Robert Way

Thesis

Alibaba Group Holding Limited (NYSE:BABA) is slated to report its FQ1’23 earnings release on August 4. BABA investors have been hammered (again) over the past month as the bears returned to haunt Chinese stocks. The delisting fears are back!

In our June downgrade (Hold rating), we cautioned investors that we noted significant selling pressure at its critical resistance zone ($125) and urged them to avoid adding at those levels. Despite the sharp recovery from its May lows, we were concerned that the market could use the bullish sentiments in June to attract buyers into a trap before digesting those gains.

Consequently, since our June article, BABA has significantly underperformed the SPDR S&P 500 ETF (SPY). As a result, it posted a return of -14.5%, against the SPY’s 11.06% gain over the same period.

The market has leveraged the recent pessimism astutely over its delisting risks and China’s increasingly tenuous GDP growth target to shake out weak hands. As a result, the market pessimism has presented investors with another opportunity to consider adding BABA again!

Therefore, we revise our rating on BABA from Hold to Buy. Notwithstanding, we caution investors that our price action analysis has yet to indicate any potential bear trap (indicating that the market decisively denied further selling downside) yet. Therefore, we are “front-running” the market in anticipation of robust buying support at the current levels to appear soon.

Delisting And GDP Growth Target Fears!

BABA slumped on July 29 as the US SEC added China’s e-commerce behemoth to its delisting list, which stunned the market.

However, are such headwinds new? Absolutely not. So, we urge investors not to overreact to such a move by the market to shake out weak hands. BABA got a boost recently as the company highlighted that it could seek a primary listing in Hong Kong, quelling fears of its delisting in the US. Furthermore, a primary listing in Hong Kong would enable Alibaba to leverage investors in mainland China to invest in its stock.

Citi’s (C) recent commentary was favorable of the move by Alibaba to seek a primary listing in Hong Kong. It emphasized (edited):

We view the move as positive given the continued overhang on ADRs from the threat of delisting. A smooth transition to the new primary listing could pave the wave for other companies that already have dual listings. We view this as an important sentiment shift to attract more capital and liquidity to Alibaba and other China Internet stocks over time. – Barron’s

Notwithstanding, KGI Asia (a leading Hong Kong brokerage firm) noted that the process could be more complex than what investors assessed. Accordingly, it accentuated (edited):

On top of earnings concerns, there are some worries that the listing timetable for Ant might be delayed by Jack Ma’s decision to give up his control over Ant Group. It’s hard for A-share companies to obtain approval if there is a change in key shareholding structure within three years. – Bloomberg

Furthermore, the market could also have been spooked by the language used by the Chinese government after its recent Politburo (China’s highest decision-making body) meeting, chaired by Chinese President Xi Jinping.

The language in its statement suggested that Xi Jinping seems to be moving away from trying to maintain its 5.5% GDP growth target, which economists have emphasized for months is improbable. Bloomberg reported (edited):

China’s top leadership gave a downbeat assessment of economic growth but didn’t announce new stimulus policies at a key meeting. It stated the country should achieve “the best outcome” possible for economic growth this year while sticking to a strict Covid Zero policy. There was no mention of the national economic goals as there was at the April meeting, suggesting the government is downplaying the target of “around 5.5%” growth for this year that most economists think is impossible after a slump last quarter. – Bloomberg

Investors Could Be Concerned With A Downbeat Q1 Earnings

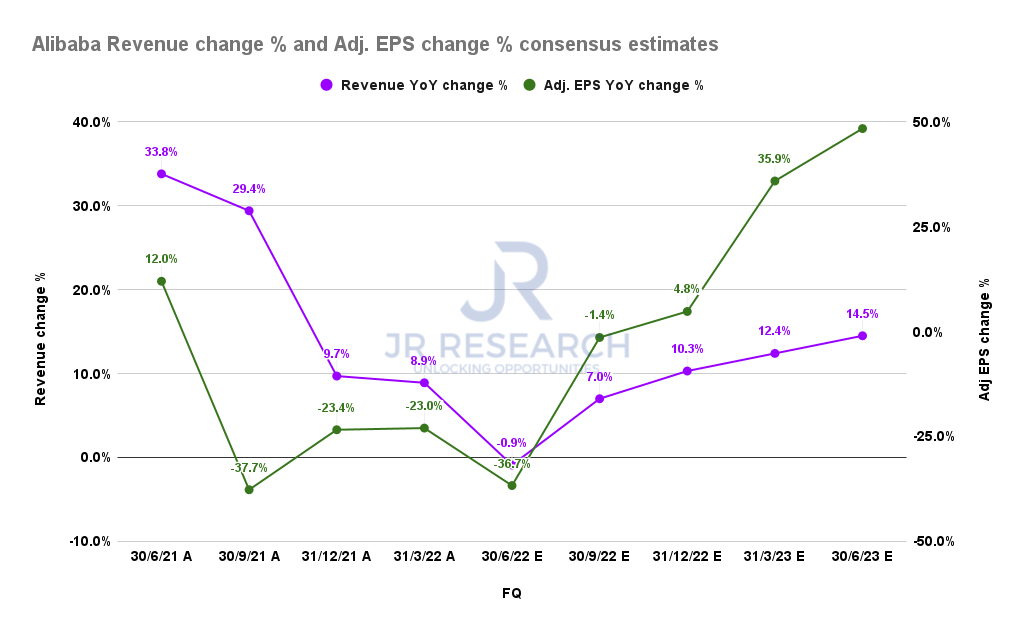

Alibaba revenue change % and adjusted EPS change % consensus estimates (S&P Cap IQ)

As a result, we believe the market is attempting to de-risk its valuation of BABA, heading into its Q1 earnings.

The revised consensus estimates (very bullish) suggest that Alibaba could post revenue growth of -0.9% YoY in FQ1, following Q4’s 8.9% increase. However, its profitability could continue to see further headwinds, as its adjusted EPS is projected to fall by 36.7% YoY.

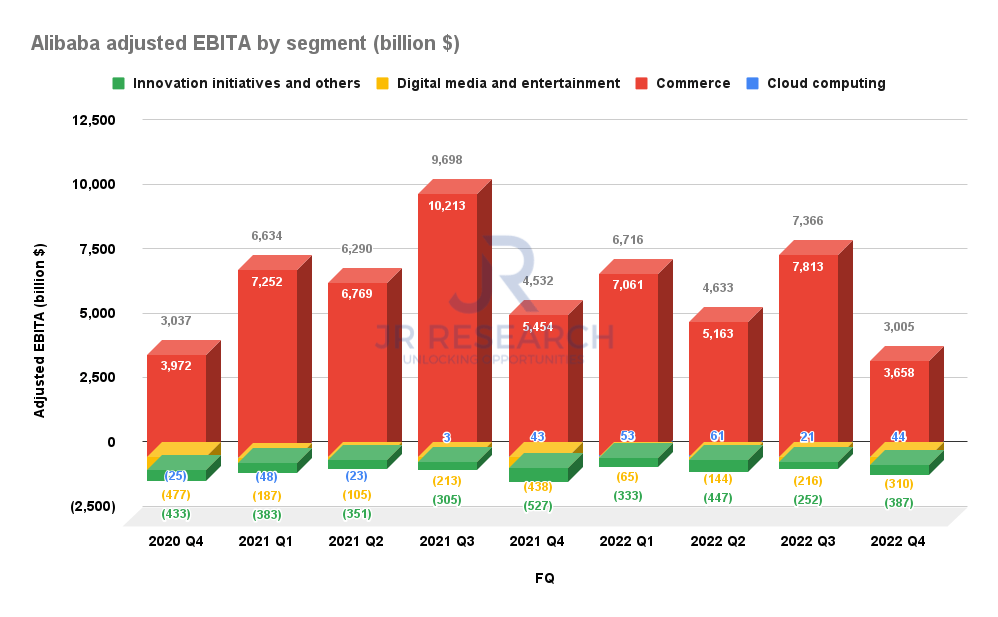

Alibaba adjusted EBITA by segment (Company filings)

However, we believe investors should not be stunned. There shouldn’t be any surprises, right? Despite the growth momentum seen in Ali Cloud, commerce (physical and e-commerce) remains Alibaba’s most critical adjusted EBITA driver, as seen above.

Therefore, the current macro headwinds that have continued to impact China’s consumer discretionary spending, coupled with the COVID lockdowns, would likely be persistent.

Furthermore, the ongoing property market malaise has seen little signs of turning for the better, as homebuyers have gone on strike over making further mortgage payments on unfinished homes.

Is BABA Stock A Buy, Sell, Or Hold?

We revise our rating on BABA from Hold to Buy.

We believe the recent pessimistic sentiments on BABA sets up the stock very nicely, heading into its Q1 card. In addition, positive commentary from management about its expected recovery from 2023 should help stabilize the stock. With a net cash position of $43.92B, Alibaba is in an enviable position to continue making strategic stock repurchases to underpin its recovery momentum moving forward.

While we do not expect BABA to break below its March lows of $73, we have yet to observe constructive price structures that suggest its selling downside is facing significant buying pressure. Therefore, our Buy rating attempts to front-run the market, and investors should be ready for potential downside volatility.

Be the first to comment