krblokhin/iStock Editorial via Getty Images

Introduction

It has been almost two years since my last article on Alpine Banks of Colorado (OTCQX:ALPIB) was published. This small-cap bank with a balance sheet total of approximately $6B is operating in Colorado and has a strong history of exceptionally low loan loss provisions thanks to its focus on credit quality.

After the most recent capital raise completed in July, the market capitalization is now approximately $505M based on the current share price of just under $31 and the current share count of 16.37 million equivalent shares. The shares trading on the exchange are non-voting shares, while the bank also has just over 52,000 A-shares outstanding. Those shares do have voting rights and are entitled to 150 times the economic interest of the B-shares. In this article, I will only discuss the B-shares and I have multiplied the A-shares by that same factor of 150.

The first half of the year was fine as loan quality remains strong

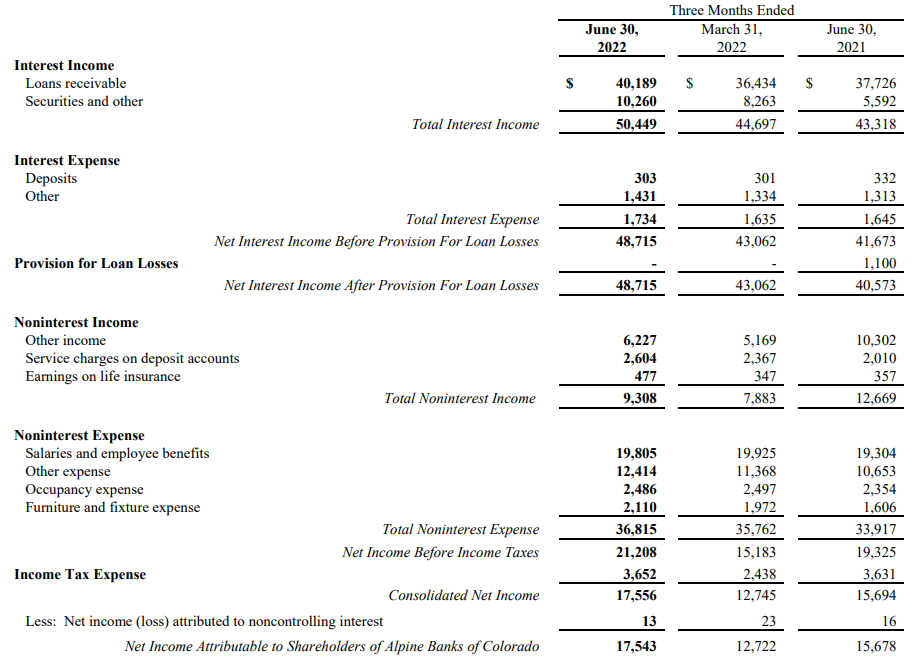

Alpine’s performance in the second quarter was good, as the company reported a net profit increase compared to the first quarter of the year.

During the second quarter, the net interest income increased by almost $6M and that was the main reason why the pre-tax income increased by a similar amount, ultimately leading to a net income of $17.5M for an EPS of $1.14 per share.

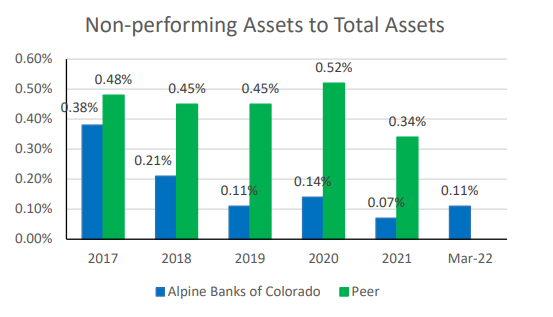

ALPIB Investor Relations

As you can see in the image above, the bank hasn’t had to record any additional loan loss provisions, which once again is a testament to the excellent credit quality of the loan book. Alpine Banks did not publish a presentation discussing its Q2 results, but the Q1 presentation shows Alpine Banks of Colorado has a long history of outperforming its peers when it comes to the quality of its assets.

ALPIB Investor Relations

The recently completed capital raise will beef up the balance sheet

In July, the bank announced it completed a $34M placement of common stock by issuing just under 1.2 million shares of Class B stock at $28.5/share. Alpine Banks mentioned the use of proceeds would go toward general corporate purposes and to support organic growth while supporting regulatory capital ratios.

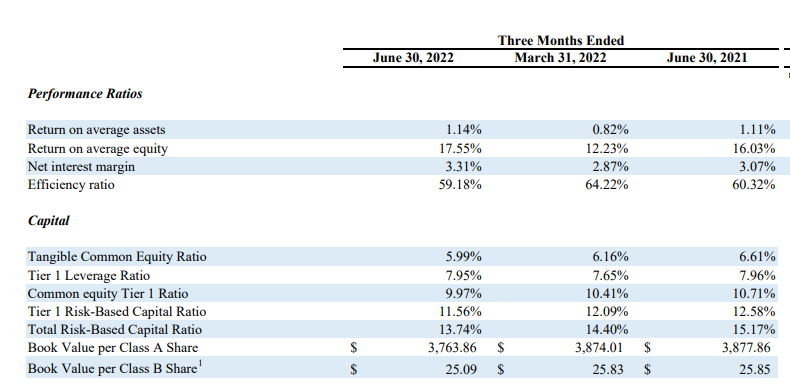

As of the end of June, the bank’s capital ratios were pretty decent, but the CET1 ratio dropped below 10% and the Tangible Common Equity Ratio fell from 6.61% a year ago to just 5.99% as of the end of June of this year. That’s not necessarily an issue as the regulatory minimum for the CET1 ratio was just 6.5% as of the end of last year and I don’t anticipate any drastic or dramatic changes in this requirement, so Alpine Banks didn’t have a gun to its head to raise the cash.

ALPIB Investor Relations

The capital raise will achieve two important things. First of all, there should be a positive impact on the CET1 ratio. Although the bank has not disclosed its total amount of risk-weighted assets used for the calculation, I would assume the CET1 ratio jumps to in excess of 10.5% again (excluding the impact of retained earnings and additional losses on the AFS portfolio during Q3). A bond rating document shows the Q1 2022 RWA at approximately $4B, which means the $32M net proceeds could boost the CET1 ratio by up to 80 base points, so my target of 10.5% is likely conservative.

Secondly, although it may sound counter-intuitive to boost the book value by issuing new shares, this actually was a move that made a lot of sense from a balance sheet perspective. As of the end of June, the book value per B-share was $25.09 while the tangible value per share was $23.93 after deducting the $17.6M in goodwill from the equation. This means the recent raise was priced at a premium of 19% to the most recently known tangible book value per share.

Keeping all things equal and assuming a 6% total cost related to the share issue for total proceeds of $32M (the total finders fees were estimated at $1.655M but I’m rounding this amount up to $2M as there will for sure be some legal fees as well), the tangible book value per share will actually increase by about 20 cents to $24.13 (this again excludes the impact from retained earnings and the evolution of the value of the securities portfolio). So, the capital raise made sense on multiple levels. That being said, Alpine Banks repurchased in excess of 200,000 shares during the second quarter (as the share count decreased from in excess of 7.5M shares to just over 7.3M shares) and as the stock was trading above $30/share throughout the quarter it looks like Alpine raised cash at a lower level than it was buying back its own stock at, and that’s not something I generally like to see.

Investment thesis

While the underlying results are strong, Alpine’s capital ratios and book value were hit by the direct impact of an increasing interest rate on the value of the portfolio of securities available for sale. While I usually support a company’s capital raise as it definitely is a sign of prudent capital management and balance sheet management, I’m a little bit surprised the bank issued new shares just weeks after buying back its own stock at a higher price.

Despite this, I do think Alpine Banks is well lead and it’s unfortunate to see the book value erode due to the lower value of the available for sale investment portfolio, which reduced the book value per B-share by $3.48 in the second quarter after already recording a $1.97 hit in Q1. The reported book value fell by just over $2/share in the first semester thanks to the bank’s policy to retain most of the profits on the balance sheet and ALPIB retained about $1.6/share in profit in the first half of the year.

Be the first to comment