mariusFM77

Article Thesis

The world is very uncertain, and a recession in 2023 would be far from surprising. In an environment like this, going for companies that have proven to be resilient versus all kinds of crises could be a wise move. And when those equities offer nice dividend yields, that’s even better. Philip Morris International (NYSE:PM) and Altria (NYSE:MO) are two such resilient high-yielders, but I believe that one — Altria — is a much better investment than the other at current prices, which I will explain in this article.

Tobacco Stocks For Crisis Protection

2023 could be a difficult year for the economy and for the stock market. The Fed is poised to increase interest rates further this year, as inflation hasn’t slowed down to the desired 2% range yet. At the same time, it’s pretty likely that the interest rate increases will result in a slowdown of economic activity. Housing, automobiles, and so on will be hit by higher financing costs, which will negatively impact economic development this year. On top of that, the war in Ukraine continues, supply chains remain under pressure, and COVID is a wildcard as well — although the biggest proponent of Zero COVID, China, has moved away from that policy in recent months.

In an environment like that, cyclical businesses could be a risky investment. Depending on how much the economy slows down, automobiles, industrials, and similar industries could suffer from lower revenue generation and weaker profitability. If that happens, their shares will most likely come under further pressure.

Other industries aren’t as exposed, however. Non-cyclical consumer goods, or consumer staples, such as food and beverages or household products, generally see consistent demand even during recessions. This also holds true for the tobacco industry. Cigarette demand does not decline during recessions, despite the fact that consumers have less cash to spend. Some studies show that there is even a positive impact on smoking rates (at least from tobacco companies’ viewpoint) from recessions. One study on the impact of the Great Recession on smoking rates in the US claims:

Results: Joinpoint regression analysis revealed no significant changes in smoking prevalence trends over the period 2005-2010. The crisis resulted in an increase in the number of smokers in the US by 0.6 million. This is largely due to an unexpected decrease of 1.7 million smokers among employed and an increase of 2.4 million smokers among unemployed individuals, whose smoking prevalence also remains extremely high in the post-crisis period (32.6%).

If the US were to enter a recession this year, the impact on smoking rates would thus, I believe, not be negative. Instead, it should be either neutral, or a recession might actually result in higher demand for cigarettes, which would be positive for the tobacco industry. I expect that a similar effect would be at play during a recession in overseas markets.

The tobacco industry thus seems like a good choice for a crisis-proven, resilient investment. The fact that many tobacco companies offer high dividend yields is another positive, as strong income helps investors keep calm in case equity markets pull back further (which is far from guaranteed, but possible).

MO Versus PM: Foreign Currency Exposure

Altria and Phillip Morris sell pretty similar products, as they more or less control the same brands — Altria sells them in the US, while Phillip Morris is responsible for the non-US business. One of the biggest differences between the two companies is thus their respective exposure to currency movements. Since Altria is only active in the US, there is no currency rate risk. Phillip Morris, on the other hand, with its entirely non-US business, is heavily impacted by currency rate movements. Currency rate movements can be an advantage for PM, but they can also be a disadvantage, depending on whether the US Dollar is getting weaker or stronger versus other currencies. In the recent past, the US Dollar has strengthened versus most currencies, including the Euro, Yen, and so on, which has been a drag on Phillip Morris’ profitability.

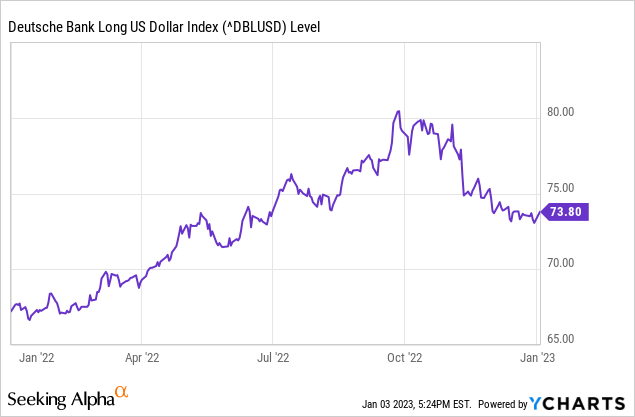

For fiscal 2022, Phillip Morris is forecasting (the fiscal year has ended but the company hasn’t reported Q4 results yet) currency-neutral earnings per share growth of 10% to 12%, with its Heatsticks/iQOS business being an important growth driver, while price increases on a per-pack basis also help improve profitability. Analysts predict that earnings per share will decline in non-currency neutral terms, however, as Phillip Morris is forecasted to see its profit drop from $6.05 to $5.69. In other words, Phillip Morris has been hit by a ~15% headwind from currency rate movements in 2022. And it looks like 2023 could be a year with a negative currency rate impact as well:

While the US Dollar Index has come off its highs that were hit in fall 2022, it’s still up meaningfully from where it stood one year ago. During Q1 of 2023, results should thus be negatively impacted to a meaningful degree as long as the US Dollar remains as strong as it is right now. The same holds true for Q2, as the Q2 2022 average is also below where the US Dollar stands today. Altria, meanwhile, will not feel any currency rate impact whatsoever — making it the less risky choice from a foreign exchange perspective.

There are other risks, of course. Regulation is a factor to consider, but there is no clear advantage here, I believe. Both companies face some regulatory pressure in the coming years. Altria is negatively impacted by potential nicotine regulation by the FDA, while Phillip Morris is negatively impacted by some anti-smoking regulation in countries such as New Zealand.

Altria Offers A Much Higher Yield At A Lower Valuation

Altria’s non-existant currency rate risk is not the only positive relative to Phillip Morris, however. Altria also offers a much higher yield and trades at a more attractive valuation.

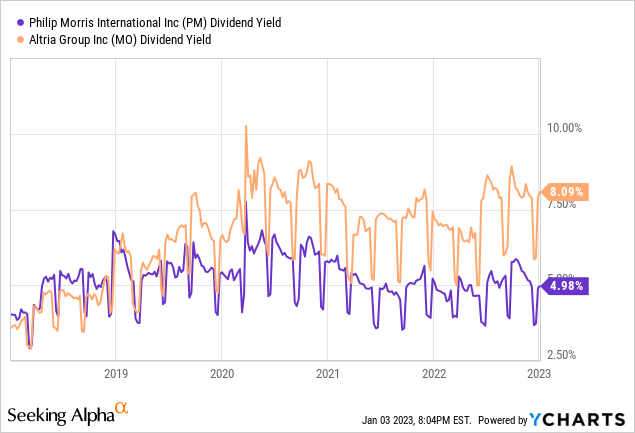

Based on the dividends that were declared over the last year, Altria offers a dividend yield of 8.1%, versus a 5.0% yield for Phillip Morris. While a 5% yield is still attractive in absolute terms, and versus the yield one can get from the broad market, Altria’s dividend yield is more attractive. In fact, Altria’s dividend yield is so high that no meaningful earnings growth or share price upside would be needed for MO to be a solid investment.

Altria has also offered more pronounced dividend growth in the recent past. Over the last five years, its dividend was increased by 34%, while Phillip Morris increased its dividend by 19% over the same time frame. A higher yield, combined with faster dividend growth, is preferable, of course. But on top of that, Altria also has a safer dividend, one could say. Its payout ratio is 78%, slightly short of the 80% long-term target that management has repeatedly touted in the past. Phillip Morris pays out 89% of its profits, which leaves less wiggle room in case earnings decline — due to the non-cyclical nature of the business, that’s not very likely, but if the Dollar continues to strengthen, that would be possible. No matter what, PM’s higher dividend payout ratio will leave less room for pronounced dividend growth in the near term, I believe.

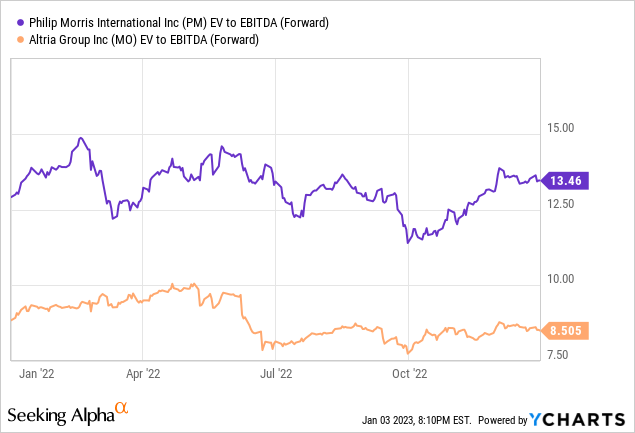

Looking at the two stocks’ valuations, we see that MO trades at 8.5x EBITDA, while PM trades at 13.5x EBITDA. I look at enterprise value for both companies, instead of market capitalizations, as we can account for differences in debt usage by doing so. Altria looks pretty cheap, whereas Phillip Morris is considerably more expensive. On an absolute basis, PM isn’t dramatically expensive, but it doesn’t look like a great value, while one could argue that MO is attractively priced with its EV/EBITDA multiple standing well below 10.

Takeaway

The two companies own the same brands and both benefit from the resilient nature of the tobacco industry. But MO is not exposed to a strengthening US Dollar, unlike PM, and MO offers much better dividend characteristics. This includes a much higher yield, faster dividend growth, and substantially stronger dividend coverage. When we add MO’s much lower valuation, Altria seems like the better pick to me at current prices.

I last covered PM in 2020, when I called it a Buy. But following a total return of more than 50% in a little more than 2 years (the broad market delivered an 11% return over the same time frame), Phillip Morris does not look like a Buy here, and Altria seems considerably more attractive to me at current prices.

Be the first to comment