6381380/iStock Editorial via Getty Images

Antero Midstream Corporation (NYSE:AM) posted solid third-quarter results, both operationally and financially. Despite the company’s skimpy dividend coverage, we believe its unique business model ensures that its dividend is safe as long as its sponsor, Antero Resources Corporation (AR), develops its acreage at a pace that keeps production flat.

Unless Antero Resources steps up its pace of development, AM offers little by way of dividend growth. In light of the natural gas takeaway constraints in Appalachia, we see AM’s dividend increasing in line with inflation, though not much more over the next few years.

AM’s Third-Quarter Highlights

AM reported third-quarter Adjusted EBITDA results and throughput volumes that were in line with analyst consensus expectations. Gathering volumes were marginally higher from both the previous year and the previous quarter. The company’s fee rates increased by 3% to 5%, due primarily to the inflation escalators in AM’s contracts with its sponsor, Antero Resources, which accounts for nearly all of AM’s revenue.

HFI Research

Shareholders should be encouraged to see AM’s shift from incurring debt over the previous four quarters to paying down debt in the third quarter. The previous four quarters saw long-term debt increase by $67 million to $3.16 billion, while the third quarter saw debt repaid by $16 million. Management guided to a continued cash flow surplus after dividends, which it intends to allocate toward continued debt reduction. Its stated goal is to reduce AM’s leverage ratio from its current 3.6-times to 3.0-times by the end of 2024.

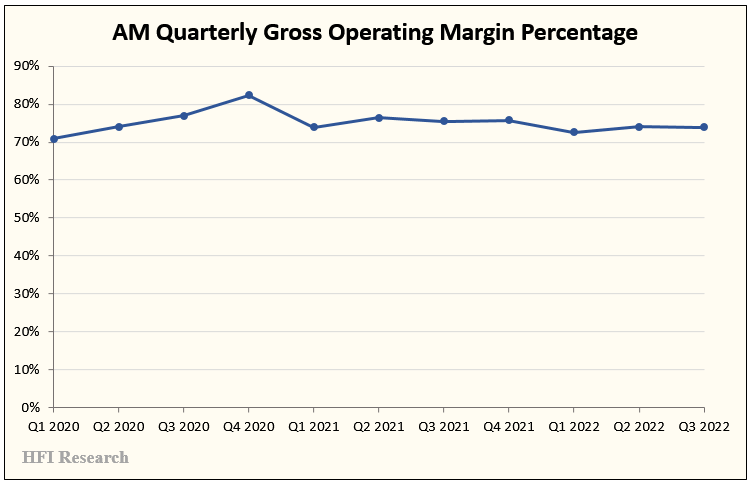

AM’s Stability Leads To High Returns On Capital

AM’s return on capital is among the best for gathering and processing companies. Its revenues are underpinned by long-term contracts that designate AM as the exclusive midstream operator on the acreage it services for Antero Resources. AM benefits from advanced knowledge of AR’s capital budget, so it can adjust its expense profile and capital planning in a way that sustains its gross operating margin in a very narrow range, as shown in the following chart.

HFI Research

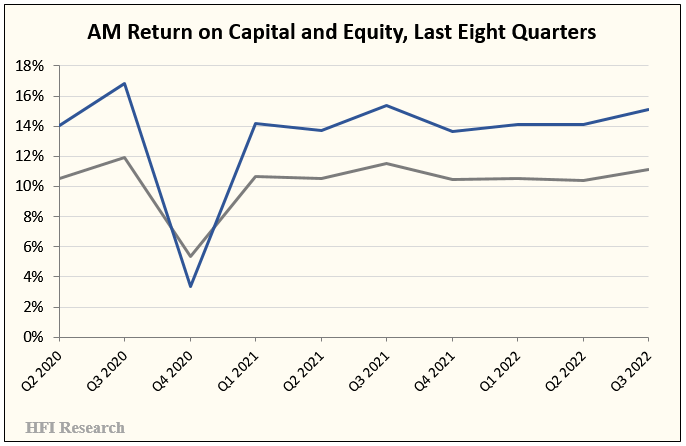

AM’s unique business model allows it to generate some of the highest returns on capital employed and returns on equity among midstream gathering and processing companies. Its returns are also remarkably stable.

HFI Research

In October, AM acquired the Appalachian assets of Crestwood Equity Partners (CEQP) at a bargain multiple of 6-times EBITDA. The deal was particularly attractive to AM because it includes 425 of Antero Resources’ undeveloped drilling locations. The locations add years to AM’s drilling inventory, which now stretches well into the 2040s. With AM as the operator, Antero Resources is more likely to develop them. The acquired assets will save AM $50 million in capex that it would have spent if it were to develop the acreage from scratch.

Neutral Outlook For AM Shares

AM’s management guided to a mid-single-digit percentage volume increase in 2023. We expect revenues to be up in the mid-single-digit percent for the year, roughly in line with inflation.

With little top-line growth, AM has to generate a cash flow surplus in order to create additional value for shareholders. Until the third quarter, it has not managed to do so, as shown in the table below.

HFI Research

We should point out that AM’s management claimed it generated $30 million of free cash flow after dividends, citing a 54% decrease in capital expenditures to $37 million. However, AM’s financial statements show third-quarter capital expenditures of $74 million.

According to AM’s GAAP figures, it operated at a cash flow deficit in the third quarter and paid down debt by using the cash generated from an asset sale and the reimbursement of previously made capital expenditures related to a sale of a natural gas processing plant.

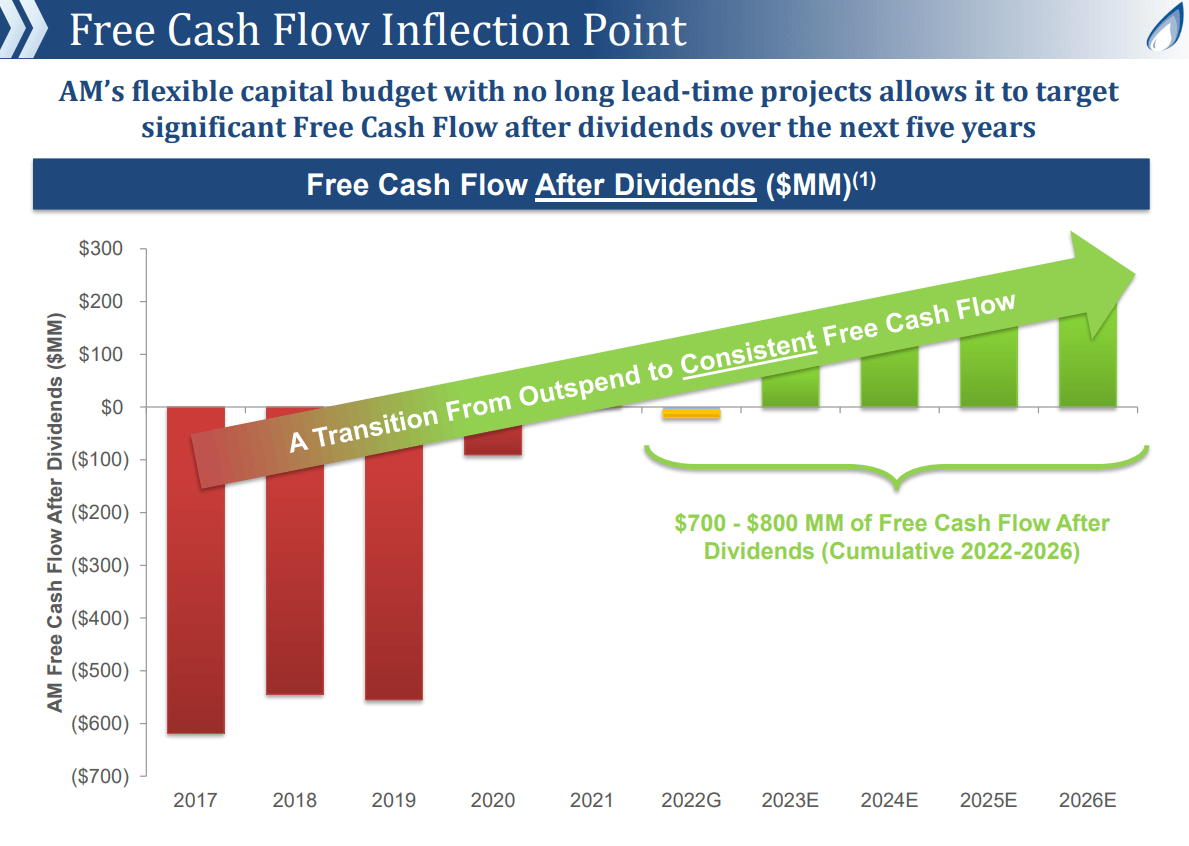

In AM’s third-quarter earnings conference call, management guided for an increasing cash flow surplus over the coming years, as shown in the following graphic from its third-quarter earnings slide presentation.

Antero Midstream

AM can generate a cash flow surplus if it reduces its capex, which is what management intends to do. Over the past four quarters, the company spent $312 million on capex. For 2023, it is budgeting $275 to $300 million. To the extent that its operating cash flow is equal to or greater than 2022 levels, the company should generate a cash flow surplus that management can use to pay down debt.

However, management’s goal of reducing AM’s leverage ratio to 3.0-times is a tall order. Assuming Adjusted EBITDA increases by 3.5% annually, AM would have to generate a cash flow surplus of $600 million over the next two years to achieve it. Unless the company manages to grow its top line at a greater rate than its mid-single-digit percentage guidance, the goal appears to be out of reach. We don’t expect stepped-up return of capital to shareholders until the 3.0-times leverage target is reached.

Valuation

Our EV/EBITDA valuation assumes AM’s Adjusted EBITDA and dividend grow by 3.5% per year through 2026. With no debt paydown or share repurchases, the shares have 11.8% upside. By 2026, the upside increases to 67.0%, due primarily to annual dividend payments.

HFI Research

AM’s trading multiple of 10 to 11 times EBITDA is high for a gathering and processing operator, but we believe it is justified due to the company’s consistently superior return on capital. Still, the elevated multiple carries downside risk if the company’s volumes fall. If its EV multiple were to fall to the industry average of eight to nine times EBITDA, its shares could decline by more than 20% if EBITDA is flat with 2022. Of course, a more significant EBITDA drop could be disastrous for the shares.

AM is exposed to various risks stemming from fundamentals. The foremost is a steep and protracted decline in natural gas prices, which could cause Antero Resources to ratchet back its development plans. Fewer well completions would of course be negative for AM. Look no further than AM’s MarkWest joint venture production results—which are shown in the Quarterly Operating Results table above—to see what happens to its acreage in the absence of capex.

Conclusion

We believe Antero Midstream Corporation is fairly valued. Current holders who are confident about Antero Resources’ production outlook can hold the shares and enjoy their above-average 8.3% yield. However, investors looking to commit new capital should avoid AM. They’re better off buying one of the many income-producing energy equities that offer more upside and less downside risk.

Be the first to comment