Mario Tama

Looking at the recent gains in some well known mega-cap tech names, investors may be forgiven for thinking we are back in 2021 with no inflation in sight and Fed’s Zero Interest Rate Policy (“ZIRP”) in full flight. Granted, some of these names were beaten down excessively in 2022 and deserved a bit of a break in 2023 but something like a 100% gain in Tesla, Inc. (TSLA) from its recent lows is mind boggling to say the least.

Meanwhile, away from much fanfare, Altria Group, Inc. (NYSE:MO) has gotten off to a quieter start returning about 4% so far while also announcing solid earnings and guidance, with a buyback announcement being the cherry on top. Although I believe Altria deserves a position in any diversified portfolio anytime, I present five reasons (two Macro and three Altria related) as to why Altria deserves your attention right now. Let us get into the details.

Macro: Market Valuation

NASDAQ fell by 33% in 2022 and the financial media acted like the World was coming to an end, with absolutely no context to what got us there. But in about a month in 2023, NASDAQ gained ~15% at its peak. Using a simple $100 example, the 33% fall in 2022 took us to $67 and the 15% increase in 2023 has pushed us back to $77. That means, since the last trading day of 2021, the tech heavy NASDAQ is down just a little bit above the classic bear market definition of 20% on the back of a decade long bull market buoyed by ZIRP.

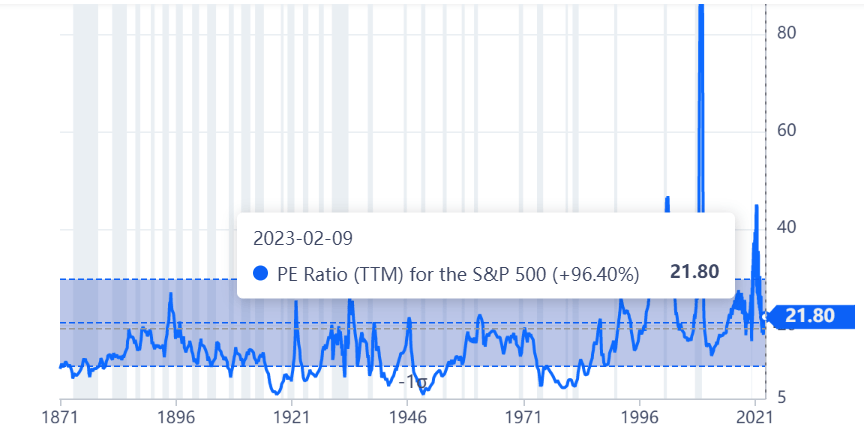

If you believe using NASDAQ is cherry-picking, let us look at S&P 500’s valuation (chart below). The current multiple is almost 22, which doesn’t appear too bloated until you factor in the expected earnings growth of 2.5%. As funny as that sounds, that gives the market a Price-Earnings/Growth (“PEG”) ratio of 8.8. As I’ve stated before, valuation does not matter until it does. The contrarian in me believes the January effect was exaggerated this year due to December (and the entire year) we had coming in. Now maybe the time to seek shelter in reasonably valued stocks like Altria Group, Inc.

S&P 500 PE (gurufocus.com)

Macro: Powell and Fed

“Powell speaks and the market dips” used to be the 2022 tagline. But from the limited opportunities we’ve had this year, it looks like the market is getting complacent and is only seeing what it wants to see and not what all there is to see yet. As can be seen in this transcript, it is pretty evident that the Fed still has a lot of work before it reaches its targeted inflation rate of 2%.

In addition to raising interest rate by 25 basis point as expected, Chairman Powell also mentioned ongoing increases will happen and are needed to meet the target. In addition, the Job market is still so strong that those who bet in favor of a rate cut can forget it for at least a year. The report also says that consumer spending is not increasing at the expected pace and that usually means inelastic products (like Tobacco) tend to do better than elastic products.

Altria: Declining Volume, Sure But A Fortress

The recent Q4 report had a line that caught my attention recently:

In 2022, our businesses were not materially impacted by increased costs resulting from global supply chain challenges and high inflation.”

Altria’s declining volume (perhaps, rightly so) gets a lot of attention. But not the fact that it was one of the few companies that did not face any pressure not just due to inflation but also the global supply chain issues that crippled almost every company. In short, Altria is operating a mini-kingdom that is its fortress with minimal dependencies on things it cannot control. To summarize Altria’s strength as a business and investment:

- Pricing Power – Check

- Brand Loyalty – Check

- Operational Discipline – Check

- Commitment to Shareholders – Check

Altria: EPS Estimates – Revising Up

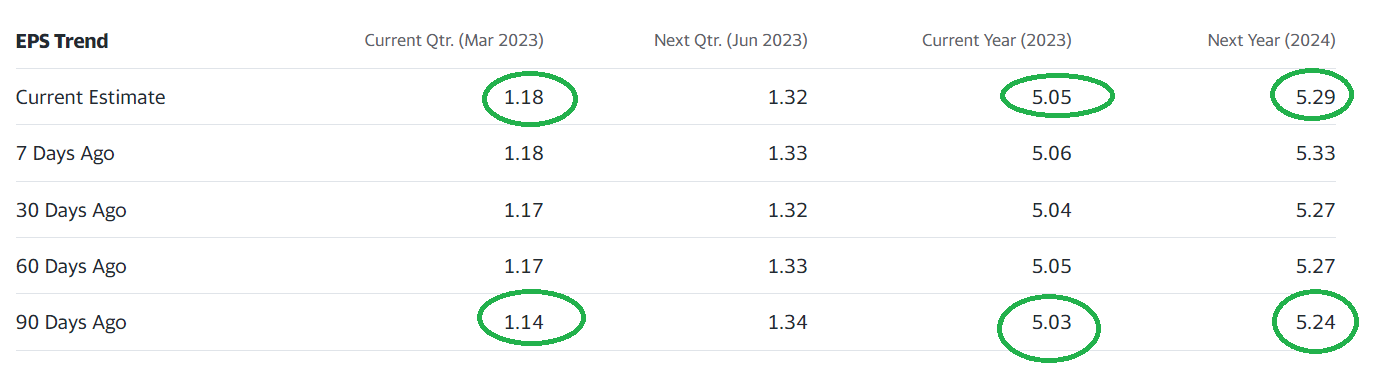

Altria’s earning estimates have been trending up for most part as shown below, which is a rarity in this market. Using 2023’s EPS estimate of $5.05, the stock is trading at a forward multiple of 9.30. Obviously, that number by itself looks massively attractive but when put into context with an expected earnings growth rate of 4.64%, the stock carries a PEG multiple of 2. That is not exactly cheap by definition. Generally, I’d stay away from stocks with a PEG >2 but Altria gets an exemption due to its reliable (and increasing) dividend.

MO EPS (Yahoo Finance)

Altria: Breaking Out – Technically

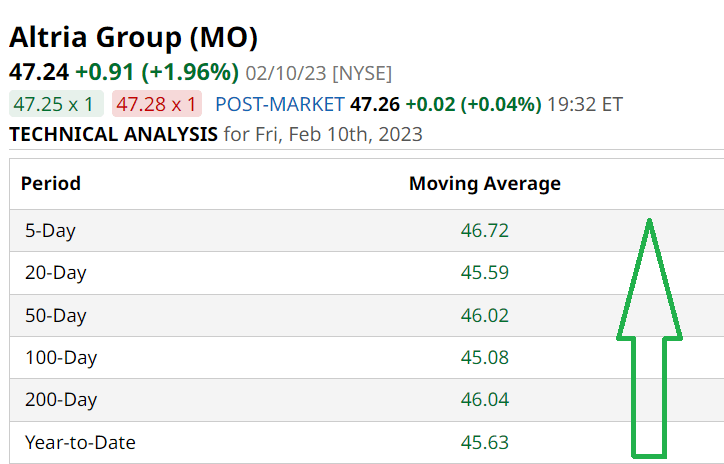

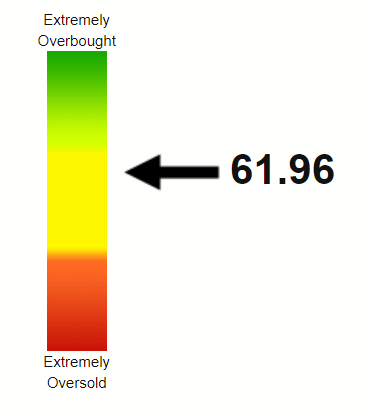

The recent post-earnings run-up in price has helped the stock clear all the commonly used moving averages as shown below. The fact that Altria has managed to break out above the 200-Day moving average without being overbought AKA “chased” shows it has been in a general period of consolidation and the stock may be poised for a run higher. Altria’s Relative Strength Index (“RSI”) is about 60, which is considered a sweet-spot as it shows the stock is having momentum but still has room to run.

MO Moving Avgs (Barchart.com) MO RSI (StockRSI.com)

Conclusion

While I am glad my “cutting edge” stocks like Tesla and Meta Platforms, Inc. (META) have produced wonderful returns so far in 2023, the contrarian in me cannot help wondering if that space is once again getting too crowded. The recent excitement around Artificial Intelligence in general and ChatGPT in particular is bringing a lot of focus back on technology sector.

Once again, being a contrarian, I don’t personally like much attention and don’t want my stocks to be in the limelight unnecessarily. I continue enjoying the shelter Altria provides with its stability and ever-increasing dividends. If you don’t hold a position in this stock, I see a margin of safety till the multiple reaches at least 11, which as things stand now is till the $55 price point.

Be the first to comment