georgeclerk/iStock Unreleased via Getty Images

It’s been a difficult year for Amazon (NASDAQ:AMZN), and the stock’s price action illustrates the challenging environment, down by nearly 40% YTD. Growth concerns, recession fears, disappointing earnings, and other elements have worsened sentiment surrounding Amazon, causing many investors to flee the stock. However, despite the recent difficulties, growth slowdown, and the “coronavirus hangover effect,” Amazon remains the dominant market-leading e-commerce stock to own moving forward. Threats of increased competition are exaggerated, and the company should perform well during a downturn. Additionally, the company’s growth story is far from over, and we should see Amazon becoming increasingly profitable. The company’s stock is inexpensive, and shares should benefit from the recent split. Amazon is a buy now, and the company’s stock should move considerably higher in the coming years.

The Coronavirus Hangover Effect

Amazon is the ultimate name in e-commerce. Last year, the company accounted for approximately 57% of all e-commerce sales in the U.S. Also, Amazon saw a remarkable surge in revenues during the coronavirus crisis. The company’s revenues skyrocketed by 67.5% in two years, from 2019 to 2021. This surge in sales was partly because many consumers shopped from home instead of brick and mortar establishments during the pandemic. However, now that the coronavirus dynamic is much less restrictive, many shoppers are returning to their offline shopping habits.

This year’s consensus revenue estimates are for $525 billion, implying that Amazon’s sales growth will be around 12% YoY. While this figure may appear “slow” relative to prior years, we should consider the hangover effect associated with the coronavirus. Amazon cannot increase revenues by 30% or more annually, especially when millions of shoppers are increasing their visits to malls and other brick-and-mortar establishments. Nevertheless, Amazon is still about to increase revenues by approximately $55 billion YoY. The company’s sales growth is a phenomenal achievement, considering the environment. Moreover, Amazon’s revenues should come in at about 88% above 2019 levels, yet its stock now trades only around Amazon’s 2018 and 2019 highs.

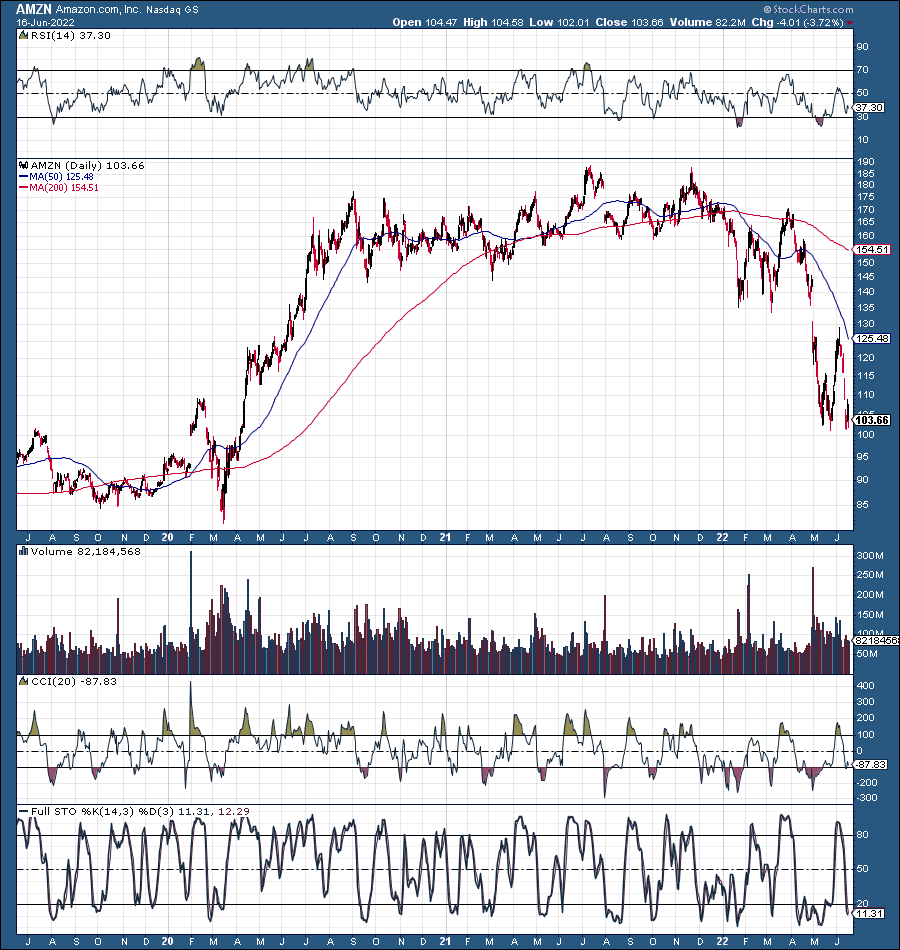

AMZN Stock – A Technical Image

AMZN (StockCharts.com)

Amazon was down by about 47% from its highs last year. We also see that the stock is down to around $100. Remarkably, AMZN is back down to levels we saw in 2019 and as far back as 2018. However, in 2019 Amazon’s EPS came in at $0.93, and next year’s EPS estimates are for approximately $2.50. Moreover, 2019 revenues were $280 billion, and next year’s revenues should come in at around $610 billion (consensus estimates). Therefore, we’re looking at a stock that was trading at approximately 100 times forward EPS estimates and 3.6 times forward sales around the highs in 2018 and is only trading at about 40 times forward EPS estimates and 1.64 times forward sales now. Yes, Amazon is finally cheap, the downside is probably limited here, and there’s potential for much more upside in the coming years.

Amazon Is Becoming Increasingly Profitable

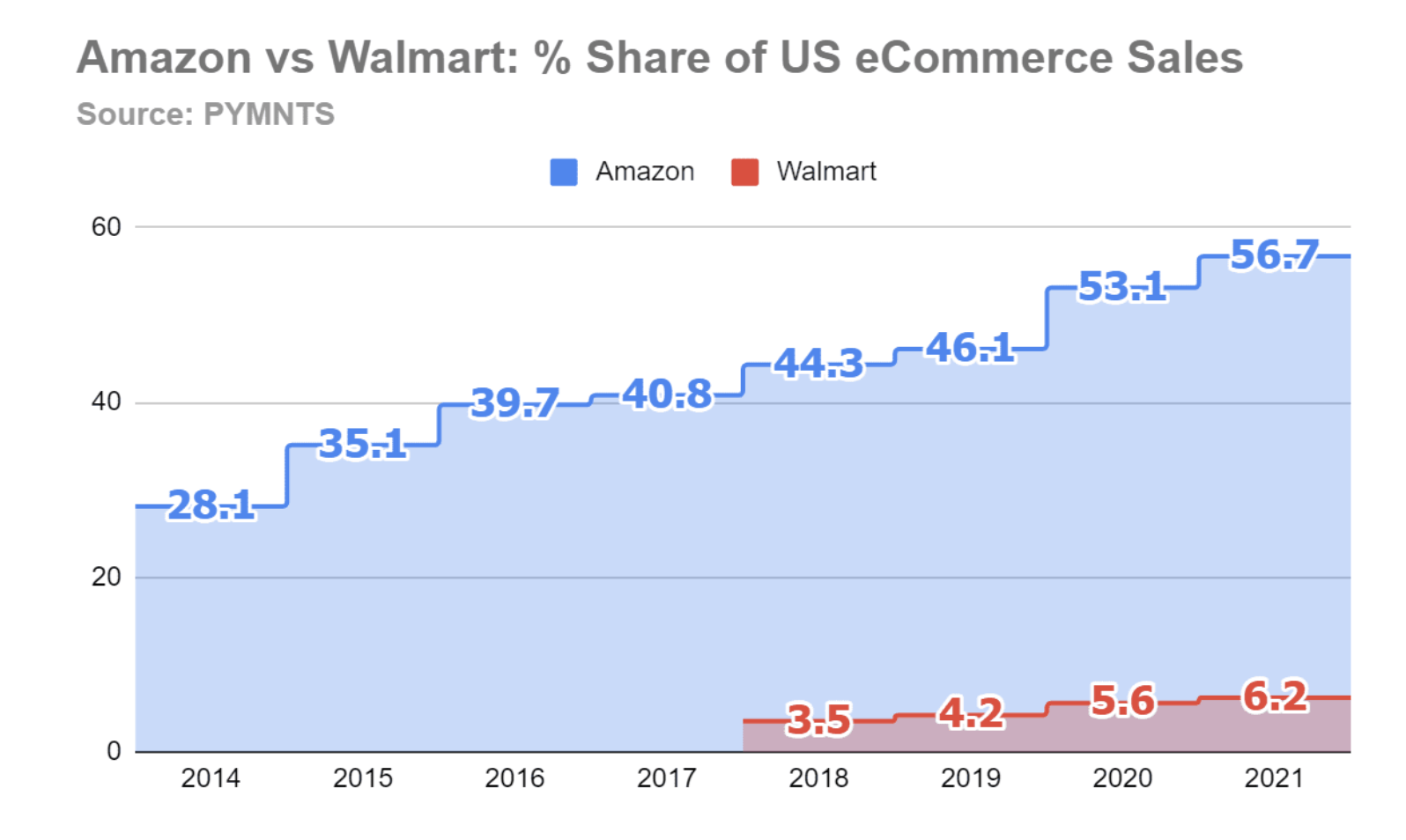

First, I would like to point out that Amazon’s growth story is far from over. Amazon is the dominant e-commerce giant in America and has significant operations in several key international markets. The company has dedicated operations in the U.S., U.K., Canada, Mexico, India, France, Germany, Italy, Spain, China, Japan, and Australia. Also, those saying that Walmart (WMT) or someone else will take market share from Amazon or beat the company at its own game may be mistaken.

Amazon vs. Walmart

AMZN vs. WMT (Pymnts.com)

We see that Amazon dominates e-commerce sales in the U.S. and may achieve similar success in other countries. While Walmart has had some success in recent years, its market share is limited relative to Amazon’s advantage.

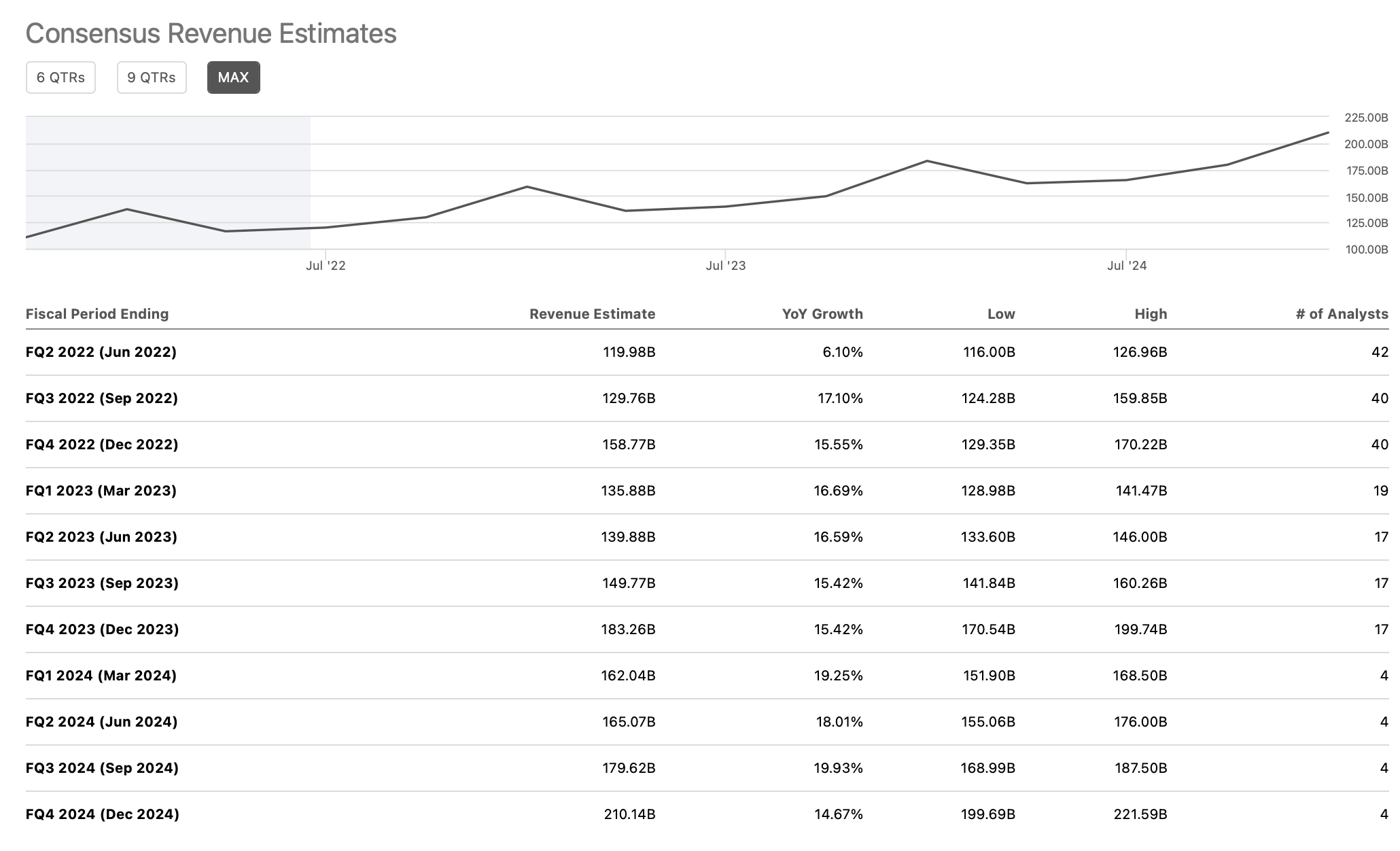

Revenue Estimates

Revenue estimates (SeekingAlpha.com)

We discussed that Amazon would likely deliver around $520 billion in revenues this year, roughly a 12% YoY increase. However, next year’s consensus estimates are for $610 billion, approximately a 17% YoY increase. Therefore, the company’s growth will probably increase once the coronavirus hangover effect wears off. Moreover, 2024 consensus revenue estimates are for about $717 billion, roughly a 17.5% YoY increase from 2023’s consensus figures.

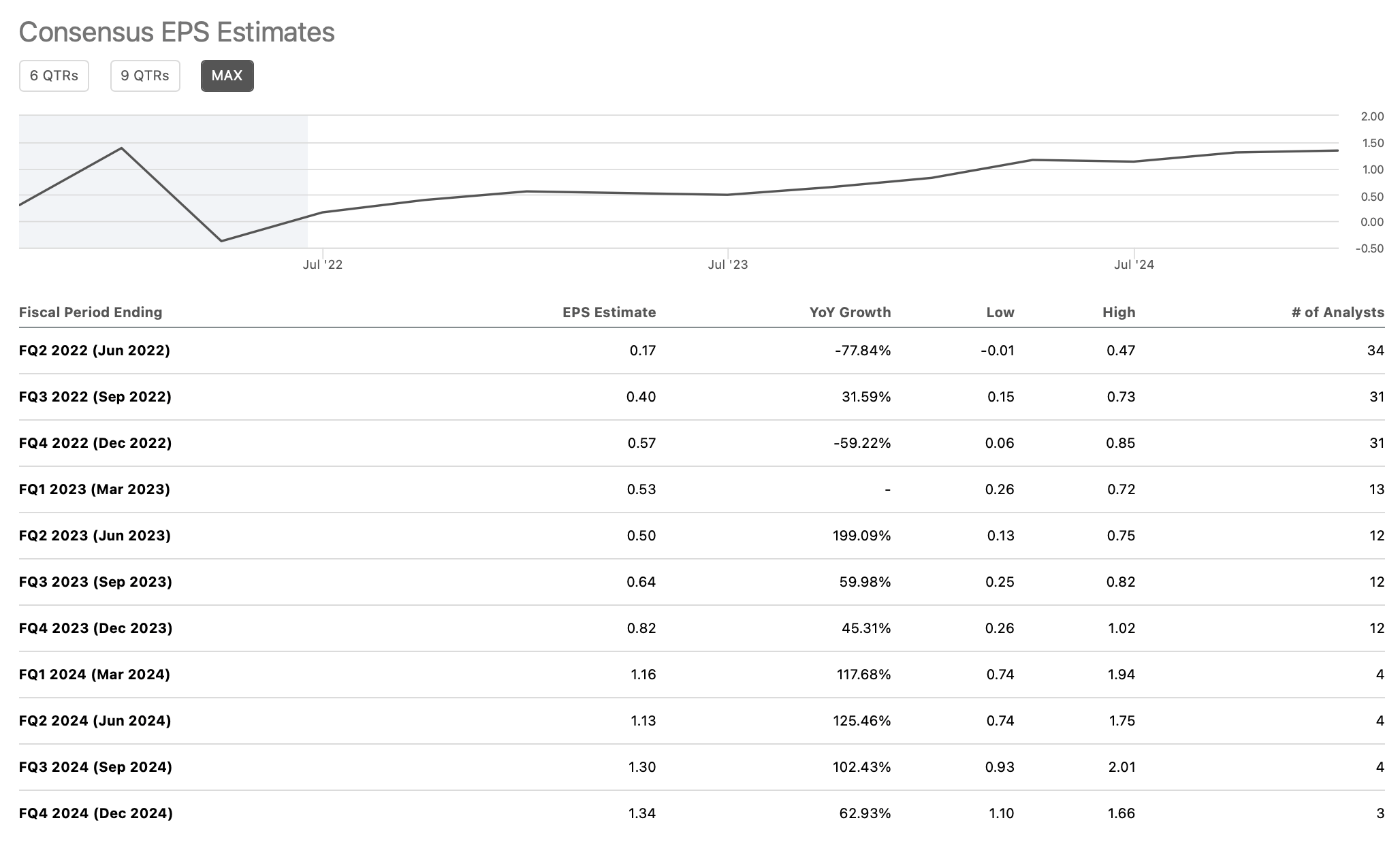

EPS Probabilities

EPS probabilities (SeekingAlpha.com )

Amazon should deliver about $2.50 in EPS in 2023, but consensus analysts forecast approximately $5 in 2024. Therefore, we could see Amazon become increasingly profitable in the coming years, and the company’s stock is trading at only about 20 times 2024 EPS estimates now. This valuation is remarkably cheap for a leading growth company like Amazon.

Is Amazon Recession Proof?

I know there’s much talk about a recession lately, which is one reason why Amazon’s stock is down by so much from last year’s highs. However, even if the economy falls into a mild recession, people still need to shop, and there’s no better place to do it than Amazon. Moreover, with surging gas prices, more people may shop online to save money and time. Therefore, even in a slowdown, Amazon should weather the storm relatively well, and we should not see significant revenue or EPS declines from the e-commerce giant. Additionally, once the economy is ready to come out of the downturn, Amazon may be one of the top stocks to benefit from the increases in consumer spending, sentiment, and confidence. Therefore, I want to own this stock. I recently reentered Amazon and may increase my position as we advance.

Here’s what Amazon’s financials could look like as we advance:

| Year | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 |

| Revenue Bs | $520 | $610 | $717 | $839 | $973 | $1,120 |

| Revenue growth | 17% | 17.5% | 17% | 16% | 15% | 14% |

| EPS | $0.76 | $2.50 | $5 | $6.50 | $8 | $10 |

| Forward P/E ratio | 40 | 40 | 40 | 40 | 40 | 40 |

| Price | $100 | $200 | $260 | $320 | $400 | $500 |

Source: The Author

Risks To Amazon

While I’m bullish on Amazon in the intermediate and long term, risks exist. There’s some risk of increased competition, where other companies could take more market share from the e-commerce giant. There is also the risk of growth being slower than other analysts and I anticipate. The recession is likely approaching, and there is the risk of more downside pressure on the stock. Also, Amazon may not become as profitable as estimated, and it may take the company longer to achieve significant ($10 or higher) EPS. Therefore, there’s a risk of Amazon’s stock not reaching my price targets as quickly as estimated. Investors should weigh these and other risks carefully before investing in Amazon.

Be the first to comment