John Moore/Getty Images News

Summary

Albemarle Corporation (NYSE:ALB), like many LCE (Lithium Carbonate Equivalent) producers, has immensely benefited from the LCE price run up in 2022 driven by the auto & battery industries supply needs. The primary dilemma facing the shares is if these prices are sustainable or will they crash. Under my sensitivity analysis I concluded that ALB’s valuation is pricing long term LCE at US$20k vs the most recent US$71k ton spot price. Thus, in my view, ALB looks like solid risk reward idea in the lithium sector.

LCE Prices

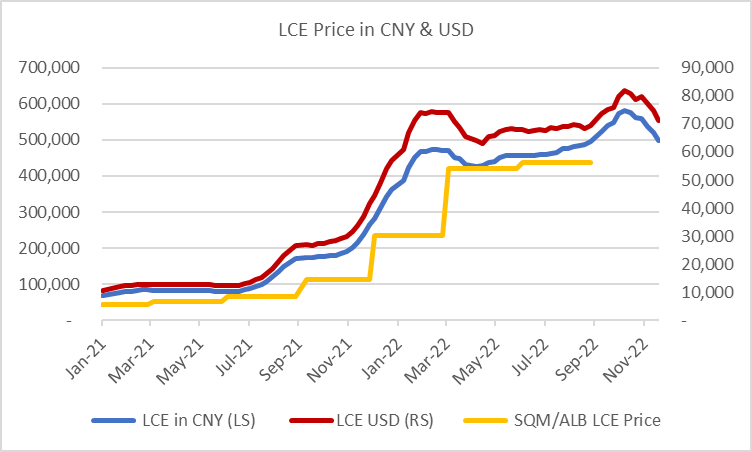

China LCE spot price has increased from US$10k/ton during the pandemic to US$81k/ton peak in November 2022 and now have declined to US$71k/ton. At the same time ALB and SQM have seen realized prices increase from US$5.5k/ton to US$56k/ton as they move away from fixed price contracts to market pricing. Is this a strategic mistake or do the two top LCE producers understand the demand and supply equation a bit better than the market gives them credit for? Given that China has ended its zero Covid policy it may be that EV and battery demand actual increases. While US and Europe have not altered their end of combustion engine time frames. This means that three very large auto markets need to convert for EV manufacturing rapidly. Once US billons are committed to developing EV’s and the OEM supply chain, speed bumps are unavoidable but the strategic change unlikely.

China Spot LCE Price vs ALB/SQM (Created by author with data from Investing.com and ALB/SQM)

Sensitivity Analysis

ALB does not provide explicit quarterly volume or pricing disclosure, which makes modeling more difficult. However, I can extrapolate volumes and pricing from peer Sociedad Química y Minera de Chile S.A. (SQM) which I also cover, that does provide operating details.

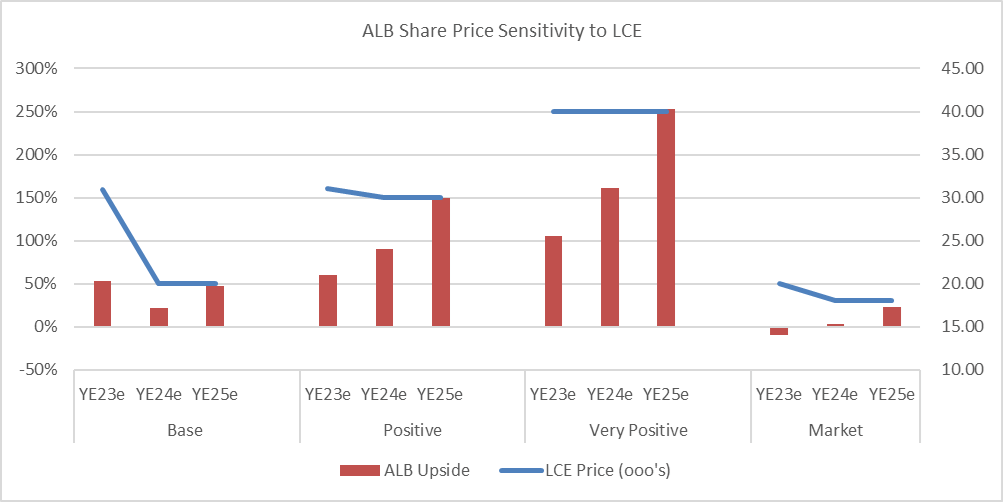

Under my conservative base case scenario, I assume LCE prices will decline to US$30k/ton in 2023 and stabilize at US$20k/ton going forward. Under ALB’s volume growth target, EBITDA margin and capex assumptions, the company should generate substantial free cash flow that generates value. At a 10x EV/EBITDA target multiple the stock has 50% upside in 2023.

Under a worst-case scenario, where LCE prices collapse to US$20k/ton in 2023 the stock would be fairly valued. This means that the market is already pricing in a worst-case scenario. This situation is not exclusive to ALB and can be seen in SQM’s valuation as well, for which I conducted a similar exercise. (SQM: Market Is Pricing The Stock At $20k/Ton LCE)

Obviously LCE prices above US$30kton long term would be very positive for ALB’s operating results and valuation as seen in the Positive and Very Positive scenarios.

ALB Valuation Sensitivity to LCE Prices (Created by author with data from and ALB)

Lithium Operations Overview

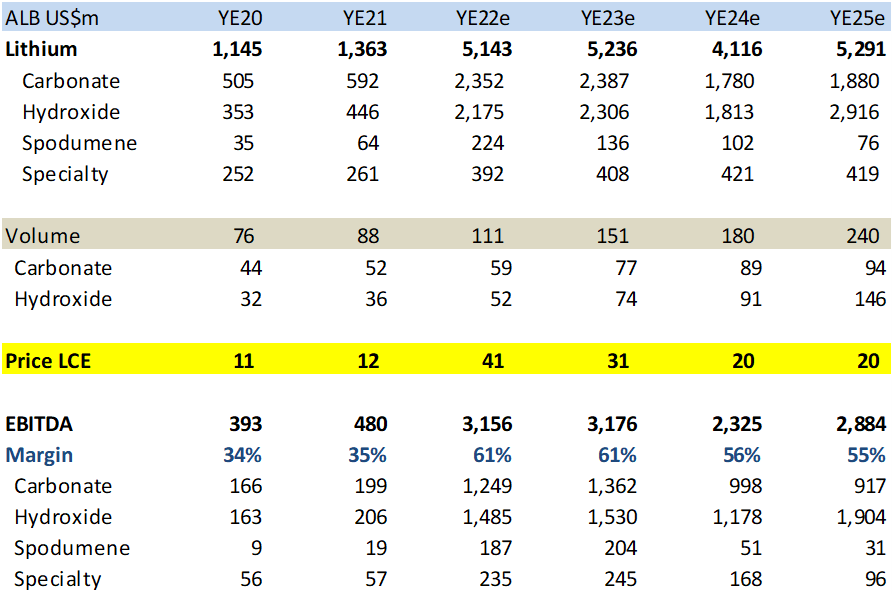

ALB has an estimated LCE capacity of 111k/ton for 2022 and is slated to expand to 240k/ton by 2025 or about an annual 20% growth rate. This capacity expansion comes mostly from the Chile Salar operations (concession to 2043) and the Wodgina Australia JV (60% stake) while US expansion may face delays. The 49% stake in Talison/Greenbush operations is not consolidated and the company adds the net income to its EBITDA report. Australia produces lithium concentrate from spodumene that then is sold as feed stock or can be used internally as ALB adds chemical conversion capacity in Australia, China and the US. ALB should invest over US$1bn a year to achieve this growth rate, that can be funded by cash flow with LCE price below US$20k/ton.

While prices for the different products vary from market to market, I am synthesizing all into LCE, this could make for a more conservative revenue model. I am also basing cash costs and EBITDA margins on SQM’s reports given ALB’s poor disclosure.

As highlighted in the base case sensitivity analysis, I am assuming LCE prices peak in 4Q22 and then begin to decline to US$30k/ton by 4Q23 and then stabilize at US$20k/ton going forward. This high price does not materially affect royalty payments in Chile since the top take rate is 40% with prices above US$10k/ton.

ALB Lithium Operating Model (Created by author with data from and ALB/SQM)

Consensus Comparison

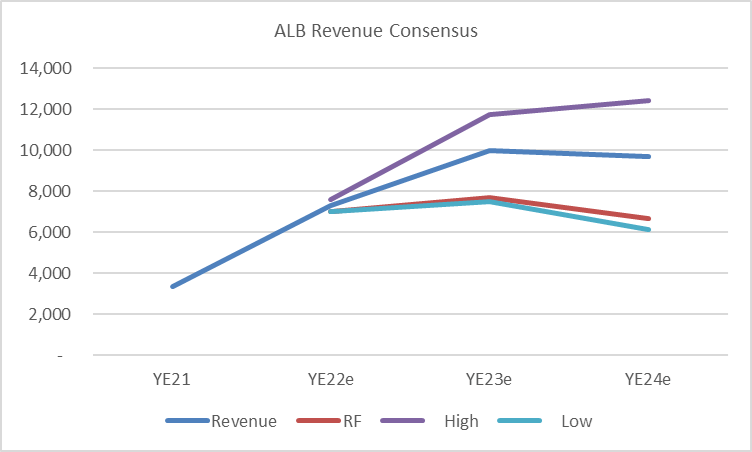

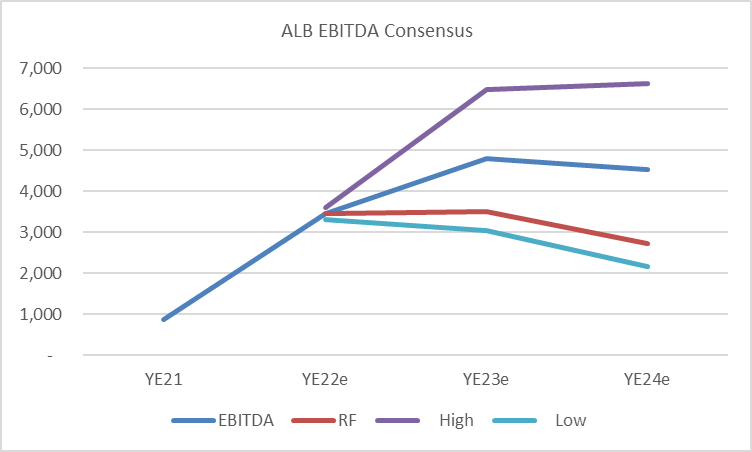

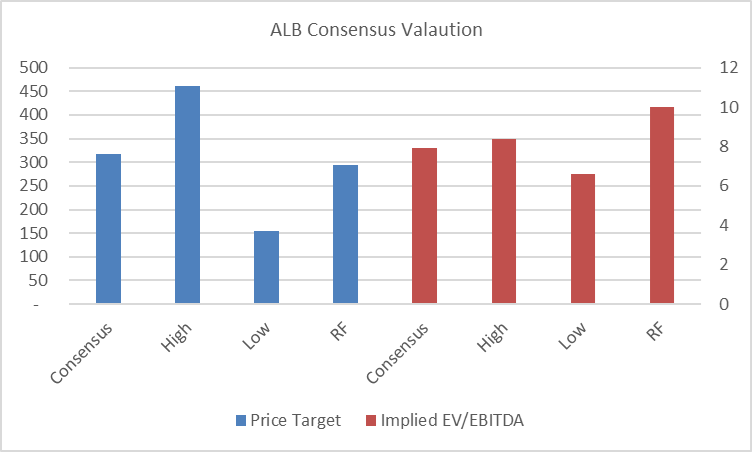

ALB is a well-covered stock with 20 analyst crunching numbers that make for a good data set to form a comparison base vs my estimates. As can be seen in the two charts below my estimates are below consensus and near the low end of the data range. This indicates that the sell side is projecting far higher LCE prices. However, the same analyst value the stock at under 8x EV/EBITDA vs historical range above 10x when ALB was a slow growth specialty chemical stock. I seriously doubt this lower valuation is due to a higher discount rate, its most likely on the fear of short-term share price correction as LCE price gyrate.

ALB Revenue Consensus (Created by author with data from Capital IQ) ALB EBITDA Consensus (Created by author with data from Capital IQ) ALB Price Target Consensus (Created by author with data from Capital IQ)

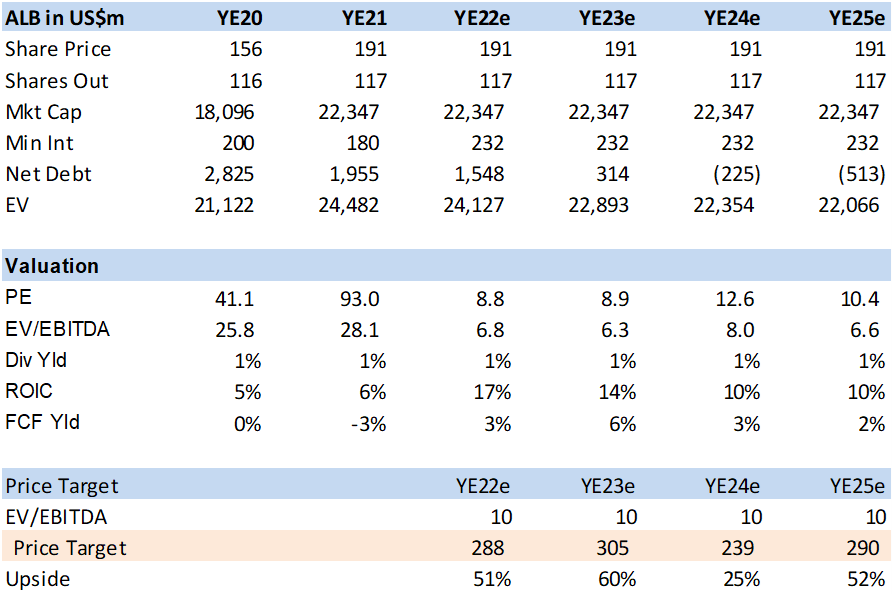

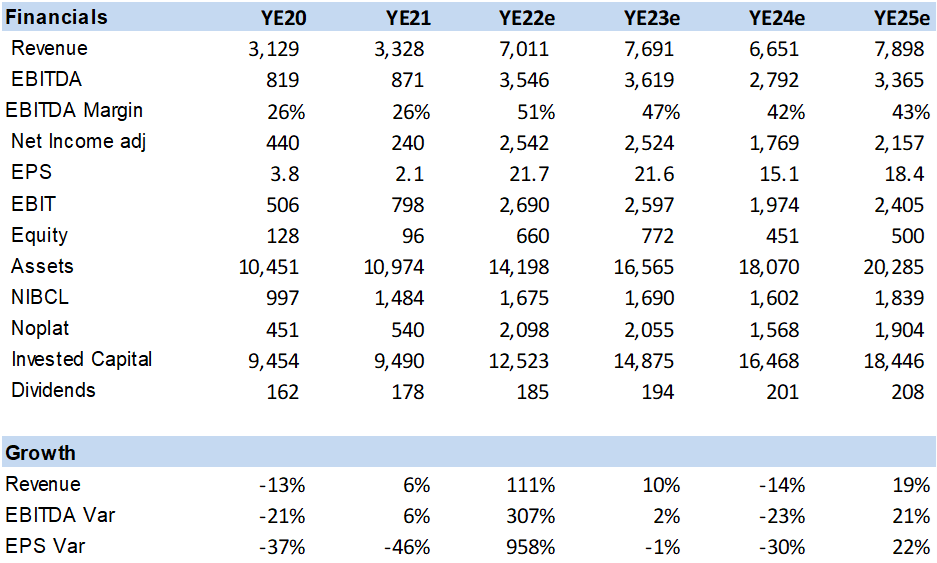

Valuation

I value ALB at 10x EV/EBITDA, below its historical average of 12x and below its growth rate or cash flow generation and ROIC. This equates to about 15x P/E. Under my conservative scenario of declining LCE prices from US$80k/ton to US$20k/ton in 2024 the stock upside may appear low or erratic. It’s important to keep in mind that these estimates are designed to be conservative, to test the stocks potential even under a weaker operating scenario.

ALB Valuation (Created by author with data from ALB) ALB Financial Summary and Estimates (Created by author with data from ALB)

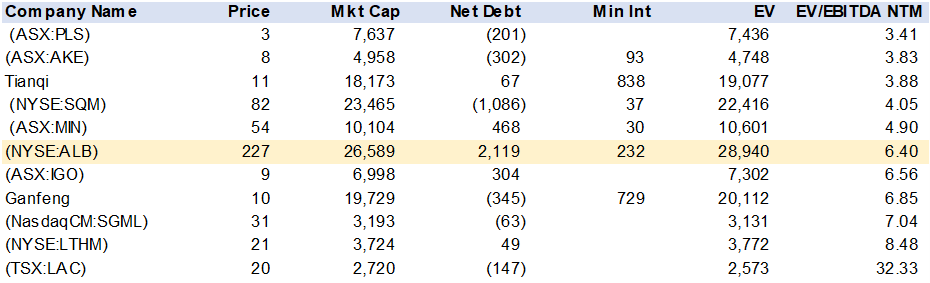

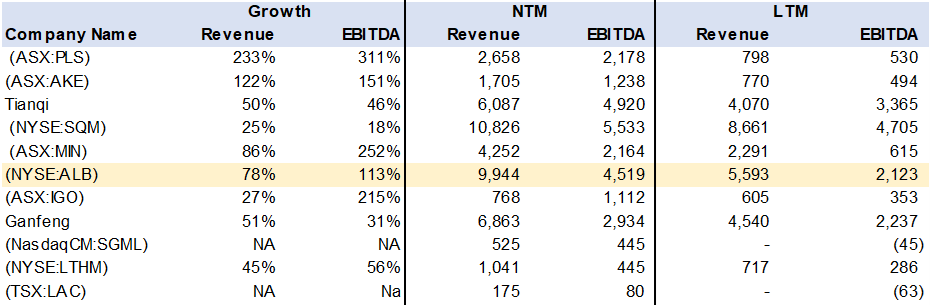

Peer Comparable

ALB is not the cheapest stock, nor does it have the highest growth rate in the lithium sector, but it is the largest by market cap that could look to consolidate the sector. The Chines companies, Tianqi and Ganfeng have also been active in M&A, while the smaller and cheaper Australian players could be targets.

Consensus Peer Comparison (Created by author with data from Capital IQ) Consensus Peer Comparison (Created by author with data from Capital IQ)

Conclusion

ALB is a leading global lithium player that is investing to grow volumes by 20% annually through 2025. However, its shares appear to be priced on a near-term collapse of LCE prices that I find attractive.

Be the first to comment