Wirestock/iStock Editorial via Getty Images

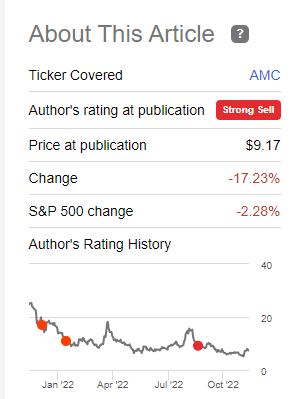

When we last covered AMC Entertainment Holdings, Inc. (NYSE:AMC) and its preferred shares (APE), we stamped another “Strong Sell” rating on the two stocks. Our logic was not focused on any of the conspiracy theories floating around in this company. It was based on sound albeit generous, valuation measures that suggested that a 90% downside would be pretty standard. Specifically, we said,

AMC still sports a $4.95 billion market capitalization and APE sports another $3.0 billion. That combined is at least $7.5 billion more than in it needs to be. Ahead of that is more than $5.4 billion of debt (ignoring operating lease liabilities). AMC’s peak, pre-COVID-19 EBITDA was $1 billion.

It’s hard to value this at even 6X EV to peak EBITDA let alone the implied 15X multiple today. Short interest is not too high, all things considered and we think both the AMC and APE shares are a “Strong Sell,” although we could see the logic in a Long APE, Short AMC trade.

Source: Oh When The ‘Apes’ Go Marching In

AMC has held up well relative to our expectations.

Returns Since Last Article-Seeking Alpha

With Q3-2022 results out, we decided to see if the company offered any hope to the long-suffering bulls.

Q3-2022

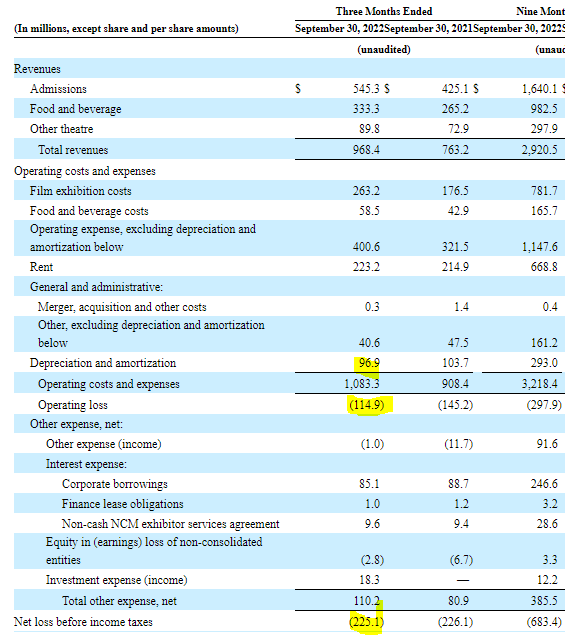

AMC delivered yet another massive operating loss of almost $115 million. Total losses reached $225 million. Even backing out depreciation from the equation offered very little hope to the bulls.

AMC Q3-2022 10-Q

We would note that these numbers came in a quarter with rather strong ticket sales and total revenues. Total sales were up 26% year over year from Q3-2021. Despite operating costs only moving up 19%, AMC still dug itself a large hole. The theatre business is a poor margin business during the best of times. Rent and film exhibition costs take away any possibility of making a decent profit. You can see above that the two categories mentioned eat up almost 90% of the admission revenues.

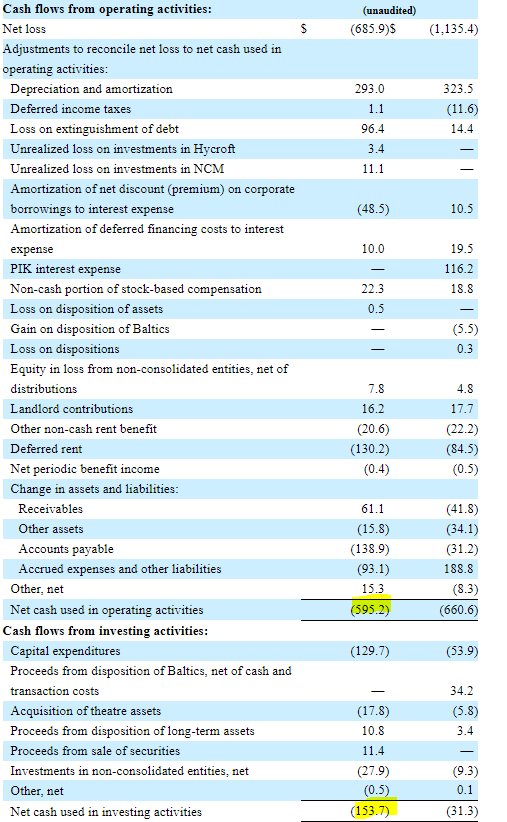

The income statement is always the warm-up to the main event and that main event is the cash flow statement. While total losses were close to $700 million for the year to date, the cash flow statement actually looked worse. The first three quarters showed a $750 million in total cash burn from operating activities and from capex.

AMC Q3-2022 10-Q

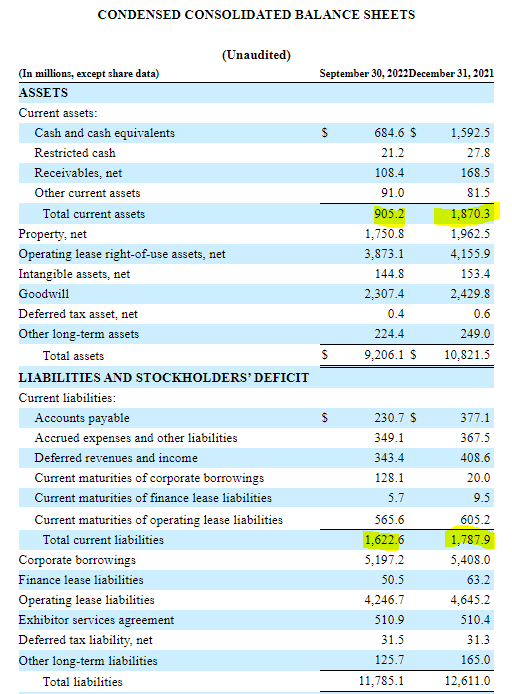

Most companies cannot sustain such massive burn rates and AMC is no different. For the first 9 months of 2022, the cash burn worked to systematically demolish the company’s current asset buffers. Current assets dropped from a chunky $1.87 billion on December 31, 2021, down to $0.9 billion at the end of the third quarter.

AMC Q3-2022 10-Q

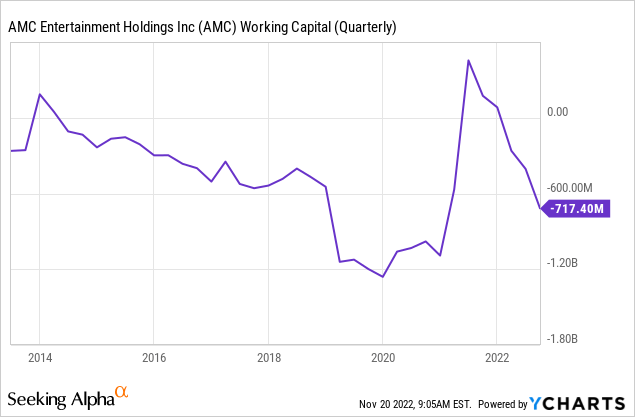

The size of AMC’s problem is also well visualized by seeing its working capital setup. Current liabilities now exceed current assets by $700 million.

The lowest this number ever got was near a negative $1.2 billion and we might add that happened during extremely loose monetary conditions. All other things being equal, we should go sailing past the $1.2 billion mark in the next 3 reported quarters.

Bonds Not Buying The Rescue

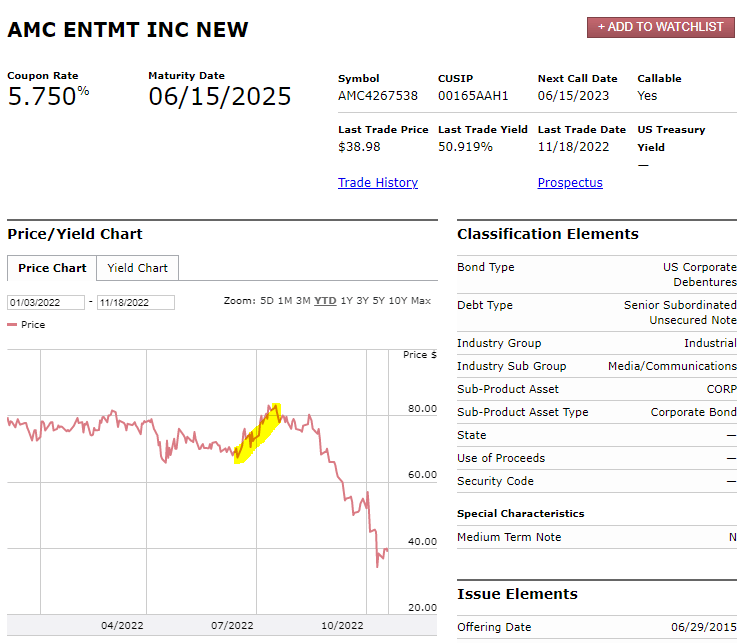

One potential savior for the company has always been dilution. It was the same dilution that allowed this saga to continue for so long and suckered in so many additional bulls. The recently released preferred APE units have unfortunately not worked as the company might have hoped. Their setup was as a backdoor dilutive unit, but they have stayed detached from AMC’s shares. When their listing was first announced, bonds showed a measure of hope.

FINRA Nov 20, 2022

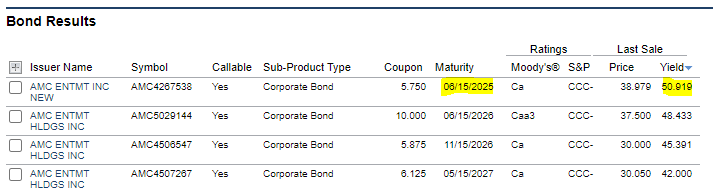

Unfortunately, as it became increasingly clear that that form of dilution would also be heresy to the AMC bulls, bonds began to lose hope. Currently the nearby bonds have yields between 42.00% and 50.9%.

FINRA Nov 20, 2022

The bond prices have dropped by about 50% since our last article while the common stock is just down 17%. We actually think even these bond prices are optimistic as there should be zero recovery beyond the secured debt, which these bonds are not.

Outlook & Verdict

Every dance to zero has a few steps that go in the opposite direction. This one will be no different. Unfortunately with dilution out of the question at present, AMC’s timeline appears in little doubt. We think a filing by Q4-2023 is now virtually certain. We base that on another potential $1.0-$1.2 billion of cash burn by then versus $900 million in current assets. Any short squeezes should be used to exit long positions as we approach the final chapter in this saga. On a scale of 1 to 10, this should be an 11.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment