Anton Vierietin/iStock via Getty Images

Article Thesis

Alibaba (NYSE:BABA) continues to see its shares fall, mainly due to China-centered macro risks, whereas company-specific news isn’t bad. We’ll look at some of the items impacting Chinese equity markets and at what Alibaba’s potential looks like going forward.

Alibaba Drops Further On China Worries

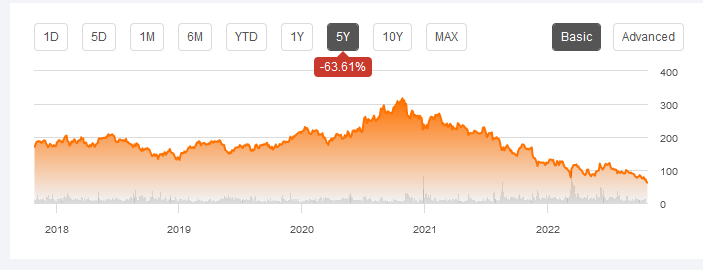

On Monday, Alibaba saw its shares slump to a new five-year low:

Seeking Alpha

With a 5-year performance of minus 64%, and now trading around 80% below the all-time high, Alibaba has been a very bad performer in recent years. The steep share price drop on Monday was caused by broad selling in Chinese equities, which also took down the shares of companies such as Tencent (OTCPK:TCEHY), NIO (NIO), XPeng (XPEV), Li (LI), Weibo (WB), JD (JD), and so on.

The factors that caused this selling of Chinese equities include the developments around the Communist Party’s congress over the weekend. China’s President Xi Jinping was awarded a third term, and he made moves to further strengthen his power in the country. This included the fact that Xi’s predecessor was escorted out of the event, a move that was seen as an affront by many and as a warning from Xi to potential rivals by some. Overall, the events from the weekend’s congress were interpreted as China becoming more open about the country being under almost complete control of President Xi. This stoked fears in the West that an investment in Chinese equities could be even more risky than previously thought – after all, when not even high-ranking party members such as Hu Jintao are off-limits, what might Chinese leadership do to companies that do not act the way the country’s leadership wants? There is some merit to that thought, I believe, as politics definitely are a key risk for Chinese companies such as Alibaba. Then again, I do not believe that hurting these companies is in the best interest of China and its leadership – after all, China benefits from the jobs these companies create, from the taxes they pay, from their R&D spending that allows for technological progress in China, and so on.

There also was another China-specific news item, as the country’s currency, the Yuan, continues to weaken. This is not bad for Chinese companies per se, and it might actually help some of them as it makes Chinese exports cheaper, all else equal, thereby potentially making the products of Chinese companies more competitive in global markets. But for investors from outside of China, a weakening Yuan means that profits will be lower once translated to their currencies, all else equal. When the Yuan weakens versus the US Dollar, for example, US-based investors will see the company generate lower earnings per share once denominated in USD, even if results remain stable in the Chinese local currency. Since most of BABA’s revenues are generated in China, and thus in Yuan, the company is not really able to offset the impact of the weakening Yuan via its non-Chinese businesses, as those are too small to offset the hit.

There also was some positive news out of China, however. During the third quarter, China’s gross domestic product grew more than expected, even though it was the lowest reported growth rate in many years. Q3 GDP was up 3.9% year over year and quarter over quarter, beating estimates of ~3.5% growth both on a year-over-year and quarter-to-quarter comparison. Chinese GDP growth was driven by higher exports and industrial production primarily, which does not necessarily offer a direct benefit to Alibaba. But consumption rose as well, with retail sales up 2.5% year over year in real terms, with inflation already being accounted for. That suggests that Alibaba should have delivered at least some growth in its core business during the last couple of months. Analysts are currently predicting that revenue during the September quarter will be down 8% year over year, to $29 billion. Some of that can be explained by the aforementioned currency impact, as a better performance in local currencies is partially offset by a weakening Yuan, relative to the strong USD. But I nevertheless believe that there’s potential for Alibaba to beat estimates when it reports in mid-November, after all, Alibaba has a history of outperforming expectations – it has beaten revenue estimates in nine out of the last 12 quarters.

Alibaba: Risk Versus Reward

With a company such as Alibaba, it’s pretty clear that there are risks. The country’s political leadership may move against Alibaba or its key personnel, as it has done in the past, when Jack Ma came into conflict with politics. Regulators in China might also move against Alibaba – again, that has happened in the past, and Alibaba was forced to pay some fines. On the other hand, investors should consider that this is not a unique risk for Alibaba, as Western tech companies are regularly fined for all kinds of things as well, including in the US and Europe. Some of these fines have been larger than the largest fine BABA has had to pay so far, which was $2.8 billion in early 2021. As long as these fines do not occur all the time and as long as underlying profits remain high, they are not a company-threatening issue. Instead, one might even see these as a “cost of doing business”, both when it comes to BABA as well as when it comes to Alphabet (GOOG) (GOOGL), Amazon (AMZN), or Meta (META) and the fines they receive from time to time.

Alibaba is also subject to some other risks. If tensions between Taiwan and China would escalate, that would have a potentially enormous impact on the economies in these countries. As a consumer goods company, Alibaba obviously would be impacted. Then again, the market does not seem to price this risk into the stocks of Western, highly-exposed companies to a large degree – Tesla (TSLA) and Apple (AAPL) are highly dependent on their Chinese operations, and yet they trade at high valuations. It looks like the market is pricing Chinese equities as if trouble was a sure thing, whereas Western China-exposed companies are priced as if trouble was pretty unlikely, which seems like a disconnect.

All in all, we can summarize that Alibaba is not a low-risk stock. There are clear risks investors should keep an eye on. But even stocks with elevated risks can make for a solid investment as long as the potential return is large enough. In BABA’s case, there is hefty upside potential in case everything goes right.

Based on forecasts for the current year, Alibaba is trading for just 8.5x this year’s net profit right now. And that profit number will be suppressed due to the lockdowns China has been experiencing and due to China’s below-average growth this year. In a more normal environment, one can expect the Chinese economy to do a lot better, and BABA would arguably earn a lot more in such an environment. Alibaba is thus, not surprisingly, forecasted to earn around 50% more three years from now relative to what is expected for the current year. If one were to put a 15x earnings multiple on the forecasted $10.82 in earnings per share three years from now, one could get to a $162 share price – which would be up almost 170% versus the current share price of $61. A 15x earnings multiple isn’t demanding at all, at least in a normalized environment where domestic and geopolitical tensions are lower and where the Chinese economy is no longer impacted by lockdowns and other COVID measures. In fact, one could argue that BABA might even trade at more than 20x net profits in such an environment, as it has done in the past for long periods of time, and as many US-based tech companies have done and continue to do. But that wouldn’t even be needed for Alibaba to deliver highly compelling returns.

We can thus summarize that Alibaba is a stock with elevated risks, most of those being China-related macro risks instead of company-specific issues. At the same time, BABA offers a lot of return potential if things go right – or rather, if they don’t go too wrong. Even if BABA were to grow its EPS by just half the expected rate over the next five years, and even if the earnings multiple was at 12x three years from now, BABA could climb to $108, which would be far from a bullish scenario, and which would still allow for returns of more than 70% in a three-year time frame.

Takeaway

Alibaba continues to head lower and lower, as the market becomes more and more worried about the risks of investing in Chinese equities. These risks exist for sure, and should not be neglected. But it is also noteworthy that Chinese equities are priced for doom and gloom, whereas Western, very China-dependent stocks such as AAPL and TSLA continue to trade at very elevated valuations. The market is not pricing in doom and gloom in these stocks, which seems like a disconnect.

It is far from guaranteed that the risks Alibaba faces will hurt the company in the long run, and if things go right, BABA could deliver (very) elevated returns. In the current environment, it thus looks like a higher-risk/higher-return stock that may be right for some investors, depending on one’s risk tolerance.

Be the first to comment