Sjo

Ahead of the half-year results, we published our first article on Air France-KLM (AFRAF; AFLYY) with an explicit no-go opportunity. From time to time, we made mistakes (lucky for us, we do have a supportive investment track record), but this time we really hope you followed our advice.

Air France-KLM: Currently A No Go

Source: Mare Evidence Lab’s previous publication

Last time, we anticipated the following:

- A supportive travel rebound in Q2 and a “V-shape recovery from pre-COVID-19 level” for the summer season

- A 40% discount to the stock price level due to the capital increase

Q2 results

Looking at the results and starting with the revenue line, Air France-KLM recorded €6.7 billion in sales, up 143.9% year-on-year. The group’s operating result was €386 million compared to a loss of €753 million over the same period of 2021. After several successive quarters of losses that forced Air France-KLM to take out loans from the French and Dutch states, the group recorded a net profit of €324 million against a loss of €1.49 billion a year earlier. To be precise, Air France-KLM had not generated a positive net result since the fourth quarter of 2019.

According to a consensus available on the company’s website, analysts on average expected revenue of €6.27 billion, an operating profit of €141 million and a net loss of €36 million. Thus, the company exceeded all the Wall Street analyst’s expectations. FCF was also positive in the period and net debt was reduced. The company also indicated plans to issue hybrid bonds for a total consideration of €1.2 billion under favorable market conditions.

Air France-KLM financial snap

Source: Air France-KLM Q2 press release

Conclusion

Although the chaos in the airports is affecting the holidays of those who are leaving these days, passengers want only one thing: to leave for vacation as soon as possible and reach family and friends.

The airline group Air France-KLM announced that it expects to achieve a “clearly positive” operating result in the third quarter and a “positive” result for the whole of 2022, which would be the first since the 2019 financial year.

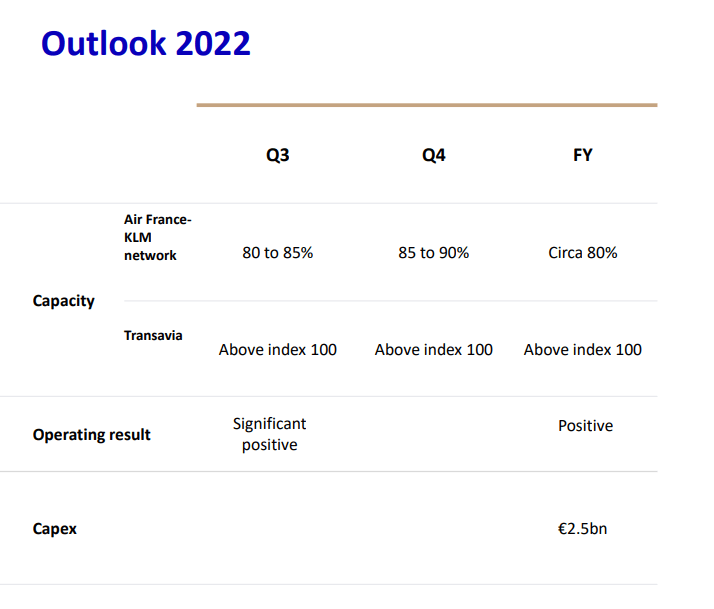

However, Air France-KLM was forced to revise downwards its capacity forecast for the third quarter. The group forecast a passenger capacity between 80% and 85% against a previous target range estimated at 85% to 90%.

Air France-KLM guidance

Source: Air France-KLM Q2 results

This revision is due to the operational difficulties imposed by some airports such as London Heathrow and Amsterdam Shiphol (KLM hub). These difficulties resulted in additional customer compensation costs of €70 million. On one hand, delays and cancellations have reduced the number of passengers, on the other hand, the company also increased the fares of air tickets with a future positive impact on the underlying profitability. Of course, the airline companies have attributed these inconveniences mainly to airports which, due to lack of staff, have imposed limits on flights. However, airlines have been accused of selling airline tickets despite knowing that flights could not be made, causing inconvenience to passengers who were forced to reschedule their flights, often after arriving at the airport. If this is proved by regulators, airline companies might be exposed to pretty high fines. After having carefully analyzed the half-year report, we conclude that Air France-KLM is fairly priced at this level. Thus, we reaffirm our neutral rating, favoring the following companies:

- Deutsche Post: Strong Results And A New Buy In Our List

- Ryanair Is Set To Fly

The risk paragraph was included in our previous company publication.

Be the first to comment