Robert Way

Thesis

Alibaba Group Holding Limited (NYSE:BABA) heads into its highly-anticipated FQ2’23 (quarter ended September 30) earnings release on November 17, even as it held back from reporting actual sales figures for its 2022 Singles’ Day (11.11) sales event for the first time.

Alibaba reported that its 11.11 event “[delivered GMV] for brands in line with [2021] despite economic and COVID-related headwinds.” Notably, Alibaba reported a gross merchandise value (GMV) of RMB540.3B for 2021’s 11.11 event.

Therefore, all eyes will be on CEO Daniel Zhang & team on November 17, as Bloomberg had reported earlier that Alibaba’s 11.11 event “may suffer a decline unprecedented in the event’s 14-year history.”

Despite that, BABA has outperformed the S&P 500 (SPX) (SP500) since we upgraded it to Strong Buy in our previous article. Moreover, BABA’s recent recovery was bolstered by the anticipation of a progressive easing of COVID policy. As such, the positive reaction by the market was not surprising as China’s 20th CPC National Congress had ended with no signs of any easing.

Hence, the market had likely written off any near-term likelihood of even progressive easing as it slashed the valuations of China equities in response to the start of President Xi Jinping’s unprecedented third term.

We discuss why we glean that the mean reversion move for BABA remains attractive at the current levels. Despite the massive pessimism seen as investors further de-rated China’s political risks, BABA’s price action remains constructive. Coupled with a well-beaten-down valuation in line with its Hong Kong tech peers, we assess that BABA’s reward/risk profile remains attractive.

Maintain Strong Buy with a medium-term price target (PT) of $90.

Refinement Of China’s COVID Policy Is Good Progress

China lifted the market’s sentiments last week as the newly installed Politburo Standing Committee (PSC) highlighted the need for “more decisive” measures, as Bloomberg reported:

In a meeting of the new Politburo Standing Committee chaired by President Xi Jinping, the members called for more decisive measures to curb the spread of the virus so as to resume normal life and production as soon as possible, according to the Xinhua News Agency. – Bloomberg

Therefore the “20 measures” rolled out by China’s State Council and National Health Commission that reduced centralized quarantine time and flight suspension penalties were not expected by the market. Moreover, it occurred while COVID cases continued rising. Bloomberg reported that China’s COVID cases increased to 11.3K on Friday (November 11), breaking above 10K for the first time since April on Thursday.

Furthermore, some cities actually reduced mass testing despite the rising cases. Hence, we believe the odds for a progressive ending in COVID zero are increasingly likely.

Still, investors should not rule out Beijing tightening its COVID policy again if COVID cases continue to rise higher, or even spike. China has maintained that the recent measures do not indicate that China has moved to living with the virus. Stamping out COVID expeditiously remains the guiding principle of its policy measures. As such, investors should expect near-term downside volatility if Beijing tightens further.

What’s Next For Alibaba?

Alibaba Revenue change % and Adjusted EBITDA change % consensus estimates (S&P Cap IQ)

Therefore, we think the thesis for a bottoming in Alibaba’s revenue and profitability growth by FY23 (year ending March 2023) is increasingly likely.

Xi Jinping’s hand has likely been forced by the worsening global macroeconomic headwinds that has added significant stress to its domestic malaise. As a result, China is almost certain to miss its 5.5% GDP target for this year. Moreover, China’s trade surplus weakened further in October as exports fell for the first time since May 2020, down 0.3% YoY.

Furthermore, China’s producer price index (PPI) declined 1.3% YoY in October, down for the first time in over two years. Hence, the disinflation signals are building up in China’s economy, likely spurring policymakers to act more urgently to arrest China’s economic malaise.

Therefore, while Alibaba may report a relatively tepid or even lower-than-project FQ2 earnings release, the market is already looking ahead. While still early, Goldman Sachs had previously highlighted that it expected a reopening in the “second quarter of [2023].” Therefore, we believe Wall Street’s estimates have been predicated on such a possibility.

Given that Xi Jinping has already started to set the wheels in motion, despite the surge in COVID cases, we believe the reward/risk for an earlier exit is likely pointing to the upside.

Is BABA Stock A Buy, Sell, Or Hold?

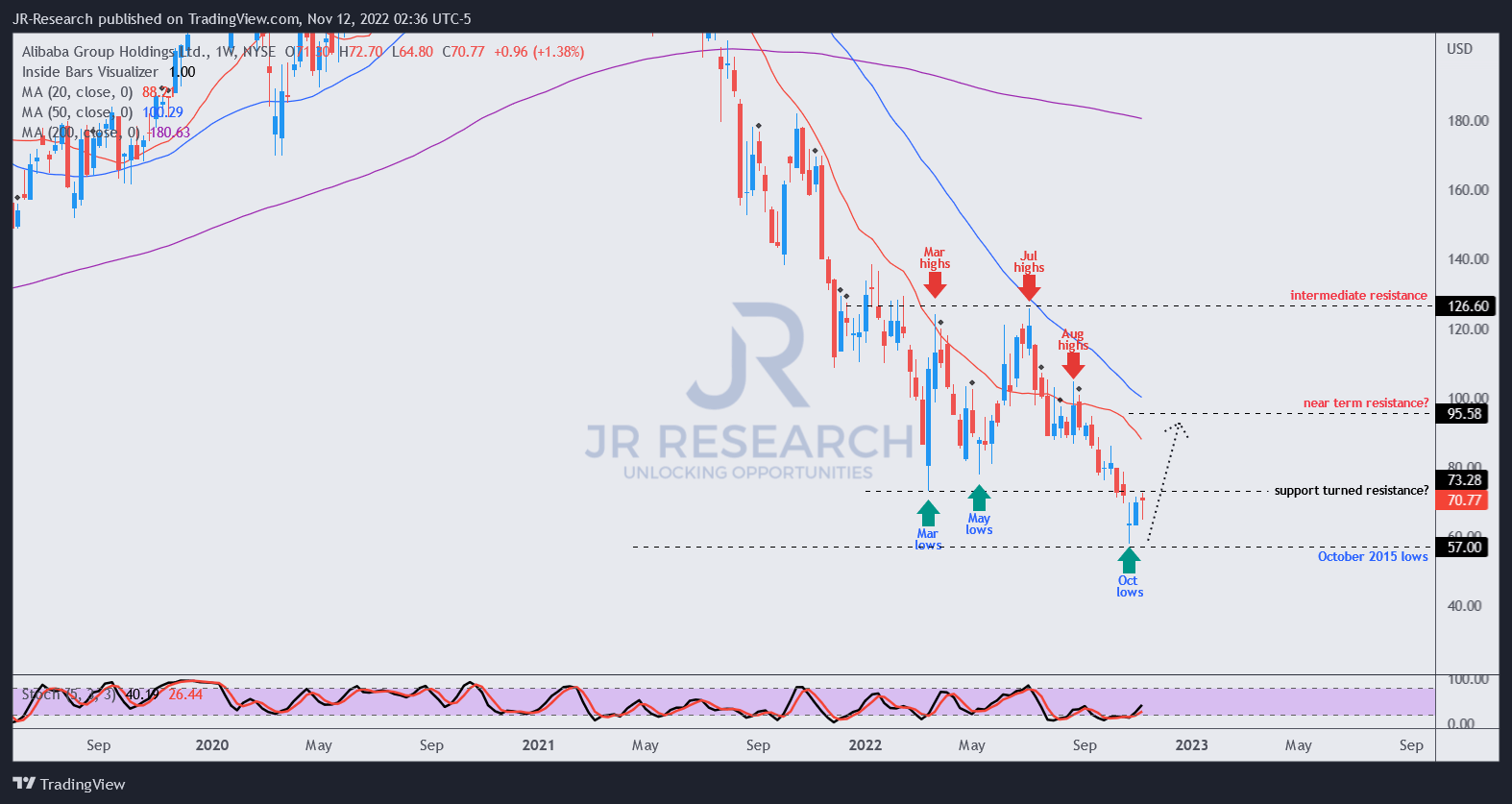

BABA price chart (weekly) (TradingView)

We emphasized in our previous update that BABA has two robust support zones that could see buyers defending vigorously against further selling pressure.

Therefore, even after the market forced sellers to give up after it broke below its March lows, buyers came in to defend its October 2015 levels ($57). That level appears to have been defended resolutely, which suggests that the market pulled the rug on weak holders who added the dips in March/May 2022.

Notwithstanding, we still need BABA to retake its March level and sit above it decisively for our thesis of a mean-reversion setup toward the $95 level to play out accordingly.

With China moving progressively away from its zero COVID strategy, we believe the potential for Alibaba to outperform the markedly downgraded consensus projections is looking increasingly likely.

Maintain Strong Buy with a medium-term PT of $90.

Be the first to comment