Aaron Chen PS2/iStock via Getty Images

Investment Thesis

Alcoa (NYSE:AA) prospects are likely to change. Both positive and imminent change is on the cards.

But before going further, I’m going to start this analysis with a quote from Alcoa’s management in the Q&A section of the earnings call. This lays out the core of the bullish thesis and we can then work backward from this quote which provides context, and add color around the positive and negative aspects weighing on the stock.

… the fact that you have 50% of your smelters in the world that are underwater at these prices, it tells you that there’s a lot of catalysts for significant changes in the market

I’ll explain the bullish drivers and what got me excited about investing in Alcoa, while at the same time describing what’s weighing down the stock right now.

Q3 Results, Looking Back

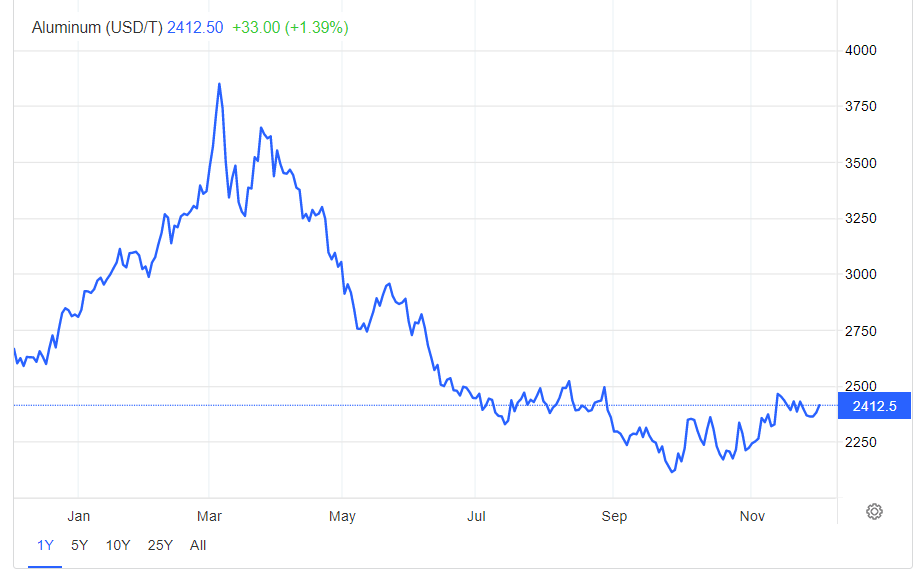

There was no positive news expected going into this earnings result. Across the board commodity prices have long ago fully rolled over and aluminum has been no different.

There’s no point in sugarcoating what is obvious, during a downturn, everything goes on sale. So, with that in mind, why should one even consider sticking with Alcoa?

I never cease to be impressed with operating leverage and how much of a driver of the underlying business it can be.

With Alcoa, given its very high fixed cost base, when there’s high demand for aluminum, aluminum prices move higher, all that excess revenue drops to the bottom line, and Alcoa oozes free cash flow. And the same in reverse too.

AA Q2 2022

As I’d been reporting for some time now, aluminum prices had been hit really hard in 2022 because of two aspects, per the red box above.

Firstly, there had been a huge amount of supply becoming available from China. Also, bottlenecks in EV production and a slowdown in manufacturing had materially impacted demand.

Trading Economics

Both aspects together had led to aluminum prices falling nearly 50% since March highs.

However, there are now three different catalysts that could soon reverse this oversupply.

In the first instance, Alcoa contends that approximately 25% of the aluminum product in China is now uneconomic. Also, close to 50% of the rest of the world’s aluminum production is now uneconomic.

AA Q2 2022

And that had been one of my considerations for investing in Alcoa.

I knew that Alcoa’s cheap US-based energy would allow the business to generate a profit at a much lower aluminum price, compared with its peers outside the US.

That being said, the remainder of Alcoa’s business outside the US, particularly in Europe is unprofitable too.

Therefore, this is my strong argument. That Alcoa’s US-production has a moat, as its energy costs are dramatically lower than its peers in Europe.

Secondly, given the Russian invasion and the various sanctions hitting Russia, I had expected that aluminum would not be immune from the sanctions. And so far, that line of thinking hasn’t delivered any positive prices for aluminum.

This is what Alcoa said on the call,

[Trading companies, such as the LME] are not going to want to hold on to metal that in the end won’t either be deliverable to the LME or deliverable to most of the customers, and certainly, customers that are willing to pay full price or even at discounts.

That would create a lot of disruption if you think about it. As a customer, there’s no point in you embarking on transactions on LME for aluminum, if ultimately that aluminum doesn’t get delivered to the LME.

I’m not going to say that is going to happen with absolute certainty, but it does appear to be a ”potential soft catalyst” that could drive aluminum prices higher.

I’ll add a further quote from the earnings call that I believe encapsulates my bullish argument succinctly,

[…] the fact that you have 50% of your smelters in the world that are underwater at these prices, it tells you that there’s a lot of catalysts for significant changes in the market and having the Russian metal not be able to be delivered would be just more and more of those pieces that could have fundamental impacts.

And now, we’ll discuss the third, and possibly strongest catalyst.

The China Factor

There’s an increasing amount of speculation that China is considering reopening its economy. But what’s most particular to Alcoa, is that China’s industrial sector is a top consumer of aluminum.

From its housing sector to EVs, solar panels, to electronic gadgets. It’s all about aluminum consumption. And that’s going to be a game-changer for Alcoa.

Thus, to summarize the bull case, Alcoa’s prospects have been so bad, that investors have wanted nothing to do with the stock.

But now, you have most of your peers struggling to profitably produce aluminum, while Alcoa has access to substantially cheaper energy costs. Isn’t that some kind of moat?

Alcoa’s Financial Position

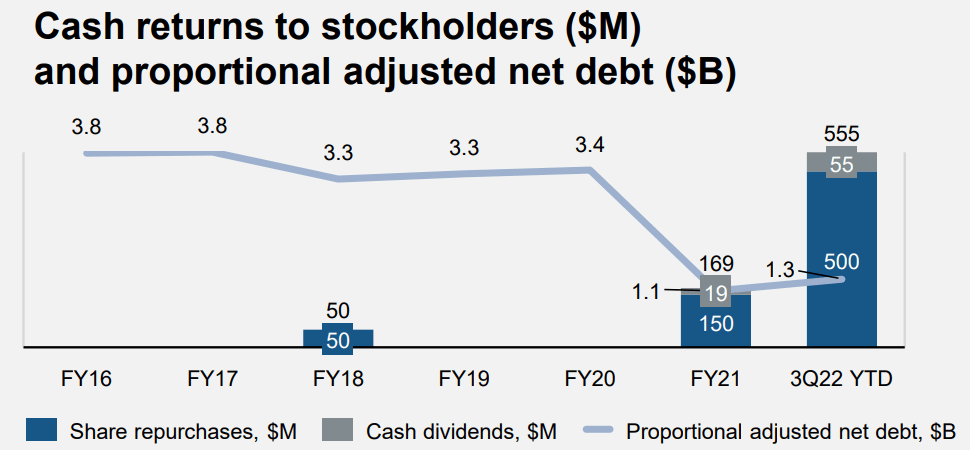

AA Q3 2022

The graph above requires some interpretation. What you see above is that Q3 2022 has $1.3 billion of net debt. That includes debt plus pension liabilities, partially offset by cash.

Clearly, the net debt positioning, the blue line, is directionally coming down over the past few years, even if it ticked up slightly from Q4 2021 at $1.1 billion to now around $1.3 billion.

In fact, I wish to highlight that for the first time in a long time, Alcoa’s balance sheet is investment-grade. That’s really, really crucial for a commodity company looking to navigate a bear market.

With the benefit of hindsight, management was very consistent in Q4 2021 through Q3 2022 that it would continue to prioritize Alcoa’s balance sheet.

Even when analysts were consistently urging management to be more aggressive with its capital return program, Alcoa stood resolute on its priorities of investing in the business, followed by shoring up its balance sheet, and only then returning capital to shareholders.

In hindsight that was a very astute strategy.

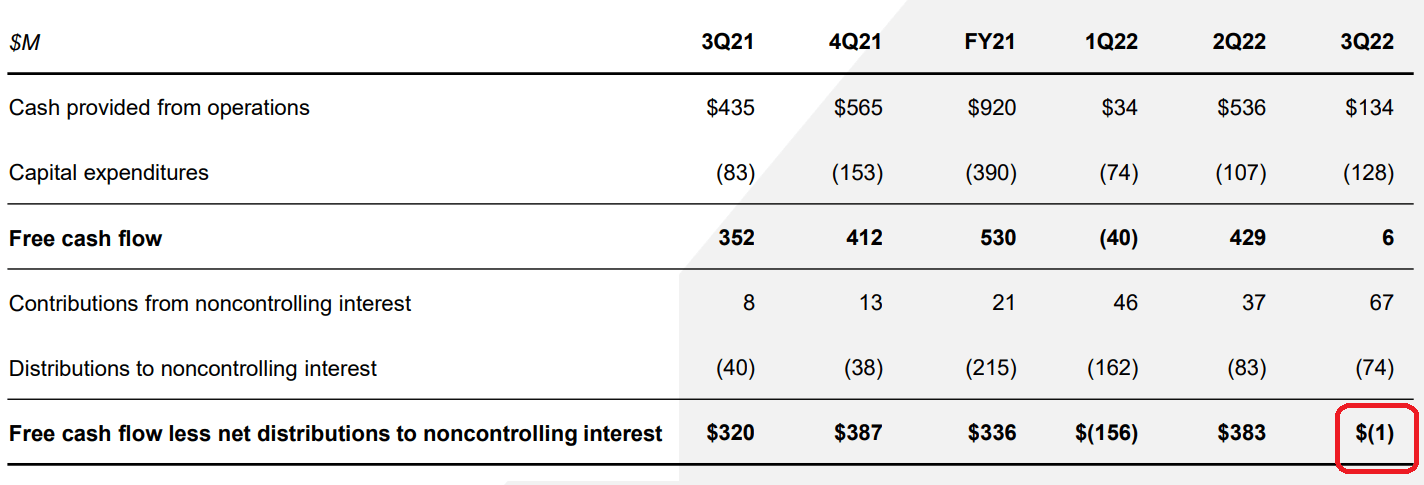

AA Q3 2022

Next, as you can see above, Alcoa squeezed its working capital, so that its free cash flow line ended at breakeven.

I’m not going to say that isn’t that bad. But it really isn’t a horrendous quarter, when all is considered.

AA Stock Valuation — ‘Dead Money’ For Now

This quote from Alcoa’s CEO surmises the overall context,

The combination of increased uncertainty, weakening European demand and the global energy market distortions created by the ongoing Russian aggression in Ukraine demonstrate how quickly our energy markets, and therefore, the Aluminum industry can be impacted.

This is an echo of everything we are now going to be hearing in the next few weeks. For now, energy is the only game in town.

But I recognize that until energy prices return to being affordable and reliable, high-energy industries such as aluminum could be challenged, so investors should remain aware of the impact of elevated US energy prices.

The Bottom Line

It’s so difficult to have a time horizon longer than a few quarters in a bear market. When stocks are going up, nobody is asking difficult questions. And all is well.

But when stocks are going down, investors become gloomy, particularly as we enter tax loss season.

As I recognize the negative considerations facing this investment, I continue to remain hopeful that the bottom could soon be in for Alcoa. I believe that I’ve already embraced the bulk of the potential negative outcomes of this investment.

So on a risk-reward balance, I’ve had all the risk and none of the reward. Now, I believe that it’s worthwhile to try to sit on my hands and wait a little longer.

Be the first to comment