David Becker/Getty Images News

Executive Summary

This year, Alibaba Group Holding Limited (NYSE:BABA) faces multiple revenue headwinds hampering its growth prospects. Management’s growth initiatives have long-run potential but are too small to make a meaningful difference in the short and medium run. Alibaba’s growth-oriented shareholder base will exacerbate a volatile market reaction over what we see as a disappointing earnings release in May.

Investment Thesis

News of Charlie Munger selling significant portions of his Alibaba position doesn’t come as a surprise. My last two articles (found here and here) offered a rebuttal of The Daily Journal (DJCO) mogul’s investment thesis touting Alibaba’s shares on news media, citing competitive advantage, growth, and “value for the dollar invested.” Hearing him, I realized that his investment thesis needed updating and, more importantly, how oblivious Alibaba’s investors are to its new realities.

Until recently, Alibaba abused its market position to force merchants to sign exclusivity agreements, prohibiting them from marketing products on other platforms. What Charlie Munger thought was “competitive advantage” is, to a large extent, a monopoly that has come to an end after a brutal corruption and regulatory crackdown.

Munger also mentions a “higher value of a dollar invested” in Alibaba than its US and European counterparts. This hypothesis was true six months ago, but today, there are many western tech companies trading at discounts after the growth-to-value rotation.

Finally, the growth argument is also no longer helpful because of a maturing core segment and the low revenue base of growth drivers such as Cloud and the international market. The Q3 (December quarter) mediocre revenue growth mirrors these dynamics.

Revenue Trends

Alibaba investors should prepare for volatile quarterly results this May. Realizing the rough patch ahead, Munger shrank his position, and you should consider doing the same. As always, be careful using leverage. Contrary to popular opinion, Alibaba is not necessarily at the bottom.

Last month, growth-hungry shareholders weren’t kind to the ticker after disappointing topline results, pushing shares to multi-year lows. Regardless of how much data and price multiples support your hypothesis, nothing can prevent shares from dipping again. Market prices are determined by supply and demand, and I believe there is a discrepancy between what Alibaba can deliver and what its shareholders expect in terms of growth.

The company faces three main headwinds:

- Macro-economic challenges

- Maturing Chinese Market

- Rising Competition

The zero-COVID policy is squeezing China consumers, dragging down consumer confidence. Google “China Lockdown,” and you’ll find chilling videos of desperate Chinese citizens struggling with lockdowns. In this video, Shanghai residents are heard screaming from their balconies in protest of the lockdowns, and they don’t seem in the mood for shopping on Alibaba. Instead, they appear more concerned about increasing prices, lack of income, depleting savings, food shortages, and inadequate food rations. The economic environment is not accommodative for Alibaba to meet Wall Street’s 33% 2022 revenue growth expectations.

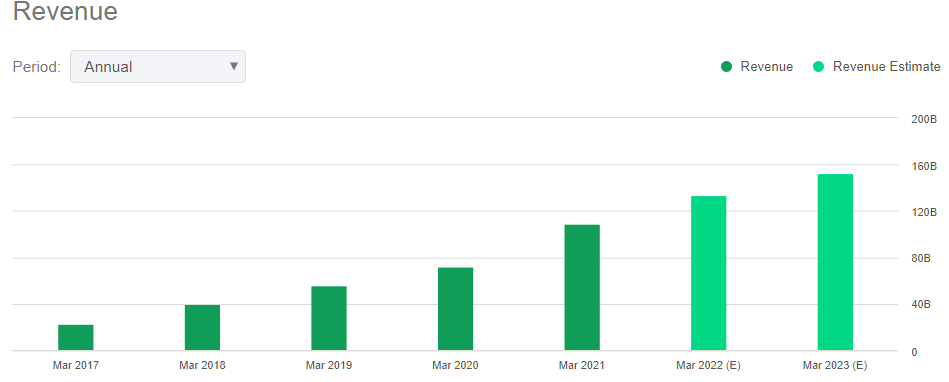

Alibaba Revenue Estimates (Seeking Alpha)

Alibaba’s macroeconomic challenges are the least of its troubles. One might argue that business cycles are temporary, similar to COVID policies, despite their short-term impact on this year’s revenue. This would make a solid contrarian strategy, especially for those with a stomach to sit on losses for long periods of time, if it wasn’t for the fundamental, long-term revenue disruption impacting Alibaba.

The China e-commerce “CEC” segment constitutes 70% of Alibaba’s revenue. Annual active users now stand at 937 million against a total population of 1.4 billion, with 260 million below the age of 15, pointing to a saturated market. Last quarter, CEC grew 7%, a disappointing figure given it includes inorganic growth from the Sun Art acquisition, mirroring demographic challenges facing its core segment.

Management is trying to find growth in rural China. However, sales data from its competitor, Pinduoduo Inc. (PDD), which focuses on this market and posts 900 million annual active users, points to a weak purchasing power that is not enough to create meaningful growth.

The same goes for cloud computing and international markets, which, together with rural China expansion, represent the company’s official growth strategy. The Cloud and International Segment represent 8% and 7% of total revenue. For these segments to compensate for a 10% decrease in core operations, both need to grow by 50% just for revenue to remain constant, still a hard-to-swallow proposition for a growth-hungry shareholder base.

I don’t believe that those buying the dip had enough time to analyze and study the company’s revenue trends and drivers. Alibaba’s fall was abrupt, accelerated by a brutal anti-monopoly crackdown that permanently changed the IT competitive landscape in favor of smaller peers. While new investors are showing courage in buying the dip, management is terrified, as reflected in merchant subsidies, which dragged net income 74% last quarter in an unsustainable attempt to maintain revenue and users.

Cash Flow And Share Buybacks

Fundamentally, Alibaba’s business model is sound, generating lucrative, scalable operating cash flows that encouraged the e-commerce giant to extend a share buyback program last month. Alibaba’s challenges stem from its inability to manage investors’ expectations. Historically, Alibaba attracted a growth-oriented shareholder base, and now that its core operations are maturing, management is finding it hard to communicate its transitionary state to shareholders. Investor presentations still market Alibaba as a growth company.

The problem is that many are falling for it. A few weeks ago, Kevin O’Leary was touting his new Alibaba position, citing the growth potential of Chinese tech. Munger and O’Leary are representative of this growth-hungry shareholder base.

How Loyal Is Softbank

SoftBank Group (OTCPK:SFTBY) owns about a third of Alibaba’s share, rendering the Japanese financial giant its largest shareholder. Softbank is known for its risk-taking and support for emerging tech companies. However, its participation in early capital-raising cycles means the dollar-average price of its position is far less than ordinary investors. For example, in FQ4 2021, Softbank reported a $558 million gain on selling some Alibaba shares, despite the ticker’s selloff.

Softbank is facing renewed capitalization issues. The Japanese lender might be forced to sell Alibaba stock, especially if shares tumble further after a potentially disappointing earnings release. One thing is for sure, and the current situation is testing Softbank’s loyalty to Alibaba.

Summary

Alibaba is heading towards disastrous quarterly and end-of-year results in May. I can’t imagine a scenario where Alibaba delivers on its shareholder’s high growth expectations. The Chinese economy, where Alibaba generates most of its income, struggles with rising COVID cases and rigid lockdown rules. The timing couldn’t be worse for Alibaba, currently toiling with new regulations that stripped it from its “competitive advantage.” The core segment, i.e., China e-commerce, has reached maturity with 973 million users.

Growth drivers touted by management only increase the discrepancy between its shareholder base and what it can deliver in terms of growth. Cloud and international segments are too small to offset the challenges of its core operations. Charlie Munger, the long-time proponent of the e-commerce giant, threw in the towel, cutting his position by the half, sensing the difficult times ahead. Alibaba’s volatility will test Softbank’s loyalty. Still, investors should note that the Japanese lender secured better prices than most, capitalizing on its participation in early capital-raising rounds before Alibaba went public. Alibaba might be a good investment in the long run, but I doubt it offers a better risk/reward balance than the market.

Be the first to comment