skynesher/iStock via Getty Images

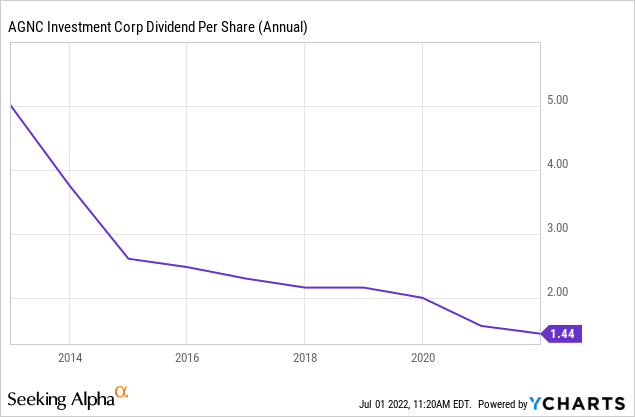

AGNC Investment Corp. (NASDAQ:AGNC) has a history of cutting dividends, and a new round of book value losses and declining income could force the mortgage trust to cut its dividend yet again.

AGNC Investment currently trades at a 12.6% yield, indicating that investors are becoming more concerned about the possibility of another dividend cut.

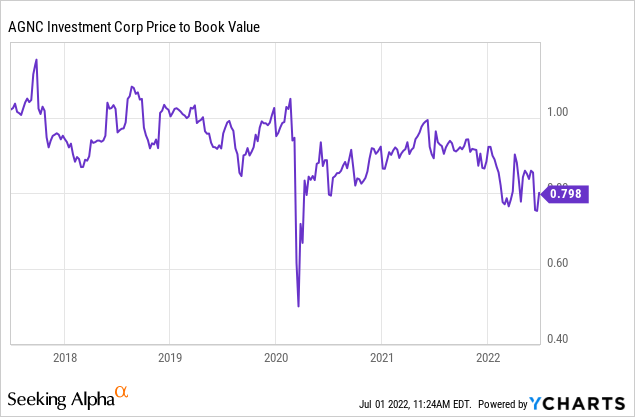

Given AGNC Investment’s large book value loss in the first quarter and rising risks to leveraged trust funding costs, investors should expect AGNC to trade at a lower valuation (P/B-multiple) in the future.

The Central Bank Is Moving Aggressively On The Interest Rate Front

Inflation has become a serious problem not only for consumers, but also for corporations, which are affected by inflation/interest rates in two ways: they are forced to deal with higher borrowing costs, implying lower margins, and higher interest rate costs make debt-driven business models, such as AGNC Investment’s, more expensive.

In May, inflation rose at an annual rate of 8.6%, prompting the central bank to finally respond by raising benchmark interest rates by 0.75 percentage points in June. It was the largest increase in interest rates in 28 years.

Because inflation remains completely out of control, the central bank is likely to continue aggressively raising interest rates in 2022. Two weeks ago, Federal Reserve Chair Jerome Powell expressed support for another 0.75 percentage-point increase in benchmark interest rates in July, which would counteract inflation on the one hand while making debt servicing more expensive for businesses that rely on it on the other.

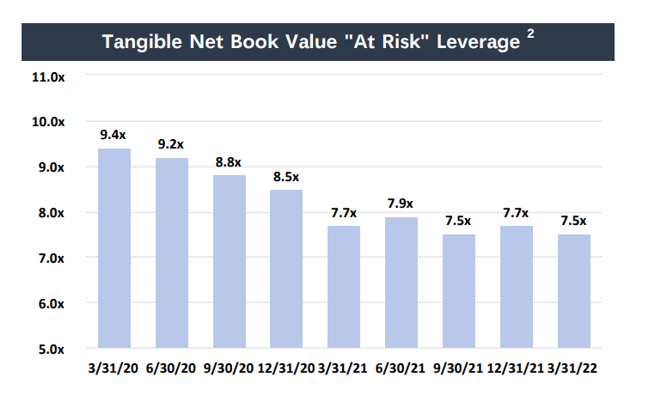

Mortgage trusts such as AGNC Investment rely on debt, despite the fact that the mortgage trust has already reduced its leverage from 9.4x on March 31, 2020, to 7.5x on March 31, 2022. AGNC Investment’s leverage ratio remains high.

Tangible Net Book Value Leverage (AGNC Investment Corp)

Book Value Losses And Multiple

Higher interest rates will make AGNC Investment’s business more expensive, especially given the trust’s reliance on debt to acquire mortgage assets.

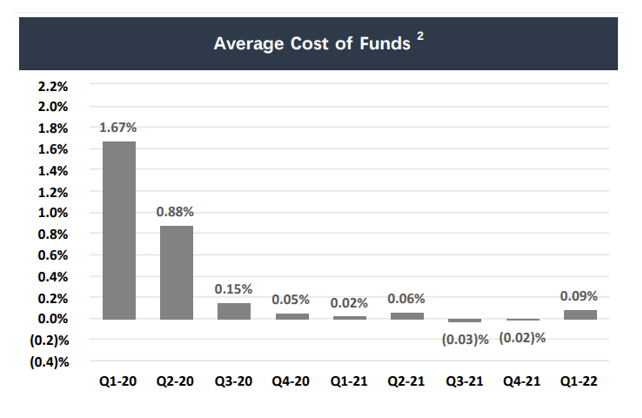

AGNC Investment has benefited greatly from the central bank’s loose monetary policy during the Covid-19 pandemic, but borrowing costs began to rise in 1Q-22 and will continue to rise, implying a lower net interest spread for the mortgage trust in the future.

The average cost of funds for the trust should rise further in the second quarter. If funding costs continue to rise, AGNC Investment may be forced to reduce its payout once more.

Average Cost Of Funds (AGNC Investment Corp)

AGNC Investment has cut its dividend more than once before.

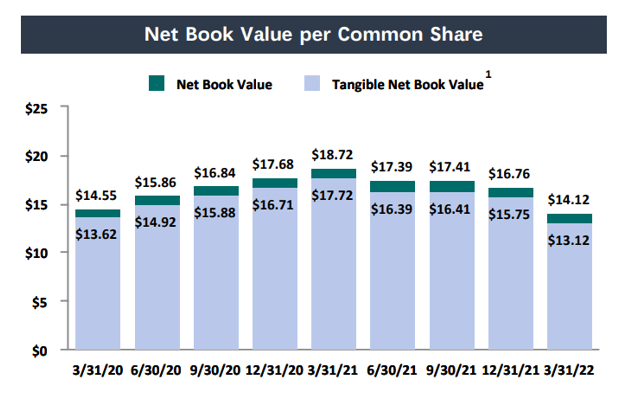

Regrettably, significant changes in the central bank’s interest rate policy during the first quarter resulted in a significant book value loss for AGNC Investment.

The mortgage trust had to report a 16% QoQ decrease in book value, finishing the quarter with a book value of only $14.12 per share. AGNC Investments’ book value has decreased by 25% since March 31, 2021.

It’s pretty devastating for a mortgage trust to lose 25% of its book value in a year, and it should convince dividend investors that neither AGNC Investment’s book value nor dividend are sustainable.

Net Book Value Per Common Share (AGNC Investment Corp)

Given the risks of higher funding costs and lower net interest spreads in the future, as well as AGNC Investment’s negative book value trend over the last year, the trust should trade at a much larger book value discount than the 21% we currently see. AGNC Investment’s book value is likely to fall again in 2Q-22, implying that the effective book value discount is less than 20%.

Why AGNC Could See A Higher Valuation

Higher interest rates are a drag on the corporate sector in general, but mortgage trusts in particular because they rely so heavily on cheap debt to buy mortgage assets and profit from the spread between borrowing costs and investment yields.

If the central bank abruptly decided to stop raising interest rates, perhaps to prevent the economy from entering a recession, mortgage trusts could see renewed investor interest and lower book value discounts.

My Conclusion

Mortgage trusts are in peril right now. Interest rates are expected to rise further in 2022, requiring mortgage trusts like AGNC Investment to absorb a significant increase in funding costs, which will eat into profits. Because the central bank is expected to raise interest rates further, AGNC Investment’s net interest spread may contract, necessitating another dividend cut.

These rate hikes are a problem for trusts like AGNC Investment, which has been a serial dividend cutter, and could lead to even larger book value losses in the coming quarters.

I don’t believe AGNC Investment’s dividend is particularly safe here, and investors must prepare for yet another dividend cut in 2022.

Be the first to comment