CatLane

Introduction

I’m starting coverage of Ally Financial (NYSE:ALLY), as we’ll be focusing more on automotive and related loans in the future. And what better way to start than diving into the company’s just-released quarterly earnings, which came in better than expected at a time when “everyone” seemed to be bearish on automotive loans and credit quality. Even better, the company’s guidance exceeded expectations, while credit quality isn’t expected to deteriorate by a lot.

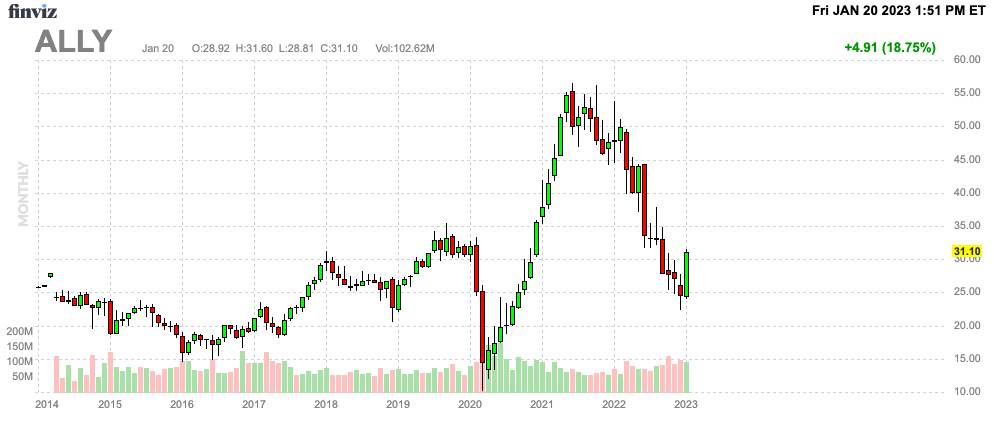

It triggered a stock price rally of almost 20%.

FINVIZ

The bottom line is straightforward. Investors who believe the Fed can achieve a soft landing might enjoy buying ALLY at current levels. Investors who believe that ongoing economic developments will last should be very careful of current optimism.

I believe that caution is appropriate, as I’m not yet buying the soft landing narrative.

Now, let me elaborate on all of this!

A Quick Company Overview

Located in Detroit, Michigan, Ally is a company providing financial services, including car finance, online banking via direct bank, corporate lending, vehicle insurance, mortgage loans, and related services.

Founded in 1919 by General Motors (GM), the Motown-based corporation has become the largest car finance company in the United States.

Ally Financial

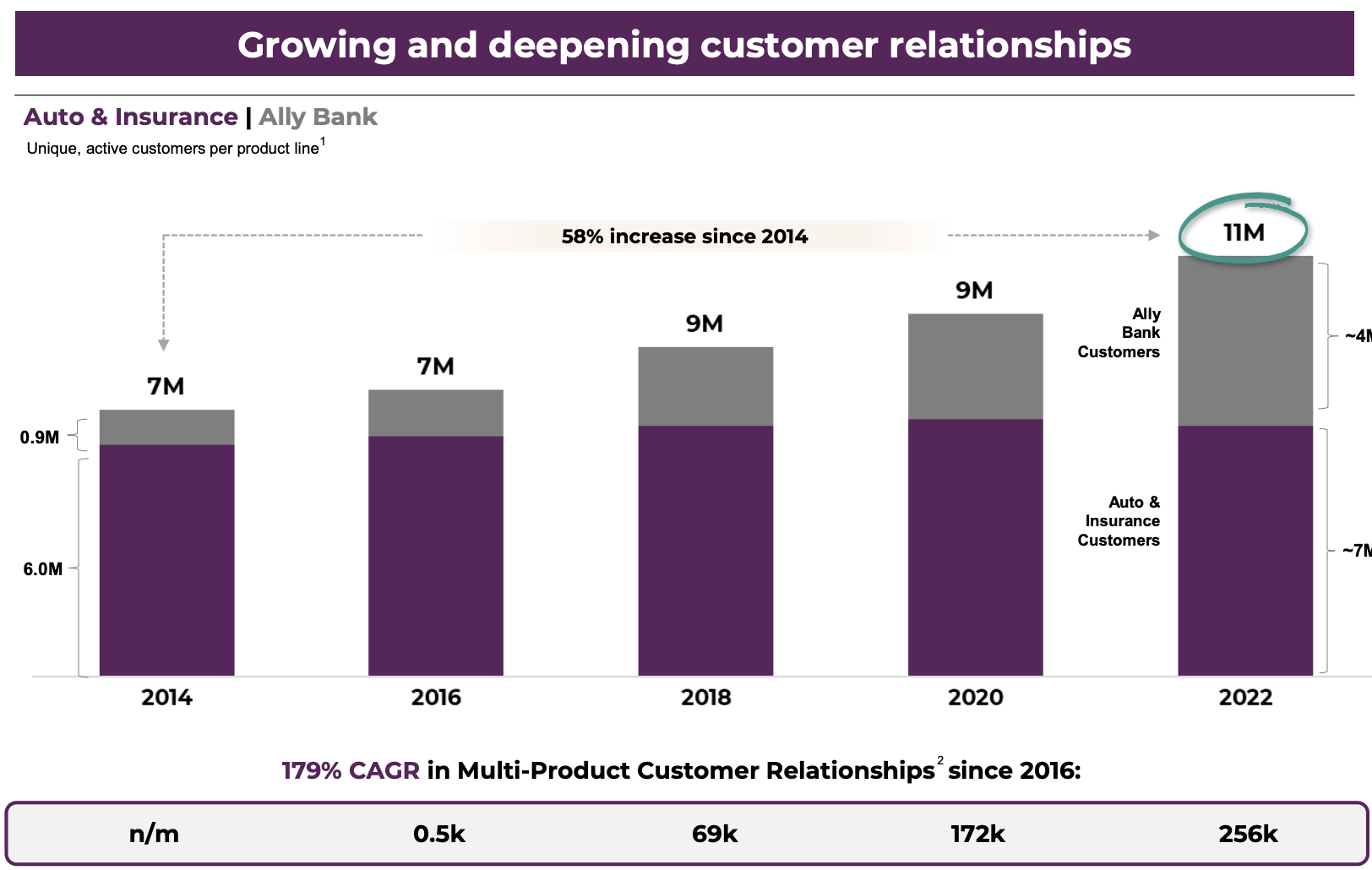

The company has 11 million customers. Seven million of them are part of auto and insurance. Four million customers are Ally Bank customers. Moreover, the company is rapidly growing multi-product customer relationships. In 2022 alone, it added more than 250 thousand multi-product customers.

Ally Financial

Until 2010, the company was known as GMAC, which meant General Motors Acceptance Corporation.

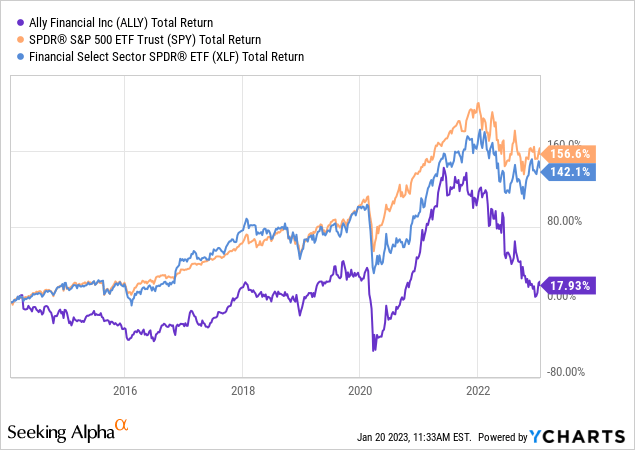

The company went public in 2014. Since then, it has returned 17.9%, including dividends. This is not even close to what the market and financial stocks have returned since then.

Like many other banks and financial institutions, investing in ALLY is a bit like picking up pennies in front of a steam roller, as economic declines and financial headwinds tend to quickly erase long-term gains.

The reason that has pushed the ALLY stock price from $55 in 2021 to $25 before the earnings call is weakening credit fundamentals.

An Awful Macroeconomic Environment

I’m not telling you anything new when I say that we’re in a tricky market environment. Inflation is high and persistent, economic growth is weakening, and the Fed is eager to not only fight inflation but keep it down on a long-term basis. After all, that’s its job.

The bad news is that this is putting tremendous pressure on the automotive sector and its clients. Needless to say, that industry is highly dependent on credit and customers’ willingness/ability to spend.

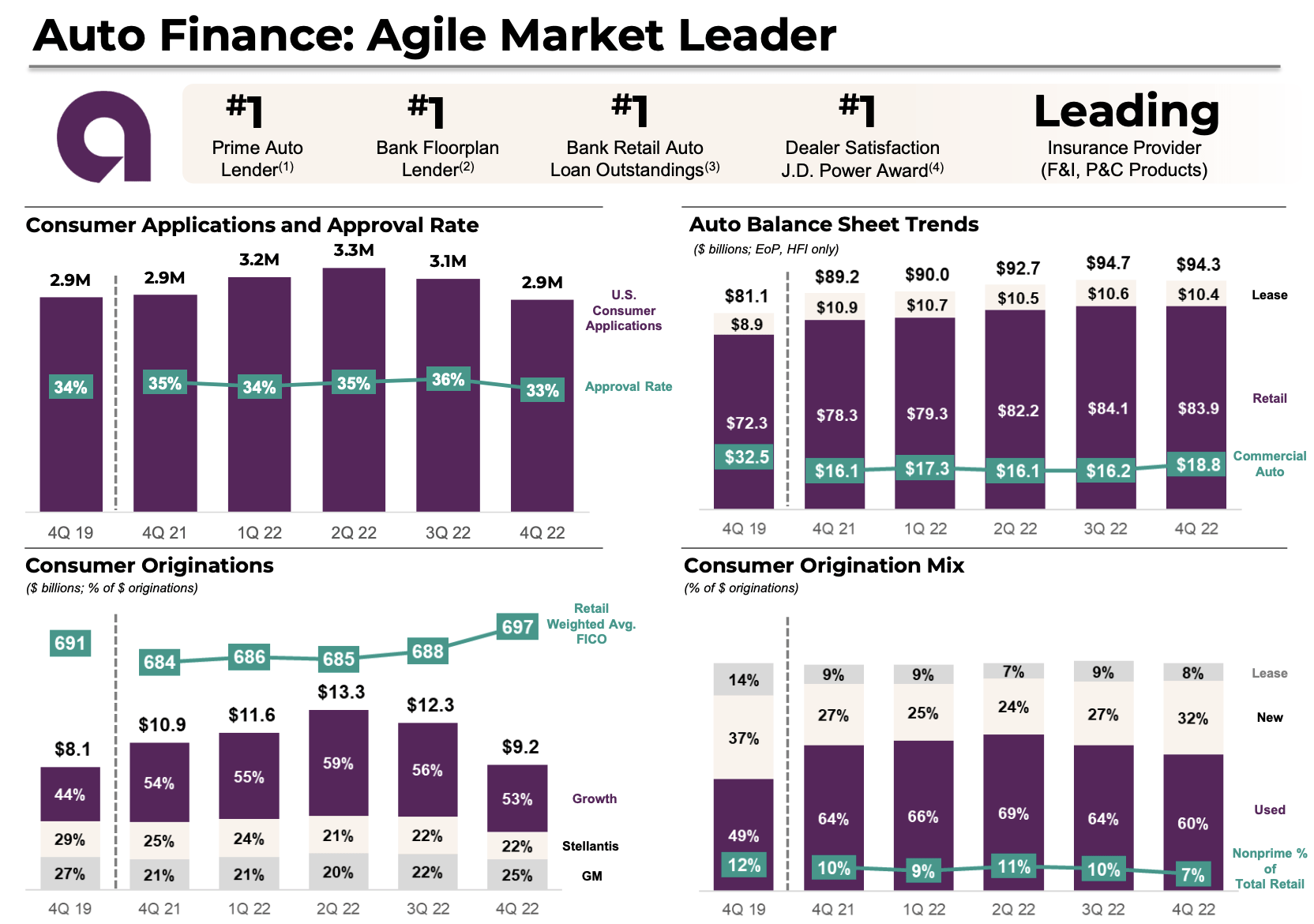

Ally Financial has $84 billion worth of retail auto loans on its balance sheet, which excludes $11 billion worth of leases and $17 billion worth of commercial auto loans.

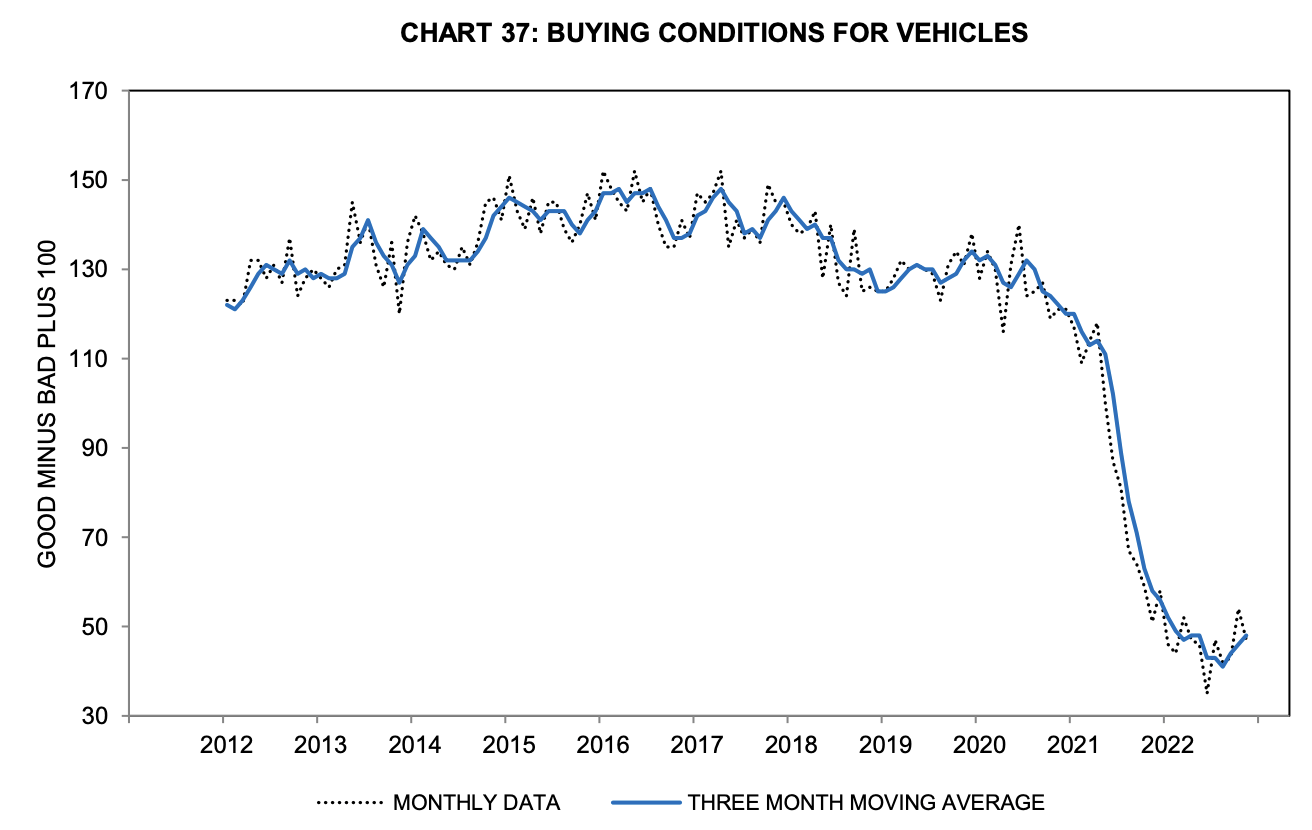

The chart below shows what buying conditions for vehicles look like. The toxic mix of macro headwinds caused affordability to implode. While we have seen some improvement, the situation remains dire.

University of Michigan

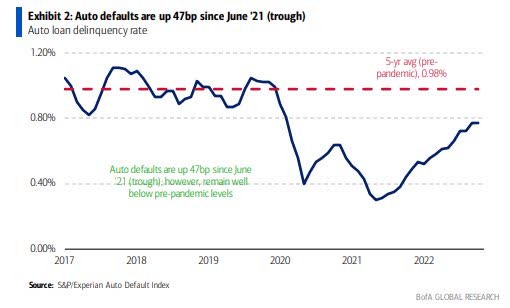

As a result, credit quality is also weakening. My friend and macro expert Disruptor Stocks shared a few charts with me that perfectly capture the bigger picture.

Auto defaults have steadily risen after government stimulus, and low rates pushed defaults to very low levels after the pandemic. Now, the uptrend is on its way to pre-pandemic levels close to 1.0%.

Bank of America

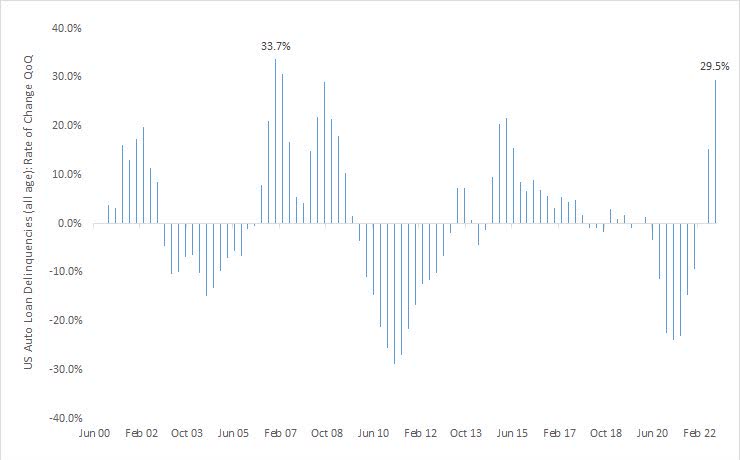

Even worse, the rate at which auto loan delinquencies rise has accelerated to multi-year highs. Again, delinquencies are subdued, but the trend goes in the wrong direction – and it’s gaining momentum.

DisruptorStocks

As of December 2022, the auto loan default rate is 0.87%.

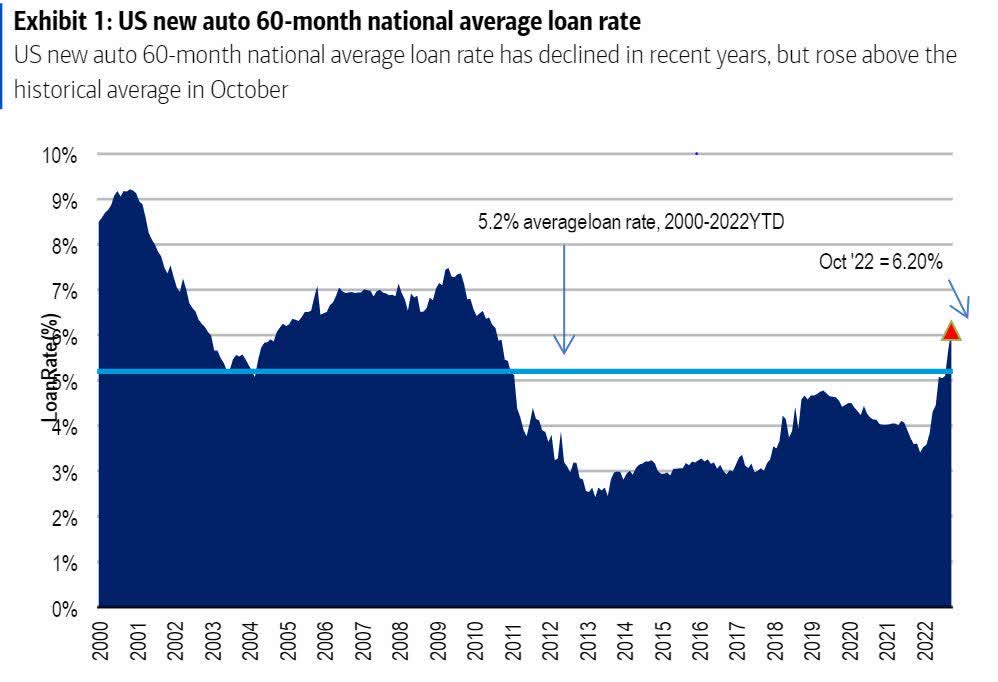

Not only are used car prices still elevated, but car buyers are also facing higher rates. In October, the average rate was 6.2%, which is now above the 22-year average.

Bank of America

According to LendingTree, the average monthly payment for a used car is $700. That’s 13.3% higher compared to 2021.

15.7% of consumers who financed a new vehicle in 4Q22 committed to a monthly payment of $1,000 or more. 17.4% of new vehicle sales with a trade-in had some negative equity in that quarter. That’s up from 14.9% in 4Q21.

These numbers are truly stunning and bad news for financing companies. According to automotive expert and industry insider CarDealershipGuy:

Softening prices and negative equity means trouble for banks bringing the wave of missed payments and repossessions, so financial institutions tighten their credit policies. Cox reports that access to credit tightened in December on most channels except for certified pre-owned (CPO).

Lenders need to make money, and some are taking advantage of vulnerable customers. Credit Acceptance Corp is sued by New York, accused of knowingly writing thousands of loans to low-income individuals that could not have afforded repaying them. As I wrote in my previous newsletter, some lenders are playing with the debt-to-income ratio or are dropping the existing auto loan stipulation to squeeze customers into approvals.

So, what does all of this mean for ALLY?

Ally’s 4Q22 Results

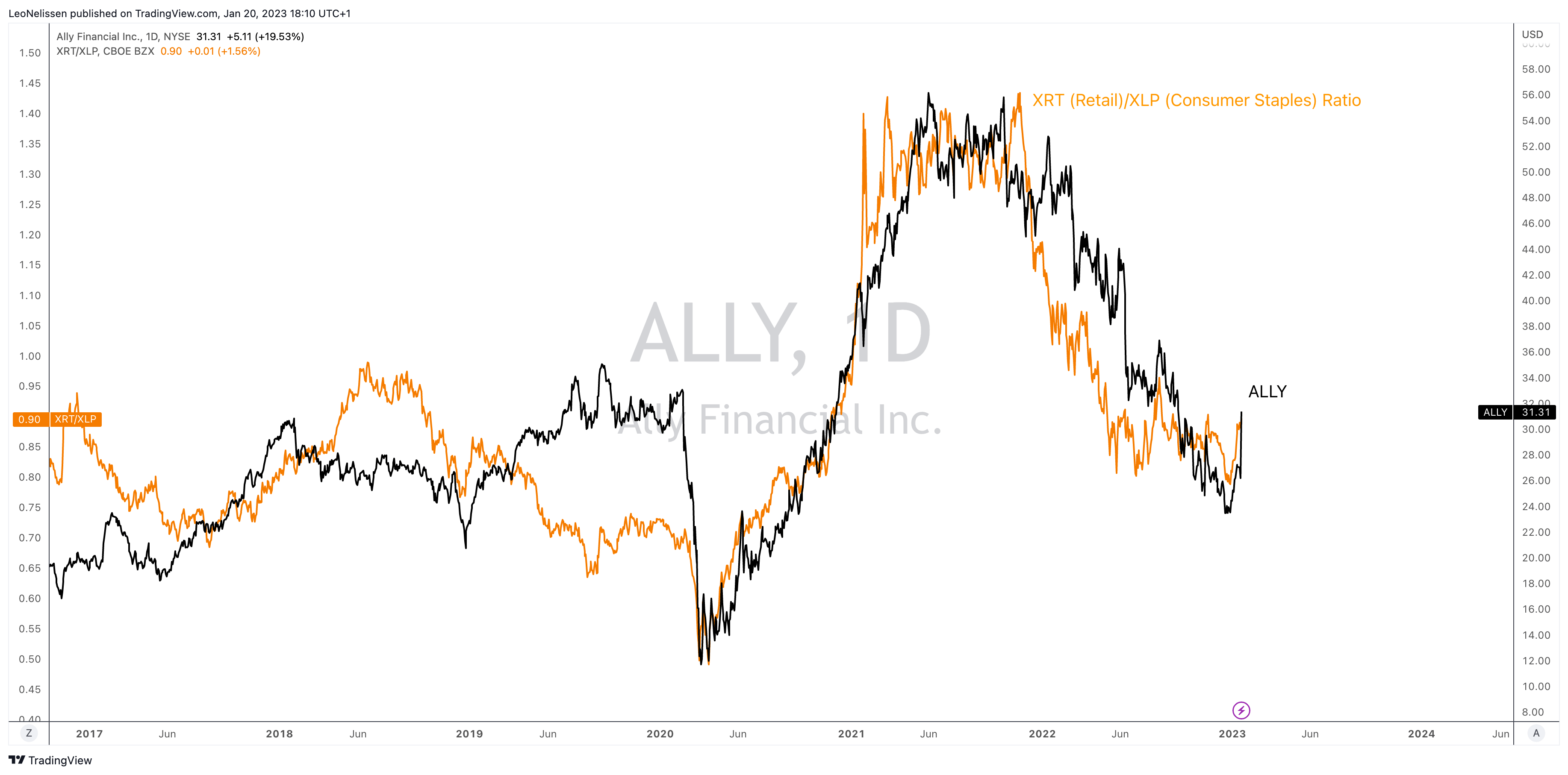

First of all, the slump in Ally’s stock price wasn’t caused by mismanagement or something similar. I made the chart below to visualize this. The orange line displays the ratio between retail stocks (XRT) and consumer staples (XLP). A rising line means that retail companies are outperforming. It’s a good proxy for sentiment in the consumer space. The black line shows ALLY’s stock price.

TradingView (XRT/XLP, ALLY)

ALLY was the victim of rapidly deteriorating sentiment, fueled by terrible headlines that just keep getting worse.

Hence, it helps that ALLY just beat earnings estimates, showing that it’s doing much better than expected. That warrants a higher valuation.

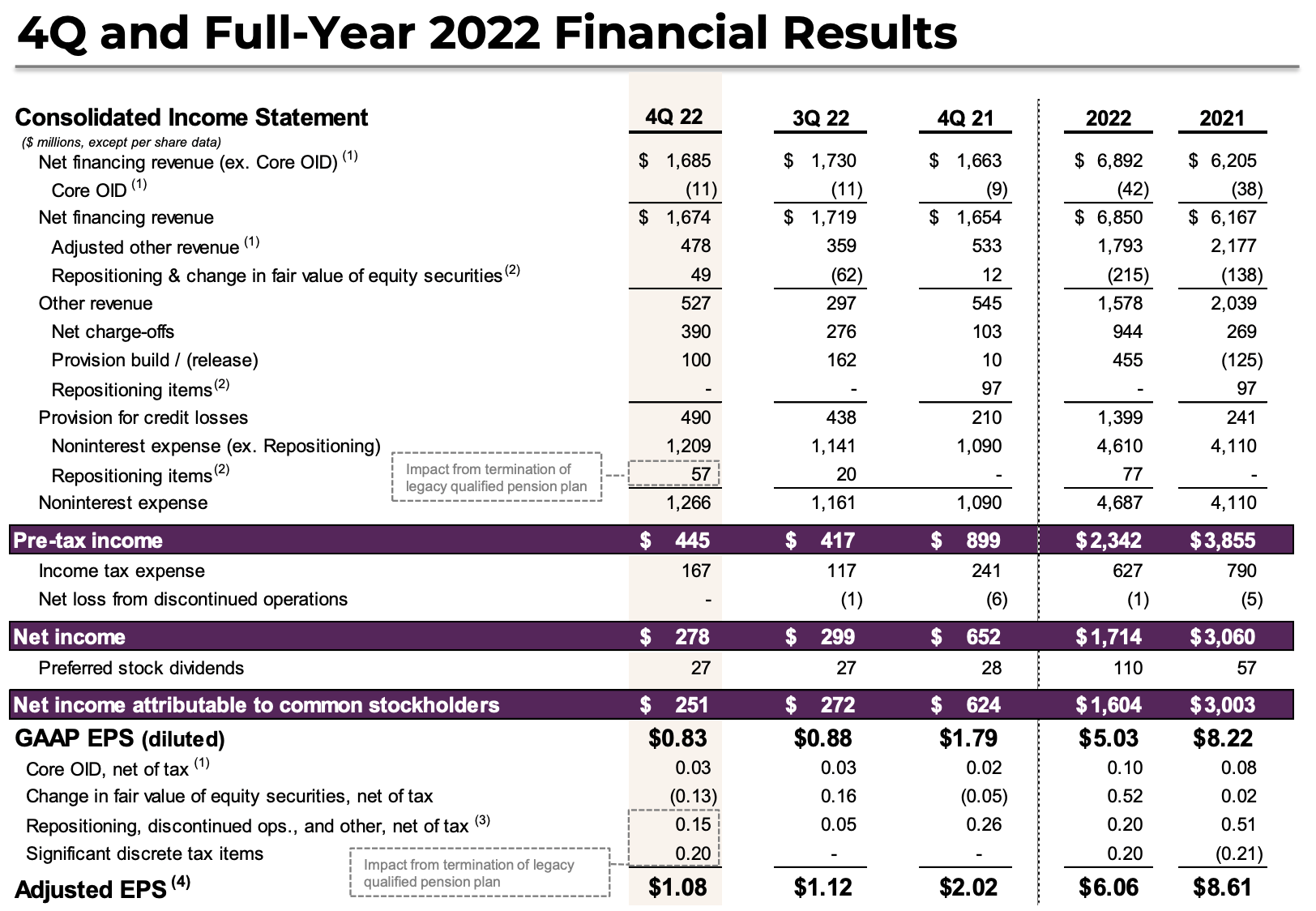

In 4Q22, ALLY reported $2.2 billion in revenue. That’s flat versus 4Q21 and $140 million higher than expected. Non-GAAP EPS came in at $1.08, which is $0.07 above consensus estimates.

In 4Q22, net financing revenues were stable, falling by just 2.6%. Other revenue improved to $527 million thanks to higher “other” revenues and rebounding values in repositioning & change in fair value of equity securities.

Ally Financial

So far, so good. When it comes to credit quality, we see a deterioration, as net charge-offs increased by 41% to $390 million.

According to the company:

Provision for credit losses increased $280 million to $490 million compared to the prior-year quarter due to continued normalization in credit as well as modest reserve build to support asset growth and changes in macroeconomic assumptions.

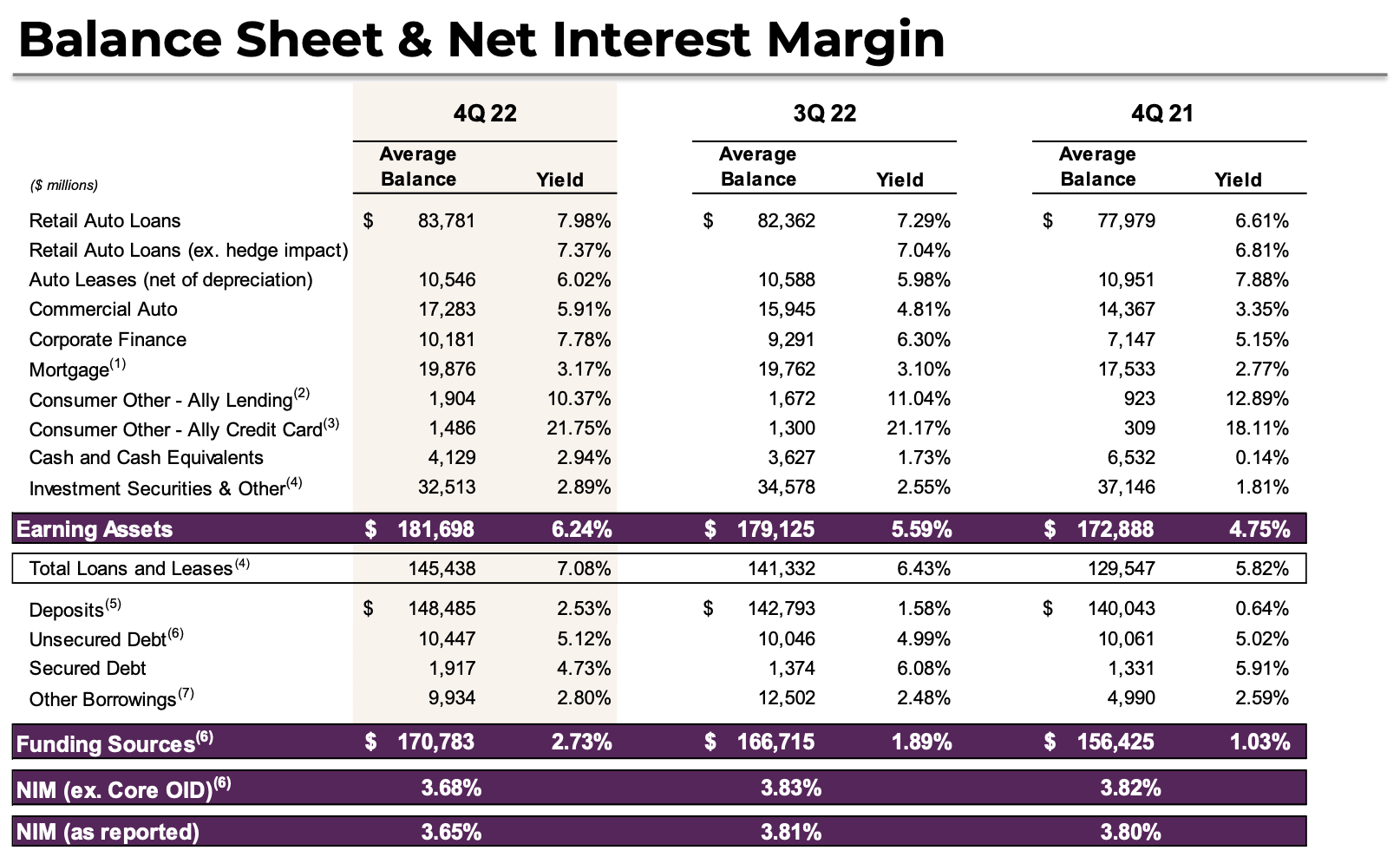

In its fourth quarter, the company added more than $1.4 billion in retail auto loans. These loans have a yield of 8.0%, which pushes the company’s average yield on earning assets to 6.2%. On funding, it pays 2.7%, resulting in a net interest margin of 3.7%. This is down from 3.8% in the prior quarter, as the rise in funding costs outperformed the rise in earning yields.

Ally Financial

The company expects retail auto yields to remain high, averaging 9% in 2023. The estimated originated yield on retail auto loans was 9.6% in 4Q22. The portfolio yield, including hedges, was 8.0%

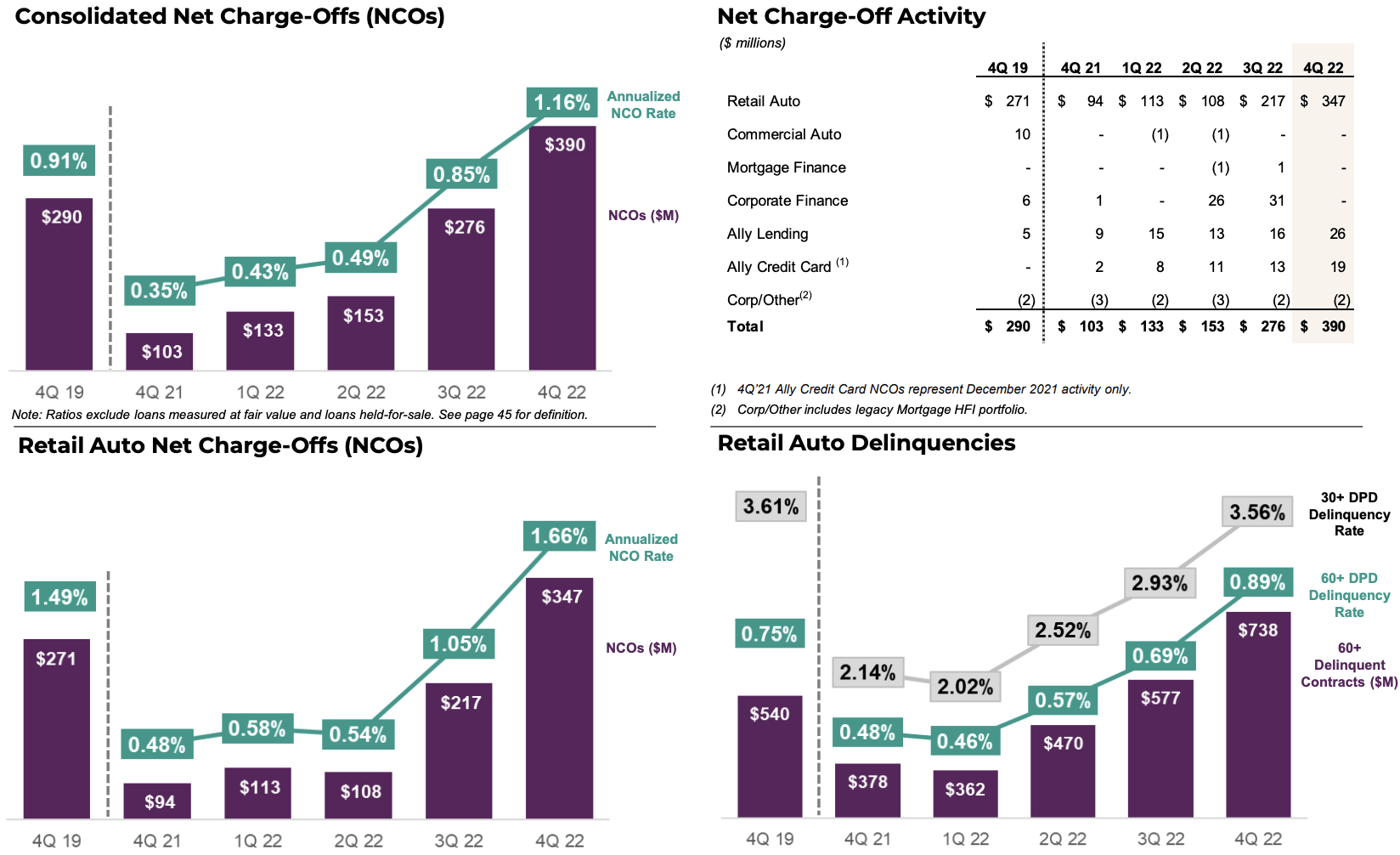

Going back to asset quality, the company’s net charge-offs increased to $390 million, as we already briefly discussed. The annualized NCO rate is now 1.16%. At the end of 2019, that number was 0.91%.

$347 million worth of NCOs came from the company’s retail auto lending activities. In that area, the NCO rate hit 1.7%. In 4Q19, that number was 1.5%. In other words, while we’re seeing a rising uptrend with strong momentum, we are not yet seeing alarming numbers. The same goes for the 30+ DPD delinquency rate, which came in at 3.6%. This ratio is back at 2019 levels.

Ally Financial

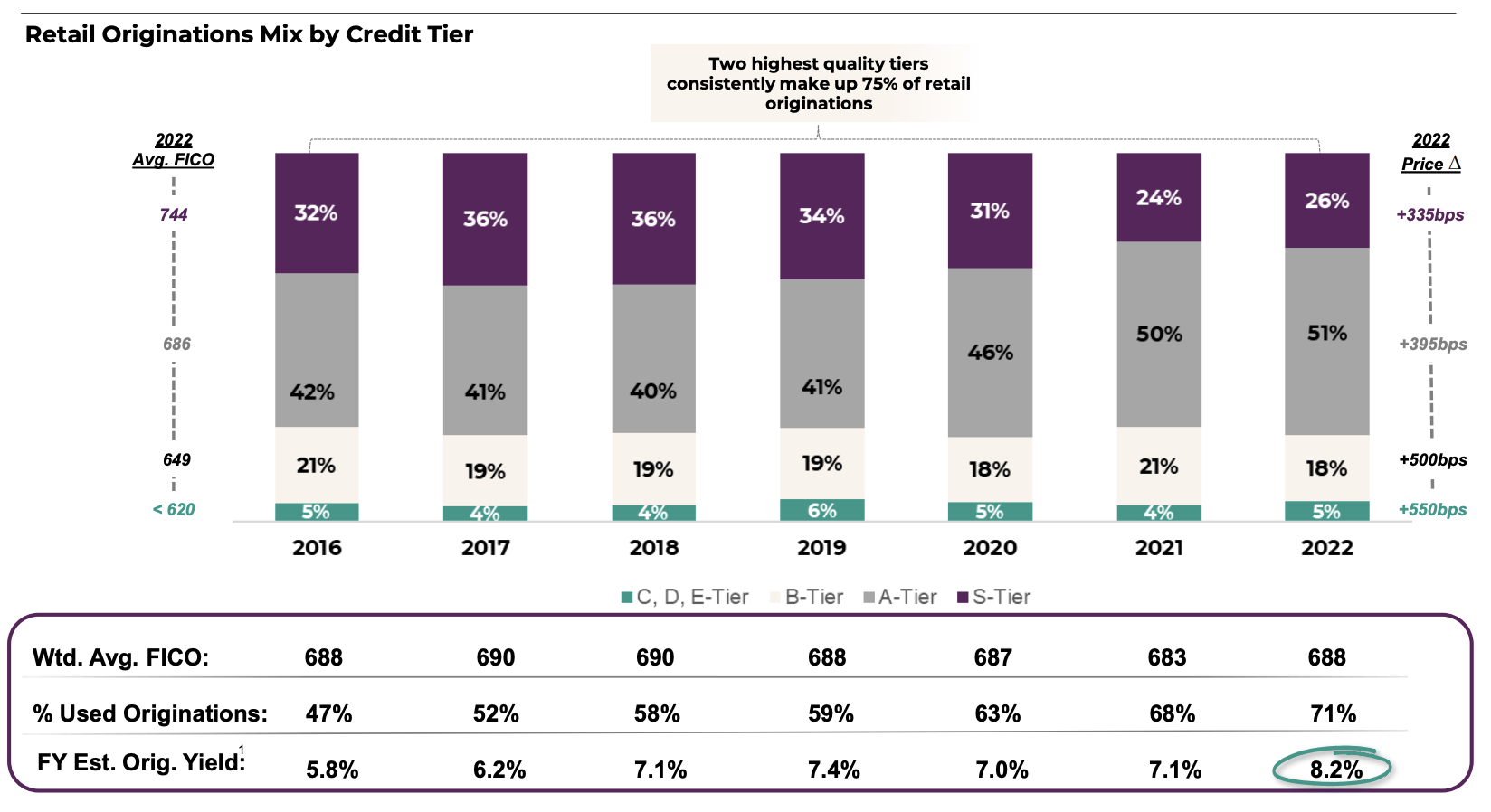

It’s also worth noting that lending in other areas enjoys high credit quality and the fact that auto lending has gone from 96% of total lending in 2014 to 77% in 2022.

The retail auto coverage ratio remains at 3.6% due to $3.0 billion in reserves. The company did not increase these reserves.

It also needs to be said that financial corporations like ALLY have learned a valuable lesson in the past. Like most major (regional) banks, all eyes have been on credit quality. People with poor credit have been pushed to other, smaller providers. ALLY customers, for example, have a weighted average FICO score of 688. That number has remained fairly consistent over the past seven years.

Ally Financial

Overall, these numbers aren’t half bad. Given macroeconomic fundamentals, I had expected much worse results.

Another Reason Why ALLY Rallied

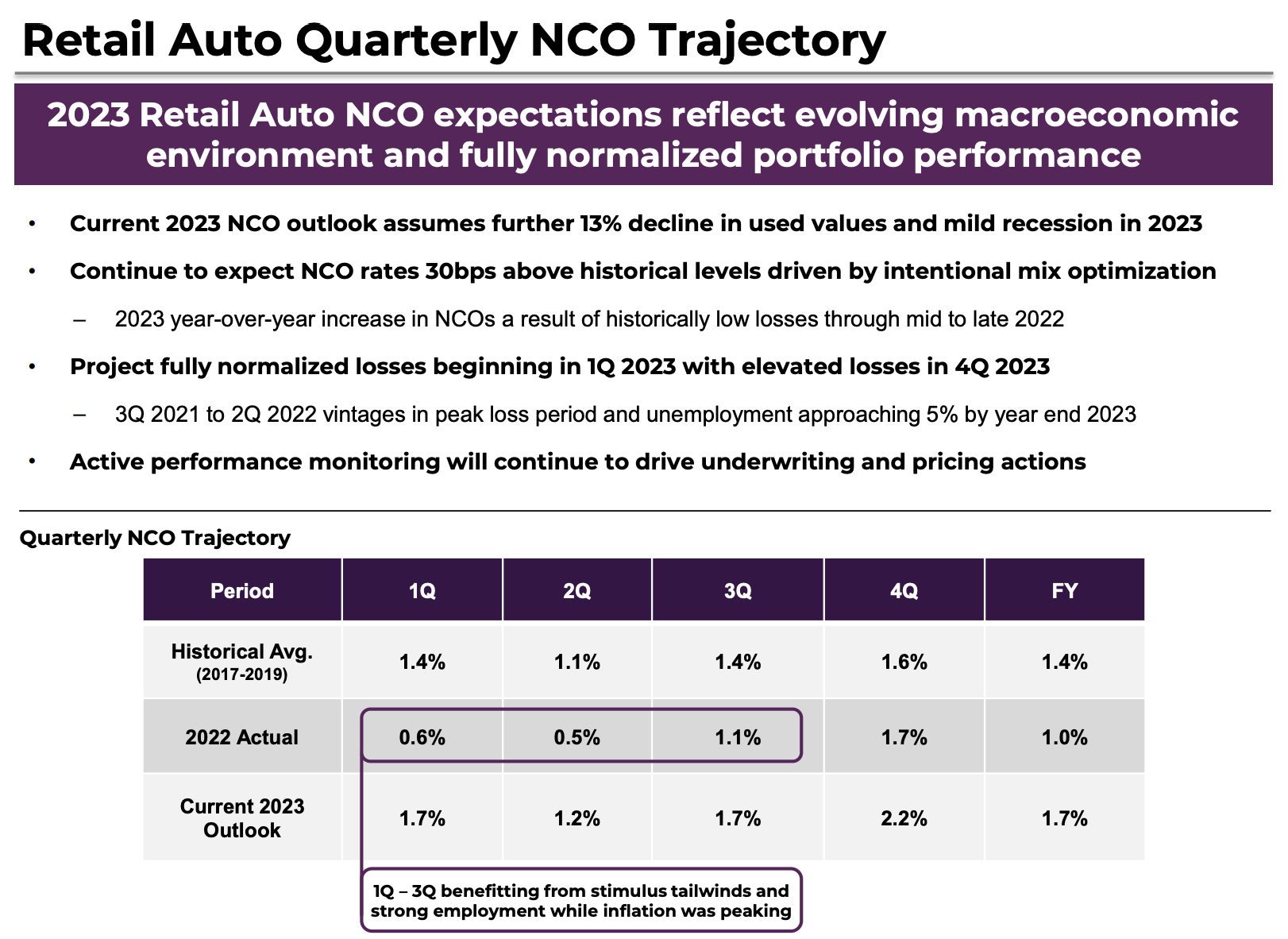

The outlook Ally Financial gave was far better than market participants may have expected. The company expects net charge-off rates to be 1.2% to 1.4% in 2023 and 1.3% in 2024. This would imply that these numbers are in a topping process, not accelerating with higher momentum.

For auto retail, net charge-offs are expected to be 1.6% to 1.8% this year and 1.6% in 2024.

For these estimates, the company uses an unemployment peak number of 5% and a 13% decline in used vehicle values.

ALLY also expects net interest margins to increase to 3.5% in 2023, with an upside to at least 3.75% in 2024.

The company’s base case is a “mild” recession. This is what most banks predict as well.

Ally Financial

According to the company (note that it expects a terminal Fed rate of 5.0%):

We continue to expect near-term compression and NIM to trough around 350 basis points, assuming the forward curve and a Fed funds peak of 5%. In retail auto, we added 395 basis points of price into the market in 2022 and are currently originating loans in the 10% range. On the deposit side, our OSA pricing has moved up 280 basis points as of year-end. So prices in retail auto were 115 basis points in excess of what we passed through on OSA.

It also helps that the company continues to maintain a healthy capital ratio, allowing for higher shareholder distributions.

In 2022, we executed $1.7 billion of share repurchases as we continue to normalize excess capital. Additionally, we announced a dividend of $0.30 per share for the first quarter. We remain disciplined in our capital allocation and currently maintain $3.6 billion of CET1 in excess of our SCB requirements. Our priorities remain focused on maintaining prudent capital levels amid continued uncertainty while investing in our businesses and supporting our customers.

Valuation

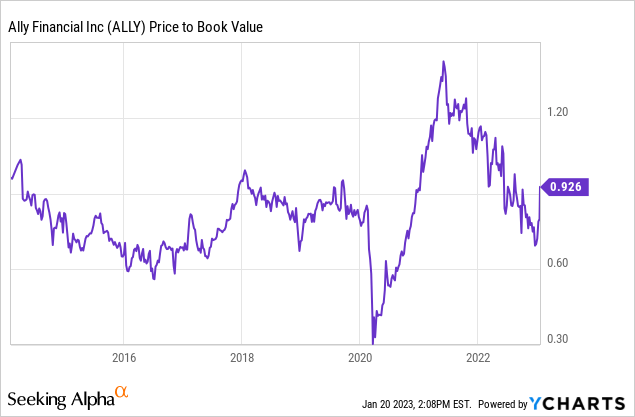

A lot of pessimism has been priced in. Looking at the chart below, ALLY shares usually trade close to 1x book value.

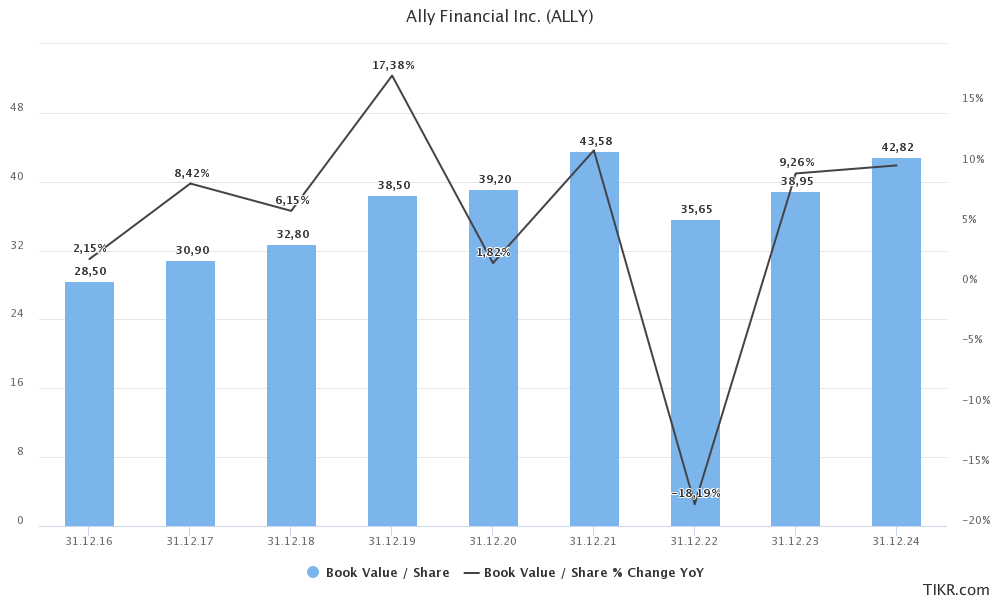

Looking at consensus estimates, we see that 2023 is expected to see a rebound of 9% to $39 per share. 2024 could see a return to pre-crisis levels.

TIKR.com

As we discussed in the introduction, we’re now at a crossroads.

- The Fed will indeed achieve a soft landing, allowing the economy to avoid anything worse than a “mild” recession. In that case, ALLY would be significantly undervalued with room to rise to $40-$50 per share.

- Ongoing credit and macroeconomic fundamentals continue to fall in a scenario where the Fed continues to hold rates close to (or above) 5.0%. In that scenario, this rally turns into another selling opportunity before the stock continues its downtrend.

I believe that ALLY needs to be avoided. While the company is handling things better than expected, I believe that auto fundamentals will end up being worse than expected, triggering a new stock price decline towards $25 and lower.

Takeaway

In this article, we started by discussing automotive credit fundamentals. While we’re not in a dire situation yet, we witness accelerating momentum in the wrong direction. Default rates are rising as affordability remains a big issue despite falling car prices. General economic weakness is not helping here either. The same goes for the Fed’s need to maintain high rates to not only lower inflation but also keep it down close to 2%.

ALLY’s financials were much better than expected. Credit quality was good and loan growth was satisfying. The outlook was even better, as it took away a lot of fears that industry fundamentals might be spiraling out of control.

While I agree with the post-earnings stock price surge, I do not recommend investors chase this rally. Given my view on economic fundamentals, I remain cautious – especially when it comes to auto loans.

(Dis)agree? Let me know in the comments!

Be the first to comment