takasuu/iStock via Getty Images

The main goal of investing is to create long term wealth, and one of the best ways to do that is to find companies which pay a high dividend yield and reinvest that money and let it grow over a longer period of time.

There are many companies which offer high dividend yields and I’ve written about others like Icahn Enterprises (IEP) and some others. But one of my all time favorites has to be Annaly Capital (NYSE:NLY), which is a REIT, or Real Estate Investment Trust, which offers exposure to certain real estate markets.

The company has seen its share price dip recently, as it closely follows interest rates and the broader real estate market, which affects the valuation of the underlying real estate. This presents a good long term opportunity as they currently distribute a cash dividend which yields just over 15.6% annually, or 3.9% every quarter when it distributes the dividend payments.

The real question is – how sustainable is the dividend payment and yield moving forward? Let’s explore.

Prime Opportunity For Long-Term Value

Why I love dividend stocks so much, and why they are an outsized portion of my long term investment portfolio and retirement account, is that the value of the stock itself doesn’t have to appreciate in any meaningful way in order to create long term value for my future plans. (Note: See additional disclosure at end of article about portfolio structuring and investments)

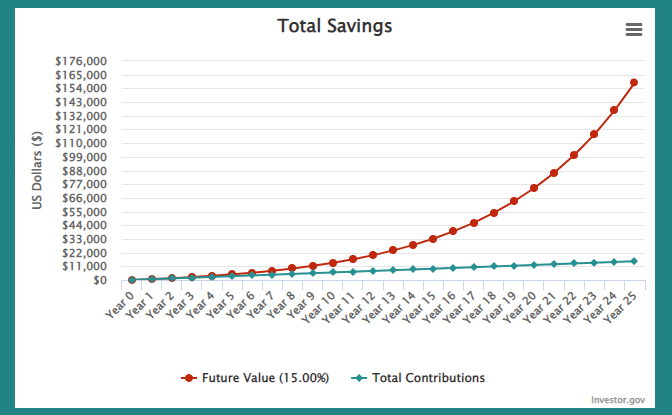

As long as Annaly Capital continues to pay around 15% in dividends each year, on average, the value it creates over the next 25 years is enormous. We can see this by plugging in the numbers to the US Government’s compound interest calculator, which it provides as an educational tool for all.

Investing $100 in Annaly Capital now, with an additional $50 each month for the next 25 years means you’d have contributed (invested) a total of $15,100 over the course of those 25 years, whereas the value of that position will be worth just over $158,000. That’s a total return of over 950%.

Compound Interest Calculator (Investor.gov)

Furthermore, this $50 per month investment can be multiplied however many times you’d like, depending on how much you can or want to invest each month. It is noteworthy that while I by no means endorse holding just 1 position in any account, increasing the monthly contribution to just under $350 every month will land you at over the coveted $1 million in value over the course of the same 25 years.

So, Can It Last?

Beyond the fact that the hardest part of this plan is actually having the discipline to maintain this position and not get enticed by the fast-growing, millionaire-maker of the day, there’s also a big question about whether the company can maintain this level of dividend payments in the long run.

As a percentage of their earnings, the company has been paying out a relatively low, yet somewhat volatile, amount of their interest income as its dividend, meaning it is sustainable, but that’s been taking place as interest rates have been at some of their highest levels in decades.

What happens once home values don’t rise as much or decline and interest rates fall? That’s the, literally, million dollar question. For now, I believe that it’s sustainable around current levels, even if the company does continue the trend of lowering their cash dividend payouts as share price fluctuates.

Even though the trend is that the company has been lowering their cash dividend payments over the past few years, the coinciding share price reduction and asset reshuffling has allowed the yield to become more and more attractive. As the company expects income per share to land at around the rate of their current dividend payout of $3.52 per share for the next 2 years, I don’t expect the dividend payout to change for the time being.

NLY Earnings Forecast (Seeking Alpha Aggregator)

Holding Strategy Can Be Tricky

While the easiest way to manage a high dividend company like Annaly Capital is to set up an automatic recurring monthly investment and dividend reinvestment (and again, see additional disclosure at the end of the article about opinion vs. recommendation), but with Annaly Capital, as well as some other dividend behemoths, I choose a slightly more active approach.

While I do have a monthly recurring investment in Annaly Capital, it’s not the entirety of my intended monthly investment and I leave some out which is intended for times when the company’s share price dips below a certain price point where the yield then exceeds 15%, or higher. What this allows me to do is take advantage of the share price dipping and allows me to incrementally increase the average yield over the long run, especially if the company lowers its dividend payout to meet the lower interest income from lower interest rates down the line.

Even with a slightly more active investing strategy, there are several risks which need to be taken into account here, especially if you’re like me and have a focus on high-yield companies which can make up a larger-than-usual portion of an investment portfolio.

Eggs In Basket, Inc

Even though there are several companies with yields around the 15% mark, they’re not as diversified, as any investment advisor would tell you is worth placing your eggs in to. Given that a sizable amount of the high-yield companies are in the real-estate sector, the sensitivity to long and short term interest rates can become dangerous.

As a result, the main risk becomes the company’s inability to maintain such a high yield. This doesn’t only mean that your annualized returns are hurt. These types of companies don’t have much appeal to investors beyond the payouts, meaning that if the company’s payout yield decreases by a significant amount, we’re likely to see large outflows in a short time period.

Beyond the main risk of dividend sustainability, high yielding stocks tend to grow into significant portions of one’s portfolio given that the returns are likely to outpace other companies and investments. As a result, you may find yourself with a larger-than-ideal portion of your investment portfolio tied to real estate and a smaller number of companies as a result.

This means that you are likely to face one of two scenarios down the line:

1. In your retirement account, an interest rate lull or housing market correction can happen in normal economic cycles, which aren’t linked to overall recessions. This means that, potentially, it won’t need to be an overall recession for the value of these companies to decline. As a result, your retirement plans can be put on hold or set back for several years.

While this is a serious risk, it’s not much different than any other retirement plans, which can face a market correction or even a bear market ahead of planned retirement, which can set your retirement goals back.

2. In a regular investment account, you may be forced to sell off a portion of your position if it or they get too large, in order to avoid the risks of short term interest rate cycles causing the value of your account to materially decline.

This means that you will incur taxes and in some cases penalties for selling early and can move back your retirement goals if you weren’t able to invest a larger sum of money into the other parts of your portfolio.

Conclusion – Grade A Pick For 2023

With a steady yield of over 15%, which I believe is sustainable at current levels at least for the coming decade, even as lower cash dividend amounts and lower share price may occur, Annaly Capital represents a superb long term compounding interest opportunity.

I am bullish on the company’s long term prospects and will continue to add to my position throughout the coming years and will hold some cash specifically earmarked for if the company’s share price dips and allows for a lower price point, which will increase the dividend yield.

Famously, at least on investment forums, the company’s share price dip a few months back allowed me to buy shares at a yield of around or even over 20%, which is going to be a good cushion for if or when the company lowers their dividend amounts if interest income declines.

Be the first to comment