ipopba

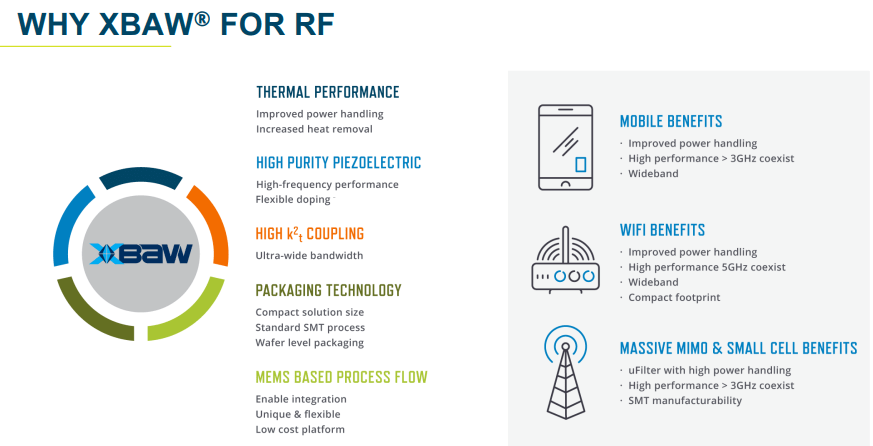

Akoustis Technologies (NASDAQ:AKTS) is a designer and producer of cutting-edge RF filters based on its proprietary XBAW technology (which we described in greater detail here and here), but is summarized in a slide from their December 2022 IR Presentation:

AKTS IR presentation

These filters go into a host of devices like mobile phones, WiFi hotspots, telecom infrastructure, and defense applications. Recently two new markets have opened up for the company, gaming and the timing and frequency market (where we have another stock, SiTime (SITM)).

The company is starting to gain significant traction with numerous design wins and an increasing number of customers already in the production phase. Two new customers entered into production in Q1/23 (the September quarter) for a total of 15 and another 4 are expected to add to this in Q2/23.

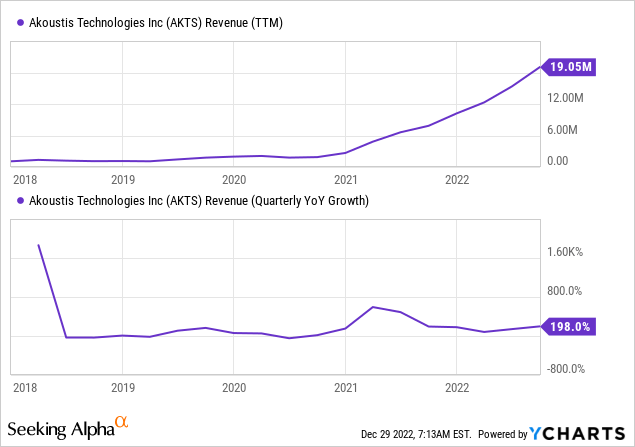

Revenue growth is well in triple-digit territory, although from a small base:

The company’s revenues could have grown even faster if not for some considerable macro headwinds, mostly confined to their WiFi segment where supply chain problems keep some customers from fully ramping up production.

Growth

The most important growth drivers are:

- Design wins

- Repeat customers

- Mobile

- Increasing content

- Own production of WLP

- New markets

- CHIPS Act

The company supplies to a number of different segments:

- WiFi

- 5G Mobile

- Network Infrastructure

- Other

WiFi

AKTS IR presentation

The supply chain problems are concentrated in their biggest market, which is unfortunate as most of the customers that are already in production come from this segment (10 out of a total of 15).

The company now has 20 design wins here with three new wins in Q1/23. They were early entrants in WiFi 6/6E/7, which explains these design wins, apart from the superior XBAW technology.

However, management argues there are signs that these supply bottlenecks are starting to ease and management expects an accelerated ramp from customers next year.

The company produced 4 new filters, two of which with a significantly reduced form factor (the 5.6 and 6.6 GHz coexistence filters), and now has 16 XBAW Wi-Fi filters, 12 for Wi-Fi 6E and Wi-Fi 7 and 4 for Wi-Fi 6.

The company gained three new design wins in Q1/23 (the September quarter) and expects new design wins for the four new filters and production by the June/23 quarter.

There was also a development order from a Fortune 100 company for their new diplexer products for WiFi 7 applications which they are already developing for one of the largest PC chipset makers. Other OEMs also expressed an interest.

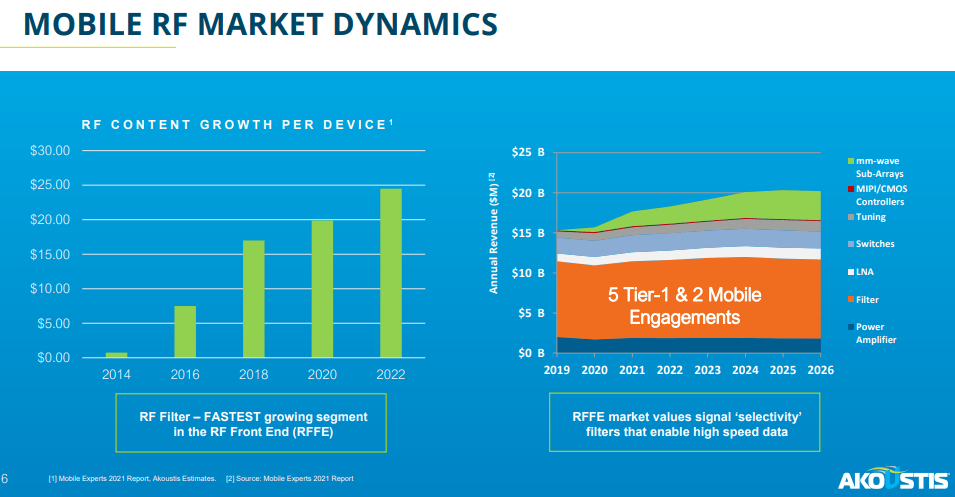

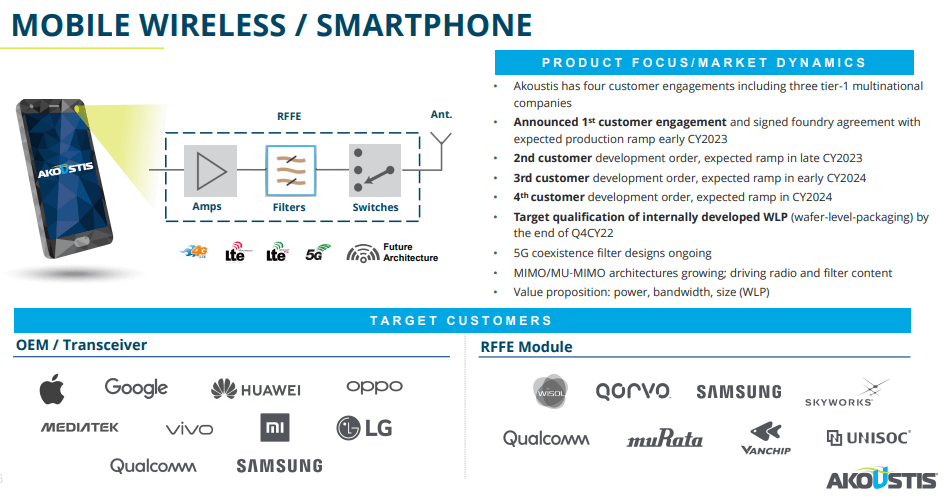

5G Mobile

AKTS IR presentation

While WiFi is probably their biggest segment right now (there is no revenue split out), the potential for the 5G mobile market dwarfs WiFi (given the number of mobile phones).

Apart from making inroads, there is also a sustained increase in content per device (see graph above) due to the increasing complexity of filters and the rise in the number of filters per device.

The company has multiple customer-funded XBAW filters in design with four customer engagements, including three Tier 1 customers. Here is how they summarized developments in the quarter (Q1CC):

We received our first purchase order from a Tier 1 RF module maker customer that we engaged with last December.

We iterated our first RF filter design for a Tier 2 foundry customer and received a purchase order for two additional filters.

We received a volume order from a Tier 1 RF component company for an expected production ramp in the first half of calendar 2023.

And finally, we have completed the process flow for our new WLP and chip scale package products and have design locked the first WLP for our Tier 1 RF component company customer.

The orders are comparable in size to what’s happening in their WiFi segment, but they are likely to increase an order of magnitude

AKTS IR presentation

And just as we’re about to publish this article they actually converted a big deal in the 5G mobile space. This is very good news, for the following reasons (company PR):

This is our first design win for the 5G mobile market that is planned to ramp production in the first half of CY2023, supporting selectivity demands in the 3 to 7GHz 5G/WiFi spectrum. Further, it is our first product that leverages our new proprietary wafer-level-package technology, which is significantly smaller than our current packages and superior in back-end manufacturing cost.

The Tier 1 client is also considering additional applications:

The customer is considering additional applications for XBAW® in future modules for 5G smartphones, tablets, wearables, and other mobile devices after the successful completion of this first solution.

The company is entering the big league with this.

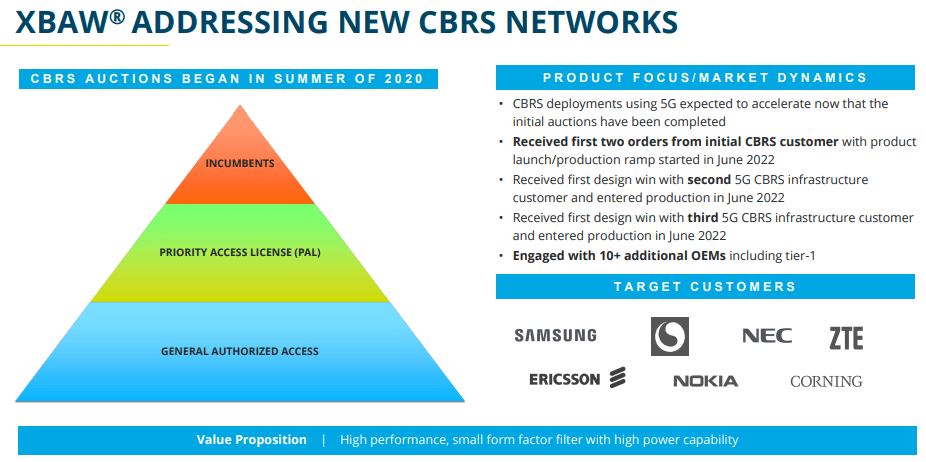

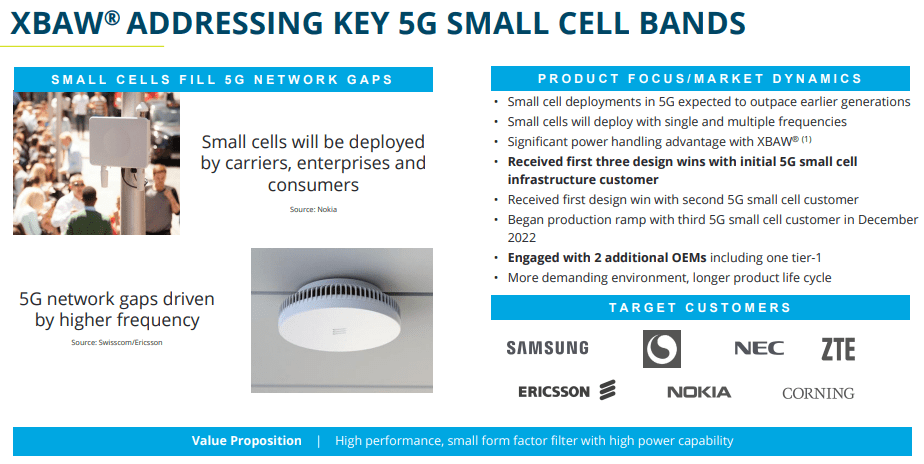

Network Infrastructure

AKTS IR presentation

The company has four design wins for CBRS (unlicensed Citizens Broadband Radio Service) network customers and five design wins in 5G small cell, one of these this quarter which is expected to ramp at the end of this year.

Three CBRS customers are ramping production, one on high volume, and the two others on low to mid-volume with multiple filters per device.

AKTS IR presentation

Other business

The company has two R&D contracts with DARPA, one of these new this year. The completion of the acquisition of RFMi in July/22 is also producing results with a significant design win from a leading IC supplier.

New segments

The company has entered two new segments:

- In the gaming they won two design wins in Q1, both of which will go into production mid-next year.

- The company also entered the timing and frequency market with their XBAW resonators, working with the producer of timing RF components and starting the qualification for their first two timing control products with their first customer, who is expected to start production in H1/23 and there is already a development order from a second customer.

Wafer Level Packaging

The company has developed its proprietary WLP solution in its NY fab facility and has completed qualification for the 5G mobile, Wi-Fi, timing control, and other markets. From the December 21 PR:

The qualification of this new, advanced WLP process and packages enables smaller form factors, lower cost and will open significant high-volume markets to Akoustis including 5G smartphones, tablets and computing, representing the largest revenue opportunities for our XBAW® technology.”

The company already has a design win for a Tier 1 RF component company. The advantages of taking the production in-house are (Q1CC):

We believe bringing the WLP process in-house enhances substantially our ability to control the quality, cost and customization of our advanced packages.

CHIPS Act

The company will apply early next year for funds from the CHIPS Act for two projects:

- Multiple new 8-inch silicon wafer manufacturing lines in their NY site

- Build an advanced packaging center (restoring).

Funding, which could arrive by mid-2023, would position Akoustis to make a leap in production capacity and manufacture and deliver billions of XBAW filter chips annually.

This can propel them make the leap servicing Tier 1 and Tier 2 mobile companies for 5G smartphones and other multibillion-dollar end markets, including 5G networks, high-frequency Wi-Fi devices and other wireless markets.

Senator Schumer has already visited their NY facility twice recently and has a blueprint to make NY a global innovation and semiconductor hub. The company fits very nicely in those plans.

Finances

This is the part where the problems lie. While the company is scaling up production very fast (which depends on customers scaling up their production), the scale is still not near enough for the company to stop the cash bleed. Some data:

- Revenues +6% q/q and +195% y/y to $5.6M

- GAAP OpEx loss $18M, non-GAAP $15.6M

- CapEx $4.8M, down from $5.9M in Q4/22

- OpEx cash $15M used, up from $11.9M in Q4/22

- Cash $60.7M, down from $80.5M Q4/22

- Q2 guidance, multiple customers ramping WiFi and network infrastructure, revenue +5%-10% q/q and +55%-70% y/y with operating cash burn at least 25% lower

The company is going to pace some CapEx and guides operational cash burn 25% lower in Q2 so cash outflow will be in the order of $15M. If cash burn doesn’t decline further it gives them three quarters to burn through all of it.

We do expect cash burn to keep decreasing on the basis of more customers ramping production and WiFi supply constraints easing. But in any case they will need to go to the markets for the production line and plants they want to build, although these would be greatly helped by CHIPS Act funding.

Valuation

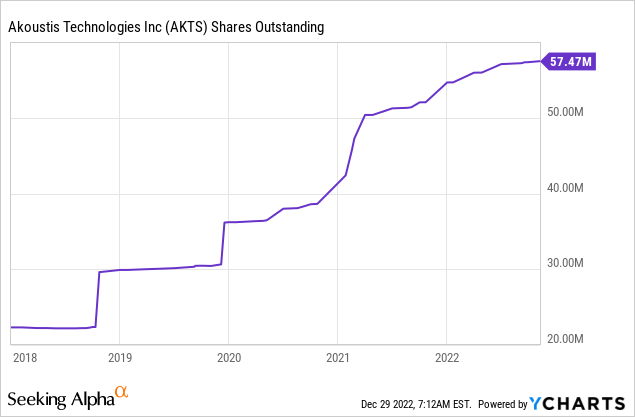

There is quite a bit of dilution on the way, from the 10-Q:

AKTS Q3-22 10-Q

So at $2.60 a share the company has a market cap of $182M which amounts to 6.7x sales (The company has $43.85M in notes outstanding but the conversion of these into shares is already included in the calculations).

On the FY24 (ending in June/24), this is halved to 3.35x as revenue is expected to double to $54.1M.

Conclusion

- The company is raking in design wins and companies that move into production (15 already, over 25 by the end of next year according to management) based on their superior XBAW technology, which it keeps improving.

- There are short-term headwinds in their biggest segment due to supply chain problems, but these are easing and management expects an accelerated ramp next year.

- It is also gaining in network infrastructure, defense (two DARPA contracts)

- The company has huge potential in the 5G mobile market which dwarfs that of WiFi and has now its first big win in this space, propelling the company to the big league.

- The company is making inroads in new markets, like gaming and timing.

- The dollar content of many of the end products for their filters is increasing due to the increasing sophistication of the filters and the increasing number of filters per device.

- The company is likely to benefit considerably from the CHIPS Act for funding additional production lines and a new WLP plant which would propel the company on a new plane and enable it to service volume demand from the biggest customers as well as design and produce the packaging in-house, which will boost margins.

- Even with CHIPS Act funding, the company is likely to need new finance somewhere next year.

Basically, the company is set to make a big leap next year if they can finance their expansion plans as the interest from customers is there, but we first have to pass a funding hobble.

Be the first to comment