DNY59

(This article was co-produced with Hoya Capital Real Estate)

Introduction

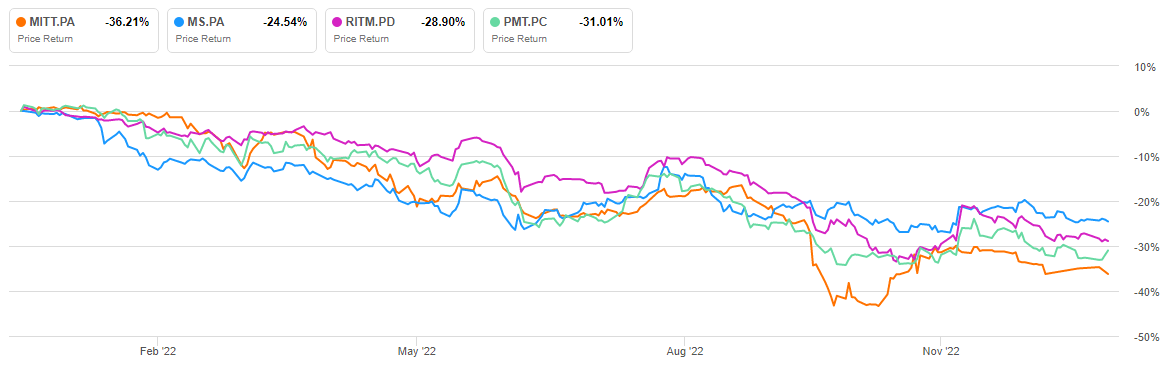

Based on the number of contributors reviewing preferred stocks, especially those issued by mREITs, there is a definite interest in these depressed, high yielding assets. Considering the FOMC just raised the Federal Funds Rate for the 7th time, along with an apparently higher terminal rate, why these stocks have been crushed in 2022 is understandable. Even those whose coupons are floating have suffered, even with the 3-month LIBOR up 450bps since late 2021.

While most preferreds and such funds I follow or am aware of are down over the past year, mREIT-issued ones have declined more. I think the concern here is how their issuers make money: lending long and borrowing short, while leveraging their assets. A flat or inverted yield curve doesn’t help. Here are a few samples of 1-year price movements.

seekingalpha.com price charts

Even the preferred from Morgan Stanley (MS), with its 4% floor, while better than the mREIT issues, is down almost 25%.

This article reviews the three preferred stocks available from AG Mortgage Investment Trust (MITT), along with MITT so readers understand the issuer. The preferreds are:

- 8.25% Series A Cumulative Redeem Preferred Stock (NYSE:MITT.PA)

- 8.00% Series A Cumulative Redeem Preferred Stock (MITT.PB)

- 8.00% Series C Fix/Float Cumul Redeem Prfd Stock (MITT.PC)

Understanding AG Mortgage Investment Trust

Seeking Alpha describes this mREIT as:

AG Mortgage Investment Trust, Inc. operates as a residential mortgage real estate investment trust in the United States. Its investment portfolio comprises residential investments, including non-qualifying mortgages loans, government-sponsored entity non-owner occupied loans, re/non-performing loans, land related financing, and agency residential mortgage-backed securities; and commercial investments. MITT started in 2011.

Source: seekingalpha.com MITT

MITT describes itself as:

AG Mortgage Investment Trust, Inc. (NYSE: MITT) is a residential mortgage REIT with a focus on investing in a diversified risk-adjusted portfolio of residential mortgage-related assets in the U.S. mortgage market. We are externally managed and advised by AG REIT Management, LLC, a subsidiary of Angelo, Gordon & Co., L.P., a leading privately-held alternative investment firm focusing on credit and real estate strategies.

Source: agmortgageinvestmenttrust.com/corporate-profile

The follow corporate data is drawn from the early November Quarterly Report PDF, starting with a statement from management:

Despite the continued themes of inflation, volatility and uncertainty, coupled with credit spread widening, our adjusted book value was down 4.2% for the third quarter,” said TJ Durkin, Chief Executive Officer. “We continued to execute our strategy of acquiring high quality, newly-originated Non-Agency Loans and we were disciplined and successful in terming out our warehouse financing into securitizations. This drove our strong liquidity position today and puts us in a position to play offense in volatile markets like this, as well as continue to invest excess capital into our common stock repurchase program.

Highlighted points about MITT and the prior quarter included:

- $11.02 Book Value per share as of September 30, 2022 compared to $11.48 as of June 30, 2022(1) $10.68 Adjusted Book Value per share as of September 30, 2022 compared to $11.15 as of June 30, 2022

- Decrease of (4.2)% from June 30, 2022 Quarterly economic return on equity of (2.3)%

- $(0.33) and $(0.03) of Net Income/(Loss) and Core Earnings per diluted common share, respectively

- $0.21 dividend per common share

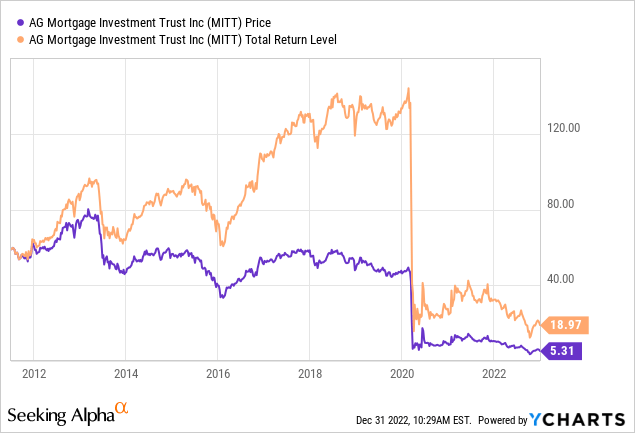

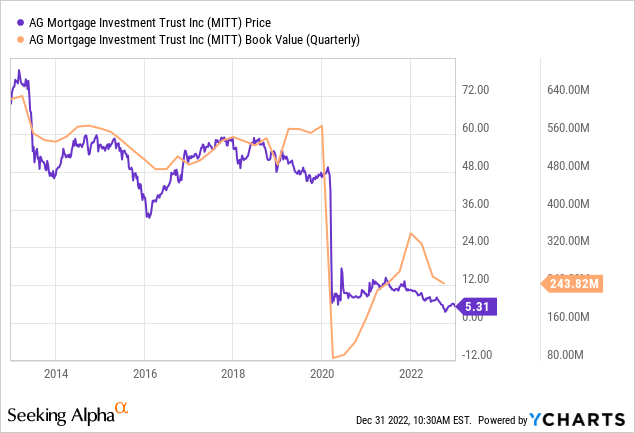

As for Book Value, it took a major hit when COVID hit, started recovering and is now suffering as the rise in short-term rates faster than long-term rates makes life tough on firms that borrow short and lend long.

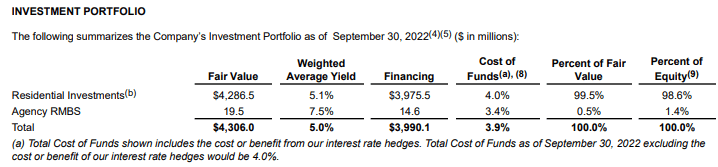

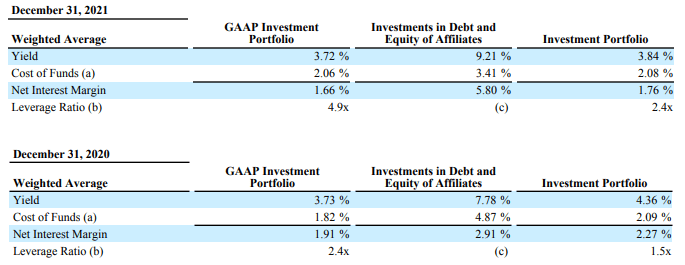

The report included this table that compare the portfolio yield versus its financing cost.

agmortgageinvestmenttrust.com

The net interest margin is 110bps. Compare that to the values at the end of the prior two years, based on the investment portfolio: 176bps on 12/31/21 and 227bps on 12/31/20.

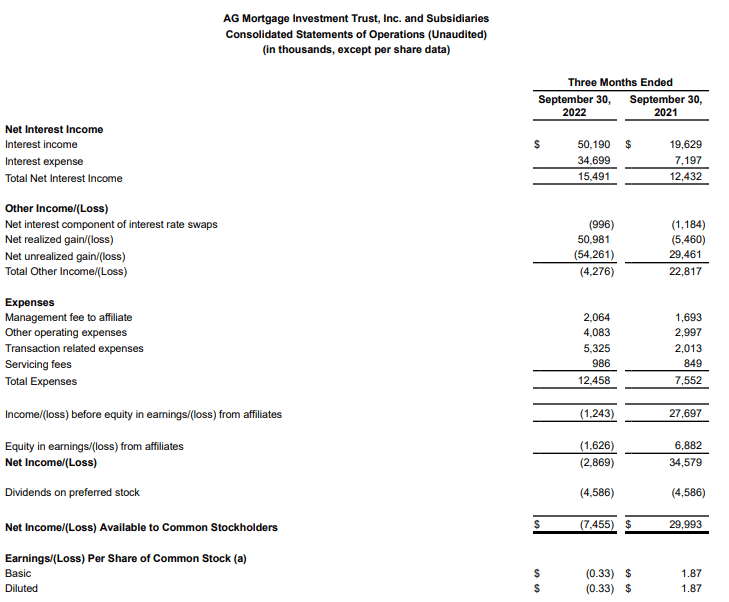

agmortgageinvestmenttrust.com

In under two years, a time when the yield curve moved up and flatten-to-inverted, the net interest margin has been cut in half! Not surprising, the Statement of Operations shows that negative effect.

agmortgageinvestmenttrust.com seekingalpha.com MITT DVDs

Distributions has been falling for almost a decade now and MITT did a 1-for-3 reverse split in July 2021. Accounting for that, payouts are down over 90% since their peak in 2013. Avisol Capital Partners recently published AG Mortgage Investment: A High Yielding Relatively Risky mREIT At A Risk-Adjusted Price, and gave MITT a HOLD rating.

Reviewing and comparing the preferreds

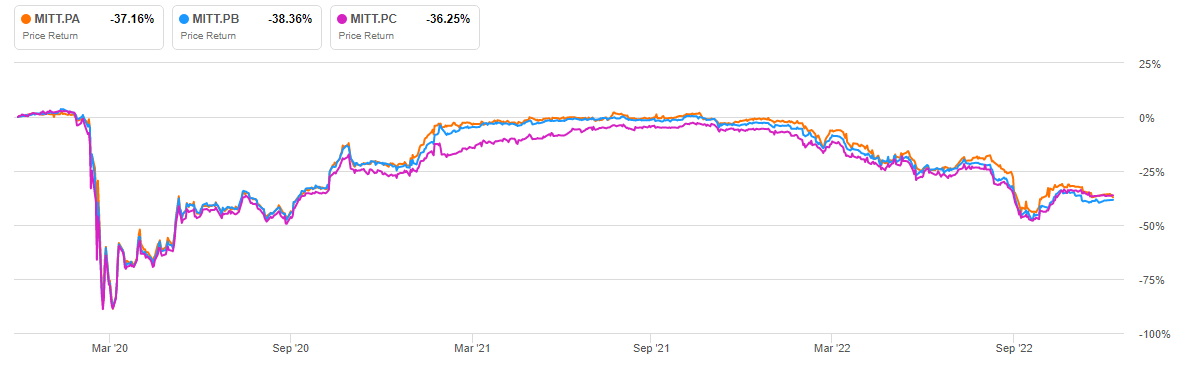

The three-year price charts are:

seekingalpha.com price charts

With dividends, the returns were about 20% better, but still double-digit negative. As expected, prices have been declining as the FOMC raised rates.

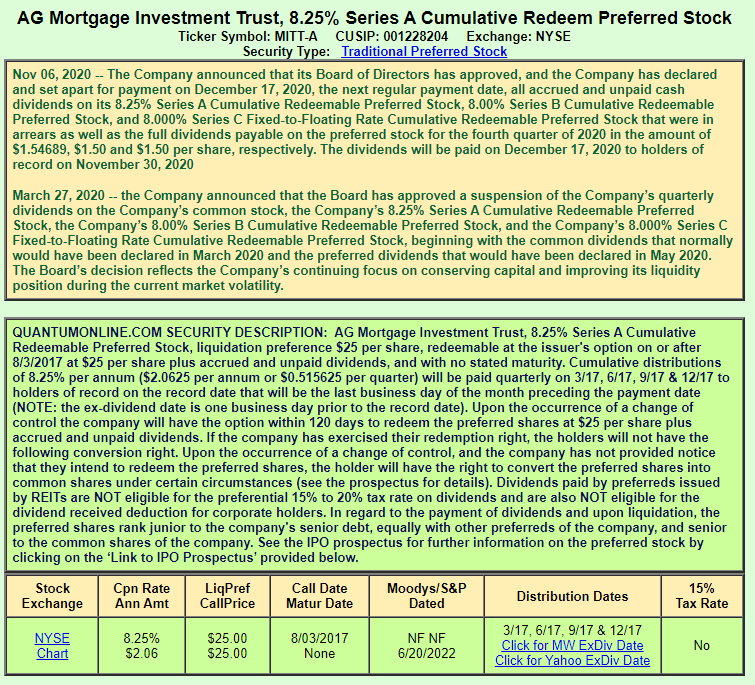

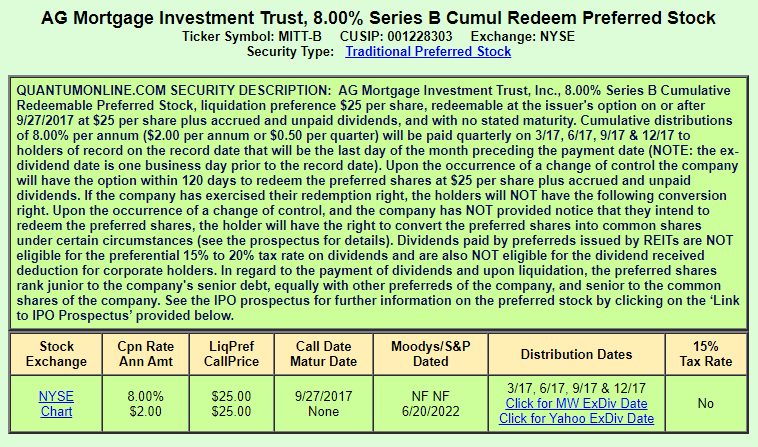

quantumonline.com MITT-A quantumonline.com MITT-B quantumonline.com MITT-C

Looking at the descriptions from QuantumOnline.com, one could get the impression that only “A” skipped a payment due to COVID, when in fact all three did, with “C” missing two payments that were made up in 12/20.

| Factor | “A” | “B” | “C” |

| Coupon | 8.25% | 8.00% | 8.00% |

| Coupon Type | Fixed | Fixed | F-2-F 3mLIBOR+6.476%** |

| Price | $16.04 | $15.64 | $16.75 |

| Yield | 12.86% | 12.79% | 11.94% |

| YTC | 37.63%* | 39.05% | 34.33% |

| Call Date | Past | Past | 9/17/24 |

* Both A & B are callable now, YTC assumes they are called on 9/17/24, like C.

** 3-mo LIBOR is 4.75% which would have coupon at 11.23%.

Possible action strategies

Before “C” becomes callable, “A” would be called before “B” since it has the higher coupon. After 9/17/24, “C” would most likely be called first if the LIBOR (or replacement rate) is above 1.77%; probably ahead of “B” if between 1.52% and 1.77%. At their current prices, I would hold “B over “A”. I would pass on “C” due to both its lower current yield and higher risk of being called first.

Portfolio strategy

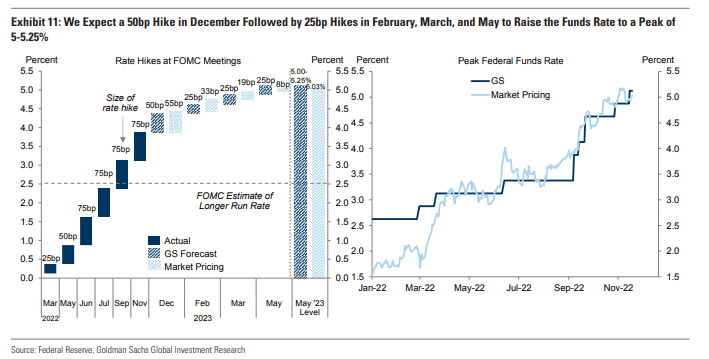

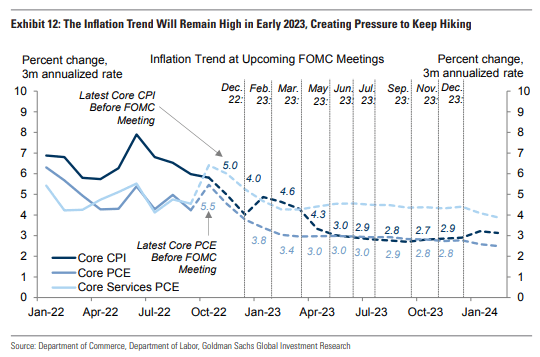

Before the December FOMC meeting, Goldman Sachs posted their economic forecast for 2023; whether they pushed up their estimates afterwards I could not find.

goldmansachs.com

As most forecasters are saying, they see the peak rate being reached next summer. They see three 25bps hikes next year raising the funds rate to a peak of 5-5.25%. Unlike the consensus, Goldman Sachs does not see a recession in 2023. The inflation forecast brings it close to the FOMC’s 2% target.

goldmansachs.com

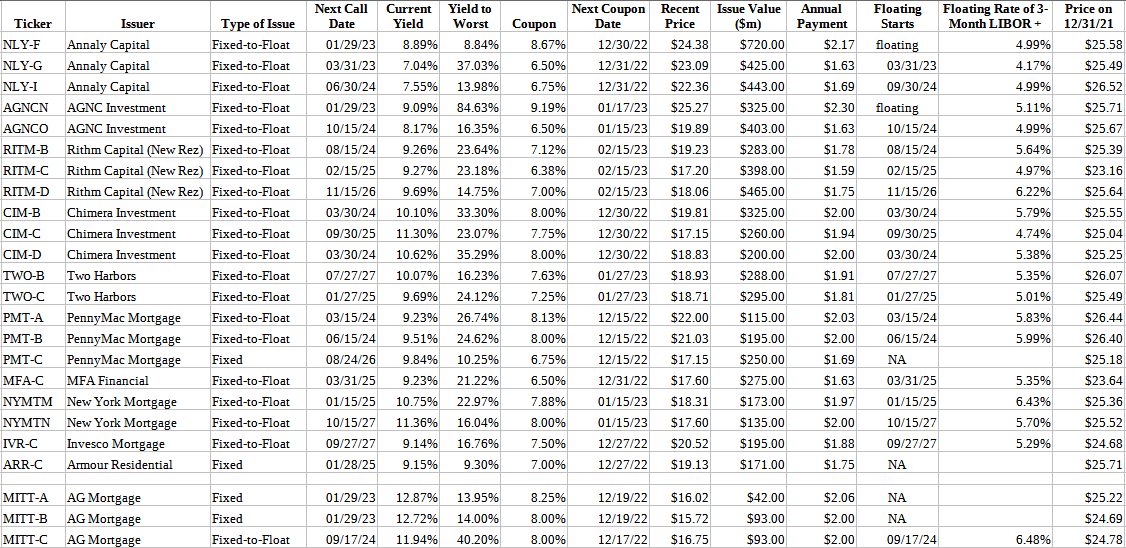

To know whether the MITT preferreds are “good investments”, one should compare them to other Residential mREIT preferreds. The next list includes all of those that the Hoya Capital Income Builder Preferred Income portfolio picks. I separated the three MITTs as they are not part of the portfolio.

Hoya Capital Income Builder

While the above is not presented as Buy recommendations as each investor has different goals, it is informative which issues are not included. The question each investor has to answer would be: “Is the 200-300bps extra yield offered by the MITT preferreds worth the possible extra risk?”.

Be the first to comment