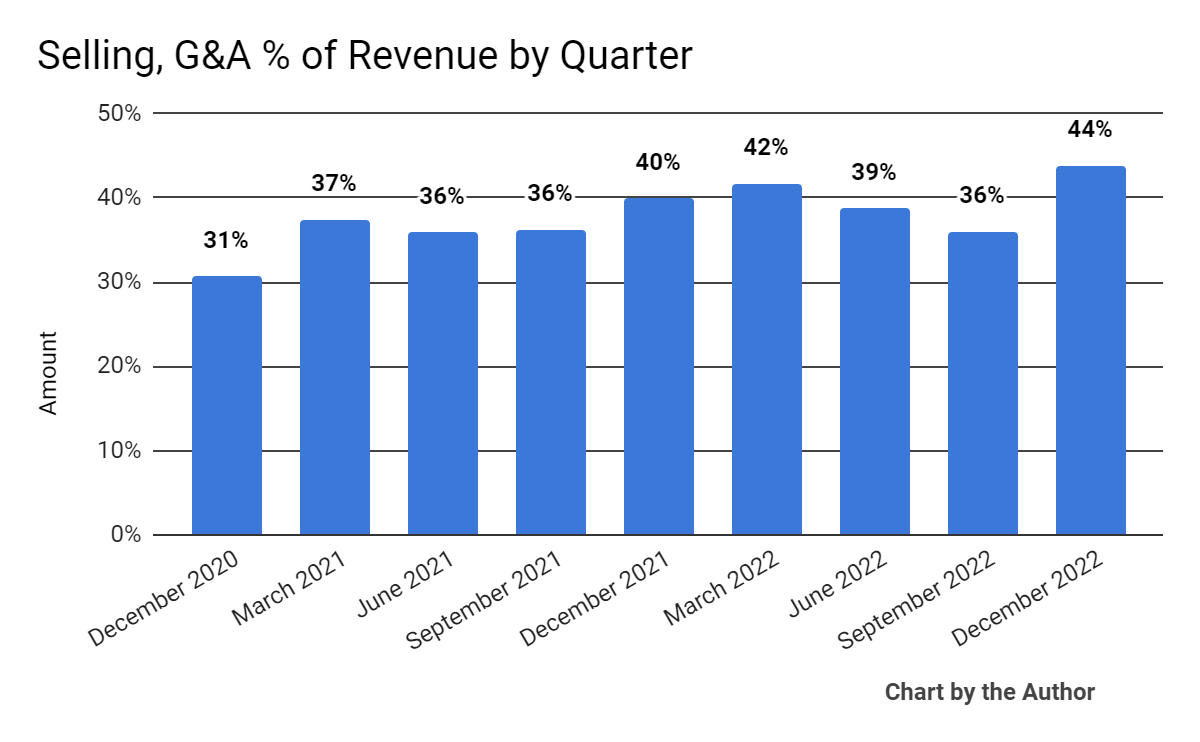

Selling, G&A expenses as a percentage of total revenue by quarter rose in calendar Q4 2022:

Selling, G&A % Of Revenue (Seeking Alpha)

-

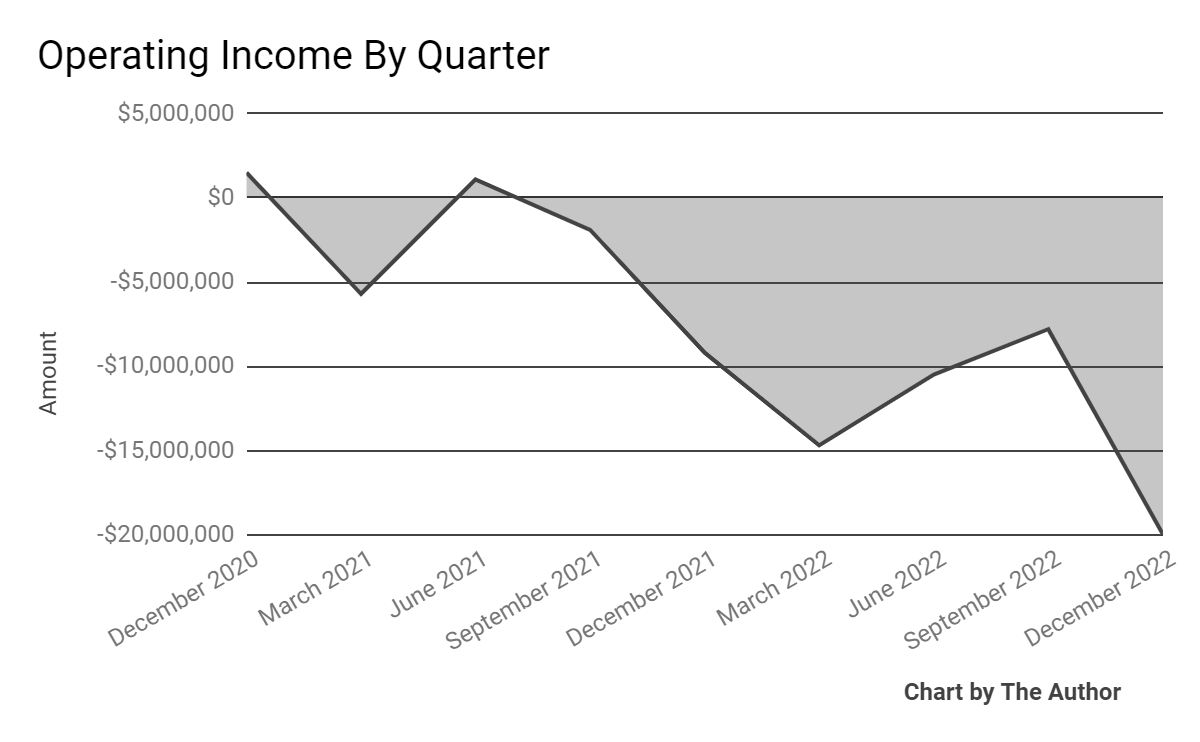

Operating income by quarter has worsened further into negative territory:

Operating Income (Seeking Alpha)

-

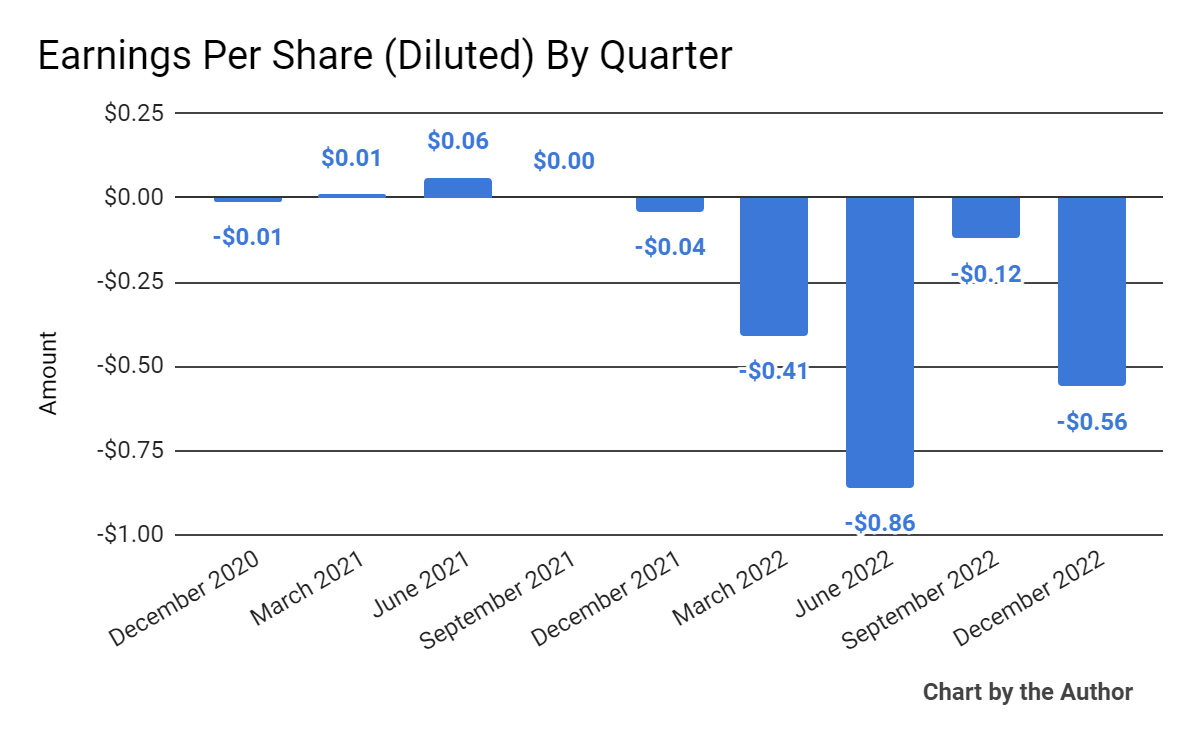

Earnings per share (Diluted) have also produced deteriorating results, as shown below:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP.)

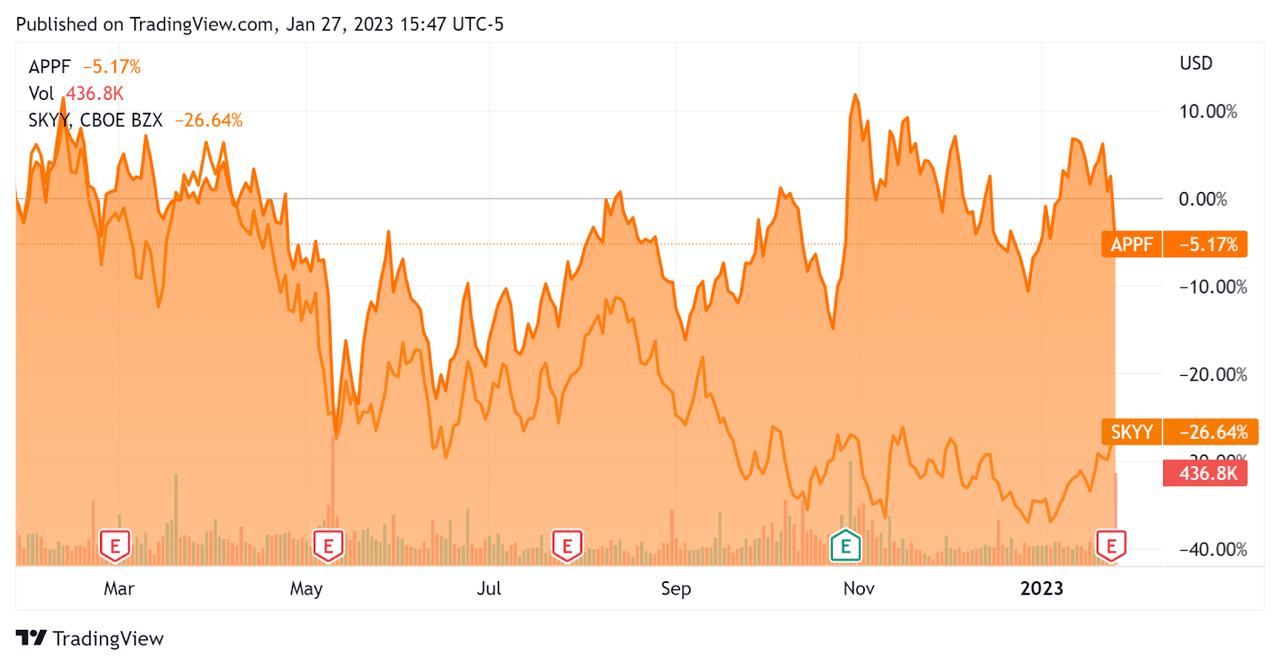

In the past 12 months, APPF’s stock price has fallen 5.2% vs. the First Trust Cloud Computing Index (SKYY) ETF’s drop of around 26.6%, as the chart below indicates:

52-week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For AppFolio

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

8.9 |

|

Revenue Growth Rate |

31.9% |

|

Net Income Margin |

-11.2% |

|

GAAP EBITDA % |

-7.4% |

|

Market Capitalization |

$4,041,420,030 |

|

Enterprise Value |

$3,931,590,910 |

|

Operating Cash Flow |

$28,216,000 |

|

Earnings Per Share (Fully Diluted) |

-$1.95 |

(Source – Seeking Alpha.)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

APPF’s most recent GAAP Rule of 40 calculation was 24.5% as of Q4 2022, so the firm needs improvement in this regard, per the table below:

|

Rule of 40 – GAAP |

Calculation |

|

Recent Rev. Growth % |

31.9% |

|

GAAP EBITDA % |

-7.4% |

|

Total |

24.5% |

(Source – Seeking Alpha.)

Commentary On AppFolio

In its last earnings call (Source – Seeking Alpha), covering Q4 2022’s results, management highlighted the firm’s “resilience in the changing real estate industry in evolving macroeconomic environment.”

Leadership said the company has been “moderating and will continue to moderate” its headcount growth rate throughout 2023.

The company also plans to focus its R&D efforts around automation, centralization and adding flexibility to help customers improve efficiency and results.

As to its financial results, total revenue rose 30% year-over-year, while ARPU (Average Revenue Per Unit) increased and payments grew.

Management did not disclose any retention rate metrics, other than to characterize its retention as “high” without providing further details.

The firm’s Rule of 40 results have been disappointing, with a reasonably solid revenue growth result offset by a negative operating result contributing to a mediocre figure for this metric.

SG&A expenses as a percentage of revenue increased markedly during the final quarter of the year and operating losses worsened dramatically to the worst performance in nine quarters.

For the balance sheet, the firm ended the quarter with $160.1 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash flow was $18.9 million, of which capital expenditures accounted for $6.5 million. The company paid a hefty $43.2 million in stock-based compensation.

Looking ahead, management guided full-year 2023 total revenue to an expected growth rate of 21% over that of 2022.

Regarding valuation, the market is valuing APPF at an EV/Sales multiple of around 8.9x, which has risen slightly in the past few quarters.

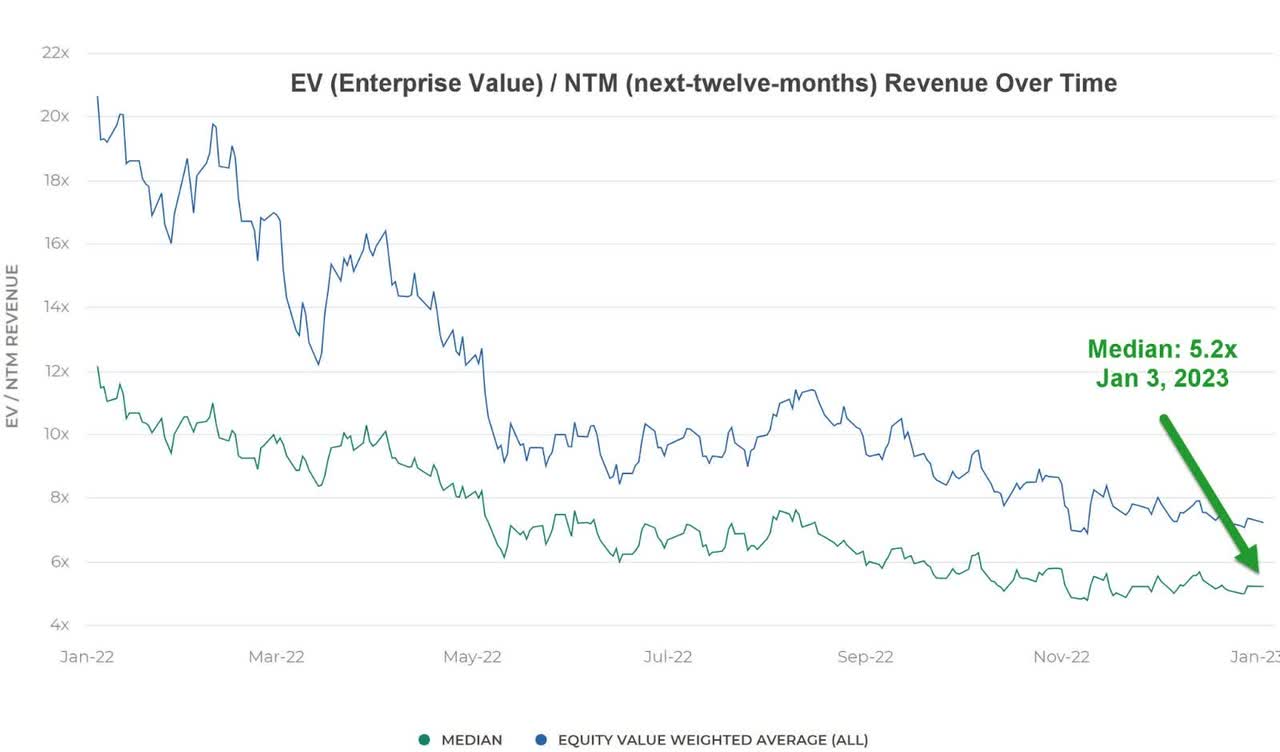

The Meritech Capital Index of publicly held Software as a Service “SaaS” software companies showed an average forward EV/Revenue multiple of around 5.2x on January 3, 2023, as the chart shows here:

Public Company EV/NTM Revenue Multiple (Meritech Capital Index)

So, by comparison, APPF is currently valued by the market at a significant premium to the broader Meritech Capital Index, at least as of January 3, 2023.

The primary risk to the company’s outlook is a macroeconomic slowdown, which may accelerate new customer discounting, produce slower sales cycles and reduce its revenue growth trajectory.

The market for multi-family is in flux now, with higher rents attracting developers while higher interest rates are making new projects harder to pencil.

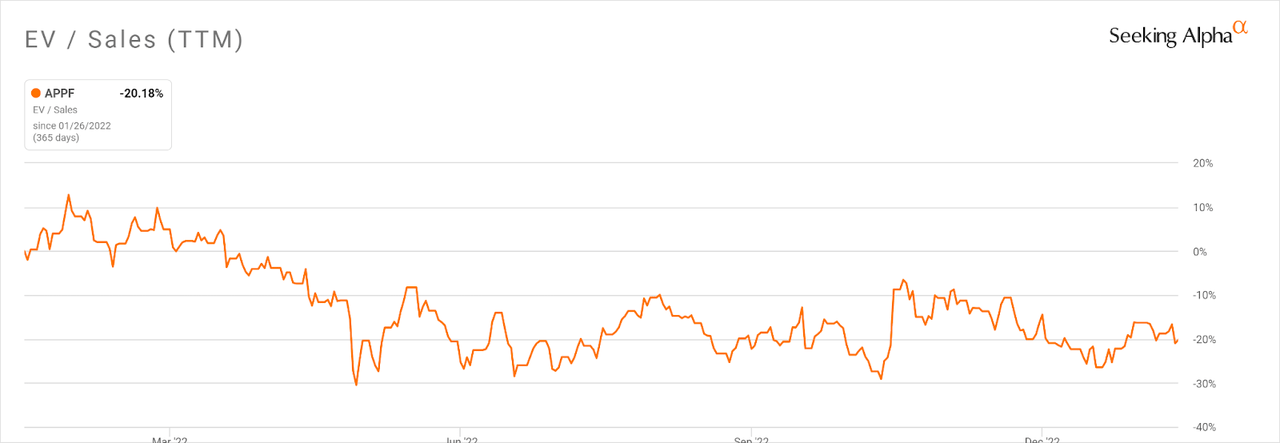

Notably, APPF’s EV/Sales multiple [TTM] has compressed by 20.2% in the past twelve months, as the Seeking Alpha chart shows here:

Enterprise Value / Sales Multiple History (Seeking Alpha)

A potential upside catalyst to the stock could include a ‘short and shallow’ downturn, boosting revenue growth higher than expected.

However, given the firm’s high and increasing operating losses in a higher cost-of-capital market environment, until management can make meaningful progress toward operating breakeven, I’m on Hold for AppFolio, Inc.

Be the first to comment