Mario Tama

Shares of Altria (NYSE:MO) surged 6% after the tobacco company presented earnings for the fourth-quarter a week ago, but the company’s solid 8% dividend yield is still cheap. Altria returned a significant amount of capital in FY 2022 to shareholders of the business and it will continue to buy back a ton of shares in FY 2023. While there are fundamental challenges for Altria such as inflation and the decline in the share of smokers, the firm delivers a dividend that is covered by adjusted earnings. Additionally, Altria’s low valuation makes the stock interesting for dividend investors! Last I covered Altria in Nov 2022.

Top line challenges are real

Altria’s net revenues declined 3.5% year over year to $25.1B in FY 2022 due to a number of factors including falling industry volumes and high inflation. Top line challenges have existed for a while in the tobacco industry which is seeing a secular shift away from traditional products like cigarettes and cigars.

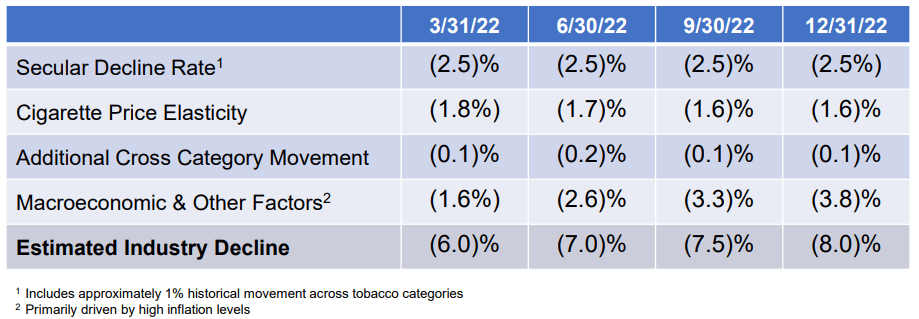

According to Altria, the adjusted cigarette industry volume declined 8% in FY 2022 due chiefly to macroeconomic factors. The total industry decline rate of 8% in FY 2022 is explained by a number of different factors that include the secular decline rate (which was stable at around minus 2.5% throughout last year), price elasticity factors (1.6%) and especially macroeconomic factors which include the impact of inflation which is weighing on demand. Macroeconomic headwinds were by far the biggest factor explaining the decline in industry cigarette volumes in Q4’22 as well as in FY 2022.

Source: Altria

Altria has seen a gradual slowdown in its top line growth rates for years and investors shouldn’t expect a major change to occur going forward. In FY 2023 and FY 2024, Altria is expected to grow its revenues of 1.7% and 1.1% which means that the potential for a significant up-wards revaluation of Altria’s shares will remain limited, in my opinion.

Altria is a capital return play

Although Altria is struggling on its top line, the company’s product portfolio generates a decent amount of cash that allows the tobacco company to fund generous capital return plans for the benefit of shareholders.

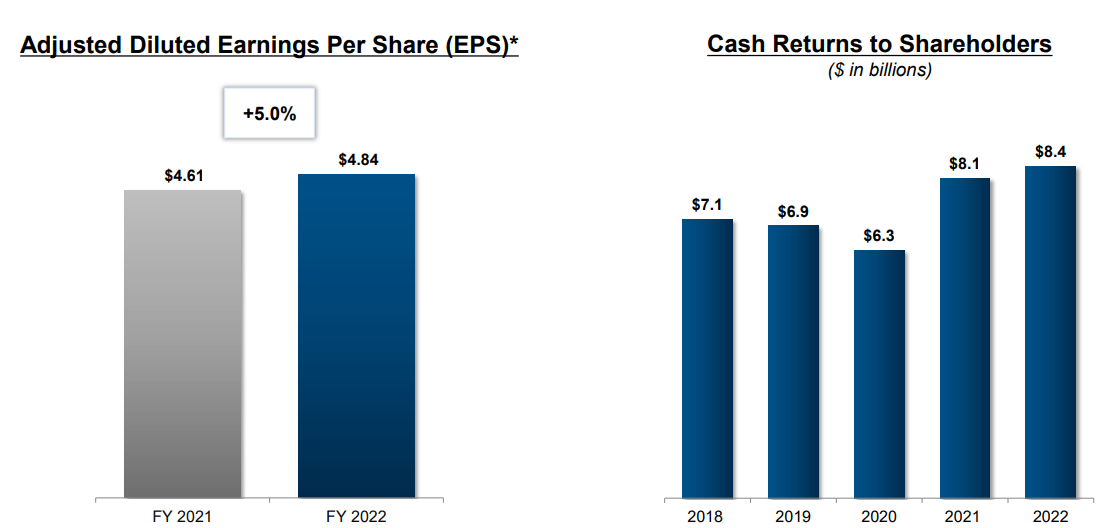

In FY 2022, Altria returned $8.4B of its cash to shareholders, $6.6B of which related to the tobacco company’s dividend payments. On average, Altria returned $7.4B each year between FY 2018 and FY 2022. The tobacco company also said that it exhausted its previously authorized $3.5B stock buyback authorization in the fourth-quarter and announced a new stock buyback of $1.0B. The new buyback is expected to be completed by the end of the year.

Source: Altria

EPS outlook for FY 2023, estimated forward dividend coverage ratio and valuation

Altria earned $4.84 per-share in adjusted diluted earnings in FY 2022, showing 5% year over year growth. The company’s earnings easily covered the tobacco company’s total annual dividend payment of $3.68 per-share. Based off of adjusted EPS, Altria paid out 76% of its earnings in the last year.

For FY 2023, Altria anticipates to be able to earn $4.98 to $5.13 per-share which implies an annual growth rate of 3-6%. Altria is going to pay two more quarterly dividends of $0.94 per-share in the first half of FY 2023 and then will have to decide about its customary mid-year dividend increase. In FY 2022, Altria raised its dividend payout 4.44% and given that the dividend is covered by adjusted earnings, I expect that the tobacco company will raise its dividend another four cents to $0.98 per-share in the third-quarter, implying a 4.3% raise.

In total, shareholders could therefore expect a total annual distribution of approximately $3.84 per-share which would reflect a 76% payout ratio on a mid-point basis. The estimated forward dividend yield then would be around 8.2%.

Based off of Altria’s new EPS guidance, shares of the tobacco company are valued at 8.9 X FY 2023 earnings. Given the limited potential for valuation gains, I consider MO to only be slightly undervalued. A P/E ratio of 10.0 X is realistic and achievable for Altria and it would imply a fair value of $50.55… giving MO about 8% up-side potential.

Risks with Altria

Altria’s core business, which is made up of smokable products, will continue to experience headwinds: the share of smokers is set to continue to decline and the regulatory environment will remain challenging as well. Restrictions on tobacco advertising, lawsuits and potential vape bans are key risks that investors have to be aware of before buying Altria’s 8% dividend.

Final thoughts

Altria is an attractive capital return play for dividend investors that plan to buy MO once and leave it in their portfolios for a long time. Although Altria’s business model is challenged in the sense that less people smoke and its top line only growth slowly, I believe Altria supplies a very attractive dividend yield of 8% which is solidly covered by the tobacco company’s adjusted earnings. Investors can continue to expect aggressive stock buybacks that are set to support the stock price and the dividend will likely also keep growing. Since shares of Altria are undervalued, based off of earnings, I believe MO has an attractive risk profile!

Be the first to comment