JL Images/iStock Editorial via Getty Images

Our most devoted readers know that we are both following Air Liquide (OTCPK:AIQUF, OTCPK:AIQUY) and Air Products and Chemicals (NYSE:APD). We are currently long on both. This next Thursday, the American company will report its three-month numbers, whereas last week it was Air Liquide time, and today we provide the Q2 quarterly analysis. Over this period, we intensively cover the French specialty gas operator and today we won’t do our usual buy case recap, here below our main publications so you can cherry pick:

- 24/03/2022 – Initiation of coverage with our long-term thesis and secular growth opportunity – we also included the valuation;

- 27/04/2022 – Q1 results comment and recent project development analysis;

- 16/06/2022 – our feedback versus Wall Street view and expectations. Plus, we include the hydrogen mobility opportunity.

Q2 Results

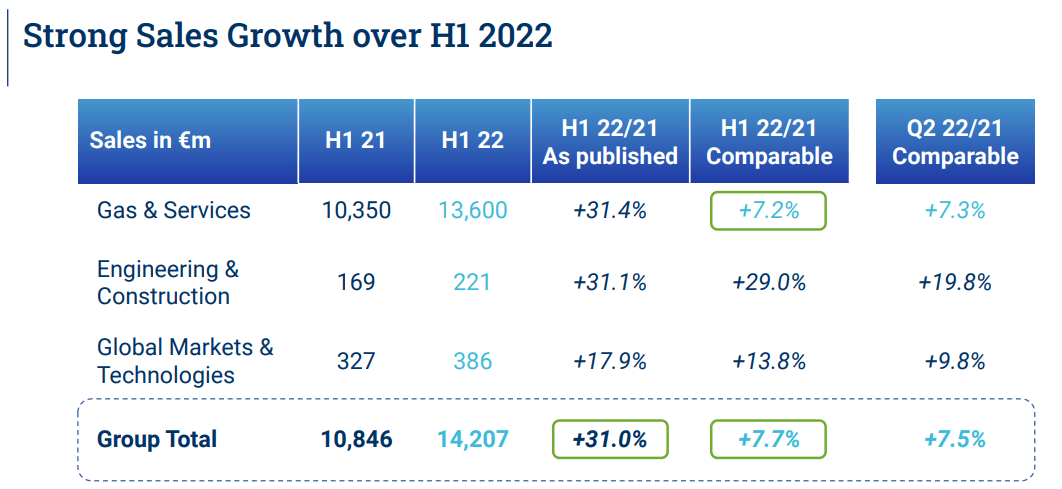

Starting from the top-line sales, the French player recorded a growth of 7.7% on a like-for-like basis between the first half of 2021 and the first half of 2022, reaching €14.20 billion (compared to €10.84 billion a year ago). Regarding the Engineering and Construction division, the main highlight was the higher order intake. The company revenue line beats the consensus expectation. Despite the ongoing energy crisis, the current operating income was €2.28 billion compared to €1.94 billion. Looking at the specifics, the group’s operating margin increased by 50 basis points arriving at 18.5% excluding energy. Here again, operating profit was 2% ahead of consensus.

Air Liquide revenue line

Source: Air Liquide Q2 results

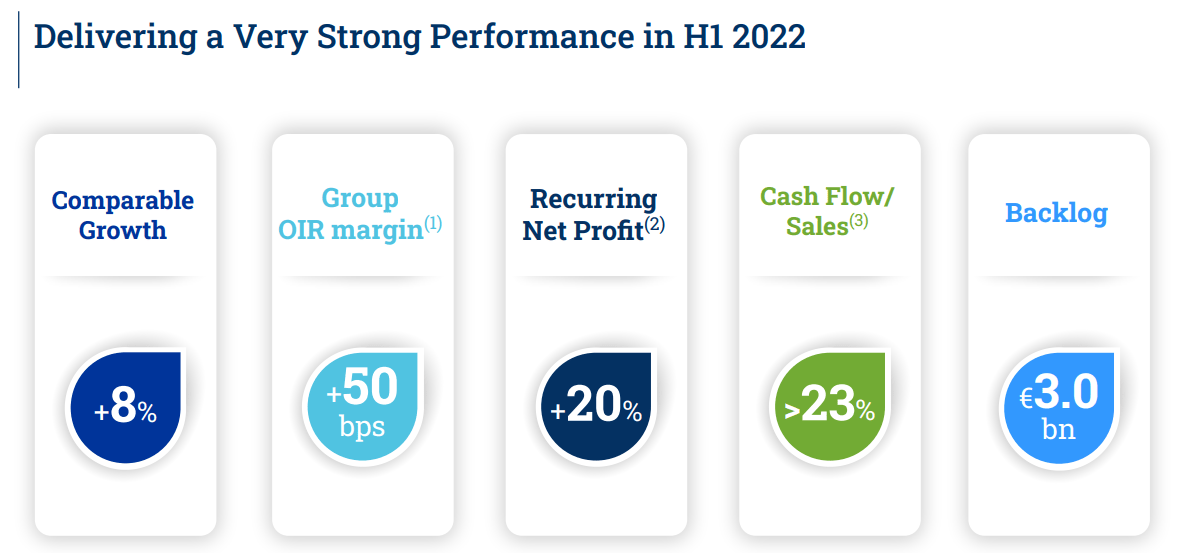

Going deeper into the analysis and double-checking the regions, America’s margins significantly increased (again ex-energy), and the performance was up by almost 20% over the period. This was due to higher efficiencies, a product mix versus the large industries (they are called LI in the presentation) and also thanks to positive electronics development. Whereas in Asia, the margin decreased for the Chinese prolonged restrictions. This was partially offset by the strong contribution that happened also in the Americas namely LI and electronics. Looking at European margins, performance was positive thanks to the portfolio disinvestment and the good underline results achieved in the healthcare sales.

Higher investments are expected in the coming years, we should note that the backlog remains at €3 billion with a €400 million decline compared to the numbers seen in quarter one. This was due to Russia and a few startups’ projects being deleted.

Air Liquide financial snap

Source: Air Liquide Q2 results

Valuation and Conclusion

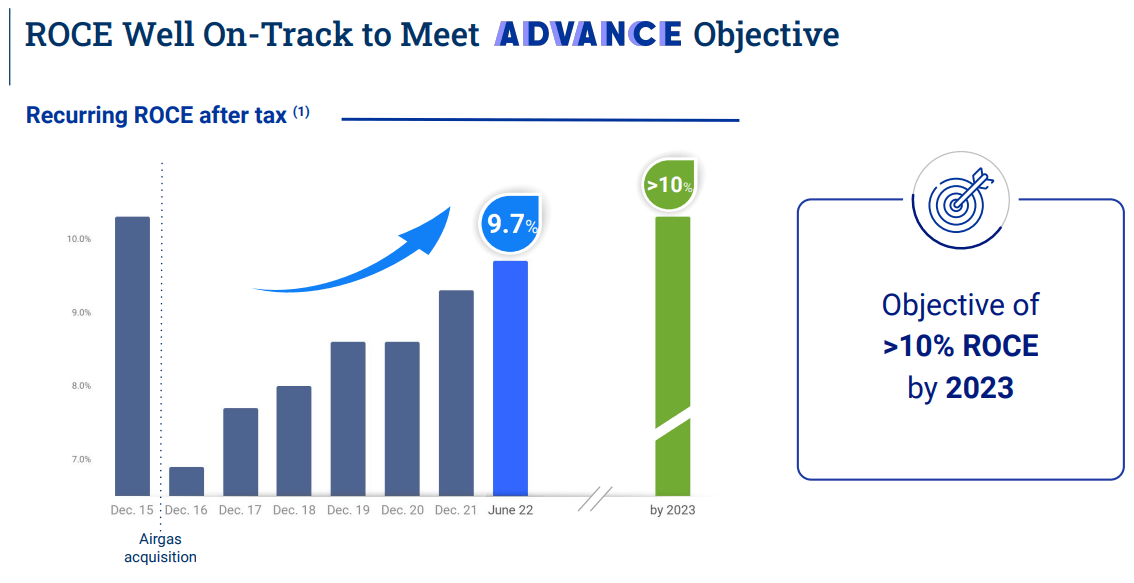

Air Liquide group confirmed its outlook for 2022. Last time, we were writing that half-year results were the company’s key turning point. Looking at the stock price appreciation, this is exactly what happened. We think that Wall Street needs to give some credit to the French group and should update their estimates. The ROCE (after tax) stood at 9.7% signing a plus 40 basis point versus last December and which was in line with the ADVANCE strategic plan presented. Therefore, we reaffirm our buy rating with a price target of €190. Adjusting the P/E estimates, we see a 25% discount compared to Linde and a 10% discount with Air Products & Chemicals.

Air Liquide ROCE

Source: Air Liquide Q2 results

Mare Evidence Lab’s previous coverage on APD: Great Mix between Value and Growth

Be the first to comment