cofotoisme

A Quick Take On Alkami Technology

Alkami Technology (NASDAQ:ALKT) went public in April 2021, raising approximately $180 million in gross proceeds in an IPO that priced at $30.00 per share.

The firm provides cloud-based digital banking software to financial institutions in the United States.

I’m on Hold for ALKT until management can make a meaningful move toward operating breakeven.

Overview

Plano, Texas-based Alkami was founded to develop a platform that improves financial institution user interfaces and integrates with various banking functions and processing systems.

Management is headed by president and CEO Alex Shootman, who has been with the firm since November 2021 and was previously CEO of Workfront, an enterprise application platform and before that, was President of Apptio.

The company’s primary offerings include:

-

User experience

-

Integrations

-

Data insights

The firm pursues client relationships with community, regional and super-regional financial institutions via a direct sales and marketing approach.

ALKT says its typical sales cycle is from 3 – 12 months and a subsequent implementation time range of 6 – 12 months.

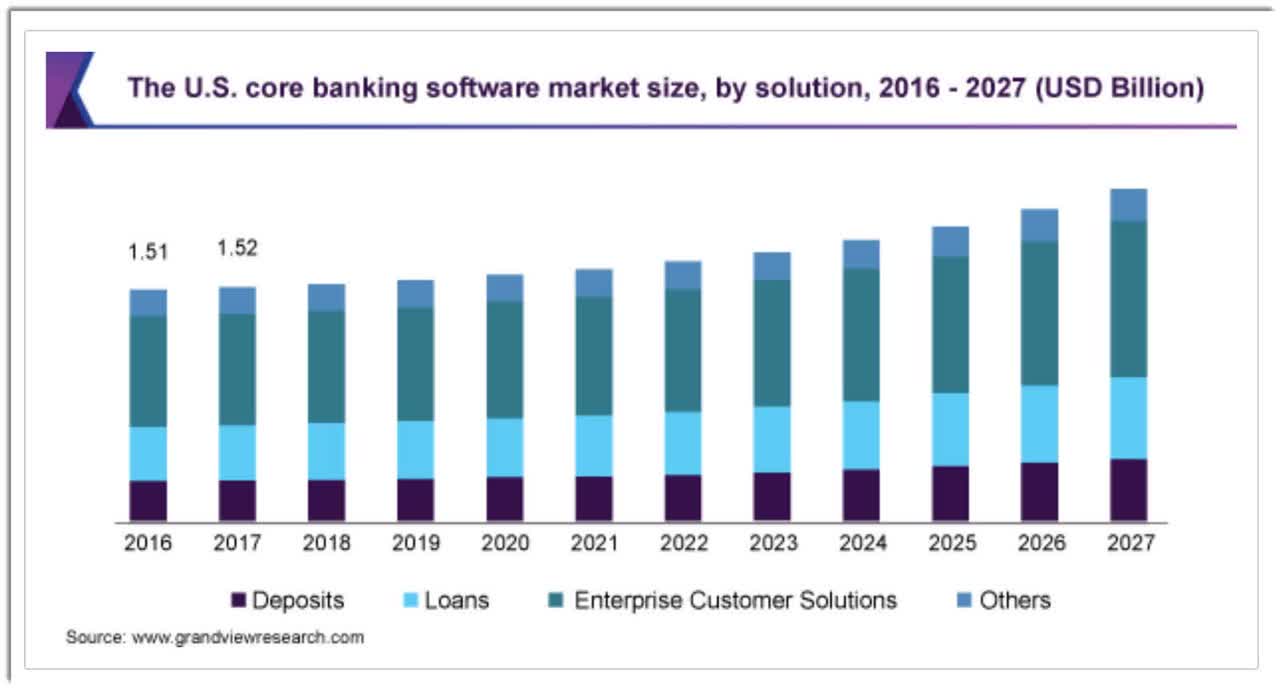

Market & Competition

According to a 2020 market research report by Grand View Research, the global market for core banking software was an estimated $9.4 billion in 2019 and is expected to reach $17 billion by 2027.

This represents a forecast CAGR of 7.5% from 2020 to 2027.

The main drivers for this expected growth are the growing demand from customers for advanced banking solutions across numerous touch points and devices.

Also, the U.S. core banking software market history and projected future growth trajectory is shown in the chart below:

U.S. Core Banking Software Market (Grand View Research)

Major competitive or other industry participants include:

-

NCR Corporation

-

Q2 Holdings

-

Temenos AG

-

Fiserv

-

Jack Henry and Associates

-

Fidelity National Information Services

Recent Financial Performance

-

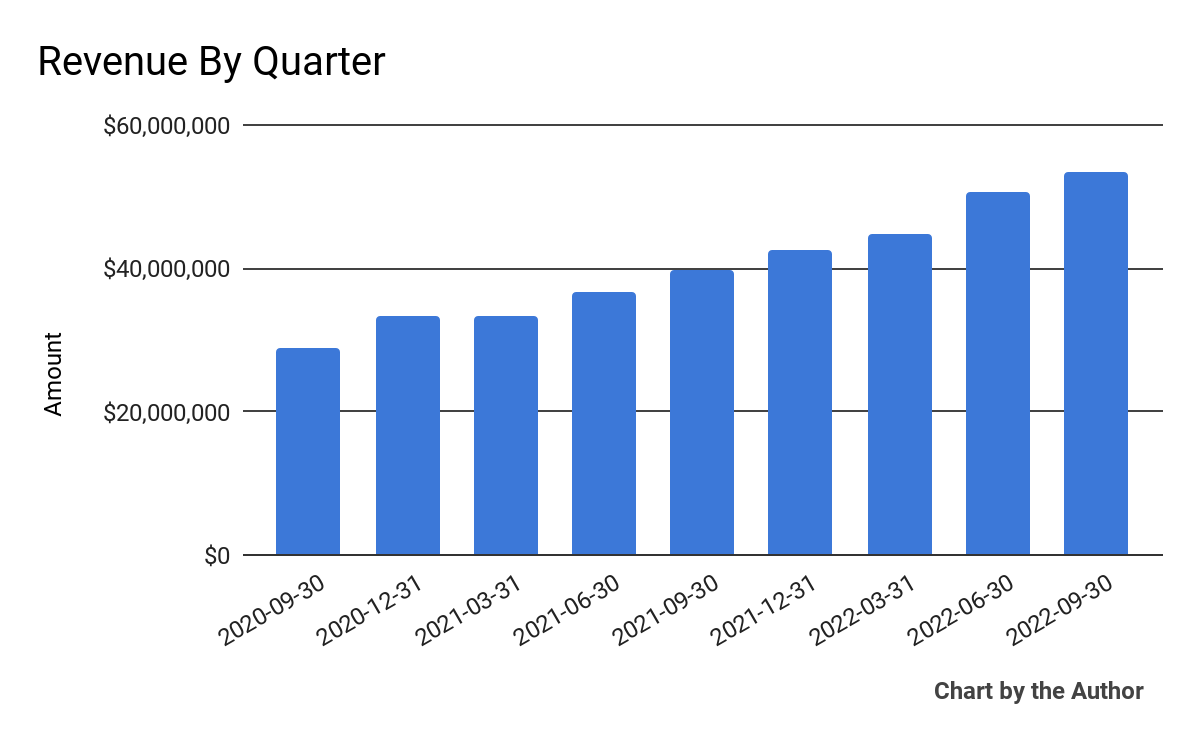

Total revenue by quarter has risen per the following chart:

9 Quarter Total Revenue (Financial Modeling Prep)

-

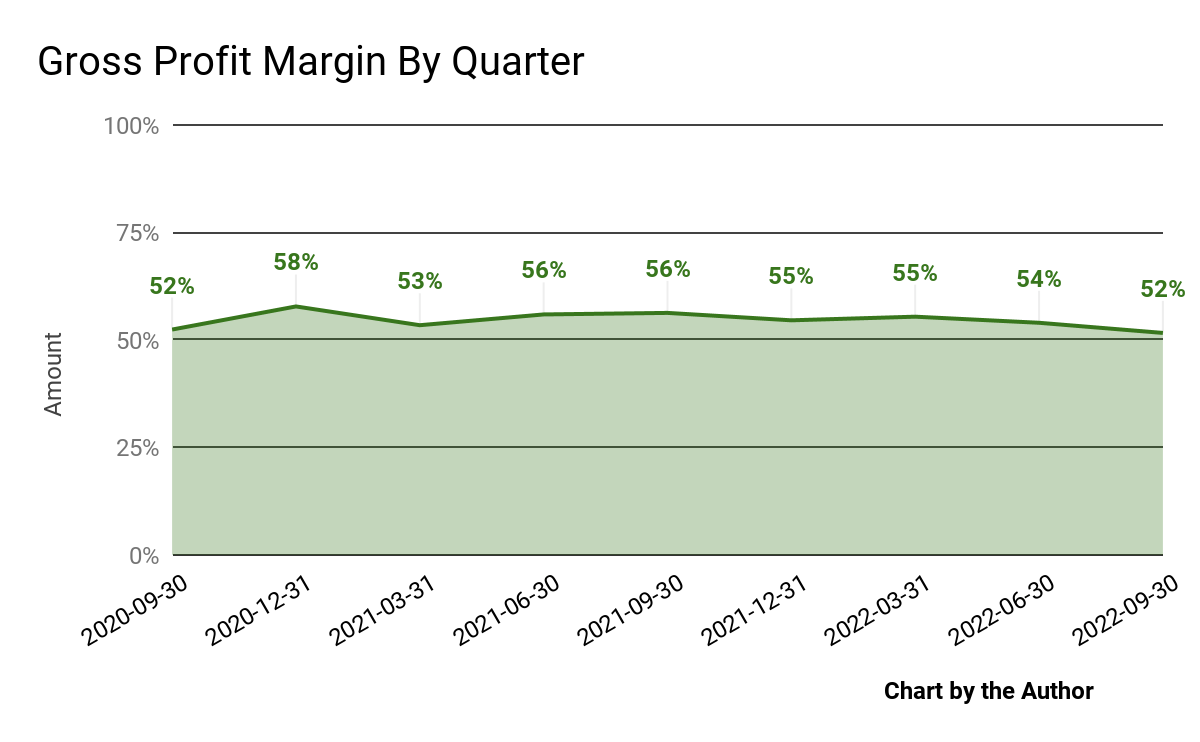

Gross profit margin by quarter has dropped somewhat in recent quarters:

9 Quarter Gross Profit Margin (Financial Modeling Prep)

-

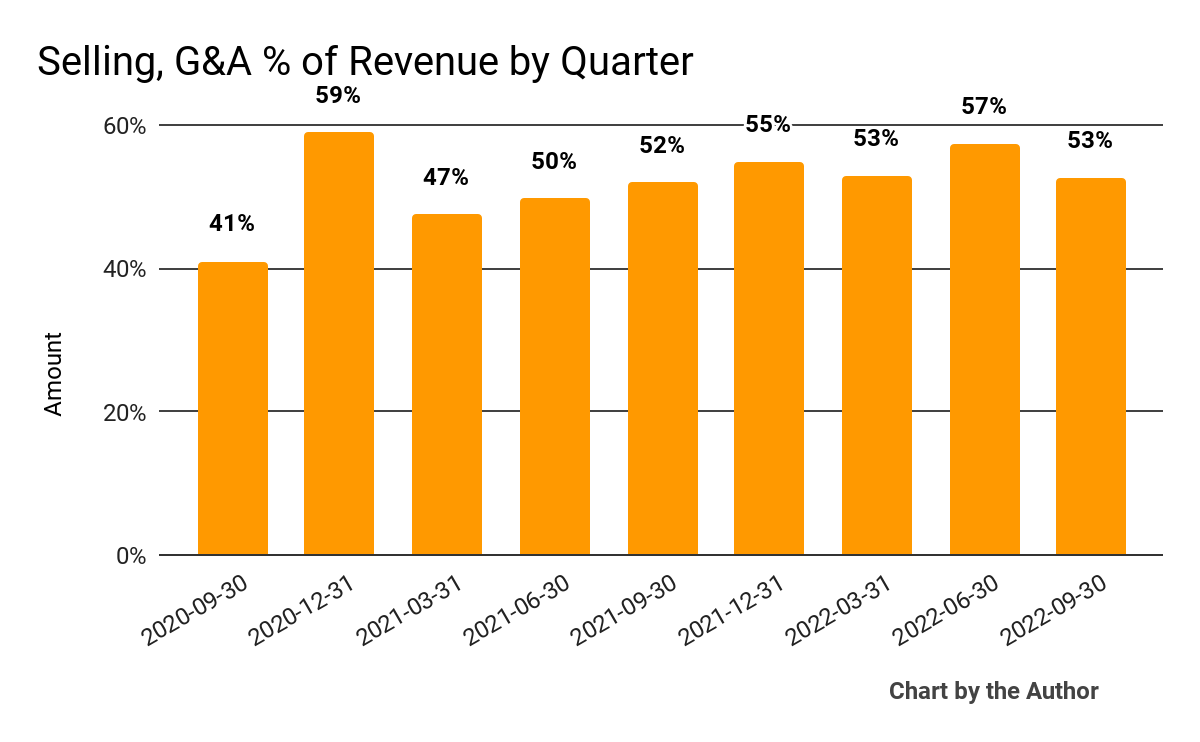

Selling, G&A expenses as a percentage of total revenue by quarter have trended higher recently:

9 Quarter Selling, G&A % Of Revenue (Financial Modeling Prep)

-

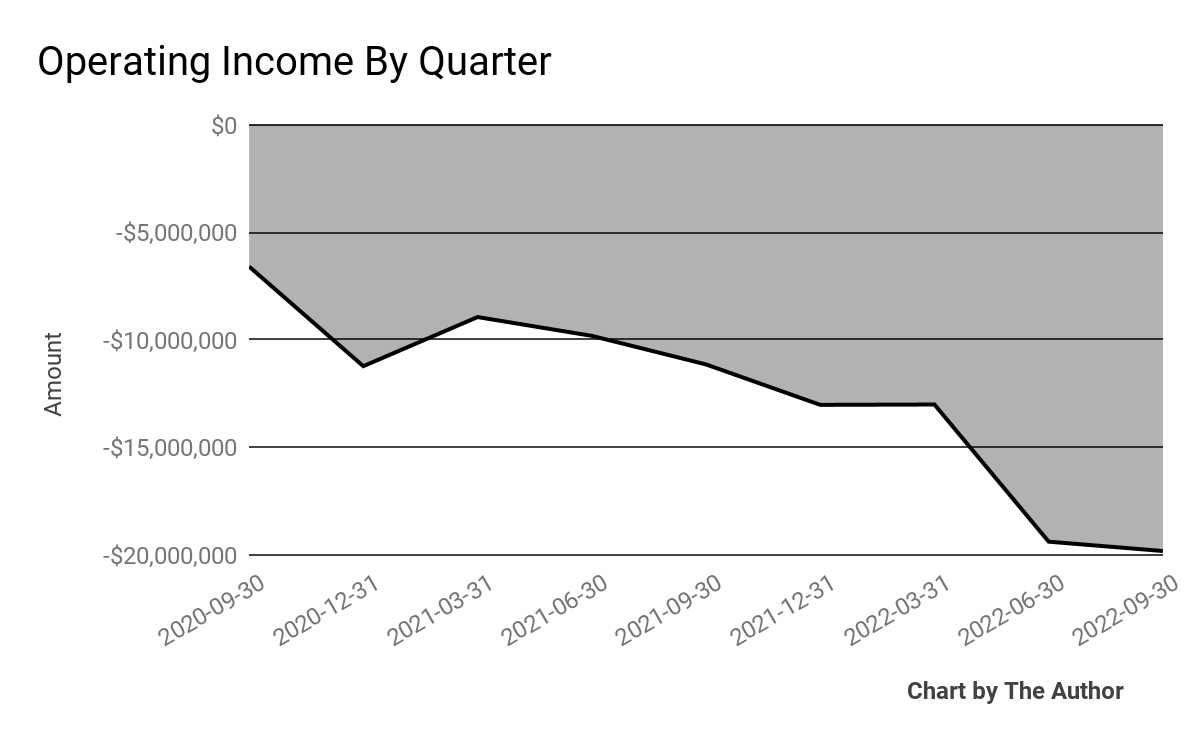

Operating losses by quarter have worsened markedly in recent reporting periods:

9 Quarter Operating Income (Financial Modeling Prep)

-

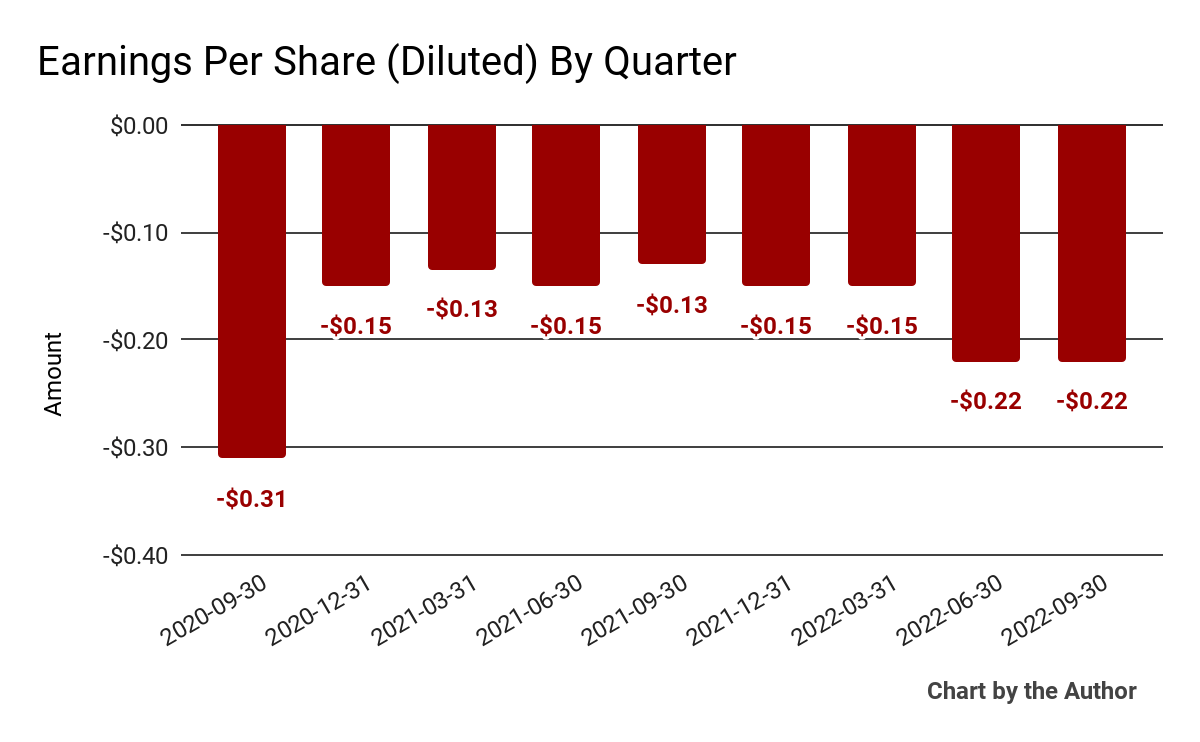

Earnings per share (Diluted) have remained substantially negative, worsening in recent quarters:

9 Quarter Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP)

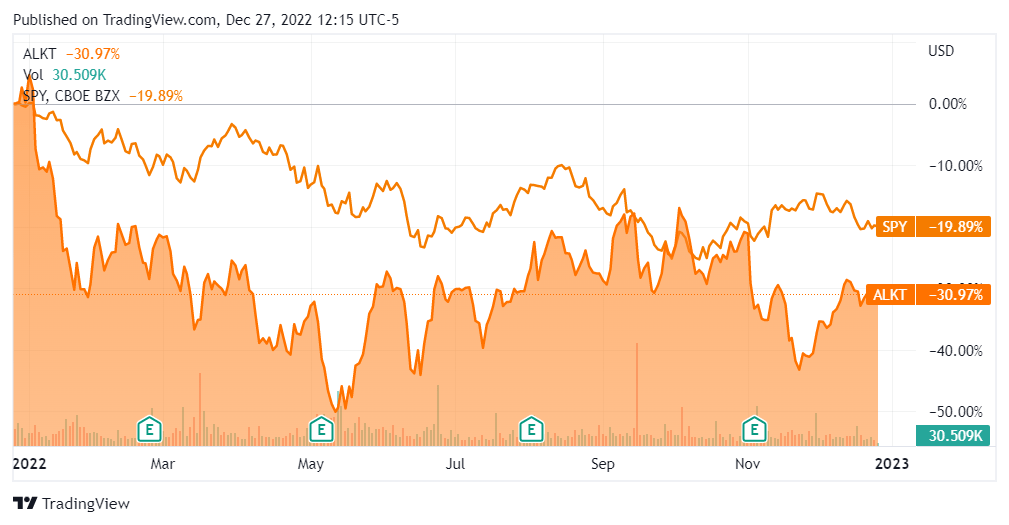

In the past 12 months, ALKT’s stock price has dropped 31.1% vs. the U.S. S&P 500 index’s drop of around 19.8%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

6.4 |

|

Enterprise Value / EBITDA |

-21.3 |

|

Revenue Growth Rate |

33.6% |

|

Net Income Margin |

-35.1% |

|

GAAP EBITDA % |

-30.2% |

|

Market Capitalization |

$1,245,930,360 |

|

Enterprise Value |

$1,229,806,041 |

|

Operating Cash Flow |

-$36,202,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.74 |

(Source – Financial Modeling Prep)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

ALKT’s most recent GAAP Rule of 40 calculation was just 3.5% as of Q3 2022, so the firm is in need of significant improvement in this regard, per the table below:

|

Rule of 40 – GAAP |

Calculation |

|

Recent Rev. Growth % |

33.6% |

|

GAAP EBITDA % |

-30.2% |

|

Total |

3.5% |

(Source – Financial Modeling Prep)

Commentary On Alkami Technology

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the growth of its user base, reaching “13.7 million live registered users on the Alkami platform, up 2.3 million users compared to the prior year.”

Leadership noted that customers have shifted their need to attracting deposits, so are investing in improved digital onboarding experiences.

The firm believes the challenging macroeconomic conditions will increase demand, with evidence that its sales pipeline is ‘stronger than at any point in our history.’

As to its financial results, total revenue rose 34% year-over-year, exceeding expectations.

The company’s gross retention rate was 97%, ‘measured in terms of ARR and digital users retained over the last 12 months.

The firm grew revenue per user [RPU] by 15%, to $15.57, with the Segmint acquisition expanding its RPU by nearly half of the 15% growth.

ALKT’s Rule of 40 results have been disappointing, with significant and growing operating losses contributing to a poor figure for this metric.

Gross profit margin dropped due to “investment in post-sell activities necessary to support [its] significant implementation backlog…from [its] MK Decision acquisition.”

However, SG&A expenses as a percentage of revenue continue to trend higher, and operating losses and negative earnings per share have worsened sharply in recent quarters.

For the balance sheet, the firm finished the quarter with $208.9 million in cash, equivalents and short-term investments and $84.5 million in total debt.

Over the trailing twelve months, free cash used was $37.4 million, of which capital expenditures accounted for $1.2 million in cash use.

Looking ahead, management raised its full-year guidance to $203.5 million in revenue at the midpoint of the range and an adjusted EBITDA loss of $18.1 million at the midpoint.

‘Adjusted’ figures usually exclude stock-based compensation, which in the case of ALKT over the past 12 months totaled $40.3 million.

Regarding valuation, the market is valuing ALKT at an EV/Sales multiple of around 6.4x.

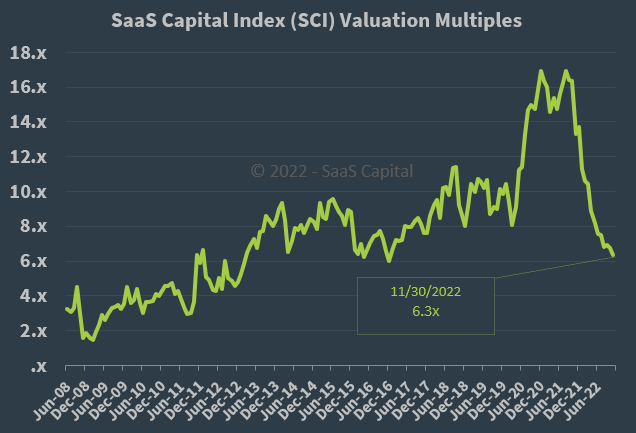

The SaaS Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 6.3x on November 30, 2022, as the chart shows here:

SaaS Capital Index (SaaS Capital)

So, by comparison, ALKT is currently valued by the market at a slight premium to the broader SaaS Capital Index, at least as of November 30, 2022.

The primary risk to the company’s outlook is an increasingly likely macroeconomic slowdown or recession, which may accelerate new customer discounting, produce slower sales cycles requiring more prospect executive sign-offs and reduce its revenue growth trajectory.

A potential upside catalyst to the stock could include increased demand for improved deposit attraction technologies by financial institution prospects.

Given the firm’s increasing operating losses despite revenue growth and management’s assertion that a slowing macroeconomic environment helps push customer demand through a need for increasing deposits, the market is punishing money-losing stocks like ALKT.

I’m therefore on Hold for ALKT until management can make a meaningful move toward operating breakeven.

Be the first to comment