watthanakul/iStock via Getty Images

All values are in CAD unless noted otherwise. This company’s stock ownership is generally restricted to Canadians.

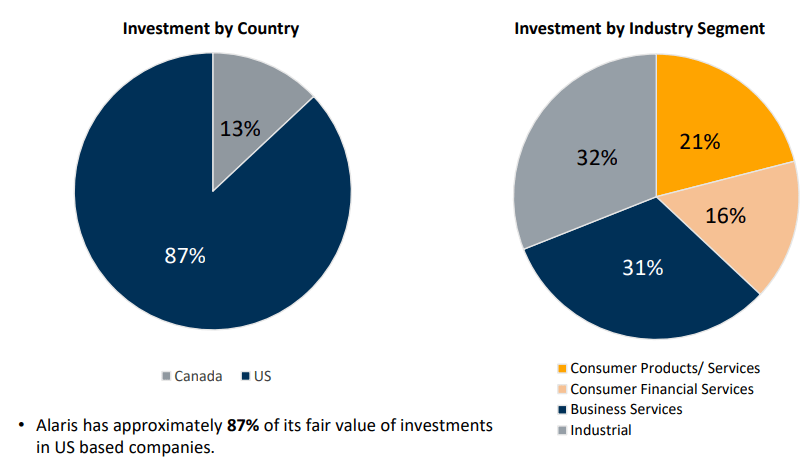

Alaris Equity Partners Income Trust (TSX:AD.UN:CA) provides financing to private businesses in North America. The trust primarily uses the preferred equity route; however, it also finances via common equity, subordinated debt and promissory notes. On a fair value basis, most of its footprint is on the other side of the pond, with investments in varied businesses.

November 2022 Presentation

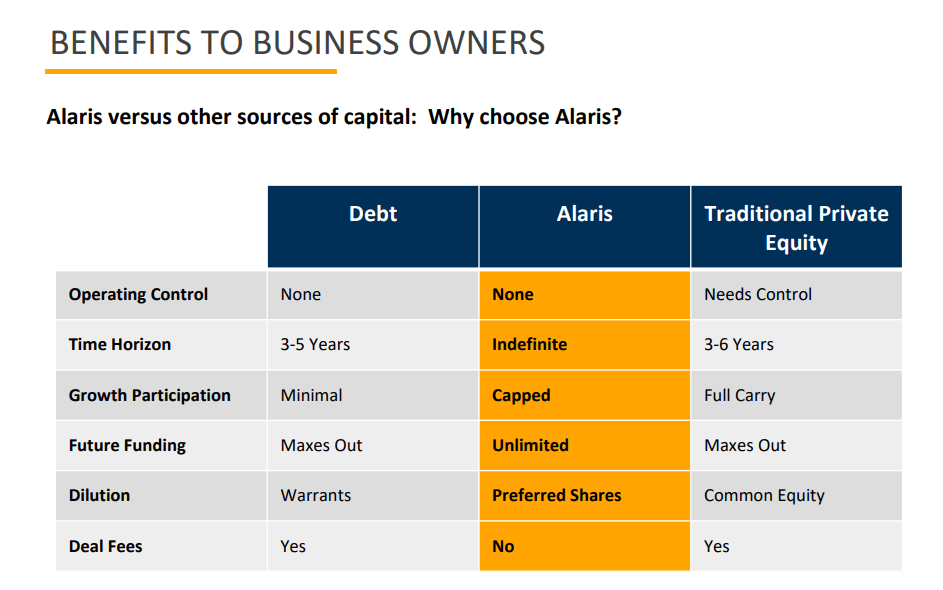

The payments to Alaris, be it dividends or interest, are determined in advance annually and paid monthly or quarterly. The payments are based on the top line measures of the private companies such as gross revenue, gross profit, same store sales and they are subject to an annual audit. Besides dividends and interest, at times Alaris also participates in capital gains via equity appreciation and premium on exit/redemption of preferred equity. Alaris points out this structure has advantages to both sides and fits between traditional private equity and debt.

November 2022 Presentation

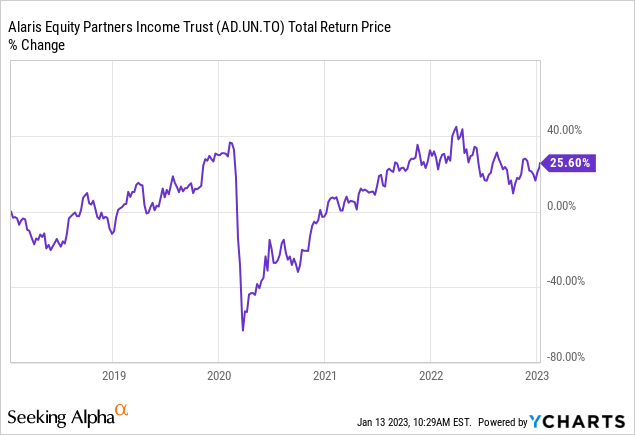

Being an investment vehicle, the trust has limited expenses and boasts about having only 17 employees. Alaris has yielded around 8% over the last few years and that has helped it navigate the pandemic period. Investors holding it over 5 years have a decent return to show for it.

Recent Results

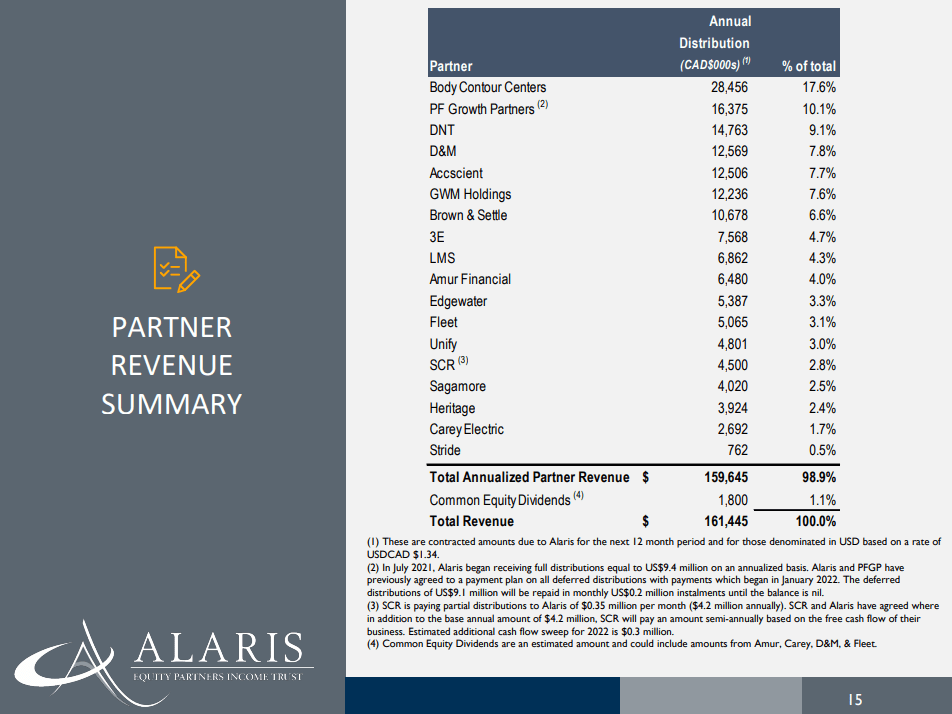

The most recent quarterly results show a diversified base of partners, but there is some concentration in the top names.

November 2022 Presentation

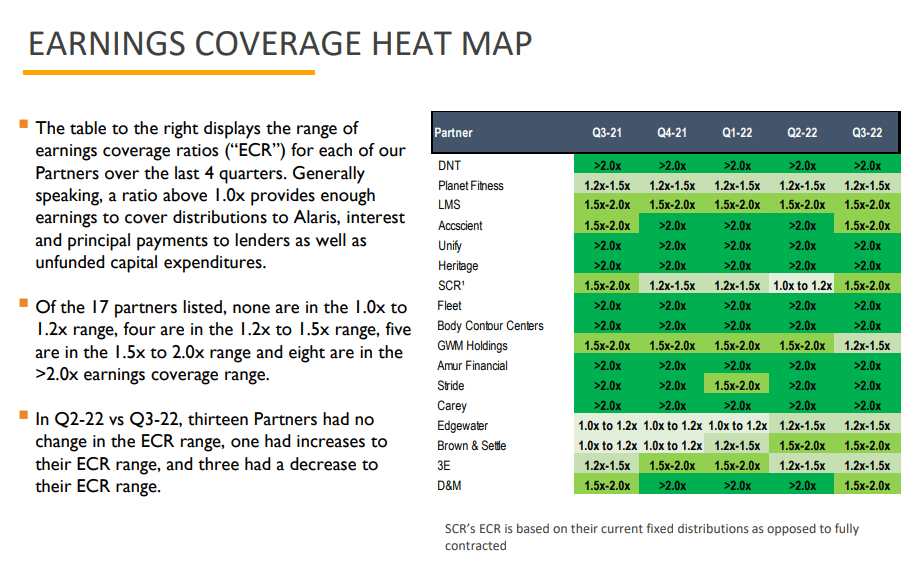

The main feature of the Alaris report is the earnings coverage heat map. This shows how well the current distribution paid by the partners, to Alaris, is covered by their own earnings. Having followed this company for some time now, we can say that the current distribution coverage is one of the best we have seen.

November 2022 Presentation

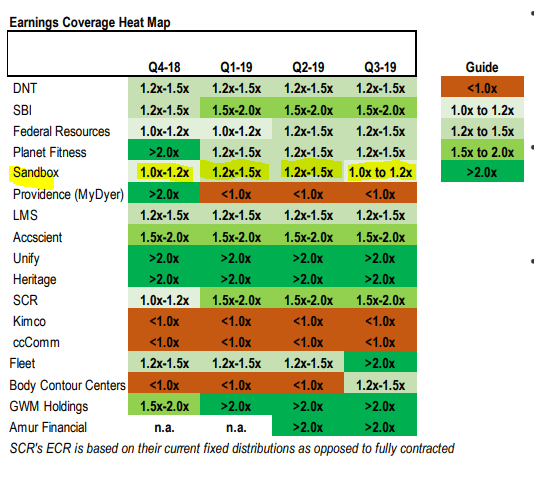

The startling number of partners that are over 2.0X coverage is very comforting. Not a single one is below 1.0X. Some recent followers might not be aware but Alaris has routinely had problems in this area in the past. Here is the same heat map from Q3-2019, a time arguably free of any discomfort for the economy.

November 2019 Presentation

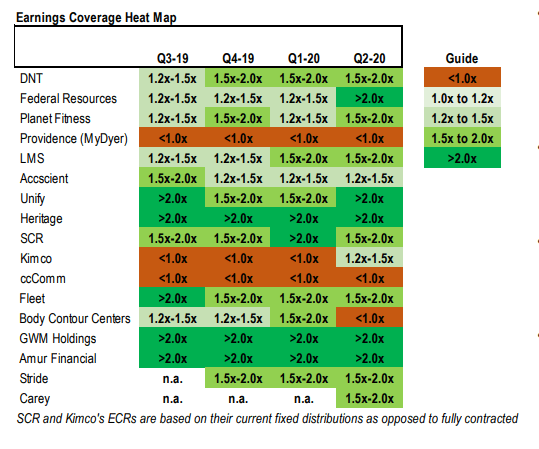

Here is another one, from Q2-2020.

November 2020 Presentation

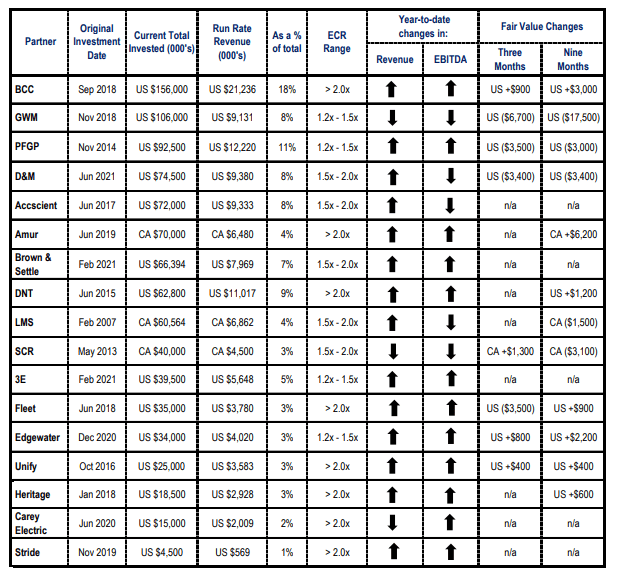

Sub 1.0X partners were a frequent occurrence and the current setup looks really good. Another way to examine the health of the individual partners is to look at their own revenue and EBITDA trends year to date.

Q3-2022 Financial Statements

Most outside of SCR, are moving in the right direction.

These amounts paid are reset every year so that likely decreases coverage ratios slightly, of course with the benefit of paying more to Alaris.

November 2022 Presentation

Valuation

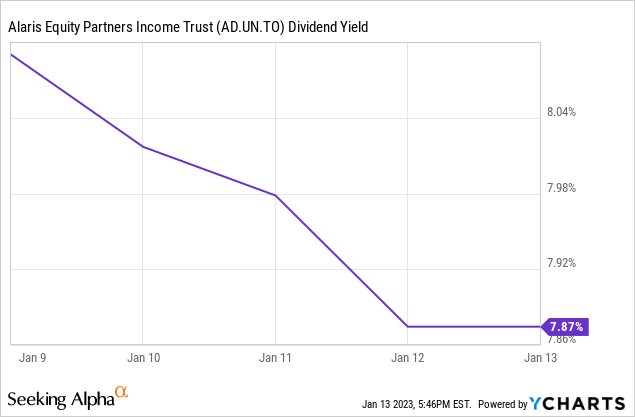

The key appeal for investing in Alaris comes from its rather large distribution yield.

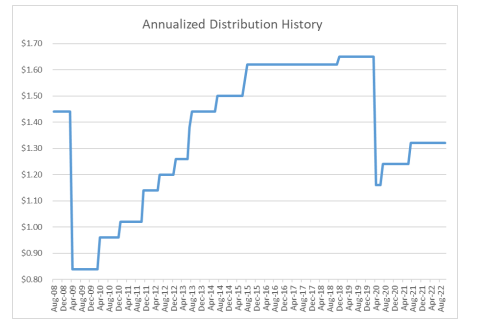

While that yield is appealing, investors have twice got hit on the head with a large cut in the payment. Alaris is not at all shy about presenting this to everyone.

November 2022 Presentation

There are few factors here that make the current yield far more sustainable than it has been in the past. The first being obviously the exceptional earnings coverage. The second being the payout ratio. Alaris frequently flirted with 90% plus payout ratios in the past. Today, it appears, they have done away with that old model in its entirety.

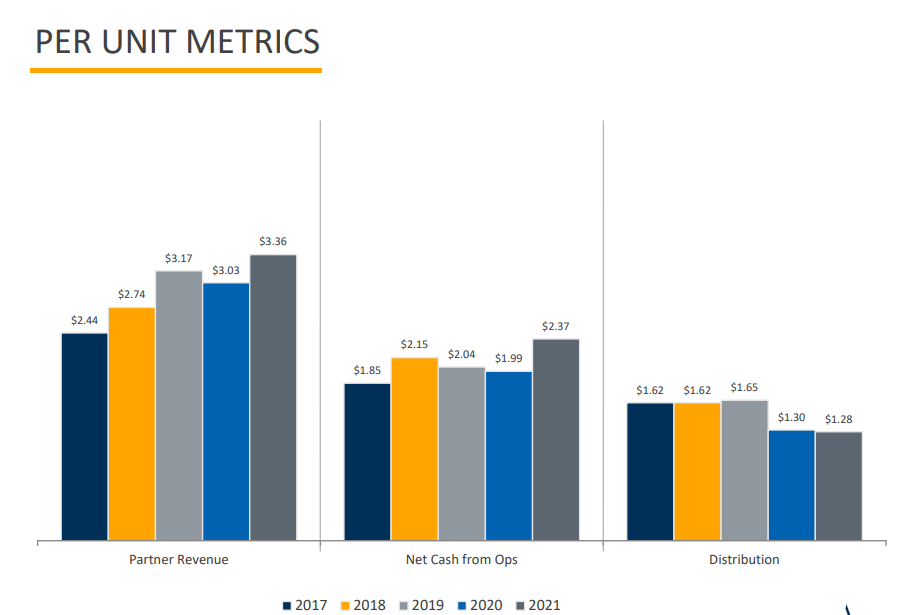

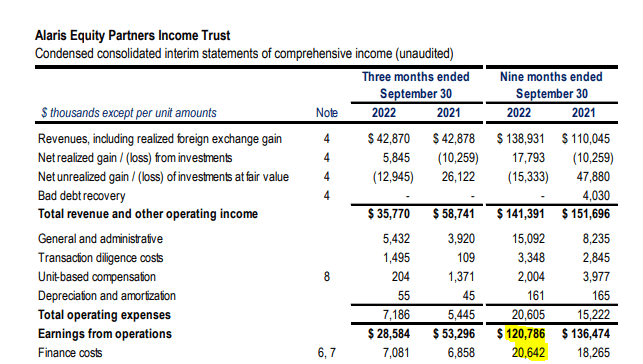

The Actual Payout Ratio (2) for Alaris for the nine months ended September 30, 2022 was 45%, an improvement from 52% in the comparable period of 2021, primarily as a result of the improvements in revenue per unit noted above.

Source: Alaris Q3-2022 Financial Statements

Cash from operations before changes in working capital will now be close to $3.50/share. Just compare that number with the dividends paid in previous years.

November 2022 Presentation

This massive improvement has stemmed from a combination of factors. The first being retention of earnings and further investments, which have enhanced cash flow. The second and more important reason is the conversion to a Trust, which has eliminated (more or less) the income taxes. The latter can ding the investor harder, as they have to pay more taxes on receipt. The distribution is no longer a “dividend” and does not qualify for the eligible dividend tax credit.

November 2022 Presentation

So in that sense this is a huge whammy to people who were previously getting $1.65 per share, being taxed at a low rate. Now it is $1.32, being taxed at a far higher rate. We have not given specifics of the exact tax rates on old eligible dividend as that depends on personal marginal tax rates.

How Alaris Can Make You Some Dough

All said and done though there are things to love about this new model. First is that you no longer have to worry about a distribution cut, thanks to how well the company is doing and how little they are paying. The second is that these same shares can be held inside a TFSA or RRSP in Canada and dodge the tax hit completely. Where else can you get a 7.8% yield with a 50% payout ratio and partners who cover the distributions so well?

An extension of this is to consider an investment in the TSX listed debentures. Alaris has two debentures AD.DB:CA, and AD.DB.A:CA. The AD.DB:CA matures in June 2024 and has a 7% yield to maturity. It is also convertible into common units at $24.25 (a price unlikely to be reached in the time horizon). The AD.DB.A:CA matures in March 2027 and has a 7.86% yield to maturity. Alongside exceptionally coverage of the distribution, it is worth noting that the company covers its finance costs by a huge margin.

Q3-2022 Financials

Total net debt to EBITDA is under 3.0X. This mitigates any recessionary risk in our opinion. We think both sets of debentures are really safe and can form parts of diversified portfolio looking to take very little risk.

Verdict

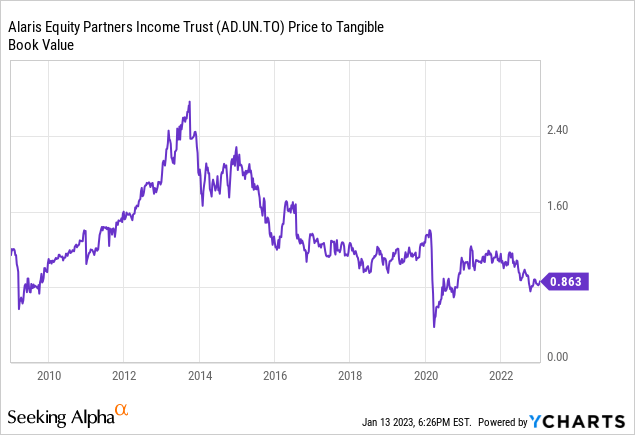

Alaris has failed to find a new investor base after the move to becoming an income trust. The current price to operating cash flow is the at the lowest multiple outside of the COVID-19 crash. The current price to tangible book value is also showing a similar symptom.

Gone are the days of euphoria at 2.5X tangible book value. What we are left with is a beaten down company with gobs of free cash flow. The stock is worth considering for tax deferred Canadian accounts and the debentures are even stronger plays for those that emphasize safety. We own the debentures and will consider the common units if we get the right setup.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment