HJBC

Is it the right time to sell Amazon.com (NASDAQ:AMZN)? I don’t believe so as the company is not in existential threat but is rather adjusting itself for its previous excesses. As cliché as it sounds, buying when there is blood on the street has served many well in the past. But the key question is, are you buying a company in death spiral? I don’t think Amazon fits in this category either. Amazon has always been what I call a “Funnel” company, constantly funneling profits from one business unit to find the next funnel that funds the next unit and so on. There will be no Amazon Web Services (“AWS”) today if not for the days of “wasting” the profits from e-commerce. Similarly, Amazon has almost quietly built itself to be the third biggest digital advertising platform. Building these enormously profitable business units cannot happen without an open mindset to try various avenues. This may backfire in the short-term, especially under trying market and economic conditions like the present but is key to not be cannibalized by others.

As I’ve mentioned in a few of my articles, one of the nicest things about writing on Seeking Alpha is the freedom to express your opinion, even if it means disagreeing with your fellow contributors. After all, varied opinions and beliefs form the basis upon which the stock market functions. For every buyer there is a seller and vice versa. If you guessed already that this is rebuttal article, you got it. This Seeking Alpha article on Amazon caught my attention over the weekend. The author calls for selling Amazon here and has listed a few reasons. While the article has some good points, I don’t agree with quite a few. In fact, the author, with a sell rating, seemed more favorable towards Amazon than those with buy ratings.

I present this article to offer a different view point to each of the concerns raised in the original article and also three ways to potentially play this sell off if you are a believer of Amazon in the long-term. Let us get into the details.

1. Cost Cuts May Signal A Turnaround

That Amazon is cutting cost and reorganizing workforce is actually a bullish sign. I wrote this article a couple of months ago that Meta Platforms, Inc. (META) announcing a sizeable layoff likely signaled its bottom and since then, Meta has gone up 35% compared to the market’s 2.32% increase. I am not claiming victory here but the point is rather than when profitable companies start layoffs, it is usually a sign that they have thrown in the towel, in a good way. To layoff and publicly announce the same hurts their ego, make no mistake about it but it at least means they admit their mistakes in hindsight and are much more likelier to proceed with caution in the near future.

As quoted in this article, a layoffs could signal either a push towards greater efficiency or a dire need for cash. Amazon, after having more than doubled its workforce between 12/31/2019 and 12/31/2021, is in the first category firmly. The change of direction is a response to its own overexpansion at the height of the pandemic.

“If a company lays off staff, the move could signal a change in direction towards greater efficiency. On the other hand, it might be the case that the company is going through some financial troubles and is laying off employees to shore up cash.“

2. Recession and Inflation

Being a contrarian in nature and investing, I believe things happen when least expected. When everyone calls for a crash, the market typically rallies. When everyone is too bullish (hello 2021), we get a 2022. In the same vein, almost everyone is expecting a recession and hence I believe we will not get one when expected. Coming to inflation, almost all the official metrics are lagging indicators. As an example, it took a while for the official PPI and CPI numbers to show the real heat the consumers were facing months earlier. The Fed reacted too late and the market didn’t react kindly. The reverse is likely to be true on the upside. Although the official numbers are coming down already, the lagging nature of these metrics could mean that the actual inflation is cooling down faster than what the numbers convey right now. When the market realizes it, watch out for the upside.

And with the announced layoffs and a better scrutiny of unprofitable business units, Amazon’s margin should improve to offset any fall in retail demand especially.

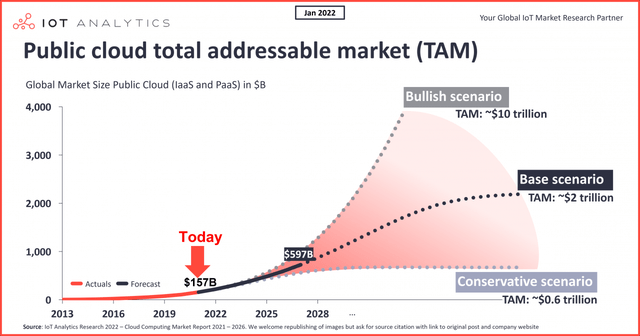

AWS – Still Scratching The Surface?

While I don’t deny that AWS will face more competitive and margin pressure in the short-term, the fact that the current cloud market represents just about 1/4th of the total bear-case total addressable market shows that over the long-term, AWS will continue its dominance. This concern in the original article is focused on the short-term (for traders) and not for long-term investors. The long-term AWS story remains intact with plenty of growth potential.

Cloud TAM (iot-analytics.com)

Valuation

This was the most compelling and hard to argue against section of the original article. Amazon is still overvalued by almost any fundamental metric. And just because it has always possessed a bloated PE (investment expenses or not), it doesn’t justify carrying a high PE in this environment.

However, I will present a few reasons to counteract this section:

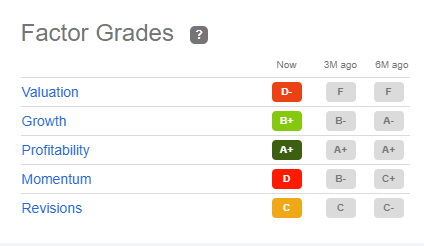

- Amazon’s valuation is going in the right direction with a current rating on D- compared to the F it had 3 and 6 months ago. If you restrict yourself to only stocks with premier, A+ ratings, you might just as well kiss good bye to tech in general and the mega-caps in particular. Only two stocks I track in my main portfolio of 20+ stocks on Seeking Alpha carry an A or A+ rating and those two are AT&T (T) and Altria Group (MO). The undervaluation thesis for both these stocks is very clear: debt and low margin for AT&T, regulatory threats and terminally declining industry for Altria. None of these apply with the same severity to Amazon.

- Apple Inc. (AAPL), often the poster child of fairly valued or even undervalued tech stocks, carries a valuation rating of F on Seeking Alpha. The other mega cap peer, Microsoft Corporation (MSFT) is no exception and carries a F on its valuation too.

- Notice the profitability rating for Amazon below and the valuation being high may seem a bit more reasonable. Once again, the three heavy weight techs are similar with Amazon, Apple, and Microsoft all having an A+ rating on profitability. A favorite (paraphrased) axiom of Warren Buffett comes to mind here: sometimes you need to pay for quality.

AMZN Ratings (Seekingalpha.com)

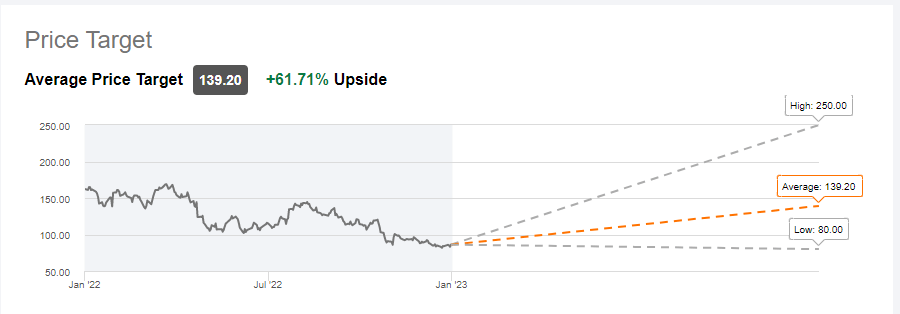

Price Targets – More Upside Than Downside

Analyst price targets are always to be taken with a pinch of salt but nothing in this section of the original article sounds bearish to me.

- Both median and mean price targets are more than 50% away from the current trading price of $86.

- The lowest price target of $80 is about 7% lower, which definitely tilts the risk-reward in favor of longs here.

AMZN Target (SeekingAlpha.Com)

Three Ways To Play If You are Bullish on Amazon

If you are an investor, with at least a 3 year time frame, this is the time to be accumulating Amazon and other big tech names that you believe in. Is the bottom in? I don’t think so but if you believe anyone can predict a bottom every single time, I have a bridge to sell.

Can the stock go down further? Sure. And it likely will. I present three things you can do to ensure you don’t go all in but at the same time, don’t miss out on the opportunity to make a lot of money in the long-term by being too worried about just the short term.

- Option #1: Stepladder your way. Pick the three factors mentioned below based on your risk tolerance and desired allocation to Amazon (or any other stock).

- The price at which you would like to purchase shares, in terms of percentage from the current share price. For example, if a stock is at $100 and you’d like to buy it at $90, that’s 10% from the current price. Step-laddering your way, in this example, means buying more shares in Amazon for every 10% fall from your last purchase price. Let’s call this X.

- Number of shares purchased in each trade. Let’s call this Y.

- Your target allocation to Amazon, in terms of number of shares or total amount invested. Let’s call this Z.

- For each x% fall, buy Y shares until you reach your target, Z.

- Option #2: Sell puts as detailed in this article. In this strategy, you agree to buy the stock at a lower price that you pick while collecting premium for doing so. Bear in mind, this strategy is a bit riskier in down-trending markets like this as your strike price maybe reached quicker than you think.

- Option #3: Sell covered calls as detailed in this article. If you already hold at least 100 shares of Amazon, you can simply sell a call at a strike price higher than the current market price to collect premiums. You may also buy shares and immediately write covered calls on them as part of this strategy. Covered calls tend to work better in down-trending markets like this one. You could potentially miss out on higher long-term profits if you are called away but at least you are collecting some premium right away in exchange. This is much better than selling out right and watching your stock go high.

Conclusion

Being a long-term investor in general, I am not convinced that selling a stock like Amazon after a nearly 60% fall from highs is the right strategy. Sure, there is no guarantee that the stock will ever reach those highs but with just AWS potentially valued at $600 Billion and the growth in advertising revenue, selling here may not be the best advice. If you are trader who thinks you can time things right enough times to make profits, go for it. For the other 99% of our readers, I say hold the stock now and buy on further weaknesses.

Be the first to comment