John Moore

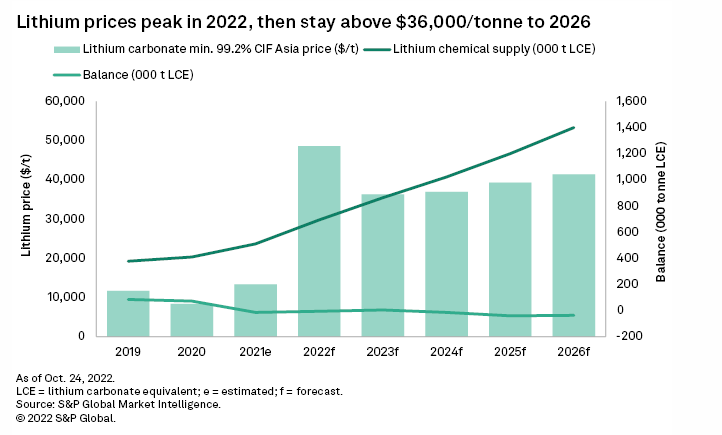

Lithium has become an increasingly important element in the global Energy Transition. Recent projections have assessed that less lithium may be needed for full decarbonization than previously thought. However, the IEA still projects that current demand could increase by 26-fold. So, there is a stable demand, and prices are expected to remain elevated to reflect the increasing demand for lithium over the coming years.

S&P Global

Albemarle Corporation (NYSE:ALB) is the world’s largest lithium miner. Aside from ALB being large, mining is an industry where assets matter. Albemarle has a considerably better portfolio of physical assets compared to its few peers and has also demonstrated that it is simply more adept at extracting one of the world’s most crucial substances (with a bullet), and this is mainly because of intangible assets like intellectual property working synergistically with their industry-leading physical assets. Also, something I really like about this company is that it has pro-shareholder rules for allocating capital to growth initiatives, ensuring that the ROIC exceeds WACC.

TD Ameritrade

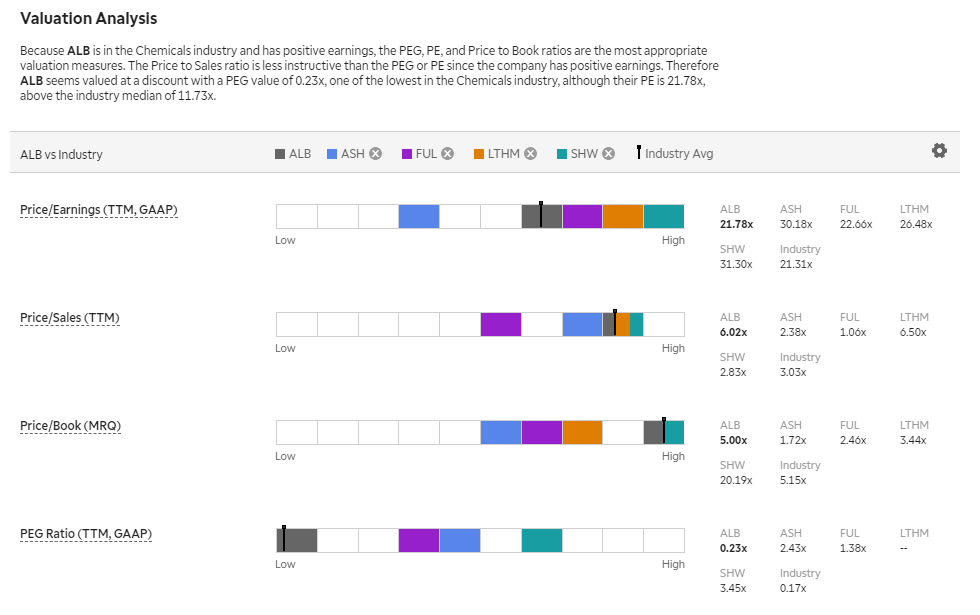

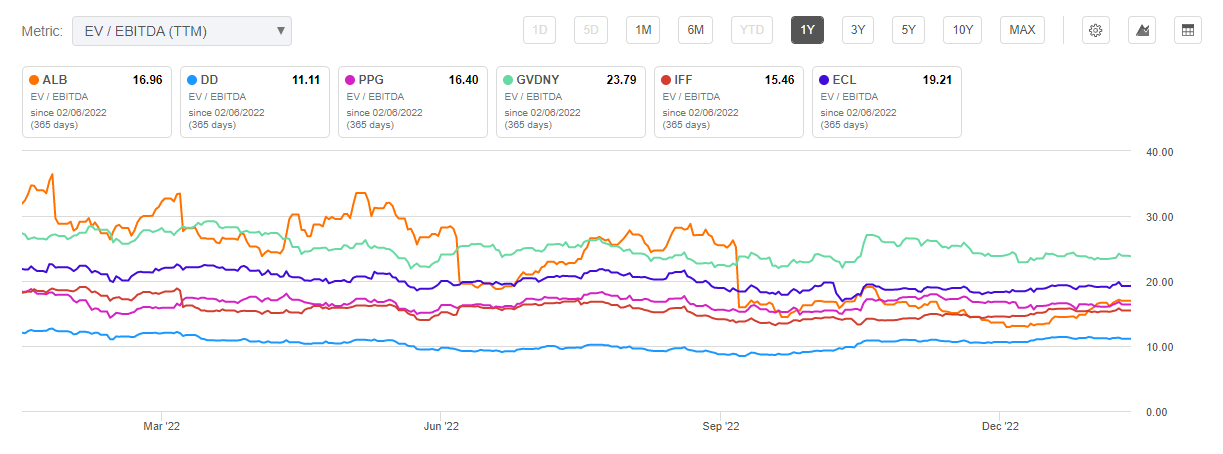

As you can see, the company is valued a bit higher than many peers across some metrics. However, for the most part, it doesn’t stand out too much from its peers except for one metric: the controversial PEG ratio. This metric is pretty simple. It is just the P/E divided by the growth rate. It can have limited utility in some circumstances, but I think it is telling here.

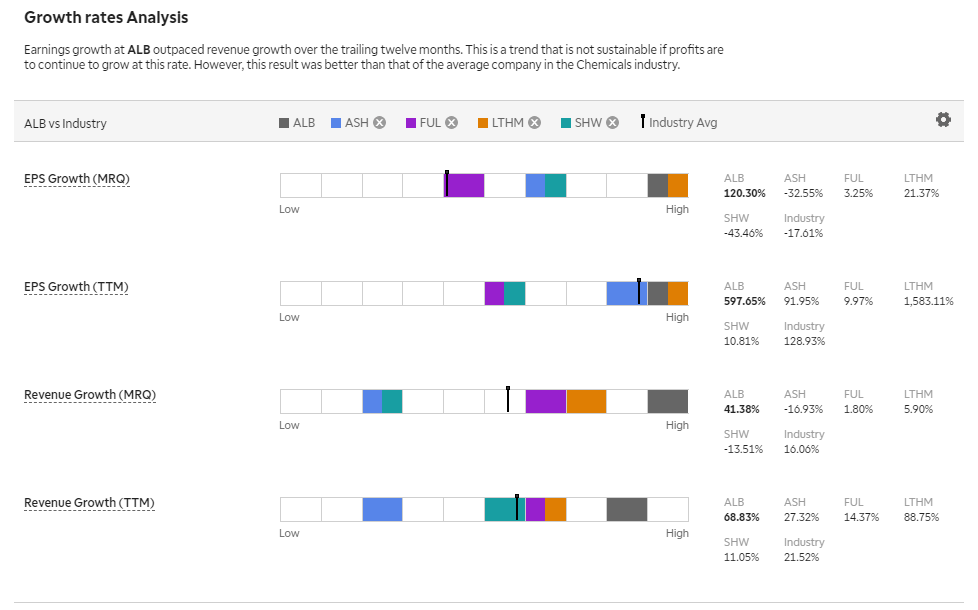

Albemarle has had a great run this year, and you may want to wait for a short-term technical pullback before entering the stock (although this is not my expertise, ask if you need some). When you compare Albemarle to the same peers and its industry using earnings growth, the outlier nature of Albemarle in terms of growth suggests it could easily attain a higher multiple over coming months, particularly as earnings growth is almost certainly to become more scarce.

TD Ameritrade

The growth should be able to continue according to the company’s estimates. Developing new lithium reserves is very intensive in terms of both capital and time. A lot of new supply is coming online, but it likely will not be enough to meet burgeoning demand. Albemarle forecasts a supply shortage over the next decade that should continue supporting price. If large-scale lithium-ion batteries to store renewables, championed by Elon Musk, turn out to be a viable solution at scale, then many projections for growth in lithium demand could end up being light.

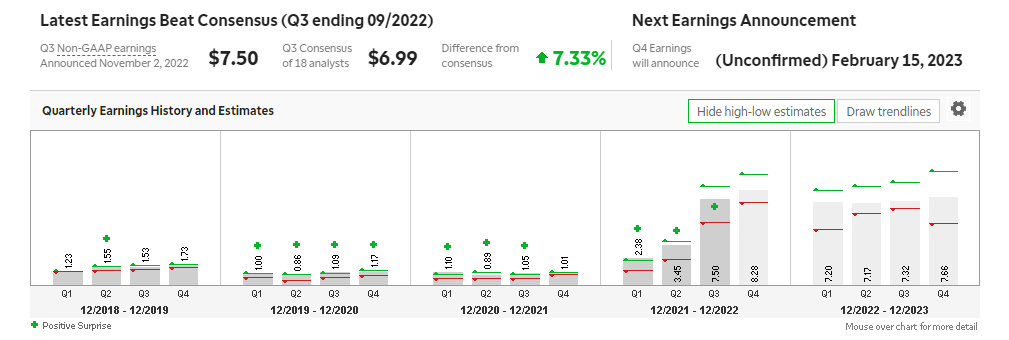

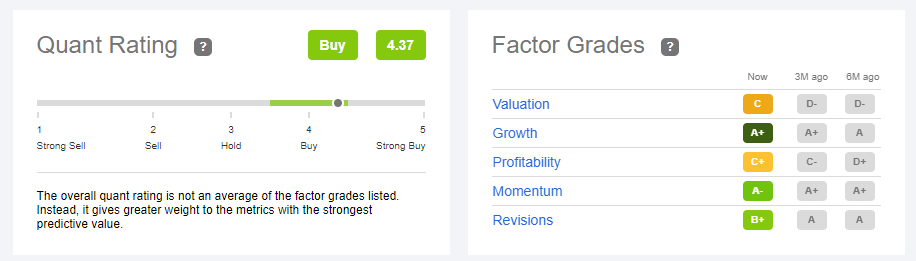

Albemarle is an “Earnings Beat Maven,” and This Likely will Continue on February 15th

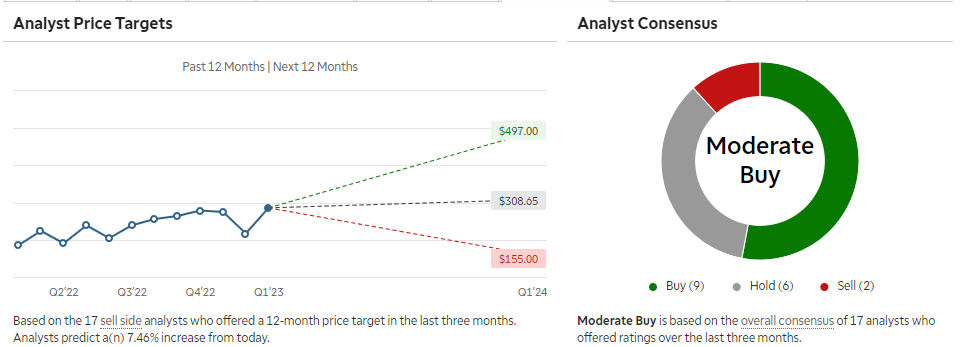

Albemarle Corporation has had an awe-inspiring performance over the last few years. In 2020, the stock was up a white-hot 102%, followed by a nearly as impressive 58.5% in 2021. Last year, it was only down about a third as much as the S&P 500 (SP500). The stock is up well into the double digits in 2023; however, unlike many other stocks that have leaped double digits at the start of this year, the world’s largest lithium miner remains below analyst targets.

TD Ameritrade

This stock is one of the beneficiaries of the world’s increasingly insatiable demand for the lightest metallic element, lithium. The substance doesn’t occur in its natural elemental form on Earth, so the mining and extraction process is particularly vital. Increased prowess in this area, as Albemarle has continually demonstrated, can lead to significantly better economics than competitors. In my opinion, Albemarle is the fiercest lithium miner, competitively speaking. It also has a stellar performance record that suggests that multiple expansion is possible over the next few years.

TD Ameritrade

The company has not missed expectations once in the past 15 quarters. It has beaten expectations nearly three-quarters of the time over that period. Earnings growth is dramatically accelerating in the first half of 2023. It is estimated that EPS will grow about 200% in the first quarter before slowing to about half of that in the second quarter. This company’s multiple is behaving like an average cyclical mining company. Still, given its attachment to the increasingly important energy transition and increased domestic and foreign government subsidization of the area, I believe this consistent grower and performer will begin to break away from the traditional mining valuation.

Company Reports

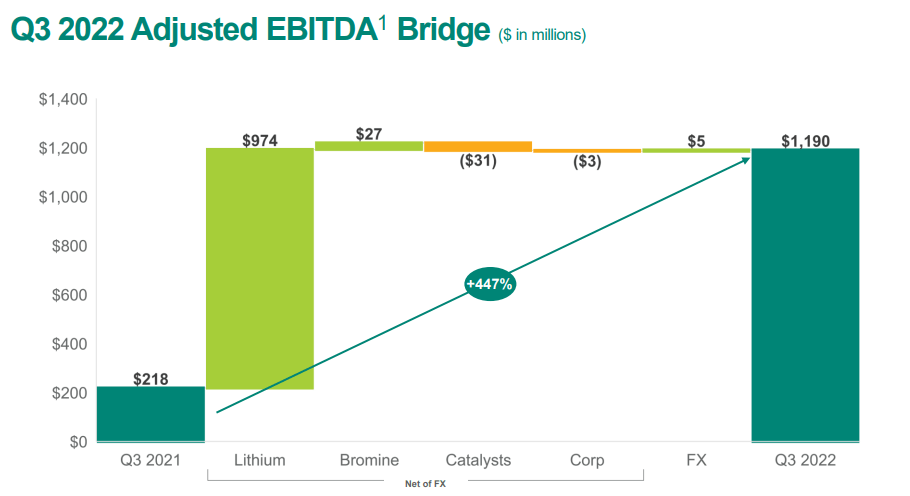

As you can see above, Albemarle’s EBITDA growth significantly outpaces the GAAP earnings growth. The company management has continually been delivering better-than-expected results through innovative and adept management, the use of talent, and the acquisition of assets. The company is known to be a great partner by consumers that matter in their industries and knows how to nurture and develop solid commercial relationships with leaders in their target markets built on endurable understanding and mutual benefit. The recent launch of an oil and gas focused subsidiary, Ketjan, shows this principle in action.

Given Albemarle Corporation’s prolific recent record at beating earnings expectations and the continued focus on the Energy Transition by many governments across the world, I believe that the company is likely to beat to the upside at its comings earnings report on February 15th, 2023. The firm recently announced it expects its Q4 earnings to surpass consensus estimates. Furthermore, it forecasted a 5-yr net sales CAGR of roughly 20%, which is well above the market’s earnings growth rate.

Albemarle Meets my Criteria for Long Picks in 2023

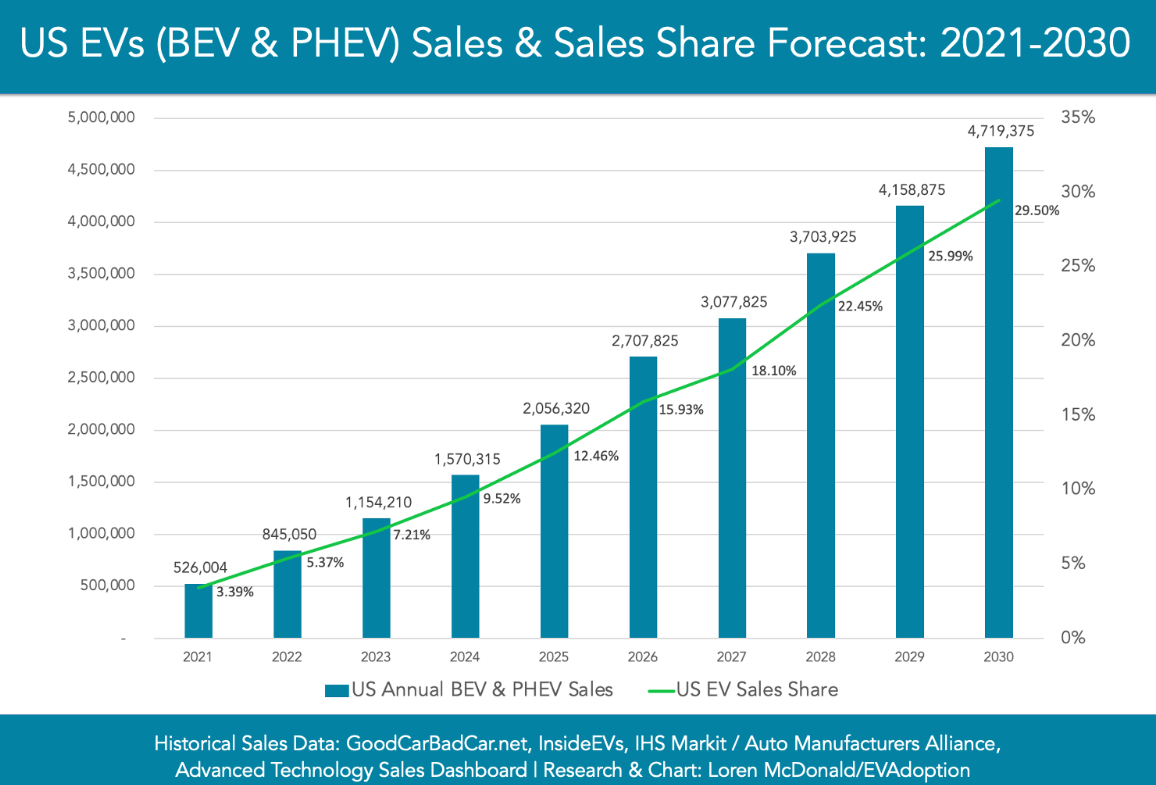

One of the things I try to focus my analysis on is identifying beneficiaries of transformational trends. The Energy Transition, and the associated electric vehicle (“EV”) revolution, have certainly made themselves known. One thing you have to be wary of, though, when picking beneficiaries of these massive secular trends is picking a horse that seems like a solid competitor day which may lose that distinction as the situation evolves. A “picks and shovels” play is a term that comes from the California Gold Rush. While the chances of striking a mother lode were not very good, the chances of getting rich and selling it to people trying to strike one were considerably better.

IEA

Thus, no matter who wins the epic “Game of Chromes” going on between Tesla (TSLA), Ford (F), General Motors (GM), and other international competitors, it’s a safe bet that lithium demand in the coming decades will be robust because of its high utility in storing electricity. Betting on any one of those names exposes you to the risk that competitive advantages and brand appeal can change on a dime in the high-barrier, ultra-difficult auto industry. In fact, Ford and Tesla are the only two American automakers to have never gone bankrupt. While the most obvious use case is now EVs, the inherent value of the commodity they mine leads me to believe other major uses will also arise.

I have been urging investors to take the risks of 2023 seriously. In my 2023 Outlook, I mentioned that I was more partial toward the crowd that believes the bond market will ultimately prove more accurate than the Fed’s December Summary of Economic Projection (S.E.P.), or as I like to call them, the “dots of doom.” Since my outlook was released, the odds have pulled in the bull’s favor, according to the Atlanta Fed’s Market Probability Tracker.

The range was larger when I did my outlook (35723-509.68). The new range is tighter, as you can see below, which might make you think the bulls are winning. However, the expected Fed Funds rate on 12/18/23 has actually ticked up slightly since by about six basis points. So, I’m always happy when the bulls are vindicated. I always prefer betting on human ingenuity instead of against it; call me sentimental. Still, a little fly in the ointment is despite all the price action and Powell’s choice not to play whack-a-mole with financial conditions; since I wrote my outlook in December, the implied Fed Funds rate at the end of the year has gone up slightly.

This means that even though markets have rallied, they have actually done so as the probability that the Fed will stay “high for longer” has actually increased, at least by the Atlanta Fed’s calculations. Again, this type of fly-in-the-ointment leads to my somewhat conservative criteria for picking longs this year. I want to mitigate risk with my stock picks and ensure that you’re getting a good balance of risk, reward, and safety. In past years, I might have told you to load up on growth and get in line for the big win.

However, given the anomalous events we’ve been through and the intense demand irregularities created by COVID, the sell-side equity analysts (the guys who REALLY know the companies) are entirely at a loss for how best to project earnings in many cases. The normal ways you can orient yourself as to where we are in the business cycle are tricky and unreliable right now. The consumers are strong but also running out of gas, and banks are raising their loan loss reserves. The market is rising, but the Fed is clearly saying “high for longer.” To say there are multiple conflicting indicators would be a generous understatement.

However, while I may be dumb enough to make a forecast, I’m not dumb enough to use that shot in the dark to exclusively guide my long stock picks. Of course, I want names with upside exposure if my prediction is correct, but those with solid enough fundamentals to outperform the market if I’m wrong. So, what I’ve tried to do with my longs is to pick companies with a few different characteristics. Albemarle, the world’s largest lithium miner, meets these criteria. The criteria are:

- Strong competitive position to help insulate against the risks of 2023, including a potential recession.

- Highly visible earnings that are not closely correlated to economic growth and are also accelerating at least through the first half of the year.

- Reliable sources of future demand and the resilience of core revenue drivers to justify a high valuation at a time when the paths of rates (and therefore pressure on multiples) are uncertain.

- Growth is ideally tied to a durable transformational trend that will likely occur significantly regardless of economic conditions and developments on crucial 2023 risks.

Risks to My Bullish Thesis on Albemarle

Making a living digging holes in the ground isn’t for the faint of heart. Even though Albemarle is primely positioned to benefit from the growing demand for Lithium as the Energy transition is heating up, it is still subject to the many risks of the very capital-intensive mining industry. Investing in the wrong assets or messing with CAPEX at the wrong time in the cycle is always a significant concern for any company involved in mining and chemicals. This is part of the reason these companies often have lower multiples. I have already gone over while Albemarle may deserve a higher multiple than some peers, it is still subject to many risks. I believe the three most significant risks are identified below.

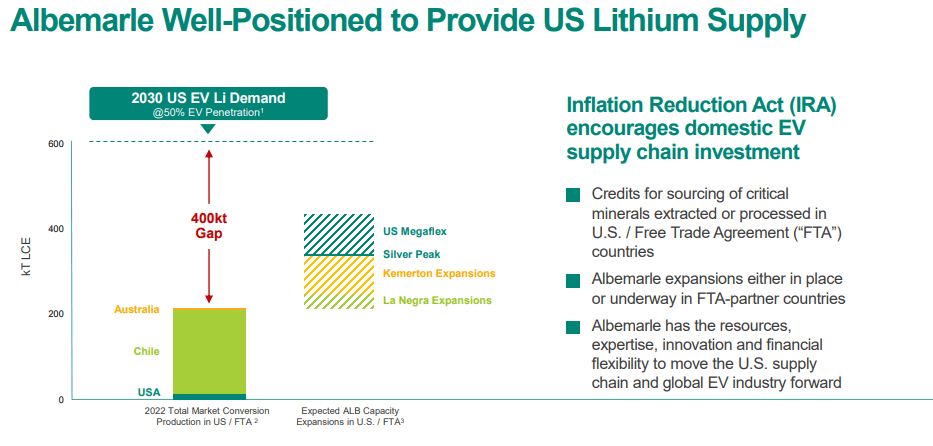

Lower Lithium Prices: One of the lynchpin of the continuation of the bull case for lithium miners like Albemarle is the continued high prices of the underlying commodity. Most of the demand has to do with electric vehicles, so any significant decline in the demand or sales of Electric Vehicles could be problematic. However, one supporting factor is the Inflation Reduction Act, which should give some price support as the government increases incentives to onshore and bolster the security of the renewable supply chain. However, if Lithium prices decline in 2023 more than consensus currently forecasts, there could be a downside for Albemarle.

Company Reports

Rising Awareness of Environmental Externalities in Lithium Mining: As I mentioned in a recent article on the Energy Sector, the rhetoric around the Energy Transition can get quite heated and make it difficult for us, as investors, to reach conclusions about future earnings that are grounded in truth. Whether at the behest of the Oil and Gas Industry or not, there have been mounting environmental concerns around Lithium mining and the potential long-term effects of exponentially increasing demand. This should be mitigated in the short term as the government clearly prioritizes Clean Energy. However, if these issues continue to become more extensive in the public consciousness, there is a distinct possibility that environmental regulation could reduce profitability.

Seeking Alpha

Technological Disruption That Diminishes Electric Vehicle Demand: Right now, Electric Vehicles and the long-term drivers of demand are the key drivers of demand for Lithium at the beginning of a long and complicated supply chain. At the same time, the current trends in batteries have tended to favor more Lithium and more Lithium Hydroxide in particular. Albemarle has invested a lot to meet this elevating demand. If technological trends took a different direction and less Lithium is needed in future batteries, this could make previous investments less profitable and fundamentally alter Albemarle’s increasingly optimistic projections. Similarly, any technology that rises in mobility that significantly displaces current EV demand projections could result in much less growth for Albemarle than is currently forecasted.

EVAdoption.com

Conclusion

Albemarle is a leader in its industry, has highly visible revenue that is growing faster than the market, and it is a beneficiary of one of the most significant transformational trends of our time. While this company currently trades at multiples comparable to many peers, I believe its consistent growth and improving prospects will likely lead to a multiple expansion, particularly if the Fed pivots sooner than is currently expected by the dot plot.

Seeking Alpha

While Albemarle Corporation has certainly been overvalued at times during the last year, it has come back down to Earth over recent months. This name has a lot of advantageous characteristics for surviving the 2023 risk environment. The stock should be poised to continue delivering to shareholders. One of my favorite parts about this company is that the management continues executing capital spending that builds shareholder value. They have built assets for a world that needs their underlying commodity a lot more. The bromine and catalyst segments are “red-headed” stepchildren compared to lithium, but they are strong businesses in their own right. Pick Albemarle Corporation for a “picks and shovels” way to play the increasingly important Energy Transition and decarbonization of the global economy.

Be the first to comment